Published on

December 24, 2025

Financial compliance in 2025 is undergoing major shifts. Key regulatory changes, enforcement deadlines, and evolving technologies like AI are reshaping how financial institutions operate. Here's what you need to know:

Compliance is shifting from checklists to outcome-focused strategies, emphasizing operational resilience and real-time monitoring. Institutions must modernize systems and integrate technology to stay ahead.

2025 Financial Compliance Statistics: Enforcement Actions, SAR Filings, and AI Adoption Rates

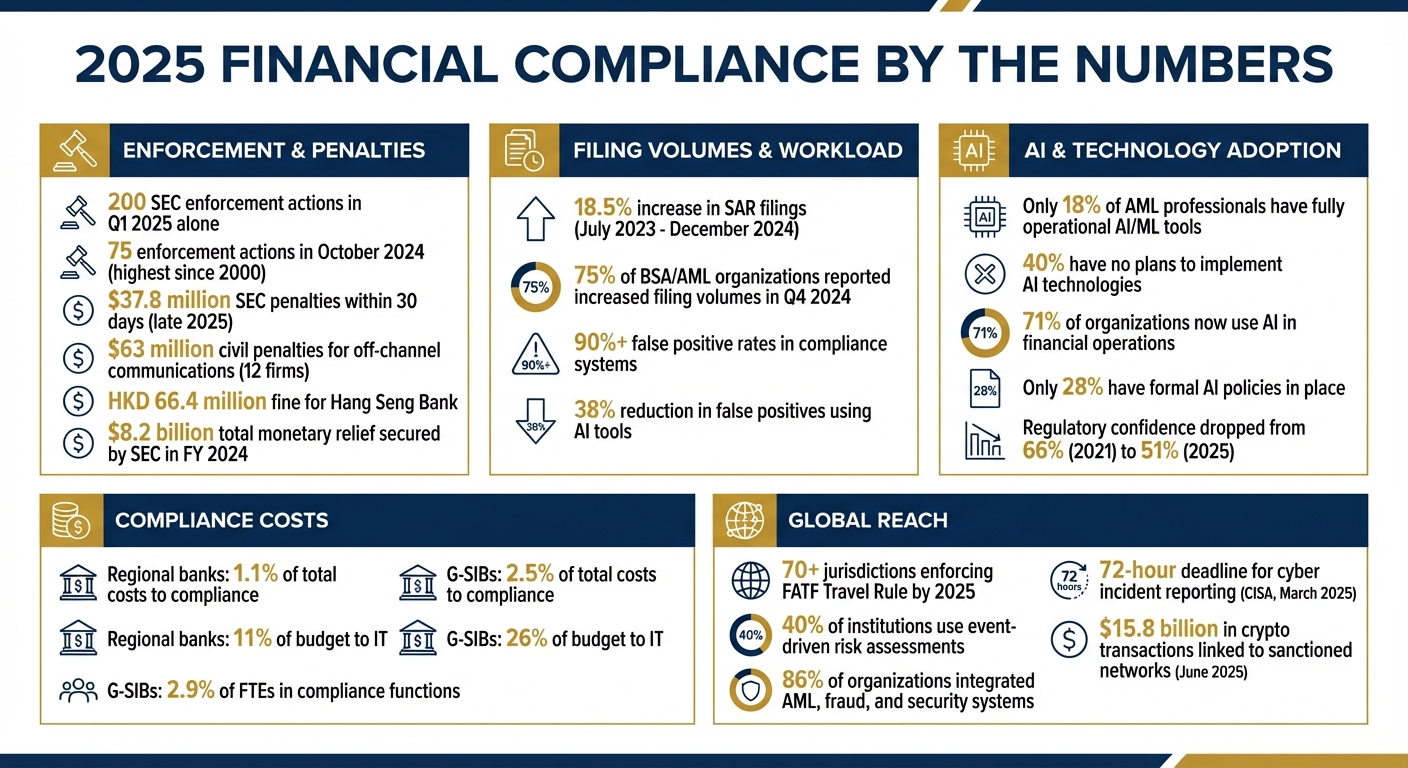

Regulators are ramping up enforcement efforts like never before. In fiscal year 2025, the U.S. SEC initiated 200 enforcement actions in just the first quarter, with 75 of those occurring in October 2024 alone - a pace unmatched since at least 2000. Sanjay Wadhwa emphasized the agency’s relentless stance during this period. Cases involving off-channel communications violations saw 12 firms collectively paying over $63 million in civil penalties. Similarly, Hang Seng Bank, Ltd. faced a hefty fine of HKD 66.4 million in early 2025 for missteps in selling investment products and failing to disclose monetary benefits over a nine-year span [3]. In late 2025, the SEC issued enforcement penalties totaling $37,812,859 within just 30 days [7]. While domestic regulatory pressure intensifies, global compliance standards continue to evolve, presenting a mix of both alignment and divergence.

