Published on

March 16, 2026

Cross-border M&A deals often come with hidden costs and risks tied to customs duties and VAT, which can directly affect acquisition costs, cash flow, and compliance. Ignoring these taxes can lead to penalties, delayed integrations, and inflated purchase prices. Here's what you need to know:

Addressing these issues early ensures smoother transactions and better long-term outcomes. Financial advisors play a crucial role in navigating these complexities, offering tailored solutions for VAT recovery, customs compliance, and tax-efficient deal structures.

Share Sale vs Asset Sale: VAT and Customs Implications in Cross-Border M&A

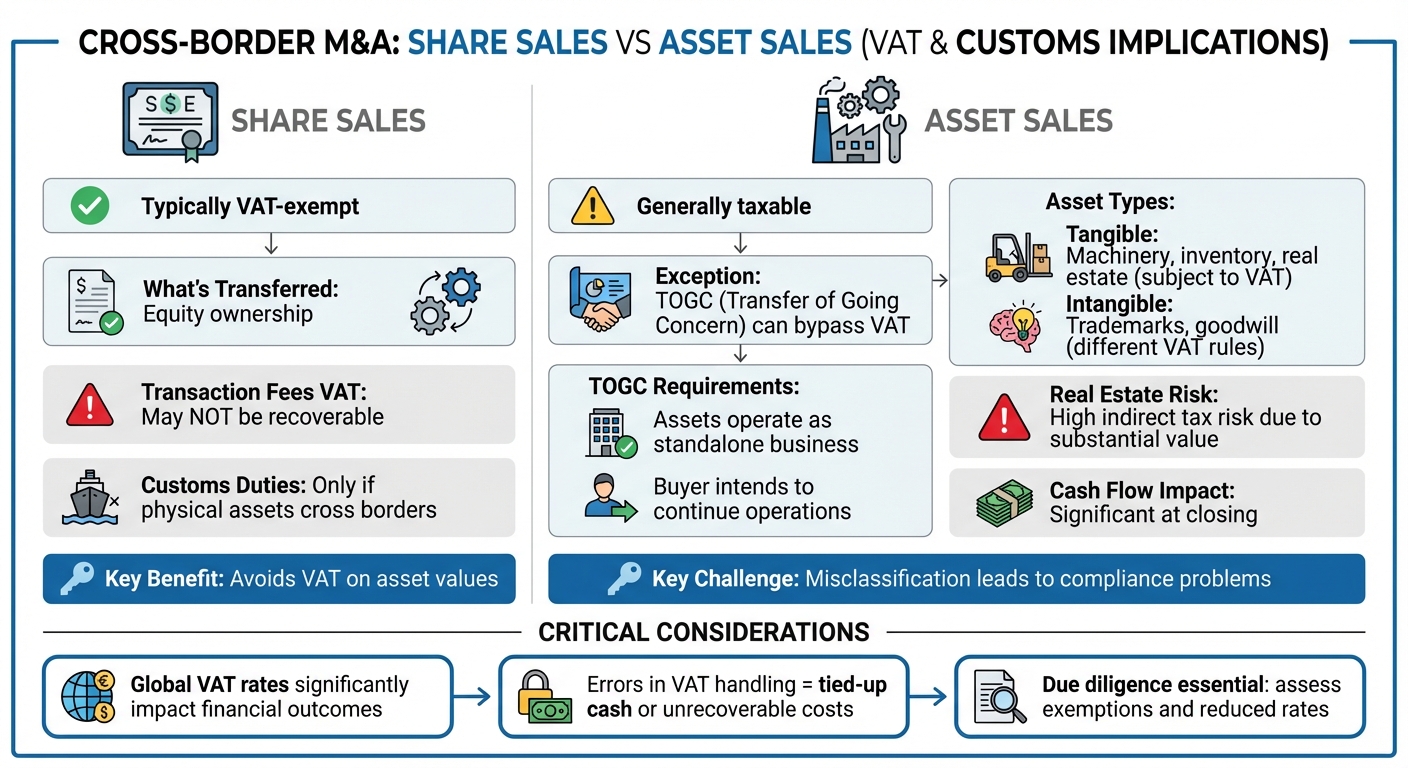

Handling VAT correctly during asset transfers is essential to avoid cash flow issues and ensure smooth deal execution. In cross-border M&A, VAT treatment significantly impacts the financial outcome of a deal, especially with high global VAT rates[9]. The application of VAT depends on the structure of the deal, the type of assets involved, and the availability of relief measures. Errors in VAT handling can lead to tied-up cash at closing or unrecoverable costs, which may increase the effective purchase price. Let’s dive into the specifics of VAT treatment in asset transfers, strategies for VAT recovery, and how VAT affects supply chains.

