Published on

June 7, 2026

Market comparables, or "comps", are a key tool for determining the value of a manufacturing business. By analyzing the sale prices or financial metrics of similar companies, you can estimate your business's worth. This method works especially well for manufacturers because of their measurable financial profiles and the abundance of transaction data in the sector.

Key Takeaways:

To maximize valuation, focus on addressing risks like customer concentration and enhancing strengths like certifications or recurring contracts. This approach ensures your business aligns with market expectations and attracts competitive offers.

Manufacturing Valuation Multiples by Deal Size & Sub-Sector (2026)

When it comes to valuing manufacturing companies, three key metrics often take center stage, each tailored to specific scenarios.

EV/EBITDA is the primary benchmark for most U.S. manufacturers. By excluding debt, taxes, and depreciation, it offers a clear view of profitability, making it easier to compare companies with varying capital structures. For businesses generating $1M–$25M in revenue, this metric is often the main focus during valuation discussions. [6]

EV/EBIT is more relevant for manufacturers with heavy asset bases, where depreciation plays a significant role. In these cases, buyers often prefer EBIT or "Cash EBITDA" (EBITDA minus average annual maintenance capex) to get a more precise picture of earnings. [3]

EV/Revenue serves as a secondary measure, mainly in high-growth niches like Industrial IoT or electronics. Here, the focus shifts to future potential rather than current earnings. For well-established manufacturers, however, this metric is usually supplementary. [6][5]

For smaller, owner-operated businesses earning less than $1M, Seller's Discretionary Earnings (SDE) is the go-to metric. Unlike Adjusted EBITDA, SDE incorporates the owner's full compensation package, offering a more comprehensive view of the total economic benefit to a single working owner. [5][4]

"There is no single 'manufacturing multiple' in 2026. There is a spectrum from 3x SDE for a sub-$1M owner-operated job shop to 12x EBITDA for a $25M EBITDA medical device CM." - Christoph Totter, Managing Partner, CT Acquisitions [3]

In U.S. manufacturing transactions, valuation multiples are applied to Enterprise Value (EV) - the total operating worth of the business. To determine the seller's actual payout, you subtract any outstanding debt and add back excess cash. [5]

These multiples are typically based on Trailing Twelve Months (TTM) financial performance, ensuring the valuation reflects the most recent and accurate data rather than older averages or speculative forecasts. [5][9]