On the global stage, financial compliance standards are taking two distinct routes. Some areas, like operational resilience, are witnessing alignment. The EU's Digital Operational Resilience Act (DORA), the UK's Operational Resilience requirements, and Australia's CPS 230 all share a focus on managing ICT risks. By 2025, over 70 jurisdictions are expected to enforce the FATF "Travel Rule", which governs virtual asset transfers [4][5].

However, when it comes to data privacy, significant differences remain. Brazil's LGPD mirrors aspects of the EU's GDPR, but notable gaps exist, such as differing interpretations of the "right to be forgotten." Meanwhile, India has implemented stringent data localization rules, mandating that personal financial data stay within its borders [2]. This lack of uniformity creates operational headaches for multinational firms, especially those that previously relied on centralized compliance systems. Adding to the complexity, the U.S. deregulatory approach under the Trump administration - marked by the "10 to 1" rule that repealed ten regulations for every new one - stands in stark contrast to the more stringent regulatory approaches seen in the UK and EU [5].

The changing landscape of enforcement has also reshaped how compliance is evaluated. Regulators are moving away from a formality-driven approach, focusing instead on whether controls are effective in practice.

"Regulators aren't just asking if you have controls - they're asking how well they actually work in practice. It's a shift from checkbox compliance to operational resilience." - Troy Huth, Senior Director of the BSA/AML Roundtable [6].

This shift forces institutions to rethink their strategies. Firms are now expected to deliver tangible results, such as ensuring uninterrupted critical services during crises or processing customer claims within 24 hours to meet compliance standards [2]. FinCEN data underscores this shift, with a reported 18.5% rise in SAR filings between July 2023 and December 2024. Additionally, 75% of BSA/AML Roundtable members noted a surge in filing volumes, prompting compliance teams to prioritize quality over quantity. Many are now leveraging AI-assisted tools to enhance the effectiveness of their investigations [6].

The fight against financial crime is entering a transformative phase. FinCEN and federal regulators now mandate that AML/CFT programs be "effective, risk-based, and reasonably designed" [9]. This means financial institutions must align their risk assessment processes with the latest government priorities for combating money laundering and terrorism financing.

Institutions are also grappling with operational pressures as filing requirements grow. To address this, the U.S. Treasury is exploring ways to simplify the SAR filing process, acknowledging the excessive documentation burden on institutions as of June 2025 [6]. Many organizations are turning to AI-powered tools to streamline data collection and reduce false positives - cutting them by as much as 38% [10].

Sanctions compliance has become an even faster-moving target. In June 2025, expanded U.S. sanctions uncovered $15.8 billion in cryptocurrency transactions linked to sanctioned shadow banking networks. Banks were required to adjust their systems and processes within just 72 hours [11].

"The surgical precision of these June designations... signals that financial institutions have days, not months, to adapt."

- Ravi de Silva, CEO of de Risk Partners [11]

Meanwhile, smaller community banks received some relief through the OCC’s new "Community Bank Minimum BSA/AML Examination Procedures", effective February 1, 2026. This program gives examiners discretion on transaction testing for low-risk banks. However, larger institutions face stricter requirements under new laws like the "End Banking for Human Traffickers Act of 2024", which demands enhanced training and monitoring to detect human trafficking transactions [6]. These shifts in AML practices are also driving tighter data privacy and cybersecurity standards.

The concept of operational resilience is replacing traditional business continuity planning as the new regulatory standard. The EU’s Digital Operational Resilience Act (DORA), which became fully enforceable in January 2025, is setting a global precedent by requiring critical services to stay functional during extreme stress or system failures [2]. Regulators now expect institutions to demonstrate their ability to withstand severe disruptions.