The VAT treatment of asset transfers varies depending on the type of asset and the deal structure. Tangible assets - like machinery, inventory, and real estate - are subject to different VAT rules compared to intangible assets such as trademarks or goodwill. Misclassifying these assets can result in incorrect tax applications and compliance problems.

The distinction between share sales and asset sales is crucial. Share transactions typically avoid VAT because they involve acquiring equity, whereas asset sales are generally taxable unless they qualify as a Transfer of a Going Concern (TOGC). For a transaction to meet TOGC criteria, the assets must be capable of operating as a standalone business, and the buyer must intend to continue using them. Under TOGC rules, the sale is not treated as a supply of goods or services, which allows the transaction to bypass VAT.

Real estate transfers pose a particularly high indirect tax risk due to their substantial value. These transactions can create significant cash flow challenges at closing. During due diligence, it’s essential to assess whether the property qualifies for exemptions or reduced VAT rates to mitigate this risk.

Another often-overlooked issue is VAT on transaction fees. For example, VAT incurred on legal, consulting, or advisory fees in share-based deals may not be recoverable, directly impacting the overall transaction budget.

Recovering input VAT promptly after acquisition is critical. Buyers need to determine whether new VAT registrations are required to support ongoing operations or fulfill existing customer commitments in local markets. Without proper registration, recovering VAT and issuing compliant invoices becomes challenging.

Transitional Services Agreements (TSAs) can further complicate VAT recovery. When the seller provides post-acquisition support services - like IT, HR, or finance functions - TSAs must be carefully structured to ensure VAT efficiency. Poor planning can lead to unexpected costs and hinder VAT recovery during the transition period.

Carve-outs also bring unique challenges. Transferring or restructuring back-office operations can weaken existing tax systems, leaving the new entity without the expertise to manage indirect tax obligations. Buyers need to assess whether to strengthen internal resources or engage external advisors to handle technical VAT issues and ensure compliance across multiple jurisdictions.

VAT considerations extend beyond the acquisition itself and into supply chain integration. Post-acquisition adjustments to supply chains often come with indirect tax implications. For example, new entities may require fresh VAT registrations, and changes to inventory routing can result in different VAT treatments across borders. Processes that worked under the seller’s structure may become inefficient for the buyer, leading to cash flow challenges.

Once operations stabilize, reviewing the new indirect tax profile is a good practice. This review can help identify redundant VAT registrations, reduce unnecessary costs embedded in the supply chain, and streamline compliance efforts. Treating VAT as an ongoing operational issue - not just a closing-day concern - can prevent inefficiencies from becoming long-term problems after the acquisition.

Customs duties often introduce extra costs and compliance hurdles in cross-border M&A transactions. Unlike VAT, which primarily affects how deals are structured, customs duties impact the physical movement of goods and the day-to-day operations of the acquired business. These challenges become even more complex when buyers relocate inventory, reorganize supply chains, or inherit customs practices from the target company that may not hold up under regulatory scrutiny. Problems typically arise when goods cross borders during asset relocations, triggering specific customs-related issues.

Customs duties come into play when goods physically cross international borders. In M&A, this can occur when buyers import acquired inventory, move machinery or equipment to new locations, or shift manufacturing operations between countries. Even in share sales, customs duties may be triggered if physical assets are transferred across borders.

For transactions between related parties, customs valuation rules require proof that prices were negotiated freely. Customs authorities may reject the Transaction Value (TV) - the price paid or payable for goods sold for export - if they suspect the relationship between the buyer and seller influenced the pricing. To satisfy customs requirements, businesses must show that the price aligns with what unrelated parties would negotiate. This often creates tension: transfer pricing models designed to minimize income tax (favoring lower import values) can conflict with customs authorities, who scrutinize undervalued imports closely[10][12].

Product classification under the Harmonized System (HS) is another critical area. The first six digits of HS codes are standardized across 184 World Customs Organization (WCO) member nations[11]. In the U.S., 10-digit codes under the Harmonized Tariff Schedule (HTS) are used. Misclassification of goods can lead to either overpayment or underpayment of duties, both of which carry financial and legal risks.

