Published on

March 31, 2026

Managing loyalty program accounting can be tricky, but getting it right is essential for accurate financial reporting and compliance. Here's what you need to know:

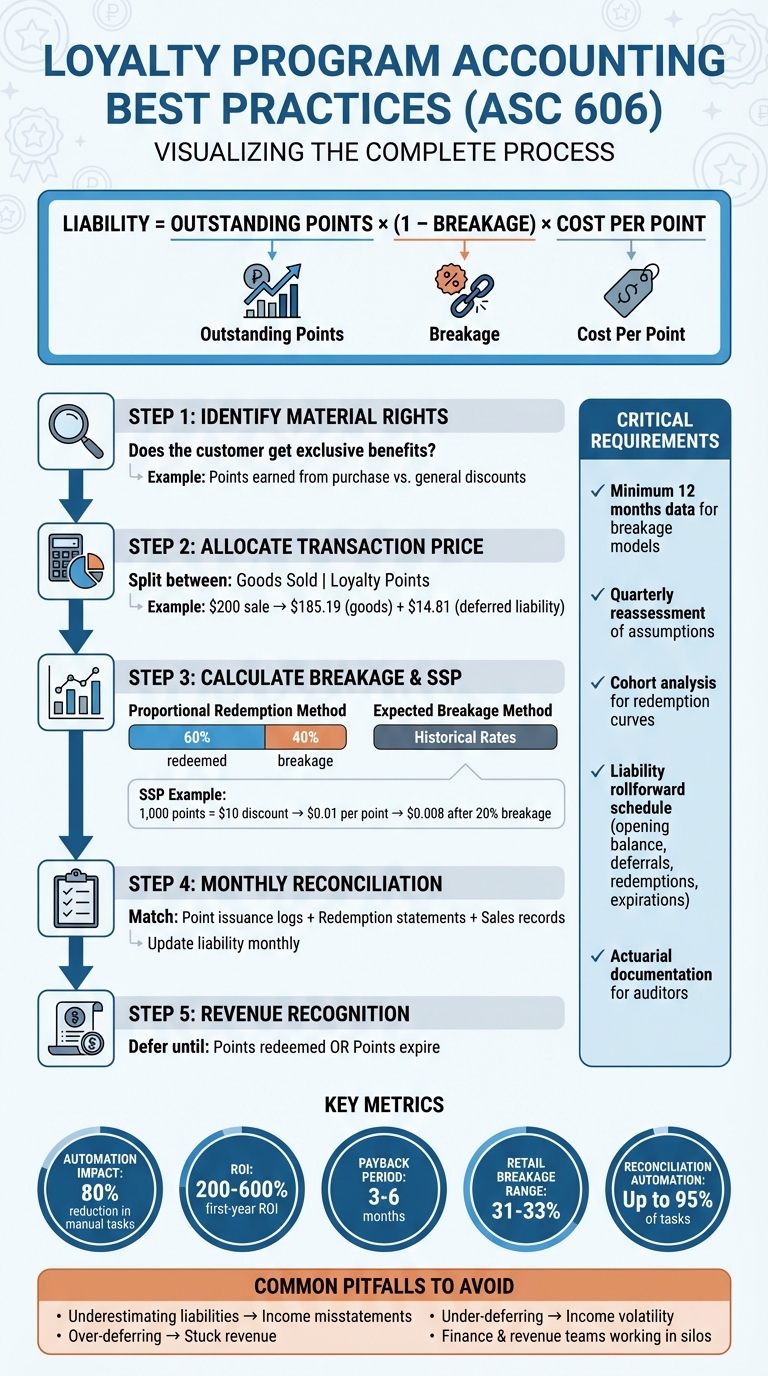

Loyalty Program Accounting Process: ASC 606 Compliance Steps

ASC 606 (Revenue from Contracts with Customers) is a framework developed by the FASB and IASB that introduced a new way of accounting for loyalty programs [5]. It emphasizes the importance of accurately tracking liabilities, which is a recurring theme in this guide. Under ASC 606, businesses must identify distinct performance obligations within a contract instead of treating a sale as a single event.

If loyalty points offer a material right, they are treated as a separate performance obligation [5]. This means part of the initial sale price is deferred as a liability on the balance sheet, with revenue recognized only when customers redeem the points or when the points expire [5]. Essentially, the sale is split into two accounting events: the immediate delivery of goods and the future fulfillment of rewards.