Data localization rules are another growing challenge for multinational firms. For instance, India’s strict regulations require personal financial data to remain within its borders. To comply, companies are adopting advanced data tagging systems to track where data resides [2].

Third-party risk management is also under the microscope. Regulators are calling for continuous, real-time monitoring of digital suppliers instead of relying on periodic checks. This shift has led to a significant integration of processes - 86% of organizations now report that their AML, fraud, and information security systems are interconnected, creating unified data ecosystems [10].

"The key to unlocking the full potential of AI and machine learning is integration of data sources, teams, and technology. The first step toward that integration is establishing a data ecosystem that combines data from all sources."

As data protection regulations tighten, institutions must also address the growing risks associated with AI.

AI is slowly making its way into compliance operations, but adoption remains limited. As of February 2025, only 18% of AML professionals reported having AI/ML tools fully operational, while 40% had no plans to implement these technologies [10]. Regulatory enthusiasm for AI has noticeably cooled - practitioner confidence in regulators supporting AI innovation dropped from 66% in 2021 to 51% in 2025. The percentage of those who see regulators as resistant to change more than doubled, rising from 6% to 13% [10].

A major focus for regulators is now on AI model explainability. A 2025 GAO report highlighted that "insufficient explainability in AI models can... inhibit a financial institution's understanding of a model's conceptual soundness and reliability, inhibit independent review and audit, and make compliance with laws and regulations more difficult" [12]. Federal agencies are increasingly aligning their guidance on model risk management with the NIST AI Risk Management Framework, which emphasizes trust, fairness, and transparency [12].

In practice, banks are deploying Generative AI cautiously, focusing on internal, low-risk applications like summarizing customer interactions, writing code, or searching legal documents rather than high-stakes decision-making [12]. Institutions investing in strong data management systems and fostering collaboration between technology, risk, and policy teams are setting themselves up for long-term success.

"Firms that press ahead with integrating data and operations with governance in mind are laying the groundwork for responsible innovation in AI and ML and will enjoy a competitive advantage over those who hesitate."

- Stu Bradley [10]

Community banks are getting some relief with the OCC's new "Community Bank Minimum BSA/AML Examination Procedures." Starting February 1, 2026, this applies to banks with assets up to $30 billion, simplifying certain compliance requirements. Meanwhile, credit unions are seeing changes too. The NCUA has removed "reputation risk" from its supervision program, allowing examiners to rely on conclusions from prior examination cycles for areas like training and BSA compliance officer evaluations. This shift lets credit unions focus more on combating fraud and scams, an increasingly pressing issue as digital banking continues to grow [8][13]. While traditional institutions adjust to these updates, tech-driven sectors are grappling with entirely different hurdles that call for quick and creative solutions.

Digital asset platforms are facing tough challenges with identification. Decentralized wallets and multiple blockchains make tracking transactions tricky [16]. Payment processors, on the other hand, are navigating the shift to instant payments by adopting real-time monitoring systems. This includes implementing "flow-through-of-funds" rules to catch red flags like immediate withdrawals after deposits - often a sign of fraud [6]. However, the sheer volume of transactions can lead to a flood of false positives, which can obscure genuinely suspicious activities [16].

Regulation is also evolving. Cryptocurrencies are increasingly being treated like traditional currencies for AML compliance, creating a new layer of oversight that requires specialized risk assessments. For instance, one cryptocurrency exchange agreed to a $100 million settlement with FinCEN and the CFTC in 2024 due to lapses in due diligence and suspicious transaction reporting [15]. Additionally, 40% of financial institutions now base their risk assessments on significant behavior changes or negative news alerts, rather than sticking to static, scheduled reviews [6]. These shifts highlight the dynamic nature of compliance in the digital finance space and point to significant changes ahead for investment advisers.

Investment advisers are gearing up for a major regulatory shift. Starting January 1, 2026, FinCEN will classify SEC-registered investment advisers (RIAs) and exempt reporting advisers (ERAs) as "financial institutions" under the Bank Secrecy Act. This means they'll need to roll out full AML/CFT programs, file Suspicious Activity Reports, and adhere to recordkeeping and travel rules. Non-compliance could lead to penalties of up to $5,000 per violation [14].

