Published on

March 16, 2026

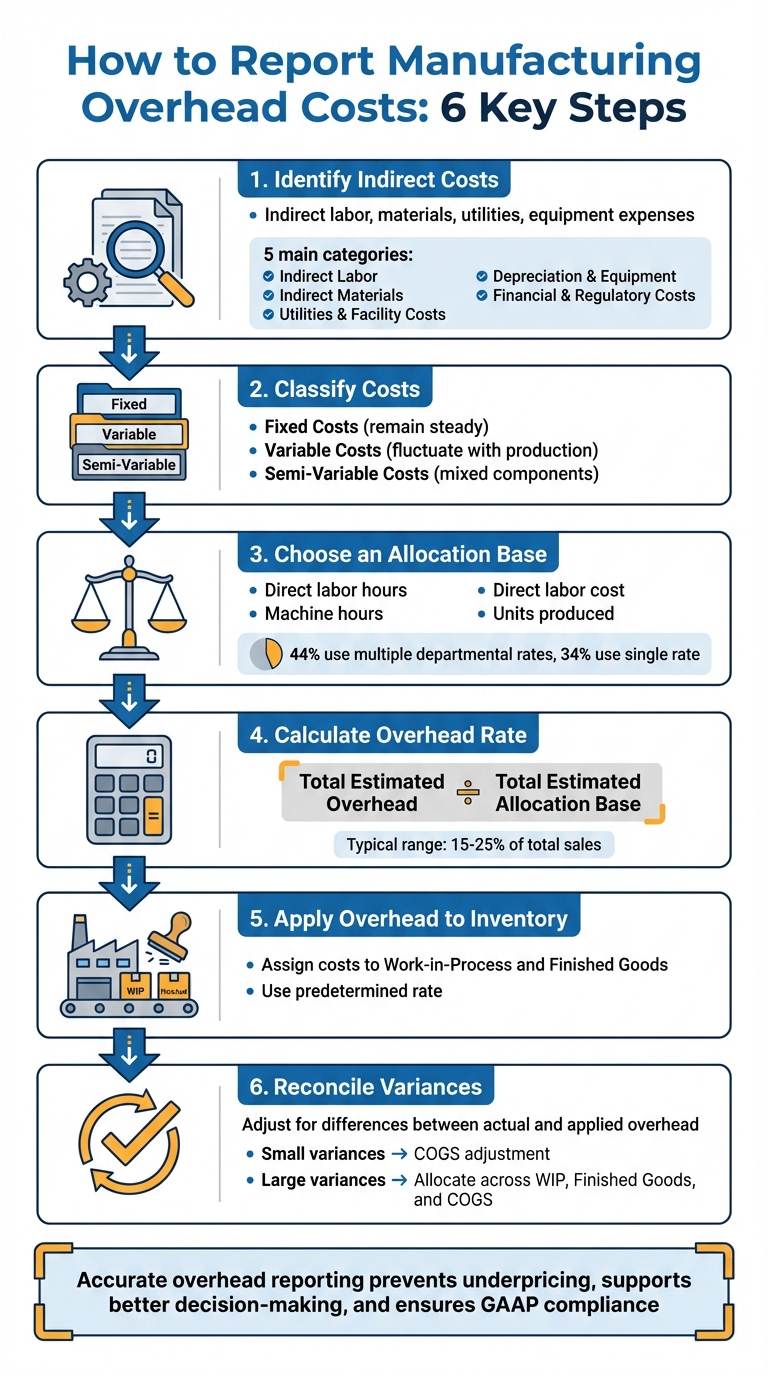

Manufacturing overhead costs are the indirect expenses required to support production but cannot be directly traced to specific products. These include factory rent, utilities, equipment depreciation, and supervisor salaries. Reporting these costs accurately is critical for compliance with GAAP and ensuring proper inventory valuation and pricing.

Accurate reporting prevents underpricing, supports better decision-making, and ensures compliance with financial regulations. Missteps, such as mixing period costs with overhead or using outdated allocation methods, can distort financial results. Regular reviews and proper documentation help maintain accuracy and transparency.