Understanding when customs duties are triggered is just the beginning - thorough due diligence is key to ensuring compliance and avoiding costly surprises during post-acquisition integration. This is especially true when managing remote M&A integration across different jurisdictions.

Start by verifying the correct HTS classifications for all goods. Errors here can lead to penalties and retroactive duty corrections. Also, evaluate whether the target company qualifies for preferential treatment under trade agreements like USMCA or other regional pacts, which can significantly lower duty expenses[13].

"Trade tariffs are more than just a line item on an import invoice - they are a dynamic legal and operational risk factor that demands proactive management." - Oberman Law Firm[13]

Valuation practices also deserve close attention. Importers must ensure that specific costs - such as commissions, brokerage fees, container costs, royalties, license fees, and assists (e.g., materials or tools provided by the buyer at a reduced cost) - are included in the Transaction Value if applicable[10][12]. Since the Transaction Value method is used in 90% to 95% of imports globally[12], it serves as the default approach. If rejected, customs authorities may turn to alternative methods like valuations based on identical goods, similar goods, or even computed production costs.

Internal audits and simulated customs exams can help assess the company’s readiness for regulatory inquiries and ensure its recordkeeping practices are solid[13]. Additionally, review the target’s Incoterms (such as FOB or CIF) in contracts, as these terms dictate whether freight and insurance costs must be included in customs valuation[11]. To protect against surprises, buyers should negotiate contractual provisions like indemnities for misclassification or origin errors and tariff adjustment clauses that allow price renegotiations if duties change[13].

Building on earlier insights about VAT and customs challenges, let’s dive into strategies that help limit indirect tax risks in cross-border M&A. Success here hinges on early identification of potential pitfalls, efficient tax system integration, and leveraging available tax reliefs to cut costs.

Before finalizing a deal, it's crucial to scrutinize tax provisions, open tax years, and any pending audits. This includes verifying VAT registrations and filings, such as European Sales Listings and Intrastat, as well as ensuring customs declarations and transfer pricing compliance are in order. For instance, a U.S. multinational avoided hefty fines by adjusting its royalty rates to align with OECD guidelines during due diligence, addressing both transfer pricing and VAT concerns[1][4]. Additionally, securing clear representations and warranties in share purchase agreements can protect buyers from pre-transaction liabilities[3]. Thorough due diligence not only identifies risks but also sets the stage for successful tax system integration post-acquisition.

Post-acquisition, aligning VAT and customs processes is essential. Simplify VAT registrations and filings, such as VAT returns, Intrastat, or One Stop Shop, by rationalizing legal entities[4]. On the customs side, focus on managing duties at import points while unifying global tax processes to maintain control over indirect tax exposure[4][5]. Cross-functional workshops involving tax, legal, and finance teams can help map out filing deadlines and simulate post-deal scenarios, ensuring a smoother transition[4][6]. Restructuring entities to support scalable compliance can lead to better efficiency, while creating compliance calendars with clear accountability helps avoid penalties[4][6]. Once systems are in sync, applying tax reliefs becomes significantly more effective.

Tax exemptions and reliefs offer opportunities to lower indirect tax costs. For example, zero-rated VAT on exports, full VAT credits for qualifying investments, or customs deferrals via bonded warehouses can all make a difference[2][7]. In the EU, frameworks like the Import One Stop Shop (iOSS) and the Union Scheme simplify cross-border filings[2]. Procedures such as Procedure 42 allow goods to enter free circulation without immediate VAT charges, shifting liability to the recipient and avoiding complex VAT reclaim processes[7]. Separating mixed transactions to apply lower VAT rates and filing treaty-based returns to secure reduced withholding rates can also help[1][3]. Structuring deals early with mechanisms like merger roll-over or participation exemptions can lead to considerable savings[1][3].

Navigating cross-border mergers and acquisitions (M&A) involves tackling a complex web of tax challenges, including customs compliance, VAT management, and transfer pricing. Financial advisors play a key role in ensuring these elements are seamlessly integrated throughout the deal lifecycle. By addressing these areas comprehensively, they help buyers minimize value loss across jurisdictions while facilitating smoother post-deal integration. This builds on earlier discussions around managing indirect tax risks and focuses on reducing exposure in cross-border transactions.

