Published on

December 21, 2025

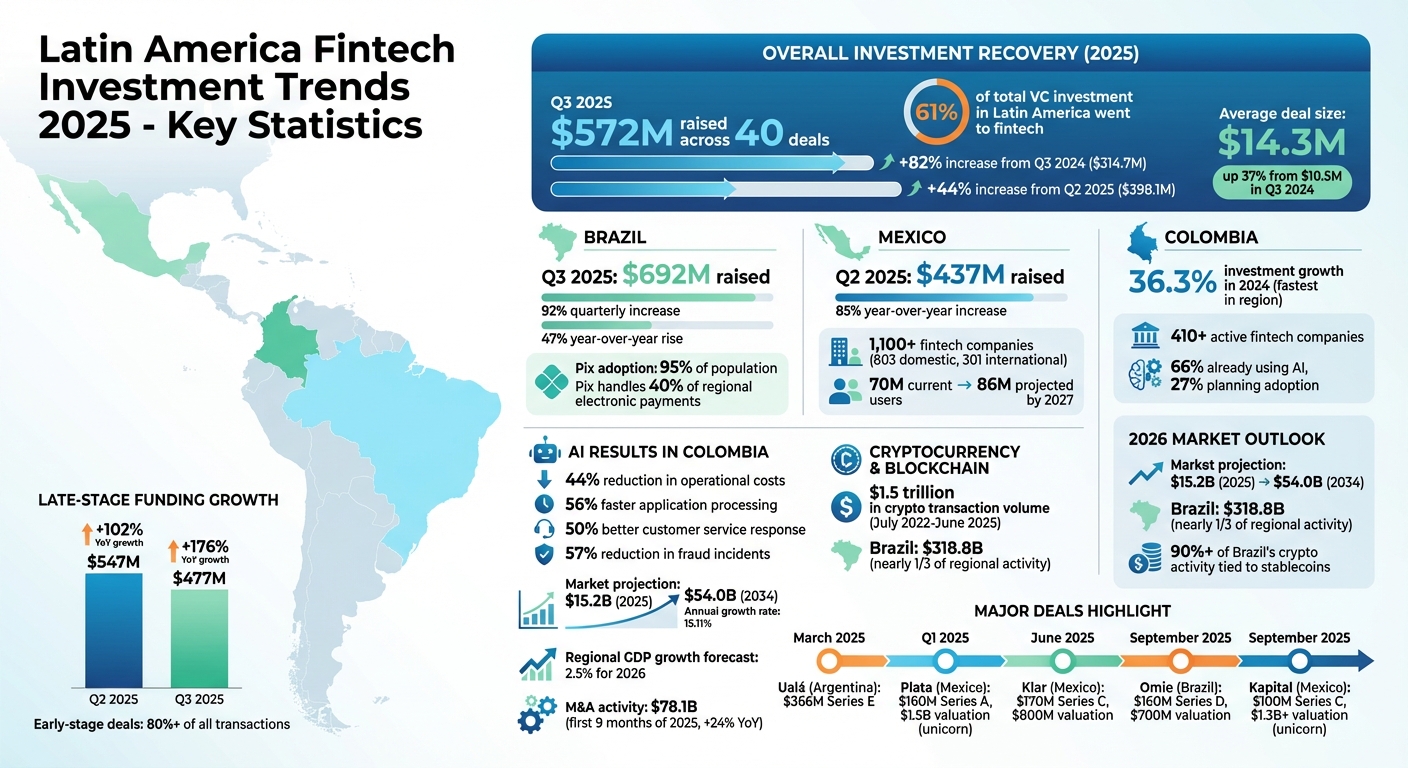

Latin America's fintech sector rebounded strongly in 2025, accounting for 61% of venture capital investment in the region. Key highlights:

Latin America's fintech landscape is evolving, emphasizing financial discipline and sustainable growth as it moves into 2026.

Latin America Fintech Investment Growth 2024-2025: Key Statistics and Market Trends

Latin America's fintech scene made a strong comeback in 2025 after the "VC Winter" of 2024. In Q3 2025 alone, fintech companies raised $572 million across 40 deals. This marked an 82% jump compared to the $314.7 million raised in Q3 2024 and a 44% increase from Q2 2025's $398.1 million [8].