6-Step Process for Reporting Manufacturing Overhead Costs

The first step in allocating overhead is to gather every supporting cost tied to production. This means identifying all indirect manufacturing costs by thoroughly reviewing payroll records, maintenance logs, utility bills, and lease agreements. These costs don’t directly become part of the finished product but are essential to the production process. Getting this step right is critical since it sets the stage for accurate overhead allocation later.

Manufacturing overhead typically breaks down into five main categories, helping you organize and report these costs effectively:

For instance, a furniture manufacturer calculated $140,000 in total overhead costs. They divided this amount across three cost centers - Cutting, Assembly, and Finishing - using direct labor hours as the allocation base. This resulted in an overhead rate of $35 per labor hour [3].

It's important to review a full year of records to account for seasonal changes. For example, heating costs may spike in winter, while cooling expenses rise in summer. Annual insurance renewals and other periodic costs should also be factored in. Once you've gathered this data, classify costs into one of three categories:

To ensure no overhead-generating activities or assets are missed, many manufacturers find it helpful to conduct an onsite review with their accounting team. After identifying and classifying all costs, the next step is to choose an allocation base to calculate the overhead rate.

To allocate overhead costs effectively, pick a measurable activity - known as an allocation base - that directly influences your overhead expenses. Then, calculate a predetermined overhead rate to assign these costs to products. This method ensures accurate job costing and helps with timely pricing decisions.

Your allocation base should align closely with the factors driving your overhead costs. As this activity increases, overhead expenses should rise proportionally. Common choices include:

"If you pick an allocation base that doesn't actually correlate with how overhead costs are incurred, your product costs will be distorted." – Flxpoint [4]

For businesses with varied operations - such as a mix of automated and manual processes - consider using separate departmental rates instead of a single plantwide rate. A survey revealed that 44% of manufacturers use multiple departmental overhead rates, while 34% rely on a single rate [6]. It’s a good practice to review your allocation base annually or even quarterly if costs and production volumes fluctuate significantly.

Once you’ve chosen an allocation base, calculate the predetermined overhead rate using this formula:

Total Estimated Overhead ÷ Total Estimated Allocation Base

This calculation happens at the start of your accounting period, using forecasted data. It allows you to assign overhead costs consistently throughout the period without waiting for final year-end figures.

Here’s how it works:

In manufacturing, overhead rates typically range from 15% to 25% of total sales, depending on the industry and production methods [1].

Since these rates are estimates, any differences between applied and actual overhead need to be reconciled at the end of the period. Small variances can be adjusted directly to Cost of Goods Sold (COGS), while larger discrepancies should be distributed across Work-in-Process, Finished Goods, and COGS [5]. (Details on this process are covered in Step 4.) With the overhead rate established, you’re ready to apply these costs to inventory in the next step.

This step involves assigning overhead costs to production using your predetermined overhead rate. By doing so, you move overhead from a temporary holding account into inventory, ensuring that Work-in-Process (WIP) and Finished Goods are valued accurately according to GAAP standards.

Most manufacturers rely on a normal costing system. This approach tracks actual direct materials and labor while applying overhead using a predetermined rate [8]. The method is simple: multiply your predetermined overhead rate by the actual amount of the allocation base used during production.

Here’s an example: If your overhead rate is $20.00 per machine hour and a production run uses 500 machine hours, you would apply $10,000 in overhead to that job. Overhead costs are distributed to each unit as the allocation base (like machine hours or labor hours) is consumed [5]. The Manufacturing Overhead account acts as a clearing account, recording actual costs (debits) and applied costs (credits) until a reconciliation is completed at the end of the period [8].

To comply with ASC 330, overhead should be allocated based on normal capacity - your average production level. This prevents inflated inventory values during periods of low production [7]. For instance, if production falls short by 30,000 units and your overhead rate is $5.00 per unit, this could result in a 3% margin impact on $5 million in sales [7].