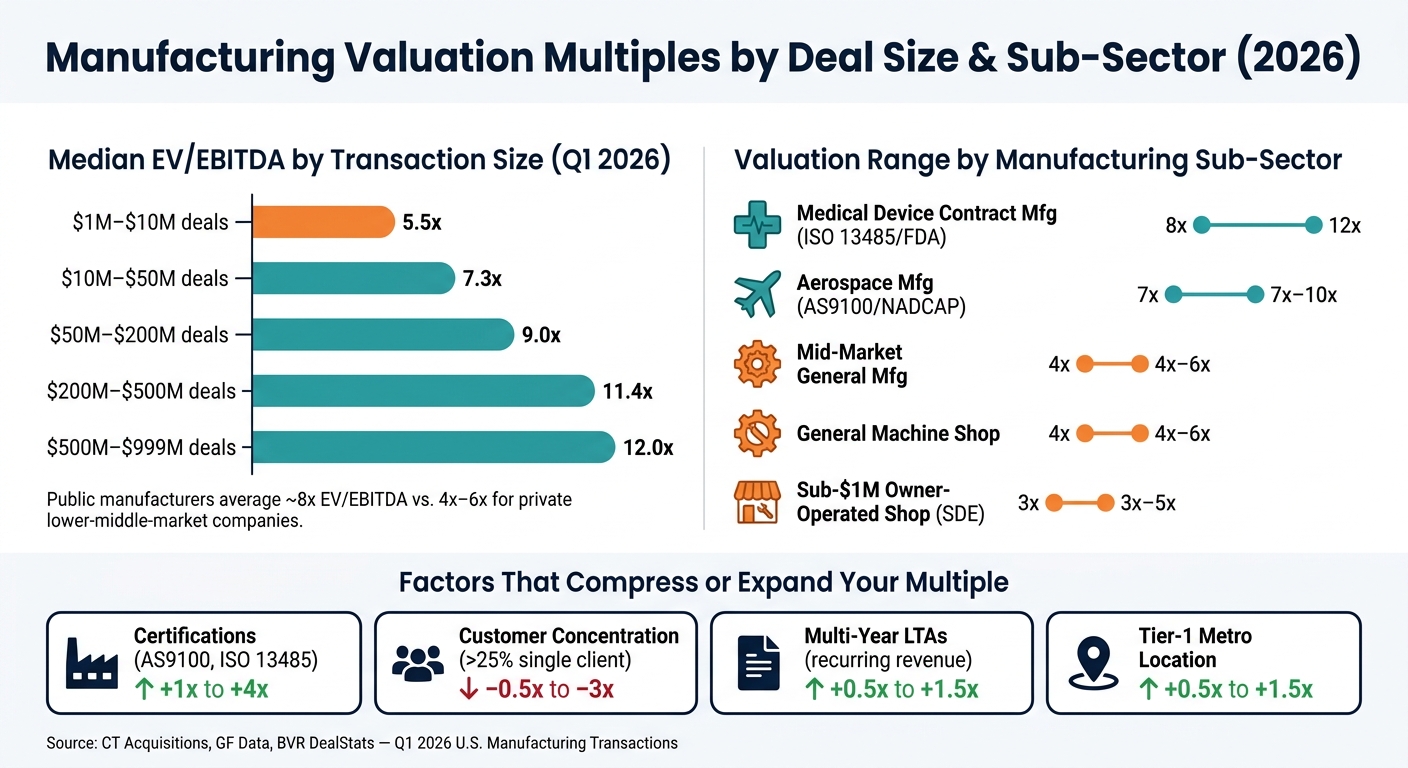

It's crucial to understand the disparity between public and private company multiples. Public manufacturers often trade at around 8x EV/EBITDA, but private companies, especially in the lower middle market, usually fall between 4x and 6x, accounting for size and marketability adjustments. As of Q1 2026, private deals in the $10M–$50M range had a median multiple of 7.3x, while smaller transactions in the $1M–$10M range averaged 5.5x. [5][10]

| Deal Size (Total Enterprise Value) | Median EV/EBITDA Multiple (LTM Q1 2026) |

|---|---|

| $1M – $10M | 5.5x |

| $10M – $50M | 7.3x |

| $50M – $200M | 9.0x |

| $200M – $500M | 11.4x |

| $500M – $999M | 12.0x |

The choice of valuation multiple depends on factors like company size, profitability, and the specific sub-sector.

Size plays a bigger role than many business owners anticipate. A company with $3M in EBITDA might look similar to one with $15M in EBITDA, but the larger business attracts more interest from private equity firms and strategic buyers, driving up its valuation multiple. Smaller businesses, with fewer potential buyers, often see compressed multiples. [11][3]

Sub-sector specialization also impacts valuation. For instance, aerospace manufacturers with AS9100/NADCAP certifications typically achieve 7x–10x EBITDA, while medical device contract manufacturers with ISO 13485/FDA registration can command 8x–12x EBITDA. General machine shops, on the other hand, usually trade at 4x–6x EBITDA. These differences reflect factors like regulatory hurdles, customer loyalty, and market barriers. [3]

"The right manufacturing EBITDA multiple is never a single number from a Pitchbook headline. It's baseline... plus four adjusters that compress or expand the multiple by a turn or two each." - Christoph Totter, Managing Partner, CT Acquisitions [11]

One universal risk factor across all sub-sectors is customer concentration. If a single customer accounts for more than 20%–25% of revenue, the valuation multiple may be discounted by 0.5 to 3.0 turns. To counter this, sellers can address customer concentration issues 12–24 months before going to market, which can significantly improve valuation outcomes. [11][3]

When identifying comparable manufacturing companies, precision is key. Start by narrowing your search with the 6-digit NAICS code that corresponds to your manufacturing activity. For instance, NAICS 332710 applies to machine shops. However, sharing the same NAICS code doesn’t automatically mean two companies are comparable. Consider operational differences: a job shop handling custom one-off orders is fundamentally different from a contract manufacturer with multi-year Long-Term Agreements (LTAs), even if both work with metal parts. [7]

Size is another critical factor. Use a range of 50%–200% of your target company’s revenue or EBITDA to find appropriate peers. This is because valuation multiples don’t scale evenly - a company with $3M in EBITDA will attract a very different buyer pool and valuation than one with $30M in EBITDA. For example, a manufacturer with $10M in EBITDA should be compared to others in the $5M–$30M range, not to a massive publicly traded industrial conglomerate. Beyond size and industry codes, factors like geography and operations help refine the search for true comparables.

Geography plays a big role in valuation. Manufacturers located in Tier-1 metro markets often see a 0.5 to 1.5 turn premium compared to those in rural or economically struggling areas. This is largely due to higher buyer demand and a deeper labor pool in urban markets. [7] If you’re benchmarking a U.S.-based company against European data, factor in a 5%–10% U.S. listing premium to account for differences in market liquidity and investor interest. [12]

Operational factors further help identify true peers. Key considerations include:

For example, a precision machining shop with 70% of its revenue tied to long-term contracts operates very differently from one that secures work project by project. Certifications like AS9100 (aerospace) or ISO 13485 (medical devices) also matter. These certifications create specialized buyer pools and can drive valuation multiples 1 to 4 turns higher than generalist manufacturers. [3][11] These factors aren’t just minor adjustments - they fundamentally determine which companies belong in the same comparison set.

