Published on

March 21, 2026

A Lean CFO focuses on reducing waste and improving cost control by aligning financial insights with production efficiency. Traditional CFOs often track broad metrics, but Lean CFOs dive deeper - analyzing the total cost per unit, including overhead, quality issues, and waste. Their goal is to identify inefficiencies across departments and translate them into actionable financial strategies.

Key takeaways:

Lean CFOs also empower production teams by showing how their decisions impact the bottom line, turning waste reduction into a shared responsibility. This approach not only improves profitability but also supports long-term growth.

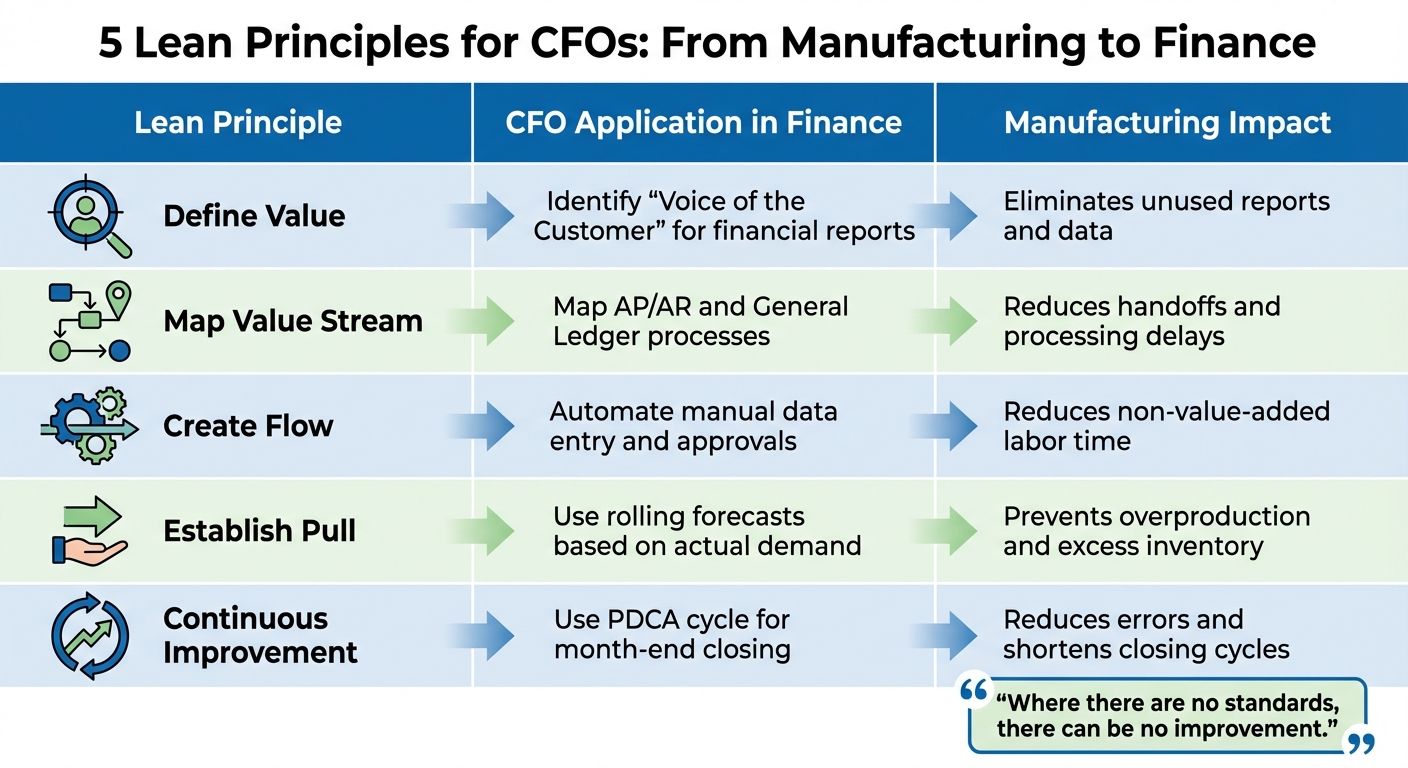

5 Lean Principles Applied to CFO Finance Operations

CFOs who adopt lean principles can turn operational improvements into measurable financial results by eliminating activities that don’t add value. The challenge lies in adapting lean manufacturing concepts into financial strategies that deliver clear cost savings.