Once you’ve calculated and applied overhead, you’ll need to record the necessary journal entries to reflect these costs in your inventory accounts.

| Transaction Stage | Debit Account | Credit Account | Purpose |

|---|---|---|---|

| Incurring Actual Overhead | Manufacturing Overhead | Cash / Accounts Payable / Accumulated Depreciation | Records actual indirect costs as they occur [10][13]. |

| Applying Overhead to WIP | Work-in-Process Inventory | Manufacturing Overhead | Capitalizes estimated overhead into inventory [10][13]. |

| Completion of Goods | Finished Goods Inventory | Work-in-Process Inventory | Transfers total costs (materials + labor + applied overhead) to finished stock [8]. |

Getting the numbers right when reconciling actual and applied overhead is essential for accurate cost reporting and compliance with GAAP. At the end of each period, you’ll need to compare actual overhead costs to the applied overhead. This process ensures that your COGS (Cost of Goods Sold), net income, and inventory values are spot on. Ignoring or mismanaging variances can throw off your income statement and balance sheet in a big way [14].

The first step is to figure out the variance. This is done by subtracting the applied overhead from the actual overhead costs [5]. Start by summing up all indirect expenses for the period - things like utilities, factory rent, depreciation, and indirect materials. Then, compare that total to the overhead applied, which is based on your predetermined rate.

Here’s how it plays out:

Take these examples:

Once you’ve calculated the variance, it’s time to adjust your records.

After identifying the variance, the next step is to close the Manufacturing Overhead account and update your financials. How you handle this depends on whether the variance is minor or substantial [15].

If the variance is substantial, it might be a sign that your predetermined overhead rate needs tweaking for the next period [15].

After reconciling actual and applied overhead, it’s critical to steer clear of common reporting mistakes. Accurate overhead reconciliation is essential for consistent financial reporting, but even with a solid process, manufacturing overhead reporting can easily go off track. Many errors come from misclassifications and outdated practices that skew financial results. Let’s break down these common mistakes and how to prevent them.

One of the most common mistakes is mixing period costs with overhead. Expenses like corporate salaries, marketing costs, sales commissions, and general office expenses are period costs, not manufacturing overhead. These should go directly to the income statement. Including them in overhead calculations inflates product costs, leading to uncompetitive pricing and inaccurate profitability assessments.

Another issue arises from using outdated allocation bases. For example, if your operations have become more automated but you’re still allocating overhead based on labor hours, your rates won’t reflect the real cost drivers. On top of that, ignoring seasonal fluctuations can create wild swings in inventory valuations and product costs. Calculating rates using monthly data instead of annual estimates exacerbates this problem.

Capacity miscalculations are another pitfall. Using theoretical maximum capacity instead of realistic "normal" capacity can result in under-applied overhead and erratic product costs. As CLA highlights:

Overhead must be allocated based on 'normal capacity' and not inflated due to idle time or abnormal production levels [7].

Lastly, inconsistent methodology - switching allocation methods or bases between periods without proper justification - can make financial results incomparable and raise concerns during audits.

Here are some ways to avoid these challenges:

Here’s a quick reference table summarizing common mistakes, their impacts, and how to avoid them:

| Common Mistake | Business Impact | Prevention Strategy |

|---|---|---|

| Including Non-Manufacturing Costs | Inflated product costs; uncompetitive pricing; distorted profitability | Define manufacturing vs. period costs; train staff on proper categorization |

| Inconsistent Allocation Methods | Incomparable financial results; audit risks; misleading trends | Document and apply methods consistently; justify changes |

| Using Maximum vs. Normal Capacity | Under-applied overhead; erratic product costs | Use normal capacity; rely on historical utilization |

| Ignoring Seasonal Variations | Fluctuating rates; unstable product costs; inventory issues | Use annual estimates to smooth seasonal effects |

GAAP and ASC 330 emphasize the need to prove that overhead is capitalized correctly, based on normal capacity, rather than being inflated by idle time or unusual production levels [7]. Without thorough records, overhead calculations could fail audits. By combining accurate cost allocation methods with detailed documentation, businesses can ensure compliance and be fully prepared for audits.

