Published on

March 21, 2026

When navigating cross-border mergers and acquisitions (M&A), understanding notification triggers is crucial to avoid penalties, delays, or legal issues. These triggers, such as transaction value, company size, and market share, determine whether filings with regulators are required. For 2026, here are the key points:

Failing to meet requirements can result in fines, such as $53,088 per day for HSR violations or $5 million per violation under CFIUS rules. Early compliance assessments and expert guidance are essential to streamline multi-jurisdictional filings and avoid complications.

When planning a cross-border acquisition, three key factors determine whether regulatory notifications are required: transaction value, company size, and market share. Each jurisdiction applies these criteria differently to safeguard competition and prevent monopolistic practices. A clear understanding of these rules can help avoid compliance missteps and align strategies with regulatory expectations.

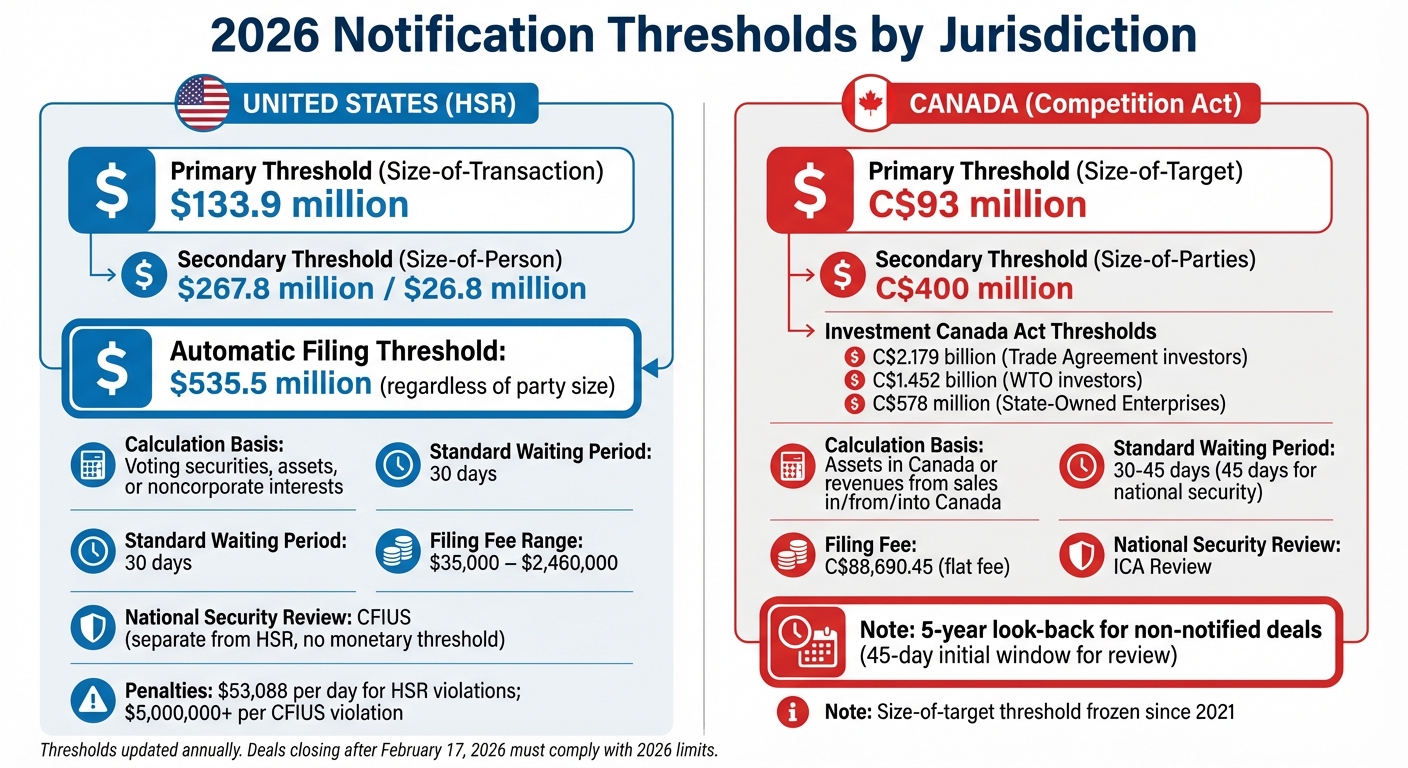

Transaction value is often the first hurdle. In the U.S., deals worth over $535.5 million automatically require notification, regardless of the parties' sizes [2]. For deals between $133.9 million and $535.5 million, the additional "Size-of-Person" test determines whether filing is necessary [2][6]. Transactions below $133.9 million are generally exempt from reporting under the Hart-Scott-Rodino (HSR) Act.