The five foundational lean principles offer CFOs a structured way to identify and eliminate waste. Defining value starts with understanding what customers are willing to pay for [5]. By focusing on the "Voice of the Customer", CFOs ensure resources are directed toward activities that enhance value while speeding up the order-to-delivery process [3][5].

Mapping value streams helps visualize the flow of financial processes, such as accounts payable and receivable. This exercise uncovers inefficiencies like redundant handoffs, approval delays, and rework [1][4]. Creating flow involves standardizing these processes, often through automation and simplified approval systems [1][4].

Establishing pull systems ensures that both production and financial planning are driven by real demand instead of forecasts. For manufacturing, this means optimizing inventory to free up capital [1]. In finance, rolling forecasts based on actual demand help avoid overproduction and unnecessary spending [4].

Pursuing continuous improvement relies on tools like the Plan-Do-Check-Act (PDCA) cycle and root cause analysis to address recurring issues. This approach shifts organizations from static budgets to more adaptive, rolling forecasts [4][5].

"Where there are no standards, there can be no improvement."

- Transformative CFO [5]

Lean efforts often fail - over 70% of the time - when they focus solely on internal processes without prioritizing customer value [3]. By keeping customer needs at the forefront, CFOs can ensure that continuous improvement efforts translate into meaningful financial gains. These principles streamline operations while shaping effective financial strategies, which are explored further in their application to finance.

CFOs apply lean principles to finance by turning them into actionable strategies that cut waste and improve profitability. Activity-Based Costing (ABC) is one such tactic, assigning costs to specific activities or products based on actual resource use. This method highlights offerings that consume excessive resources compared to their value, helping CFOs identify key cost drivers and focus on areas for improvement [1][4].

Zero-based budgeting is another tool, requiring justification for every expense instead of simply carrying over past budgets. This approach curbs unchecked administrative growth and ensures every dollar spent adds value [1]. CFOs also evaluate opportunity costs by analyzing the financial return tied up in excess inventory or idle equipment. This helps prioritize waste reduction projects that deliver the greatest financial impact [1].

| Lean Principle | CFO Application in Finance | Manufacturing Impact |

|---|---|---|

| Define Value | Identify "Voice of the Customer" for financial reports | Eliminates unused reports and data [5] |

| Map Value Stream | Map AP/AR and General Ledger processes | Reduces handoffs and processing delays [4] |

| Create Flow | Automate manual data entry and approvals | Reduces non-value-added labor time [1] |

| Establish Pull | Use rolling forecasts based on actual demand | Prevents overproduction and excess inventory [4] |

| Continuous Improvement | Use PDCA cycle for month-end closing | Reduces errors and shortens closing cycles [5] |

Empowering operations leaders with financial knowledge allows them to make production decisions that align with financial goals [1]. For instance, when shop-floor supervisors see that a 5% scrap rate on a $2 million annual material spend equals over $100,000 in waste, they become active participants in reducing inefficiencies rather than passive observers [1].

CFOs play a critical role in identifying inefficiencies, translating them into dollar terms, and prioritizing areas with the highest potential for savings. They also keep an eye on patterns across departments to track progress and areas needing attention [1]. The real challenge lies in accurately quantifying each type of waste - this precision is essential for making a strong case for targeted investments in reducing inefficiencies.

Transport and Inventory Wastes are prime examples of inefficiencies that tie up capital. Instead of relying on rough estimates, CFOs calculate inventory carrying costs with precision. For transportation waste, they measure unnecessary expenses tied to material movement and interdepartmental handoffs [1]. Considering that material costs make up 40–60% of total manufacturing expenses, even small improvements in these areas can lead to noticeable margin gains [1].