To determine whether a loyalty benefit qualifies as a material right under ASC 606, the focus is on exclusivity. A material right exists when customers gain an option to purchase additional goods or services at a discount or on terms unavailable to others [5]. The key question is whether the benefit is tied specifically to the contract. If a customer wouldn’t receive the same discount without making the original purchase, it likely qualifies as a material right.

"A material right exists when a customer has the option to buy additional goods or services at a discount or on terms that are not available to others." - Stripe [5]

For example, standard discounts open to everyone - like a 10% sign-up offer for all new customers - don’t qualify as material rights because they lack exclusivity. These discounts simply lower the transaction price of the current sale and don’t require tracking as a liability.

Once material rights are identified, the next step is allocating the transaction price. This involves dividing the transaction price between the goods sold and the loyalty points, using relative standalone selling prices (SSPs). Adjustments are also made for breakage - the percentage of points expected to expire without being redeemed [5]. Since loyalty points are rarely sold separately, their SSP is estimated using methods like the adjusted market assessment approach, the expected cost plus margin approach, or the residual approach [5].

Here’s an example: Suppose a $200 sale generates loyalty points with an expected value of $20, and you estimate 20% breakage. After adjusting for breakage and relative SSPs, the liability for the material right might be approximately $14.81 [1]. The formula for calculating liability is:

Liability = Outstanding Points × (1 – Breakage) × Cost Per Point [3].

Accurate allocation is crucial to avoid income volatility and audit issues, as discussed earlier. Many organizations leverage fractional CFO services to manage these complex revenue recognition requirements and ensure compliance. Revenue assigned to loyalty points remains deferred until customers redeem the points or they expire [5].

Getting breakage and standalone selling price (SSP) calculations right is key for tracking liabilities and recognizing revenue accurately. With solid data and consistent methods, these calculations can be managed effectively.

Breakage refers to the points customers earn but never redeem. Recognizing this as revenue requires a controlled and methodical approach, using either the proportional redemption method or the expected breakage method [1].

"Recognize breakage revenue in proportion to the pattern of redemptions or when it's highly probable that recognition will not result in a significant reversal." - Growave [1]

To build a dependable breakage model, you’ll typically need at least 12 months of data on how points are issued and redeemed. A cohort analysis - grouping customers based on when they earned points - can help create a clear redemption curve. Keeping track of the redemption lag (the time between earning and redeeming points) also sharpens forecasting. For newer programs without a full year of data, conservative assumptions are recommended, with quarterly reassessments or updates after any program changes. Adjustments to earn rates or expiration policies, for example, should prompt an immediate remeasurement of liabilities.

Once your breakage model is established, the next step is to calculate the actual value of loyalty rewards.

SSP, like breakage estimation, depends on historical redemption data and requires consistent application. It represents the price customers would pay for rewards if sold separately. Since loyalty points are rarely sold outright, SSP is often estimated by dividing the average retail value of redeemed rewards by the number of points required, then adjusting for breakage.

Here’s an example: If 1,000 points provide a $10 discount, each point is worth $0.01. With a 20% breakage adjustment, the SSP drops to about $0.008 per point. This approach is both practical and defensible during audits.

"SSP estimation uses historical redemption data, the typical value of rewards, and the probability that an issued option will be exercised." - Growave [1]

Consistency is key - whatever method you choose should be backed by historical data and applied uniformly. Be sure to document your rationale and revisit SSP assumptions quarterly or after major changes to the program. Factoring in seasonal trends or marketing campaigns can help avoid errors in liability reporting.

Keeping your books accurate month after month is no small task. Monthly reconciliation isn’t just about checking a box for compliance - it’s a critical step for catching errors early, maintaining accurate financial records, and steering clear of audit surprises. These processes build on the breakage and SSP models mentioned earlier, ensuring a smooth monthly accounting cycle.

Start by gathering all necessary documentation from your general ledger and loyalty platform. This includes point issuance logs, redemption statements, and sales transaction records [7]. Since ERP systems and loyalty platforms often use different formats for dates, currencies, or reference numbers, normalizing this data is crucial to avoid mismatches [7]. Once normalized, match transactions - whether they’re one-to-one, one-to-many, or many-to-many [7][3].

Be sure to separate timing differences, like points earned on March 30 but clearing on April 2, from actual discrepancies, which could indicate system errors or even fraud [7]. Once discrepancies are resolved, update your liability using this formula:

Liability = Outstanding Points × (1 – Breakage) × Cost Per Point [3]

Then, make the required journal entries to shift deferred revenue into recognized revenue as redemptions occur [3].

