Published on

June 6, 2026

Credit ratings and capital structure are deeply connected, shaping how companies secure funding and manage financial risks. Here's what you need to know:

Credit ratings are more than just financial scores - they influence how companies plan, grow, and secure funding. By understanding these dynamics, businesses can make smarter decisions about their financial strategies.

Credit Ratings & Capital Structure: Key Metrics by Rating Category

Credit ratings serve a dual purpose: they not only reflect a company's financial standing but also shape its ability to secure financing and the terms that come with it.

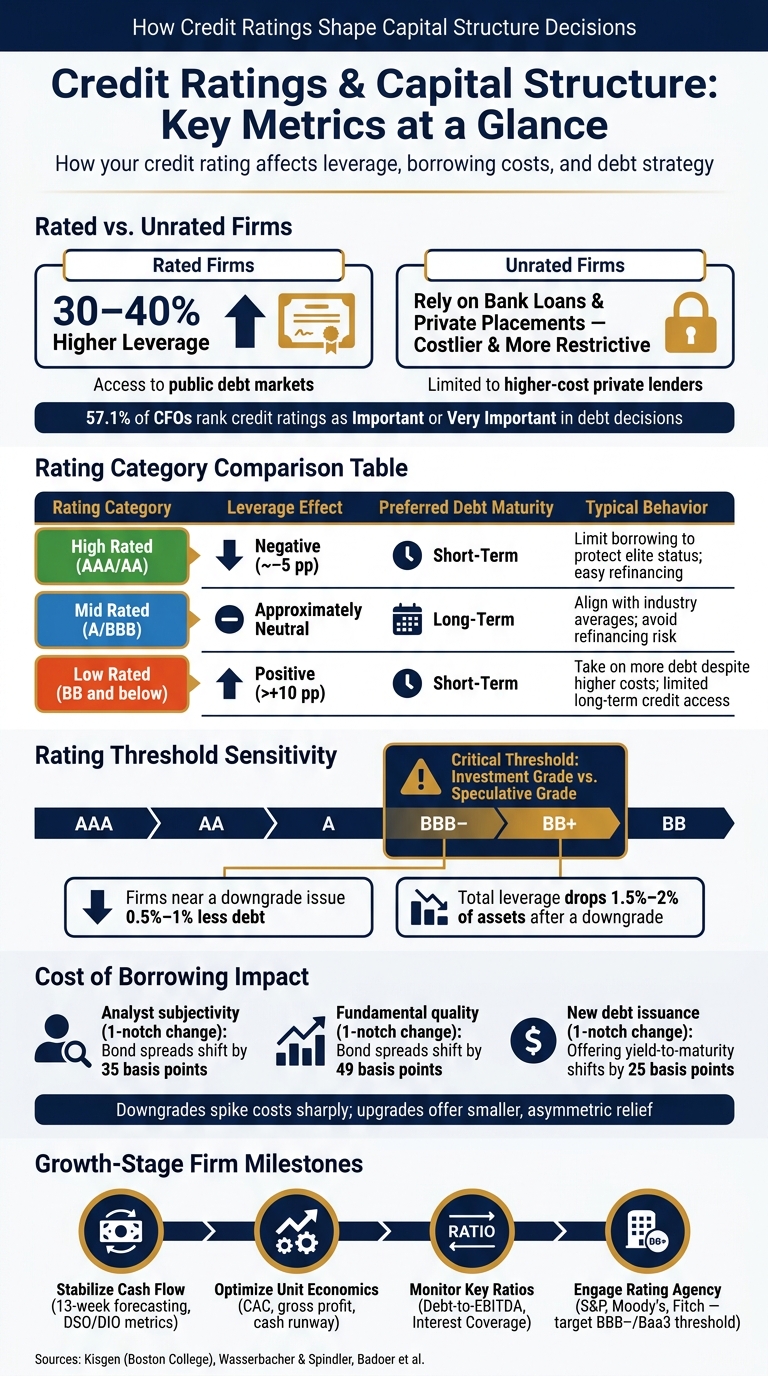

When comparing firms with and without credit ratings, the differences are striking. Rated firms tend to have leverage levels that are 7–9 percentage points higher, translating to a 30%–40% increase compared to the average leverage of unrated firms [6]. Why? A credit rating acts as a trusted signal of financial health, reducing uncertainty for lenders and investors. This opens the door to public bond markets, which often offer more favorable terms. On the flip side, unrated firms usually turn to bank loans or private placements, which are typically more restrictive and come with steeper costs [6].