Motion and Waiting Wastes are another significant drain, reducing productivity through inefficient workflows and idle time. To tackle this, CFOs use time-and-motion studies to compare actual labor hours against established standards. These analyses reveal inefficiencies like employees wasting time looking for tools, navigating poorly designed spaces, or waiting for approvals. When you factor in fully-loaded labor costs - which include payroll taxes, benefits, and workers' compensation - a $25/hour wage can easily cost the company $40–$45/hour [1]. Bottleneck and utilization analyses further help identify delays and prioritize equipment upgrades to eliminate these inefficiencies [1].

Overprocessing and Overproduction Wastes stem from producing more than needed or adding unnecessary steps to processes. CFOs identify overproduction by analyzing discrepancies between forecasted and actual demand, then calculating the working capital tied up in surplus finished goods. For overprocessing, they separate tasks that add value from those that don’t, noting that 80–90% of business process tasks often fail to deliver customer value [2]. Activity-based costing highlights which products or processes consume disproportionate resources, making it easier to pinpoint and eliminate redundant steps.

Defects and Unused Talent Wastes carry both direct costs and missed opportunities. Beyond tracking scrap rates, CFOs calculate the total cost of quality, which includes scrap materials, rework labor, inspection time, warranty claims, and even customer dissatisfaction [1]. They also analyze labor allocation to uncover situations where skilled employees are stuck performing low-value, repetitive tasks that could be automated. The hidden cost here is the missed opportunity for innovation and process improvement. Eliminating just 5–10% of these overhead costs can boost operating margins by 1–2 percentage points in many manufacturing businesses [1]. By clearly quantifying these waste categories, CFOs can leverage specialized tools to implement effective cost-control strategies.

Activity-based costing (ABC) is a standout tool for CFOs aiming to streamline operations. Unlike traditional methods that rely on broad averages to allocate overhead, ABC assigns costs to individual activities based on specific drivers. This approach highlights exactly where resources are being consumed inefficiently. Companies using ABC often find overhead savings of 20–30%, as it identifies production steps that consume resources but fail to add value [6][9][2].

Cash flow forecasting works hand-in-hand with ABC by tackling waste before it occurs. By aligning cash flow forecasts with just-in-time production schedules, businesses can significantly cut holding costs - often by 15–25% - by ensuring purchases are based on actual demand rather than projections [7][9]. This method directly addresses common inefficiencies like excess inventory and overproduction while maintaining the agility needed to adapt to changing market conditions.

KPI dashboards bring everything together by providing real-time insights into critical metrics, such as cycle time, defect rates, inventory turnover, and Overall Equipment Effectiveness (OEE). These dashboards pull data directly from ERP systems, allowing CFOs to identify waste as it happens instead of waiting for monthly reports. Companies that implement these tools have reported productivity gains of 0.5% and material waste reductions of 2.2% in targeted processes [6][8]. Key metrics to track include inventory turnover (to address overproduction), defect rates (to monitor quality), cycle time (to reduce waiting and motion waste), and value-added ratios (to identify overprocessing). By integrating these tools, businesses can not only measure waste reduction but also use the data to guide specialized advisory services for lean optimization.

Phoenix Strategy Group offers fractional CFO services tailored to growth-stage manufacturers, focusing on aligning financial planning with operational efficiency. They specialize in creating custom ABC models and advanced cash flow forecasting, which are particularly effective for businesses implementing just-in-time systems. This level of precision in financial oversight directly impacts inventory costs and overall efficiency.

Their FP&A systems are seamlessly integrated with ERP platforms, enabling continuous monitoring of waste metrics. These systems automate the tracking process through customized dashboards, allowing for predictive financial adjustments that help prevent cost overruns. For manufacturers looking to scale, attract funding, or prepare for acquisition, Phoenix Strategy Group's integrated models provide a clear view of ROI on lean initiatives. By combining bookkeeping, FP&A, and M&A analytics, their approach translates waste reduction into measurable outcomes that appeal to investors and acquirers. This data-driven strategy turns operational improvements into a competitive edge.

Lean CFOs take the insights gained from waste measurement and apply them through focused audits to create meaningful cost controls.

Waste audits put lean principles into action by translating waste metrics into financial terms. To start, establish financial baselines by documenting all costs before implementing lean initiatives. This allows for clear before-and-after comparisons, making it easier to validate ROI. For example, converting operational metrics like scrap rates into dollar values highlights the financial impact of inefficiencies [1].