Financial advisors bring expertise to areas like VAT registration across multiple jurisdictions, customs duty exposure on asset transfers, and aligning transfer pricing documentation with OECD guidelines. They analyze contracts to uncover zero-rated VAT opportunities and optimize VAT credits, which can significantly improve cash flow - especially in acquisitions involving equipment-heavy businesses. For customs-related matters, advisors streamline declaration processes and clarify import VAT settlement responsibilities for the newly combined entity. Firms like Phoenix Strategy Group specialize in addressing these indirect tax challenges while ensuring financial integration aligns with varying accounting standards.

Fractional CFO services offer targeted, cost-effective expertise to manage the intricate tax planning required in M&A. These professionals create compliance calendars with clear accountability for filing deadlines in each jurisdiction, helping avoid costly penalties. They also organize cross-functional workshops to simulate post-deal scenarios, uncovering potential risks before they escalate. Phoenix Strategy Group’s fractional CFO services are particularly beneficial for growth-stage companies, providing support for legal entity restructuring to attract investment, explore new markets, and build scalable tax frameworks. This kind of strategic planning is essential for managing the complexities of cross-border M&A.

The impact of expert advisory services is evident in real-world M&A outcomes. For instance, tax planning played a pivotal role in accelerating deal closings in December 2025, driven by U.S. sellers aiming to lock in capital gains before anticipated tax changes in 2026. Similarly, European buyers rushed to finalize transactions before the Q2 2026 implementation of BEPS 2.0 to avoid additional complications. Financial advisors also helped integrate customs compliance and VAT management into M&A strategies, especially after the Carbon Border Adjustment Mechanism (CBAM) became enforceable on January 1, 2026. By engaging early, advisors structured deals efficiently, secured advance pricing agreements with tax authorities, and adopted conservative tax strategies that could withstand scrutiny across multiple jurisdictions. These proactive measures demonstrate the tangible benefits of expert tax advisory in cross-border M&A transactions.

Cross-border M&A transactions in 2026 demand early attention to customs and VAT compliance. With the EU's Carbon Border Adjustment Mechanism taking effect on January 1, 2026, and the removal of the €150 customs duty exemption starting July 1, 2026, companies face new costs and stricter compliance rules. These changes directly influence acquisition valuations and complicate post-deal integration[14].

Ignoring indirect tax issues can lead to severe financial consequences. For example, a U.S. multinational was penalized heavily for non-compliant royalty rates in intercompany agreements, illustrating how customs and VAT oversights during pre-deal stages can result in costly liabilities after acquisition[1][3]. The compliance landscape has also tightened with the inclusion of mandatory Principal Purpose Tests in 60% of double tax agreements and updated VAT regulations affecting cross-border services, adding further challenges for firms pursuing global deals[1][2].

However, expert advisory services can transform these challenges into opportunities for tax efficiency. Financial advisors help uncover hidden VAT risks, utilize treaty elections for zero-rated withholding on dividends and interest, and structure transactions to maximize recoverable input VAT[1][2][8]. Firms like Phoenix Strategy Group provide specialized M&A advisory and fractional CFO services, equipping growth-stage companies with the expertise needed to tackle these complexities while staying focused on their goals.

Engaging tax advisors early is critical. By incorporating customs compliance and VAT strategies into the early stages of M&A planning, companies can minimize value erosion, accelerate deal closings, and establish scalable tax frameworks that support long-term growth in a more regulated global market.

Your transaction might lead to VAT or customs duties if there are problems such as product misclassification, inaccurate valuation, or failure to comply with customs regulations. These issues can expose you to audits, fines, or even disruptions in your supply chain. To minimize these risks, it's smart to perform thorough due diligence early on and consult with experts who can guide you through the process.

Reducing unrecoverable VAT during a transaction's closing requires careful planning and strict compliance with VAT regulations. Start by ensuring accurate and up-to-date documentation. This helps avoid errors that could lead to VAT becoming non-recoverable.

Timely VAT registration is another key step. Missing registration deadlines can result in penalties or missed opportunities for VAT recovery. Additionally, it’s essential to follow local VAT rules closely, as these can vary significantly between jurisdictions.

Thorough due diligence plays a crucial role too. By identifying potential VAT risks early, you can address issues before they escalate. Finally, consider structuring transactions strategically to maximize VAT recovery opportunities wherever possible. This could involve evaluating the supply chain or reviewing contractual terms to ensure compliance and efficiency.

During the due diligence process, it's crucial to examine key areas like customs classification, valuation, import/export restrictions, and tariff compliance. These reviews are essential for spotting potential risks, including penalties, shipment delays, or regulatory complications, that might affect cross-border M&A transactions.