The effect of credit ratings on leverage also depends on the rating itself. Here’s how it breaks down:

| Rating Category | Effect on Leverage | Typical Behavior |

|---|---|---|

| AAA / AA | Negative (around −5 percentage points) | Firms limit borrowing to maintain their elite status |

| A / BBB | Approximately neutral | Leverage aligns with industry averages |

| BB and below | Positive (more than +10 percentage points) | Firms take on more debt despite higher borrowing costs |

Source: Wasserbacher & Spindler [6]

Investment-grade companies (those rated BBB− or higher) often use their strong ratings to signal financial quality, which reduces their need to rely heavily on debt. Speculative-grade firms (rated BB+ or lower), however, often face capital constraints and rely more on debt, even though this comes with steeper borrowing costs [6][7]. The investment-grade boundary, particularly the BBB− to BB+ threshold, is a critical marker. Falling below this line can limit access to certain institutional investors, such as banks that are legally required to hold only investment-grade bonds [6][1].

These dynamics highlight how firms actively manage their leverage to navigate these crucial rating boundaries.

Managing leverage becomes even more deliberate when firms approach key rating thresholds. This behavior aligns with the Credit Rating-Capital Structure (CR-CS) hypothesis, which suggests that companies treat credit ratings as a core factor in their capital structure decisions. Crossing a rating boundary can lead to tangible financial consequences, making proactive management essential [2].

Firms with ratings near a downgrade or upgrade notch (like A− or BBB−) are particularly cautious. Research by Darren J. Kisgen from Boston College sheds light on this:

"Firms near a credit rating upgrade or downgrade issue less debt relative to equity than firms not near a change in rating." [2]

These firms reduce their debt issuance by about 0.5% to 1% and lower their total leverage by 1.5% to 2% of assets after a downgrade [2][6]. This cautious approach reflects Prospect Theory, which suggests that the fear of losing a rating notch outweighs the perceived benefit of gaining one.

Real-world cases illustrate this behavior. In December 2002, Fiat sold a stake in one of its business units to avoid a potential credit downgrade [2]. Similarly, in May 2004, US Airways faced immediate financing withdrawals for its regional jets after a downgrade triggered a contract clause [2].

For companies navigating growth, understanding these credit-rating dynamics is essential. Partnering with seasoned advisors - like those at Phoenix Strategy Group - can help align capital structure strategies with shifting rating thresholds.

Up next, we’ll explore how these leverage dynamics impact the cost of debt.

A company's credit rating has a direct impact on how much it costs to borrow money. Higher ratings mean lower borrowing costs, as investors demand smaller spreads over benchmarks like U.S. Treasury yields. However, when a credit rating drops, borrowing costs can rise sharply - and these changes are rarely balanced in both directions.

When a company’s credit rating is downgraded, borrowing costs can spike significantly. On the other hand, upgrades don’t necessarily bring an equivalent reduction in costs [1]. After a downgrade, companies often act quickly to adjust their capital structures and manage the rising expenses. In contrast, they tend to be less reactive when their ratings improve. This uneven market response has immediate implications for pricing.

The credibility of the rating itself also plays a role. If investors believe that an issuer-paid rating is overly optimistic compared to independent benchmarks, they demand higher yields to offset the perceived risk:

"Investors question the quality of issuer-paid ratings and raise corporate bond yields where the issuer-paid rating is more positive than benchmark investor-paid ratings." - Dominique C. Badoer, Cem Demiroglu, and Christopher M. James [8]

This phenomenon, often referred to as the "lemons discount," can drive some companies to avoid public bond markets altogether. Instead, they may turn to bank loans, where lenders provide closer monitoring and offer a more reliable signal of risk [8]. These cost dynamics highlight the importance of growth-stage firms carefully managing their credit ratings.

For growth-stage companies, maintaining the right credit rating is a delicate balancing act. While the tax benefits of debt are valuable, the costs of financial distress can’t be ignored. As Hayne E. Leland and Klaus Bjerre Toft explain:

"The tax advantage of debt must be balanced against bankruptcy and agency costs in determining the optimal maturity of the capital structure." [4]

Take Exxon Mobil as an example. The company has shown how managing the trade-off between maintaining a high credit rating and achieving optimal leverage can be a key part of its strategy [9]. For growth-stage firms, however, this challenge is even more pronounced. These companies often have fewer tangible assets, higher asset risk (measured by asset betas), and face steeper costs if they encounter financial trouble - all of which push their optimal leverage point lower [9].

Additionally, as leverage increases, the cost of borrowing rises steeply. For every dollar of added interest expense, borrowing costs escalate further, with a slope of 4.81 in cost curves [9]. By actively managing their proximity to critical rating thresholds, growth firms can significantly lower their financing costs over time.