"Teams that reconcile continuously rather than in a month-end crunch typically close faster and with fewer surprises." - Nigel Sapp, Numeric [7]

For high-volume loyalty programs, frequent reconciliations - weekly or even daily - can make a big difference. Setting specific variance thresholds for different reward types helps you avoid wasting time on insignificant discrepancies. Automation tools can handle up to 95% of manual reconciliation tasks, allowing your team to focus on exceptions [7]. Automated matching tools also help reduce discrepancies, aligning with the best practices discussed earlier.

Once reconciliations confirm your data’s accuracy, the next step is closely monitoring liability changes.

After completing reconciliations, tracking liability changes ensures financial accuracy and compliance with ASC 606. A monthly rollforward schedule should include opening balances, new deferrals, redemptions, expirations (breakage), and adjustments [1]. Under ASC 606, revenue remains deferred until rewards are redeemed or expire [1][3]. Make sure your breakage revenue reflects actual redemption patterns [1].

Keep detailed records of your methodology. Auditors will need clear documentation showing how you calculated your SSP and breakage estimates. If program rules change - such as modifications to earn rates or expiration policies - remeasure your outstanding liability immediately [1]. For particularly complex programs, consider consulting actuarial experts to ensure accurate liability bookings [3].

Centralizing data is another key step. Using a single platform to track points issued, redeemed, and expired can minimize reconciliation issues and help you avoid financial blind spots [1]. Focus your efforts on high-risk accounts that could have a larger financial impact, rather than applying the same level of scrutiny across all accounts [7].

Linking your loyalty platform directly to your accounting system eliminates the need for manual data entry, which often slows down month-end processes and introduces errors. By synchronizing your CRM or billing platform with your ERP in real time, point activity flows seamlessly into your general ledger. This setup ensures compliance with ASC 606 by deferring revenue until points are redeemed or expire. The backbone of this integration is typically ETL (Extract, Transform, Load) pipelines, which organize loyalty activity data in a way that your finance team can easily use for modeling and reporting [8].

When implemented properly, automation can cut manual bookkeeping tasks by as much as 80%. In many cases, businesses see a payback period of just 3 to 6 months, with a first-year ROI ranging from 200% to 600% [6]. Additionally, real-time financial dashboards provide instant visibility into point activity, allowing teams to identify discrepancies and adjust liability estimates quickly [6]. This integration not only simplifies liability tracking but also offers real-time financial insights.

"The failures always happen because - finance and revenue teams working in silos." - Phoenix Strategy Group [8]

To avoid these pitfalls, it's crucial to create a unified workflow where marketing, finance, and operations share the same data source. This approach eliminates the "stuck revenue" issue, where teams over-defer due to overly conservative breakage estimates, and reduces income volatility caused by under-deferring [3].

Using the breakage and SSP models discussed earlier, automated systems can continuously update liabilities as transactions occur. Once integrated, these systems apply breakage and redemption rates to outstanding points in real time, ensuring your balance sheet reflects accurate expected costs without the need for monthly spreadsheet updates [3][4]. Instead of waiting until the end of the month, liability calculations run continuously using the pre-established formula [3].

Some advanced systems even incorporate AI-driven analytics to forecast individual customer behavior, refining breakage estimates beyond basic historical averages [3]. For instance, if your retail program typically experiences breakage rates between 31% and 33%, AI can identify specific customer segments more likely to redeem their points and adjust liability estimates accordingly [4]. This detailed approach not only strengthens documentation for auditors but also helps justify estimates to regulators [3]. Moreover, these automated processes streamline tasks like handling refunds and returns.

When customers return products, your system should automatically reverse any loyalty points they earned from the original purchase. Without this adjustment, your loyalty liability could be overstated, leading to reconciliation challenges. For example, if a customer earned 500 points on a $100 purchase but later returned the item, those 500 points should be deducted from their balance, and your deferred revenue adjusted accordingly. This automated feedback loop ensures accuracy across your financial records and complements the reconciliation processes previously discussed.

For non-cash rewards like free shipping, the system must track these separately since their future costs depend on variables such as order size and destination. The integration should update liability estimates as shipping rates fluctuate. By documenting both points redemption rates (the percentage of points redeemed) and reward redemption rates (how often claimed rewards are fulfilled), you can maintain accurate liability balances even as program dynamics evolve [4].