Deal sizes also grew significantly. The average deal size in Q3 2025 hit $14.3 million, up 37% from $10.5 million in Q3 2024 [8]. Late-stage and growth funding saw remarkable gains, with $547 million raised in Q2 2025 - a 102% year-over-year rise - and $477 million in Q3 2025, representing an impressive 176% year-over-year growth [2][3]. Meanwhile, early-stage deals (Pre-Seed and Seed) continued to dominate the market, accounting for more than 80% of all transactions in the region [1]. These numbers reflect not just a broad recovery but also a strategic focus on specific fintech niches, shaping the trends that defined 2025.

Fintech continued to lead as the top sector for venture capital in Latin America, making up 61% of total investment dollars in 2024 and maintaining that dominance into 2025 [1]. However, investor strategies shifted, moving away from the "growth-at-all-costs" mindset to prioritize companies with strong fundamentals and clear paths to profitability [7][9].

Digital banking and neobanking stood out with some of the largest deals of the year. In March 2025, Argentina-based neobank Ualá raised $366 million in a Series E round to fuel its expansion and product development efforts [7]. In June, Mexico City-based digital bank Klar secured $170 million in a Series C round, pushing its valuation to $800 million [2]. Later in September, São Paulo-based Omie, a cloud-based management software provider for small and medium-sized enterprises (SMEs), raised $160 million in a Series D round led by Partners Group, achieving a valuation of $700 million [3].

Specialized lending also emerged as a high-growth area, with a spotlight on vertical-specific solutions like agro-lending and credit infrastructure [7][3]. For example, in Q1 2025, Mexico-based credit and BNPL (Buy Now, Pay Later) company Plata raised $160 million in a Series A round, earning unicorn status with a $1.5 billion valuation [5]. Additionally, AI-driven fraud prevention and regtech gained momentum, spurred by Brazil's financial sector reporting R$10.1 billion (roughly $1.88 billion USD) in fraud-related losses during 2024 [3].

"Fintech remains the region's No. 1 funded sector because trust, access and agency are still the biggest pain points for consumers and businesses." - Diana Narváez, Principal and Head of LatAm Investments, Flourish Ventures [3]

These targeted investments highlight the evolving priorities and new opportunities emerging in Latin America's fintech landscape.

Delving into specific countries within Latin America, we see a variety of factors driving fintech investments and innovation.

Brazil continues to lead Latin America's fintech scene, raising $692 million in Q3 2025 - marking a 92% quarterly increase and a 47% rise year-over-year [13][3]. This impressive growth reflects a renewed focus on growth-stage companies that combine financial services with practical tech solutions.

One standout is Pix, the instant payment system that's been adopted by 95% of the population and now handles 40% of regional electronic payments [12]. In September 2025, NG.CASH, a digital platform popular with Gen Z and boasting over 3 million active accounts, secured $26.5 million in Series B funding from New Enterprise Associates, a16z, and Monashees. The funds aim to enhance regulated stablecoin accounts and AI-powered underwriting [8].

Meanwhile, fraud remains a pressing issue, with the financial sector reporting losses of R$10.1 billion (approximately $1.88 billion) in 2024. This has led to increased investments in AI-driven fraud detection tools [13][3]. With 87% of Brazilians living in urban areas and 30% to 50% still underbanked, the market offers vast potential for mobile-first financial platforms. The focus has shifted from rapid growth to operational efficiency, customer retention, and sustainable business models. These factors set the stage for regulatory advancements and cross-border developments in Mexico.

Mexico, home to over 1,100 fintech companies (803 domestic and 301 international), briefly outpaced Brazil in venture capital funding during Q2 2025, raising $437 million, an 85% year-over-year increase [2][14]. This surge has been fueled by the payments and remittances sector, which benefits from the high volume of cross-border transactions with the United States. Currently, more than 70 million Mexicans use fintech services, a number projected to grow to 86 million by 2027 [14].

In September 2025, digital bank Kapital, backed by Y Combinator, secured $100 million in Series C funding led by Pelion Venture Partners and Tribe Capital. This funding round pushed Kapital's valuation beyond $1.3 billion, earning it unicorn status [3].

Mexico's National Digital Finance Strategy (2025–2030) aims to position the country as a regional hub for digital finance by modernizing regulations and making the 2018 Fintech Law more flexible [14]. Stablecoins are gaining traction as a faster and cheaper option for cross-border payments compared to traditional methods. Additionally, 75% of fintechs in Mexico now collaborate with traditional financial institutions, while 68% have integrated AI into their operations for analytics and security [14]. Colombia, too, is embracing AI in its fintech sector, but with a unique focus.