Researchers use several methods to measure how credit ratings affect borrowing costs. Panel regressions with fixed effects help separate the subjective influence of analysts from a firm’s actual fundamentals. For instance, a one-notch change due to analyst subjectivity can shift bond spreads by 35 basis points, while a one-notch change based on fundamental credit quality moves spreads by 49 basis points [10]. For newly issued public debt, an analyst-driven change of one notch can alter the offering yield-to-maturity by 25 basis points [10].

Other approaches include event studies, which track immediate changes in bond prices and credit spreads following a rating announcement, and partial adjustment models, which measure how firms gradually adjust their leverage ratios to align with a target after a rating change [1]. These methods consistently show that companies actively managing their ratings can achieve measurable savings on financing costs. This underscores the importance of thoughtful planning when it comes to capital structure decisions.

Credit ratings play a major role in shaping not just the cost of borrowing but also how firms approach their financing strategies. Whether a company opts for straight debt, convertible bonds, or equity often hinges on its current credit rating and where it's headed.

When a firm is close to a credit rating threshold, its financing decisions become more cautious, going beyond just managing leverage. The choice of securities - debt versus equity - becomes a critical factor. Darren J. Kisgen from Boston College highlights this in his research:

"Firms near a change in credit rating issue (retire) annually up to 1.5% less debt relative to equity as a percentage of total assets than firms not near a change, reflecting managers' desire to obtain upgrades and avoid downgrades." - Darren J. Kisgen, Professor of Finance, Boston College [11]

This means companies near a rating change issue or retire 1.5% less debt compared to equity, with avoiding a downgrade being a far stronger motivator than trying to achieve an upgrade [1][3].

The stakes of a downgrade are high. Firms may lose access to the commercial paper market, face mandatory bond buybacks, or deal with higher coupon rates. These risks push many companies to lean toward equity issuance to sidestep a downgrade [5]. For firms with speculative-grade ratings, a change in rating sends a strong signal to the market about their financial health, which can lead to even more dramatic shifts in financing preferences [3].

These shifts in security choice also influence how firms manage the maturity of their debt, as discussed below.

Beyond choosing between debt and equity, firms also adjust the maturity of their debt based on their credit rating. The relationship between ratings and debt maturity forms an inverted U-shape: firms with very high or very low ratings often prefer short-term debt, while those in the middle range (A to BBB) lean toward longer maturities [13].

Downgrades can also activate "rating triggers" in loan agreements, forcing immediate repayment or limiting access to short-term liquidity options like commercial paper [5][12]. To prepare for such scenarios, firms often restructure their debt proactively when a downgrade seems likely.

| Rating Category | Preferred Debt Maturity | Primary Driver |

|---|---|---|

| High Rated (AAA/AA) | Short-Term | Easy refinancing; low market risk [13] |

| Mid-Rated (A/BBB) | Long-Term | Avoiding refinancing and liquidity risks [13] |

| Low Rated (BB and below) | Short-Term | Limited access to long-term credit [13] |

The pecking order theory suggests that firms prioritize funding sources in this order: internal funds first, then debt, and finally equity. Equity is generally a last resort since issuing it can signal that a company's stock is overvalued. However, credit ratings can override this traditional hierarchy. When a firm is on the verge of a downgrade, even low-cost debt could push it over the edge, leading managers to skip debt issuance entirely in favor of equity - even though equity is more expensive [11].

Survey results show that 57.1% of CFOs consider credit ratings to be "important" or "very important" when deciding on debt levels [1]. Behavioral studies using Prospect Theory reveal that managers view downgrades as losses that feel worse than the gains associated with upgrades [5]. This fear of losses often drives firms toward more conservative financing choices, favoring equity when ratings come under pressure.

For companies in their growth stage, credit ratings play a pivotal role. As businesses expand, pursue institutional debt, or prepare for major capital raises, the structure of their balance sheet becomes a key focus for both lenders and rating agencies. This raises an important question: when is the right time to seek a credit rating?

The ideal moment to pursue a credit rating is once a company has reached financial stability and operational scalability. Agencies like S&P, Moody's, and Fitch assess factors such as revenue consistency, profitability, debt levels, and capital ratios to determine the likelihood of timely debt repayment [14]. These evaluations are forward-looking, placing significant weight on management quality and future business prospects [14].

A practical milestone is when a company is seeking growth capital between $2 million and $10 million, or is 12 to 24 months away from a liquidity event [15]. At this stage, having clean financial records and scalable operations becomes critical. Rating agencies will compare the company against its industry peers, and any shortcomings - like gaps in financial reporting or heavy dependence on founder leadership - will stand out [14][15].