"What's critical is that the value tied to those points is captured accurately and consistently in your financial reporting." - Alice Cresswell, Marketing Manager, Marsello [4]

Once you've automated and reconciled your loyalty program accounting, the next step is ensuring your financial statements align with ASC 606 disclosure requirements. These disclosures are essential for maintaining trust in your automated processes and demonstrating compliance to auditors and regulators. Financial statements need to detail how performance obligations are identified, how revenue is allocated, and when revenue is recognized - whether upon redemption or expiration of points [3]. This step ties together the automated systems and reconciliation processes discussed earlier, reinforcing their credibility.

Key disclosures include your accounting policy (e.g., whether points are treated as deferred revenue or a discount), the method used to estimate the standalone selling price (SSP), and your assumptions about breakage. These assumptions might involve historical redemption data or cohort analyses [9][10]. Additionally, include a liability roll-forward that breaks down new deferrals, redemptions, expirations, and the split between current and non-current liabilities [9][11].

Your disclosures should clearly explain the accounting methods applied, building on the internal models you've developed. For example, specify earn rates, redemption options, and expiration rules. Explicitly state the method used to calculate the SSP. If you chose the adjusted market assessment approach, make that clear. If you opted for the residual approach due to highly variable pricing, explain why it was appropriate and how it compares to historical stand-alone prices [10].

When it comes to breakage, outline whether it's recognized proportionally as points are redeemed or only when they expire. Include actual redemption and breakage rates, backed by historical data or cohort analyses [4]. Auditors also expect sensitivity testing on these estimates to ensure that there’s no risk of significant revenue reversals [9]. Additionally, provide the "but for" rationale, explaining why your incentives qualify as material rights [10].

It's important to disclose material judgments as they occur. For example, identify which loyalty rewards are considered distinct performance obligations and specify the event that triggers revenue recognition [3]. If you adjust your breakage rate or cost per point assumptions, disclose these changes and their impact on reported revenue for that period [9][11]. Since liability is calculated as:

Liability = Outstanding Points × (1 – Breakage) × Cost Per Point,

any change in these variables will affect your liability [3].

"Actuarial opinions are useful for justifying booked liability... Having a nuanced, granular-level outline of member behavior crafted by actuarial experts wielding potent AI-driven analytics software is an important step towards justifying your company's booked liability to regulators and auditors." - KYROS [3]

Include actuarial reports with detailed graphs, exhibits, and explanations of your methodology to back up your liability assumptions. This evidence not only supports your breakage estimates but also helps prevent "stuck revenue" from over-deferring or income volatility caused by under-deferring [3].

Loyalty program accounting requires precision and automation to handle liabilities effectively. The formula for calculating liability - Liability = Outstanding Points × (1 – Breakage) × Cost Per Point [3] - ensures compliance with ASC 606 by deferring revenue until rewards are either redeemed or expire.

Top-performing businesses streamline their loyalty data on a unified platform, automate liability tracking, and use AI-driven analytics to refine breakage estimates. Take LAFCO, for instance: after implementing a revamped loyalty structure, they saw a 26.72% boost in customer retention and a 23.39% rise in repeat purchase revenue in just three months [2]. Similarly, KBS Research experienced a 14X increase in customer retention within six months of launching their rewards program [2].

By leveraging technology, businesses can improve accuracy, scale operations, and maintain clear audit trails. Tools like automated reconciliations and actuarial reports provide financial clarity and help justify liabilities to regulators and auditors [3].

These practices serve as the cornerstone of effective loyalty program accounting. Documenting policies, revisiting estimates quarterly, and ensuring proper segregation of duties between issuing points and posting journal entries can free up capital, satisfy audit requirements, and create a solid framework for scaling customer engagement - without unexpected financial setbacks.

For companies aiming to streamline financial reporting and ensure compliance, Phoenix Strategy Group provides fractional CFO services, FP&A, and financial advisory support.

Under ASC 606, a material right refers to an option provided to customers that offers a meaningful benefit they wouldn’t receive without entering into the contract. This requires assessment to determine whether it constitutes a separate performance obligation, warranting distinct accounting treatment.

To accurately estimate breakage and point value, it’s crucial to collect data on a few key factors:

These components are the foundation for precise analysis and dependable estimations.

When recording loyalty points, follow these steps:

These accounting practices are consistent with ASC 606 and IFRS 15 standards.