Colombia experienced the fastest investment growth among major regional markets in 2024, with a 36.3% increase, outpacing Brazil's 7.9% and Mexico's 2.8% [9]. The country has shifted from rapid startup growth to a more strategic phase, hosting over 410 active fintech companies that now prioritize AI integration and operational efficiency [9].

Currently, 66% of Colombian fintechs are using AI, with another 27% planning to adopt it [9]. These companies report impressive results, including a 44% reduction in operational costs, a 56% decrease in application processing times, and a 50% improvement in customer service response times. Among the 56% of firms using AI-driven fraud controls, fraud incidents have dropped by an average of 57% [9].

"AI implementation has moved beyond experimental phases to deliver measurable business impact in Colombia." – Galileo [9]

In 2025, priorities in Colombia shifted from securing financing and launching new products to focusing on technology adoption and automation [9]. The country is also preparing to launch Bre-B, its first interoperable instant payments system spearheaded by the central bank. This initiative is expected to replicate the success of Brazil's Pix, while also generating valuable data for AI-driven financial services [10]. However, challenges remain: 90% of Colombian fintechs cite excessive bureaucracy, and 80% point to institutional rigidity as barriers to working with traditional banks [9].

Three key technologies - blockchain, artificial intelligence (AI), and regulatory technology (Regtech) - are transforming how fintech operates in Latin America. These innovations tackle challenges like financial exclusion, inefficiency, and the complexities of compliance, drawing significant attention from investors.

Blockchain has created a new financial framework, enabling Latin Americans to invest across borders and transact without relying on traditional banks. From July 2022 to June 2025, the region saw an impressive $1.5 trillion in cryptocurrency transaction volume[16]. Brazil alone accounted for $318.8 billion, making up nearly a third of the region’s crypto activity[16].

Stablecoins, in particular, have become a vital tool for cross-border payments, allowing businesses to send invoices and receive payments seamlessly. In Brazil, over 90% of crypto activity is tied to stablecoins. Meanwhile, in Argentina, Colombia, and Brazil, stablecoins make up more than 50% of exchange transactions during the same period[16]. This trend is fueled by inflation and currency instability, especially in countries like Argentina and Venezuela, where stablecoins act as a safeguard against economic uncertainty.

"Stablecoins serve as a parallel financial system, offering both a hedge and a practical payments tool where local currencies often fail to provide stability." – Chainalysis Team[16]

Traditional financial institutions are also stepping into the crypto space. Brazil’s Virtual Assets Law (BVAL), implemented between 2022 and 2025, positioned the Banco Central do Brasil as the regulatory authority for anti-money laundering and counter-terrorism financing (AML/CFT). This regulatory clarity allowed platforms like Nubank and Mercado Pago to bring crypto services to millions of users[16]. In March 2025, Binance, a Cayman Islands–based crypto exchange, completed a $2 billion venture capital raise, signaling ongoing confidence in large-scale digital asset platforms across the Americas[6].

While blockchain transforms financial access, AI is revolutionizing efficiency and customer engagement across the region.

AI has moved beyond the experimental stage to deliver real-world results. In Colombia, 66% of fintechs already use AI, and another 27% plan to adopt it soon[9]. Companies leveraging AI report 44% lower costs, 56% faster processing, and 50% better customer service response times[9]. Additionally, AI-powered fraud controls have reduced incidents by an average of 57%[9].

AI is also changing the game in credit scoring, using alternative data to evaluate underbanked populations. Tools like Cyberbank Konecta, a conversational AI platform, are improving customer interactions and response times in Colombia’s fintech sector[9].

"AI implementation has moved beyond experimental phases to deliver measurable business impact in Colombia." – Galileo Financial Technologies[9]

As AI reshapes operations, Regtech is stepping in to simplify compliance in a rapidly evolving regulatory landscape.

Regtech adoption is accelerating as governments across Latin America roll out new regulations addressing fraud, Banking-as-a-Service (BaaS) licensing, and data privacy. Startups expanding into new markets need tools that enable them to adapt, comply, and audit regulatory requirements efficiently. AI-powered Regtech solutions are shifting compliance processes from manual checks to real-time, automated monitoring.