To support your overhead allocation process, you need to document every step. This includes reconciling actual versus applied overhead, as outlined in Step 4. Proper records - like journal entries and schedules - are essential for validating overhead allocation and inventory adjustments [7].

| Record Category | What to Keep on File |

|---|---|

| Labor & Payroll | Department payroll summaries and time tracking logs [7] |

| Production Activity | Routing sheets, machine hour logs, labor hour calculations, standard lot size definitions [7][12] |

| Allocation Support | Allocation schedules, rate calculations, and normal capacity records [7] |

| Financial Entries | Journal entries for inventory adjustments, COGS records, and year-end variance adjustments [7] |

| Indirect Cost Proof | Invoices for utilities, rent, depreciation schedules, insurance premiums, and property taxes [7][9] |

Strong record-keeping is the backbone of effective audit preparation. Auditors will examine whether overhead costs are properly capitalized and whether allocation methods remain consistent over time [7]. If your allocation base changes - like switching from labor hours to machine hours - you’ll need to provide clear, written justification [7]. Sharing your allocation methods with auditors early can help address any questions before fieldwork begins [7].

It’s also crucial to separate manufacturing overhead from period costs. Harold Averkamp, CPA, MBA, from AccountingCoach, explains:

Manufacturing overhead refers to indirect factory-related costs that are incurred when a product is manufactured... the cost of manufacturing overhead must be assigned to each unit produced so that Inventory and Cost of Goods Sold are valued and reported according to generally accepted accounting principles (GAAP) [9].

Regular reviews of subledgers can help identify and resolve discrepancies ahead of audits [7]. These practices make compliance easier while also improving internal controls and financial transparency.

Overhead reporting involves five key steps. First, pinpoint all indirect costs, such as factory rent, utilities, depreciation, and supervisory wages. Next, choose an allocation base that aligns with your cost drivers. Then, calculate the predetermined overhead rate by dividing total estimated overhead by the allocation base. After that, apply this rate to production activity to assign costs to inventory. Finally, reconcile the applied costs with the actual expenses and adjust for any variances.

Keeping detailed records is crucial. Documents like payroll summaries, overhead allocation schedules, routing sheets, and journal entries provide essential support during audits. As CLA Connect explains:

Allocating labor and overhead to inventory is more than a compliance exercise - it's imperative to your operational efficiency and financial accuracy. [7]

Mastering these steps ensures your business is well-prepared to improve its cost reporting processes.

Once you've established the basics, it's time to refine your approach to meet changing manufacturing and compliance needs. Start by reassessing your allocation methods to ensure they reflect your current production setup. For example, if your operations have become more automated but you're still relying on direct labor hours as the allocation base, it’s time for an update. Reviewing your overhead rates quarterly can also help account for seasonal fluctuations and business growth.

You might also explore how advanced technology can enhance your accuracy. Tools like ERP and Manufacturing Execution Systems allow manufacturers to collect real-time data on machine performance and labor, enabling more precise overhead allocation. In fact, ERP and IoT technologies have been shown to significantly reduce overhead costs [2].

Accurate overhead reporting is more than a compliance requirement - it’s a cornerstone of effective financial management. It ensures proper pricing, supports scalability, and prepares your business for audits. Whether you’re expanding operations or fine-tuning processes, accurate overhead allocation lays the groundwork for sustainable growth. For personalized advice on manufacturing cost reporting, reach out to Phoenix Strategy Group (https://phoenixstrategy.group).

Overhead costs that are directly related to manufacturing - things like machinery depreciation, property taxes on manufacturing assets, facility insurance, production utilities, and rent for manufacturing spaces - are added to inventory as part of the production cost. On the other hand, administrative or non-manufacturing expenses - such as office staff salaries, costs tied to non-production facilities, and interest - aren't included in manufacturing overhead. Instead, these are categorized as period costs and should be expensed immediately.

To pick the right allocation base, think about how complex your operations are and how resources are being used. This ensures overhead costs are distributed fairly. Here are some common methods:

The choice depends on how diverse your production processes are and how much detail you need for making decisions.

To tackle a large overhead variance, start with a detailed variance analysis to uncover the root causes. Compare the actual costs to the budgeted figures and determine whether the variances are favorable or unfavorable. Look into potential reasons, such as changes in rates, inefficiencies, or errors in allocation.

Adopting accurate allocation methods, like activity-based costing, can provide better insights into cost drivers. Additionally, keeping a close eye on overhead costs through regular monitoring can help minimize the likelihood of significant variances in the future.