The SEC is also cracking down on misleading claims about AI in investment strategies, a practice known as "AI washing." In FY 2024, the SEC secured $8.2 billion in total monetary relief, with over $600 million tied to enforcement actions involving unauthorized communication channels [18]. The agency is expanding its data analytics capabilities to spot issues like cherry-picking and unfair trade allocations by financial advisors [18].

"As AI becomes more popular in the investing space, we will continue to be vigilant and pursue those who lie about their firms' technological capabilities and engage in 'AI washing.'"

- Co-Chief of the SEC's Asset Management Unit [18]

Looking ahead, the SEC's Spring 2025 agenda includes proposals to update custody regulations for client assets, with a focus on digital and crypto holdings. To prepare, investment advisers should start setting up identity verification systems now, as the Customer Identification Program (CIP) rule is expected to take effect in April 2026 [17].

Fragmented compliance systems are becoming a thing of the past. Financial institutions now need a unified risk framework that not only meets regulatory demands but also aligns with broader business goals. This shift encourages organizations to move beyond reactive, siloed approaches toward a "compliance-by-design" model - where regulatory requirements are seamlessly embedded into everyday workflows [19][5].

Today, compliance teams face daunting challenges, including false positive rates exceeding 90% [19]. However, institutions embracing alert automation have seen their Level 1 handling speeds triple [19]. The focus is on building systems that provide a single, real-time view of customer interactions across all channels, enabling institutions to trace customer relationships instantly [2].

"The ability to comply with regulatory requirements has become a key source of competitive advantage for financial institutions." - Boston Consulting Group [2]

Real-time monitoring is no longer optional. With instant payments taking center stage, compliance processes must now operate in seconds, not days [2]. This shift demands architectural updates that can handle automated data reconciliation and provide rapid responses to regulatory inquiries. As institutions adapt to meet these real-time demands, they must also carefully plan their compliance budgets to balance innovation with cost-efficiency.

Compliance costs vary widely depending on the size of the institution. Regional banks typically allocate about 1.1% of their total costs to second-line-of-defense compliance, while global systemically important banks (G-SIBs) spend as much as 2.5% [19]. IT investments also differ - regional banks dedicate a median of 11% of their budgets to IT, compared to 26% for G-SIBs [19].

But spending more doesn’t always guarantee better compliance. The key lies in making smarter investments. Before diving into advanced AI tools, institutions should focus on optimizing existing processes and fixing broken workflows. Automating inefficiencies only compounds problems [19].

The compliance workforce is also undergoing significant changes. G-SIBs now allocate around 2.9% of their total full-time employees to compliance functions [19]. The trend is shifting toward professionals with hybrid skills - those who combine legal expertise with data analytics. This blend of capabilities helps institutions navigate the complexities of cross-border regulations while managing costs effectively.

For growth-stage companies, the challenge is clear: how to build enterprise-level compliance systems without breaking the budget. Phoenix Strategy Group specializes in creating tailored solutions that integrate compliance into daily operations while keeping costs manageable.

Their tools, such as the Weekly Accounting System and Monday Morning Metrics, deliver the real-time monitoring that regulators now expect. These systems go beyond periodic reviews, offering continuous visibility into compliance processes. Their Integrated Financial Model further helps companies accurately forecast compliance expenses and plan for regulatory changes without disrupting growth.

For businesses preparing for fundraising or mergers and acquisitions, Phoenix Strategy Group ensures compliance architecture scales alongside business growth. With automated reconciliation frameworks and fractional CFO services, they help leadership teams see compliance not as a cost burden but as a strategic advantage that supports long-term success.

By 2025, compliance has evolved from simple checklists to a focus on operational resilience. Regulators now expect firms to demonstrate that their controls can withstand real-world stress scenarios[2][6]. With instant payments becoming the norm, sanctions screening and fraud detection must work within seconds rather than days[2]. Between July 2023 and December 2024, SAR filings rose by 18.5%, with 75% of BSA/AML organizations reporting increased volumes in Q4 2024. Automated systems are stepping up to handle routine cases, freeing analysts to focus on more complex challenges and positioning institutions for long-term success[6].