Canada takes a different approach. Under the Competition Act, the "size-of-target" threshold for 2026 is set at C$93 million in assets or gross revenues from sales in, from, or into Canada. This threshold, frozen since 2021, aims to capture more transactions for review [3]. Meanwhile, the Investment Canada Act (ICA) imposes higher thresholds: C$2.179 billion for Trade Agreement investors, C$1.452 billion for WTO investors, and C$578 million for state-owned enterprises [3].

Filing fees also vary widely. In the U.S., fees range from $35,000 for smaller transactions to $2.46 million for deals exceeding $5.869 billion [2][4]. Canada’s Competition Act filings carry a flat fee of C$88,690.45, while ICA notifications do not incur any fees [3].

The next layer of complexity comes from company size requirements.

Even when a transaction surpasses the value threshold, the size of the parties involved plays a role in determining whether notification is required. In the U.S., the "Size-of-Person" test applies to deals valued between $133.9 million and $535.5 million. Here, one party must have at least $267.8 million in total assets or annual net sales, while the other must meet a $26.8 million threshold [2][6]. For non-manufacturing entities, the net sales threshold rises to $267.8 million [2].

"HSR notification filings involve complex rules regarding valuation and exemptions that change regularly, and noncompliance with the Act carries serious penalties." – Christopher Abbott, Jacob Friedman, and Colleen M. Reddan, Jenner & Block [2]

In Canada, the Competition Act requires a "size-of-parties" test, which mandates combined assets or revenues of at least C$400 million. This threshold has remained unchanged since 1986 [3].

State-level regulations can introduce additional challenges. For example, Colorado and Washington have enacted "Baby HSR" laws. These laws trigger notifications for transactions involving approximately $26.78 million in in-state sales, roughly 20% of the federal threshold, potentially requiring state filings even when federal requirements are met [7].

Finally, market concentration adds another layer of scrutiny.

Regulators also evaluate market concentration to ensure that deals don't harm competition. Their goal is to block transactions that could "prevent or lessen competition substantially" [3]. During the notification period, agencies assess potential anticompetitive effects before allowing the deal to close [7].

In cases where concerns arise, U.S. regulators may issue a "Second Request" for additional documentation, extending the review process [1]. Violating the HSR Act carries steep penalties, with fines reaching $53,088 per day [6][7].

For 2026, the Clayton Act prohibits interlocking directorates when both corporations' capital and surplus exceed $54,402,000, unless competitive sales are under $5,440,200 or below 2% of total sales [5][6]. Companies are encouraged to review their directors' roles annually to ensure compliance.

In Canada, the C$93 million notification threshold remains below inflation-adjusted levels, ensuring that transactions with potential competitive impacts are reviewed [3]. This reflects a broader global trend, as regulators tighten oversight to catch deals that might harm competition, even if their nominal values appear modest.

When it comes to cross-border mergers and acquisitions (M&A), national security concerns play a major role in determining whether a deal requires notification. In the U.S., these concerns are handled by the Committee on Foreign Investment in the United States (CFIUS), which evaluates transactions that might threaten critical infrastructure, sensitive technologies, or personal data. Unlike traditional merger reviews, CFIUS doesn't rely on a dollar threshold - any deal can be reviewed if national security is at risk [9][11].

CFIUS focuses on transactions involving "TID" businesses - those dealing with critical technology, infrastructure, or sensitive personal data [10][11]. A filing is required when a foreign government owns 49% or more of an entity acquiring at least 25% of a U.S. TID business [9][10]. Additionally, deals involving export-controlled technologies, such as those regulated under ITAR, must be reported if an export license is necessary [9][10].

The term sensitive personal data is interpreted broadly. If a U.S. business manages data on over 1,000,000 Americans - like health records, financial information, geolocation details, or biometric data - the deal will likely face extra scrutiny [11]. Critical infrastructure, on the other hand, includes essential systems like energy grids, telecommunications networks, and water supplies, all of which are tied to national security [11].

"CFIUS is keenly interested in nearly all advanced technology sectors, and the Committee made clear in 2024 that it would become far more aggressive about policing compliance." – Jason C. Chipman, Partner, WilmerHale [10]

Violating CFIUS rules can lead to steep financial penalties, now exceeding $5,000,000 per violation. This contrasts with the per-day fines imposed for HSR violations [11]. For deals deemed lower risk, parties can submit a free 30-day short-form declaration. However, even with this option, CFIUS may request a full notice if concerns arise. In 2023, about 76% of short-form declarations were approved without needing further review [9][12].