In Colombia, 90% of fintechs cite excessive bureaucracy as a major hurdle when working with traditional banks, driving demand for automated compliance systems[9]. Companies using AI in operational tasks report 44% cost savings and 56% faster processing times[9]. Core areas fueling Regtech demand include tax auditing, AML, Know Your Customer (KYC) protocols, and compliance with data privacy laws like Brazil’s LGPD.

"Startups are expecting and understand the need for more clarity as well, hence their demand for technology that will allow them to adjust, comply, report and audit new rules quickly." – Camila Vieira, QED Investors[10]

The rise of instant payment systems like Brazil’s Pix has made fraud prevention a top priority across the region. As investors in 2025 focus on profitability and strong fundamentals, fintechs are increasingly turning to Regtech to streamline compliance and improve operational efficiency.

After the recalibration of 2025, the fintech scene in Latin America is shifting gears. The emphasis is no longer on unchecked hypergrowth but rather on what industry experts are calling "intelligent growth." This approach prioritizes profitability, operational efficiency, and sustainable business models. Investors are increasingly drawn to infrastructure projects that quietly but effectively underpin the region's financial systems. Let’s take a closer look at what the future holds for funding and exits in 2026.

A fresh wave of venture capital funding is expected in 2026. Between 2021 and 2023, 106 venture capital firms raised funds in the region, and many of those firms are now nearing the end of their typical three-year fundraising cycles. This timing sets the stage for a new influx of capital, particularly for startups that demonstrated operational efficiency in 2025[15].

Late-stage funding is now guided by the "Rule of 40", which combines growth and profitability to reach a 40% benchmark. Investors are focusing on businesses with strong unit economics, efficient use of capital, and sustainable growth, rather than chasing high-risk, speculative ventures. Fintech is returning to its roots, emphasizing infrastructure, precision, and execution.

Certain sectors are expected to dominate funding in 2026. These include B2B infrastructure providers, cross-border payment systems, compliance automation platforms, and tools for credit and risk management[19]. Real-time payment solutions, such as those complementing Brazil’s Pix system, are particularly appealing to investors. Meanwhile, artificial intelligence has moved beyond experimentation to become a critical component in areas like credit decision-making, fraud prevention, and insurance claims processing[19].

The growth potential of Latin American fintech is substantial. The market is projected to expand from $15.2 billion in 2025 to $54.0 billion by 2034, with an annual growth rate of 15.11%[17][20]. Coupled with a forecasted regional GDP growth of 2.5% for 2026, the macroeconomic environment appears stable enough to support continued investment[18].

Liquidity remains a challenge in Latin America's venture capital ecosystem, but clearer exit paths are starting to emerge. In 2026, the IPO market is expected to reopen, particularly for profitable infrastructure companies and cross-border payment networks[19].

Several fintech companies are well-positioned for potential exits. Mexico City-based Klar and Argentina’s Ualá, both of which secured significant funding in 2025, are strong IPO or acquisition candidates[2][11]. Brazil’s Agibank, valued at $1.5 billion in 2024, is another potential IPO contender as liquidity conditions improve[15].

Mergers and acquisitions (M&A) activity is also set to pick up pace. Consolidation within the fintech space is being fueled by companies acquiring niche providers in areas like KYC, collections, and risk management to build more comprehensive platforms[19]. A notable example is Visma, a Norwegian software company, acquiring Chilean building-management platform Comunidad Feliz for approximately $70 million in late 2025[19]. The appetite for strategic acquisitions is evident, as M&A activity in Latin America reached $78.1 billion during the first nine months of 2025, marking a 24% increase compared to the same period in 2024[18].

For growth-stage fintechs aiming for these liquidity events, financial discipline is key. Companies need to showcase clear paths to profitability, efficient use of capital, and scalable operations to attract buyers or prepare for public offerings. Services like those offered by Phoenix Strategy Group (https://phoenixstrategy.group), which provides fractional CFO support, financial planning and analysis, and M&A advisory, can be instrumental in helping fintechs establish the financial rigor and reporting systems necessary for successful exits.

In 2025, Latin America's fintech sector demonstrated remarkable resilience, bouncing back from earlier challenges. The third quarter highlighted a shift in focus toward capital efficiency, with investors prioritizing profitability over rapid expansion. Fintech remained a dominant force, accounting for 61% of total venture capital investment[1], largely fueled by the ongoing demand for financial inclusion - over 57% of fintechs now cater to unbanked or underbanked populations[4].