AI governance has become a pressing issue, as only 28% of organizations currently have formal AI policies in place[22]. In January 2025, FINRA’s Annual Regulatory Oversight Report introduced new sections addressing the risks tied to AI in communications and Regulation Best Interest[20][1]. With 71% of organizations now using AI in financial operations[21], the gap between widespread adoption and adequate oversight is becoming a significant regulatory concern.

These trends highlight the need for practical strategies that future-proof compliance efforts.

To keep pace with these changes, firms need to embrace strategic automation and integrated systems. For growing companies operating on tight budgets, building enterprise-level compliance frameworks is no longer optional. A good starting point is modernizing data architecture to support automated reconciliation, as regulators increasingly expect instant, accurate responses to their requests[2]. Additionally, more institutions (40% of those surveyed) are now adopting event-driven risk assessments based on behavioral changes, moving away from traditional scheduled reviews[6].

"Regulators aren't just asking if you have controls - they're asking how well they actually work in practice. It's a shift from checkbox compliance to operational resilience." - Troy Huth, Senior Director, BSA/AML Roundtable [6]

This shift underscores the need for systems that offer a unified view of each customer across all business lines. Incorporating tools like XBRL into reporting processes can eliminate manual steps and improve efficiency[21][2].

Firms that treat compliance as a strategic advantage rather than a cost burden will lead the way. For companies preparing for fundraising or exits, demonstrating scalable and robust compliance frameworks is essential. Phoenix Strategy Group exemplifies this approach by embedding compliance monitoring into tools like the Weekly Accounting System and Monday Morning Metrics. Their Integrated Financial Model not only forecasts costs but also ensures compliance systems are aligned with scalable business growth. By doing so, they position compliance as a driver of growth while meeting the real-time demands of 2025 regulations.

The EU's Digital Operational Resilience Act (DORA) is poised to reshape how global financial institutions handle digital risks. This regulation introduces stricter guidelines, requiring robust IT security systems, continuous risk monitoring, and improved incident reporting processes. The goal? To safeguard financial stability and bolster defenses against cyber threats.

For U.S.-based institutions operating internationally, especially those engaged with EU markets or entities, meeting DORA’s standards could mean adjusting existing practices. Proactively aligning with these requirements not only helps maintain trust but also reduces the risk of regulatory penalties.

Implementing AI in financial compliance isn't without its hurdles. One major obstacle is the fact that regulatory frameworks haven’t fully adapted to AI advancements. This creates uncertainty about how existing rules apply to autonomous systems, making it tricky for companies to develop AI tools that meet compliance standards. On top of that, challenges like bias, poor data quality, and lack of transparency can erode trust and attract regulatory attention.

From a technical standpoint, integrating AI into older, legacy systems is no small feat. It demands reliable data pipelines, real-time monitoring capabilities, and stronger cybersecurity defenses. Many businesses also face a shortage of in-house expertise and resources to keep up with the fast-moving world of AI. When companies turn to third-party AI vendors, the situation becomes even more complicated, as regulators often have limited oversight over external providers.

To tackle these issues, businesses frequently turn to specialized advisors. For example, Phoenix Strategy Group helps growth-stage companies by creating AI-driven compliance frameworks, ensuring data accuracy, mitigating model risks, and aligning AI projects with evolving U.S. compliance standards.

Multinational companies face a tough landscape when it comes to navigating data privacy laws across more than 160 jurisdictions. Each region has its own unique rules for handling personal data, obtaining consent, and enforcing compliance. What works in one country might break the law in another, forcing businesses to create region-specific policies instead of a single, unified global strategy.

One of the biggest hurdles is managing cross-border data transfers. Take GDPR’s Standard Contractual Clauses or data localization requirements, for example - these add layers of legal complexity and can slow down operations significantly. Then there’s the issue of varying timelines for consent and breach notifications. GDPR requires breaches to be reported within 72 hours, while many U.S. states allow up to 30 days. This means companies need real-time monitoring systems and automated reporting tools to stay compliant everywhere. On top of that, detailed data mapping, impact assessments, and regular audits drive up operational costs and demand seamless collaboration between finance, IT, legal, and risk management teams.

To tackle these challenges, many growth-stage companies partner with experts like Phoenix Strategy Group. By combining cutting-edge technology with deep regulatory knowledge, Phoenix helps businesses simplify their data privacy frameworks, automate compliance, and align privacy practices with their broader financial goals - turning what could be a liability into a strategic advantage.