Investors from "excepted foreign states" - currently Australia, Canada, New Zealand, and the United Kingdom - might qualify for exemptions from certain reviews if they meet specific criteria [9][11]. Looking ahead, starting January 2, 2025, U.S. outbound investment regulations will require notification or impose restrictions on investments in foreign companies - particularly Chinese firms - working in areas like semiconductors, quantum computing, and artificial intelligence [10][11].

These detailed U.S. regulations often set the tone for similar national security reviews in other countries.

Canada and the European Union (EU) have established their own systems to address foreign investment risks, which are similar in scope to U.S. national security reviews but differ in execution.

In Canada, the Investment Canada Act (ICA) uses a two-track system. The "net benefit" review evaluates economic impact and applies only to deals exceeding high thresholds, such as C$2.179 billion for trade agreement investors in 2026 [13]. Meanwhile, the national security review (NSR) process applies to any investment by non-Canadians that could harm national security. This includes minority stakes and even the creation of new Canadian businesses [13]. Unlike CFIUS, Canada's process examines both economic and security factors. For sensitive sectors, pre-closing filings will soon become mandatory, and the NSR regime can review deals up to five years post-closing if they weren’t pre-notified [13].

The EU, on the other hand, takes a decentralized approach. Each member state conducts its own foreign investment reviews, with countries like Germany, France, and Italy having their own screening mechanisms for sensitive sectors such as defense, critical infrastructure, and advanced technologies. Although the EU has a coordination framework, the lack of uniform thresholds and criteria across member states creates a patchwork of requirements, making navigation more complex for acquirers.

Certain industries, like banking, energy, telecommunications, and transportation, face additional regulatory hurdles beyond the typical antitrust and national security reviews. Transactions in these sectors often require dual filings with federal antitrust authorities - such as the Federal Trade Commission (FTC) or Department of Justice (DOJ) - and industry-specific regulators. These overlapping requirements can stretch approval timelines, so understanding these processes is crucial for efficient deal planning.

In the financial services industry, the Board of Governors of the Federal Reserve System evaluates bank mergers to ensure they align with prudential standards and regulatory guidelines. This review focuses on factors like competition, financial stability, risk management practices, and regulatory compliance.

For energy-related mergers, the Federal Energy Regulatory Commission (FERC) steps in to assess deals involving electric utilities and interstate pipelines. FERC's primary concern is whether a transaction could harm competition in wholesale energy markets or disrupt service reliability.

State-level regulators also play a significant role in sectors like telecommunications and utilities. Their independent reviews can add another layer of complexity, potentially delaying timelines. Transactions involving foreign investments or critical infrastructure may also trigger a review by the Committee on Foreign Investment in the United States (CFIUS). To avoid unexpected delays, it’s essential to map out federal, state, and CFIUS approval tracks early in the process.

Beyond financial and energy sectors, other regulated industries have their own unique filing requirements. For mergers in telecommunications and media, the Federal Communications Commission (FCC) evaluates whether the deal serves the public interest. Their review considers factors such as service quality, competition, and media ownership diversity.

In transportation, the Surface Transportation Board (STB) holds authority over railway mergers, ensuring these transactions comply with industry standards and do not negatively impact the sector.

Defense-related transactions face even stricter requirements. Recent legislation mandates that defense-related deals submit identical information to both the Department of Defense (DOD) and antitrust agencies at the same time. This allows the DOD to analyze potential risks to national security and defense supply chains alongside traditional antitrust reviews. Non-compliance with pre-merger notification requirements can lead to civil penalties of up to $53,088 per day [14].

Given the complexity of these overlapping obligations, it’s critical to confirm all required filings - federal and state - before closing a deal. Missing even one step could result in significant delays or penalties.

2026 Cross-Border M&A Notification Thresholds: US vs Canada Comparison

Handling filings across different jurisdictions can be tricky, as each has its own rules for timing, thresholds, and coordination. For instance, the U.S. applies "size-of-transaction" and "size-of-person" tests [8], while Canada uses "size-of-target" and "size-of-parties" criteria based on assets and revenues [3]. These variations mean there’s no one-size-fits-all formula, making detailed planning essential.

Timing matters. Filing thresholds are updated annually, so staying current is critical. In the U.S., the Hart-Scott-Rodino (HSR) thresholds adjust based on metrics like the Consumer Price Index [5][8]. Similarly, Canada’s Investment Canada Act thresholds will rise by about 4.8% to 4.9% in 2026 [3]. Take note: deals signed in late 2025 but closing after February 17, 2026, must comply with the updated 2026 limits [15]. Filing fees are determined by the thresholds in effect at the time of filing, not at closing [15].