A detailed labor cost analysis should include all associated expenses - benefits, payroll taxes, workers' compensation, and indirect support costs. Often, these audits reveal that 15–25% of total labor expenses go toward activities with minimal value [1]. These insights can identify opportunities where automation delivers better returns than manual processes.

It’s also crucial to identify inefficiencies across different functions. Audit data should evaluate inventory carrying costs and the effects of bulk purchasing, as discussed earlier. Using zero-based budgeting for overhead expenses - where every expense must be justified rather than carried forward - can lead to overhead reductions of 5–10%, improving operating margins by 1–2 percentage points [1].

Once inefficiencies are identified through audits, CFOs can calculate the ROI of automation investments. Automation is particularly effective in areas where manual administrative tasks consume resources without adding value. Tools like integrated activity-based costing systems and ERP platforms help pinpoint which products or customers strain resources without yielding sufficient returns.

For inventory management, statistical analysis provides a more accurate picture of safety stock levels compared to relying on estimates. This often uncovers overstocking issues that unnecessarily tie up working capital [1].

After implementing automation, it’s essential to continuously measure ROI to ensure lasting benefits. For instance, monitoring inventory can help avoid the 20–30% annual carrying costs associated with overstocking [1]. Comparing actual material spending against baseline scrap rates can reveal further cost-saving opportunities.

Sustaining these improvements requires building financial literacy throughout the organization. Training production managers to interpret financial statements and take ownership of P&L for specific product lines fosters accountability. This deeper understanding helps managers see how their decisions affect the company’s financial health [1]. By combining monthly tracking with incentive programs, one-time waste reduction efforts can evolve into ongoing improvement initiatives that align with the broader goals of cost control and waste minimization [1].

The lean CFO approach reshapes how manufacturing businesses tackle waste and manage costs by bridging operational metrics with financial insights. While production teams focus on output and uptime, CFOs use analytical tools to uncover hidden inefficiencies - like high inventory costs, labor expenses that add minimal value, and mismatches between purchasing and production needs [1].

This method delivers tangible results. For example, improving process efficiency can reduce costs by up to 20% without requiring significant capital investment. Similarly, cutting overhead by 5–10% can increase operating margins by 1–2 percentage points [1]. These improvements come from systematically eliminating waste rather than relying on quick fixes, ensuring long-term progress through collaboration and data-driven strategies.

One of the most impactful benefits of the lean CFO approach is how it boosts financial understanding across operational teams. When production managers see how their decisions affect the profit and loss statement, waste reduction becomes a shared, ongoing effort rather than something dependent on constant oversight. This change not only drives continuous efficiency but also prepares companies for strategic growth opportunities.

For mid-sized manufacturers without dedicated financial leadership, Phoenix Strategy Group offers tailored solutions. Their expertise in manufacturing cost accounting and fractional CFO services helps businesses identify waste, prioritize improvements, and implement strategies that lead to lasting cost control. By combining lean principles with financial tools like activity-based costing and ROI analysis, they turn operational inefficiencies into actionable plans that improve profitability and cash flow.

A Lean CFO zeroes in on efficiency, cutting waste, and managing costs, rather than sticking solely to financial oversight or long-term strategic planning. By leveraging data analytics and modern financial planning and analysis (FP&A) methods, they pinpoint areas of inefficiency and work to boost profitability.

Unlike a traditional CFO, who might focus on broader financial responsibilities, a Lean CFO takes a more hands-on role. Their approach integrates financial practices directly with operational improvements, ensuring resources are used effectively and driving ongoing efficiency across the organization.

To cut costs effectively, start by keeping a close eye on material waste, inventory waste, energy waste, and process waste. Concentrate on the metrics that impact your finances the most and streamline your operations for better efficiency.

Proving ROI for lean changes means focusing on financial savings, improvements in operational efficiency, and reductions in environmental impact. Tools like real-time data analytics, waste audits, and digital tracking systems play a key role in this process. These methods often deliver concrete results, such as saving 12–18% on procurement costs and boosting EBITDA by up to 15%.