Technology adoption has become central to operations, with AI enhancing areas like credit scoring, fraud detection, and risk management. Stablecoins are gaining momentum as a practical tool for cross-border payments, while advancements in regulatory technology are helping institutions streamline compliance processes. Brazil's well-established instant payment systems and Colombia's growing open finance initiatives exemplify how regulatory progress can unlock new opportunities. These technological and regulatory developments are reshaping the competitive landscape across the region.

Funding trends also reveal an evolving geographic dynamic. While Brazil reclaimed its lead in Q3, other fintech hubs are maturing as well. Argentina's Ualá raised $366 million in the first half of 2025[11], and emerging markets like Peru and Ecuador are experiencing annual growth rates of 44%[4].

Looking ahead to 2026, the market appears set for renewed venture capital activity as funds complete their three-year cycles. This optimism builds on Q3's strong performance, where late-stage funding saw a 176% year-over-year increase[3]. The trends discussed throughout this article underscore a critical takeaway: financial discipline is no longer optional.

For growth-stage fintechs, establishing solid financial systems and clear paths to profitability is essential. Phoenix Strategy Group (https://phoenixstrategy.group) specializes in providing fractional CFO services, financial planning and analysis, and M&A advisory to help fintechs meet the operational standards that today’s investors and acquirers demand.

The surge in fintech investments across Latin America in 2025 was driven by a combination of structural shifts and economic momentum. With a young, tech-savvy population, the region has quickly adopted digital solutions, fueling demand for online payments, credit, and insurance services. This wave of interest was further amplified by a resurgence in venture capital activity after a more cautious 2024, as both local and international investors poured funds into fintech companies with scalable business models.

Macroeconomic and political stability also played a major role. Smooth government transitions, broader internet access, and an expanding pool of tech talent positioned Latin America as a prime target for private investment. Payment-focused fintech startups, which make up over 50% of the sector, have been particularly attractive due to their rapid growth potential. Amid this thriving ecosystem, Phoenix Strategy Group has been instrumental in guiding growth-stage fintech firms. They offer strategic and financial advisory services, helping these companies secure funding and prepare for successful exits.

Stablecoins are reshaping how payments and value preservation work across Latin America. Take Brazil, for example - over 90% of crypto transactions now involve stablecoins tied to the Brazilian real, such as BRLV. This particular stablecoin connects seamlessly with Brazil's Pix payment system and the DREX settlement platform. By doing so, it helps reduce the impact of currency fluctuations and makes cross-border transactions smoother. For both individuals and businesses, this means access to a financial tool that’s more stable and efficient.

Meanwhile, artificial intelligence (AI) is playing a pivotal role in helping fintech startups across the region scale and increase profitability. AI is streamlining processes like risk assessment, tailoring financial products to individual needs, and improving customer service. These advancements allow fintech companies to move away from aggressive growth tactics toward more sustainable business operations. This shift has caught the attention of venture capitalists, driving a surge in fintech investments in Latin America. The widespread adoption of digital identities and the popularity of Pix further enhance AI's impact, creating a cycle of continuous innovation and expansion.

Together, stablecoins and AI are transforming the fintech landscape, offering both stability and operational efficiency. Companies such as Phoenix Strategy Group are well-positioned to help fintech businesses harness these technologies to scale effectively, secure investment, and prepare for future opportunities in this fast-evolving market.

Venture capital funding in Latin America's fintech sector is projected to level out by 2026, with investors shifting their attention to later-stage companies that can showcase profitability and meet regulatory standards. Unlike the early-stage, high-growth rounds that were widespread during the 2019–2021 surge, these types of investments are expected to take a backseat. Instead, areas like payments, digital banking, AI-powered tools, and logistics technologies - particularly those linked to nearshoring trends - are likely to attract the most interest. While the total amount of funding might dip slightly, average deal sizes could increase as investors focus their resources on a smaller number of high-potential ventures.

Opportunities for exits are expected to stay limited, with strategic acquisitions and secondary sales becoming more common than IPOs. A combination of tight liquidity and cautious market attitudes makes large public exits unlikely, stretching the timeline for investors to see returns. For fintech founders, the key to navigating this shifting environment will be to prioritize sustainable growth strategies and careful capital management.