Waiting periods can affect timelines. In the U.S., there’s typically a 30-day waiting period after filing, while Canada generally requires 45 days to initiate national security reviews [1][3]. However, expedited options exist. For example, you can request "Early Termination" in the U.S. or an "Advance Ruling Certificate" in Canada to potentially shorten these timelines [1][3]. In Canada, even voluntary notifications for non-notifiable investments can trigger the 45-day review period, which may help avoid the government’s 5-year look-back window for national security concerns [3].

| Metric | United States (HSR) | Canada (Competition Act) |

|---|---|---|

| Primary Threshold | $133.9 million (Size-of-Transaction) | C$93 million (Size-of-Target) |

| Secondary Threshold | $267.8 million / $26.8 million (Size-of-Person) | C$400 million (Size-of-Parties) |

| Calculation Basis | Voting securities, assets, or noncorporate interests | Assets in Canada or revenues from sales in/from/into Canada |

| Standard Waiting Period | 30 days | Varies (often 30 days; 45 days for national security) |

| Filing Fee Range | $35,000 – $2,460,000 | C$88,690.45 |

| National Security Review | CFIUS (separate from HSR) | ICA Review (45-day initial window) |

Start by identifying the ultimate parent entity (UPE) for each party. In the U.S., the "size-of-person" test includes the UPE and its controlled subsidiaries [8]. For the "size-of-transaction" test, calculate the total value of voting securities, unincorporated interests, and assets of the acquired entity that will be held post-closing [5].

In Canada, assess whether the target meets the required asset or revenue thresholds "in, from, or into" the country. The 2026 "size-of-target" threshold is C$93 million, a figure that has remained steady since 2021 [3]. The "size-of-parties" test requires a combined value of C$400 million, which includes the buyer, the target, and their affiliates [3].

For Investment Canada Act reviews, thresholds vary depending on the investor type. For example, Trade Agreement Investors have a threshold of C$2.179 billion, WTO Investors need C$1.452 billion, and State-Owned Enterprises must meet a threshold of C$578 million [3]. Even if monetary thresholds aren’t met, deals involving sensitive technology, critical minerals, or personal data could still trigger national security reviews [3]. To avoid surprises, consult legal counsel early and consider filing voluntarily to sidestep the 5-year look-back period [3].

Understanding and keeping track of notification triggers is a key part of navigating cross-border M&A successfully. Factors like transaction value, company size, and national security concerns often determine whether regulatory filings are necessary. Missing these requirements can lead to hefty penalties and significant delays.

Notification thresholds change annually, reflecting shifts in economic metrics. Timing is critical - if a deal is signed in late 2025 but closes after February 15, 2026, it must adhere to the updated thresholds.

To stay ahead, start compliance assessments early. Calculate metrics at the Ultimate Parent Entity level to determine filing obligations accurately. This approach ensures proper filing determinations for all controlled subsidiaries, as previously discussed [8].

"The HSR thresholds are only one part of the analysis to determine whether an HSR filing is required." – Winston & Strawn LLP [1]

Be prepared for potential delays and costs. Filing fees range from $35,000 to $2,460,000, depending on the transaction's size. Additionally, filings come with a mandatory 30-day waiting period, which can extend if regulators request more information [8]. Early evaluations and expert advice are essential to avoid obstacles.

With these complexities in mind, Phoenix Strategy Group offers the expertise to guide you through multi-jurisdictional filings, ensuring your transaction closes smoothly.

To determine the value of a deal for HSR purposes, the transaction value is based on one of the following: the cash purchase price, the fair market value of issued stock, or the projected earnouts. The Federal Trade Commission provides specific rules for each valuation method, and it's important to follow these guidelines carefully when calculating the deal's value.

Some transactions are exempt from requiring an HSR filing, particularly those falling below the size thresholds. For 2024, deals valued at less than $119.5 million are not subject to filing. Additionally, exemptions may apply to smaller or non-reportable transactions that do not meet specific jurisdictional criteria. Since these thresholds are updated every year, it's crucial to check the most current guidelines before moving forward.

When dealing with potential national security or security risks, it's wise to submit a notice to CFIUS (Committee on Foreign Investment in the United States) or Canada's national security authorities, even if the usual thresholds aren't met. CFIUS has the authority to review transactions at its discretion if such risks are present. Similarly, in Canada, certain security concerns or exceeding specific review thresholds might trigger a notification requirement, regardless of the transaction's size.