"Capital structure is not just a finance decision. It is a signal of how management views risk, growth, and the future of the business." - Corporate Finance Explained [16]

Preparation starts with building a solid financial foundation well before engaging with rating agencies. One key step is stabilizing cash flow. Using tools like 13-week forecasting and risk-adjusted metrics (e.g., Days Sales Outstanding or Days Inventory Outstanding) can demonstrate a company’s ability to meet debt obligations consistently [15]. Meeting investment-grade thresholds - such as BBB− for S&P and Fitch or Baa3 for Moody's - requires monitoring critical ratios like Debt-to-EBITDA and Interest Coverage [14][15].

Another focus area is unit economics. Metrics like Customer Acquisition Cost (CAC), lifetime gross profit, and cash runway offer insights into long-term business sustainability. Companies that audit their SaaS expenditures or optimize cloud costs often report savings of 20–30% and 15–20%, respectively, by connecting these expenses to unit economics and leveraging real-time data [15].

By establishing robust internal systems, companies set the stage for leveraging expert advisory services to refine their capital structure strategies.

Given the financial impact of credit ratings, expert advisory support can be invaluable. Many growth-stage companies lack the internal expertise needed to navigate the complexities of credit rating preparation. This is where fractional CFO services and advanced FP&A (Financial Planning and Analysis) tools come into play.

Phoenix Strategy Group specializes in helping growth-stage companies align their capital structures with rating objectives. They provide financial modeling, streamlined reporting, and fractional CFO services, treating financial infrastructure as the foundation for growth. Their approach ensures that cash flow forecasting, leverage monitoring, and comprehensive reporting systems are in place before evaluations by rating agencies or institutional lenders [15].

Our analysis highlights how credit ratings play a crucial role in shaping capital structure strategies. They influence how companies manage their debt, with over half of financial managers ranking credit ratings as a major consideration in their decisions [1].

Notably, rating downgrades often have more severe consequences than upgrades. They lead to wider credit spreads, stricter covenants, and tougher financing conditions. Research by Kisgen shows that managers tend to scale back debt issuance when their companies are close to a potential rating change [2].

For growth-stage companies, particularly those following a "prospector" strategy - focused on innovation and high-risk ventures - lower credit ratings are common. This is largely due to unpredictable cash flows and a reliance on intangible assets [17]. It's important for firms to align their capital structure with their risk profile rather than solely relying on current financial metrics. This reinforces earlier discussions on how leverage decisions and financing strategies are influenced by rating constraints.

To treat credit ratings as a strategic tool, companies should focus on monitoring leverage thresholds, maintaining strong governance, ensuring financial transparency, and stress-testing liquidity under potential downside scenarios. As Zac Nesper, Former Treasurer at HP, wisely observed:

"Ratings are partly quantitative (leverage, coverage, cash flow), but the qualitative overlay (management credibility, financial policy clarity, willingness to engage) matters enormously." [18]

For growth-stage firms, disciplined financial reporting and proactive communication with lenders are essential for using credit ratings to their advantage. Partnering with expert advisors, such as Phoenix Strategy Group, can help ensure that financial systems remain resilient, aligning credit rating objectives with long-term growth ambitions.

Maintaining an investment-grade rating hinges on specific financial ratios that signal a company’s creditworthiness. Two critical ones are the interest coverage ratio, which measures the ability to cover interest payments, and the leverage ratio, which evaluates the balance between debt and equity. Beyond these, rating agencies also consider factors like cash flow, profitability, and financial flexibility. Phoenix Strategy Group supports growth-stage businesses in managing these essential metrics by offering FP&A and fractional CFO services, helping ensure the financial stability needed to achieve and maintain desired credit ratings.

Companies looking to balance growth spending with reduced downgrade risks might consider equity financing or hybrid options like convertible notes instead of piling on additional debt. When firms are on the verge of a credit downgrade, they typically shift away from heavy debt reliance to safeguard their ratings. Phoenix Strategy Group specializes in helping businesses fine-tune their funding strategies, ensuring they maintain enough liquidity for growth while keeping fixed obligations in check to protect their credit standing.

Obtaining a first-time credit rating can open doors to better access to capital, lower borrowing costs, and a broader range of institutional investors. For companies without a credit rating, securing one can help bridge the information gap, enhance debt capacity, and fuel growth opportunities. Phoenix Strategy Group specializes in guiding growth-stage companies through these critical decisions and preparing them for the credit rating process. This is particularly important for firms nearing investment-grade status, as achieving this level can significantly improve liquidity and financing options.