Accurate comparisons require robust data. No single source offers a complete picture, so using multiple databases is essential. Here are some key resources for U.S. manufacturing transactions:

| Data Source | Best For | Cost |

|---|---|---|

| PitchBook | PE-backed deals, deep M&A coverage | Fee-based |

| BVR DealStats | Lower-middle-market private transactions | Fee-based (~$529/day pass) |

| GF Data | Private deals in the $10M–$500M range | Fee-based |

| SEC EDGAR | Public company multiples and large acquisitions | Free |

| BizBuySell | Small and main street manufacturing deals (<$5M) | Free |

| IBBA Market Pulse | Quarterly trend data and broker sentiment | Free |

A key rule: only use transaction data from the past 24 months. [7] Valuation multiples can shift dramatically with changes in interest rates and economic conditions. A deal closed in 2022 reflects a very different financing environment than one in 2025 or 2026. For public company benchmarks, review 10-K filings from strategic acquirers like HEICO or Roper Technologies to see what larger buyers are paying.

"Relative valuation isn't about what your business is worth in some abstract sense. It's about what other people have actually paid for businesses like yours, recently, in similar markets, for similar reasons." - Christoph Totter, Managing Partner, CT Acquisitions [7]

Once you've identified comparable companies, the next step is to ensure a fair comparison. Private manufacturing businesses often handle finances in ways that don't align with economic reality - like running personal expenses through the company or using tax-friendly accounting practices. Adjusting these discrepancies is key to an accurate valuation.

Owner compensation is one of the biggest distortions in private company financials. Business owners may pay themselves more or less than the market rate and often include personal expenses - like family salaries, personal vehicles, travel, or health insurance - as business costs. To get a clear picture, these need to be adjusted to reflect what it would cost to replace the owner with a professional manager.

For smaller businesses earning under $1.5M–$2M, Seller's Discretionary Earnings (SDE) is the go-to metric. This includes the full owner compensation package. For businesses above that range, buyers typically use normalized EBITDA, replacing the owner's pay with a market-rate management cost instead of simply adding it back [13].

One-time or non-recurring items also require adjustments. Examples include a facility relocation, a litigation settlement, or an unusual equipment repair. These should be added back to show the company's true earning power. Document all adjustments thoroughly, as buyers will examine them closely during Quality of Earnings (QoE) reviews. Missing a $100,000 adjustment could cost over $500,000 in deal value with a 5x multiple [4].

If the business owner also owns the building, the rent charged to the company must be adjusted to a fair market rate. Undercharging inflates EBITDA, while overcharging suppresses it - both distort the financial picture [2].

Finally, standardize inventory methods and capital expenditures to align your financials with industry norms.

Many U.S. manufacturers use LIFO (Last-In, First-Out) accounting for inventory because it reduces taxable income during times of rising costs. However, public companies typically use FIFO (First-In, First-Out), making it necessary to convert LIFO-based accounting to FIFO for accurate comparisons. This conversion often increases both reported income and balance sheet strength [8].

When it comes to capital expenditures, separate them into maintenance capex (needed to sustain production) and growth capex (used for expansion). Buyers focus on cash EBITDA rather than headline EBITDA, and the difference between the two can range from 15% to 30% of reported EBITDA in manufacturing [13].

"Buyers underwrite EBITDA − maintenance capex, not headline EBITDA. The gap between the two is often 15–30% of reported EBITDA." - Christoph Totter, Managing Partner, CT Acquisitions [13]

Maintenance capex benchmarks vary by industry. For example, general machine shops typically spend 3%–5% of revenue, while medical device contract manufacturers may spend 6%–10% [13]. Companies that defer maintenance to inflate short-term EBITDA will likely face a valuation reduction when buyers adjust the numbers to match industry standards.

After making adjustments for owner compensation, inventory methods, and capex, you're ready to calculate normalized EBITDA. Start with net income, then add back interest, taxes, depreciation, and amortization. Next, incorporate the adjustments: replace owner compensation with a market-rate management cost, remove non-recurring items, convert inventory to FIFO, and adjust rent to market rates [2][13].

Here's a summary of the key adjustment areas and their purposes:

| Adjustment Area | Action | Rationale |

|---|---|---|

| Owner Compensation | Add back excess; deduct replacement cost | Aligns owner pay with market rates for a professional manager [2] |

| LIFO Reserve | Convert to FIFO | Standardizes inventory value for comparison with peers [2] |

| Maintenance Capex | Deduct from EBITDA | Reflects the true cash cost of maintaining production capacity [13] |

| One-Time Items | Add back (e.g., relocation, litigation) | Removes non-recurring distortions from operational trends [2] |

| Related-Party Rent | Adjust to market rate | Ensures facility costs reflect what a third-party buyer would pay [2] |

The result is a normalized EBITDA that reflects the business's true earning potential under normal operating conditions. This figure is critical because it’s what gets multiplied by your peer comparables to determine valuation.

"EBITDA is a starting point, not a conclusion. Manufacturing companies often require machinery, tooling, maintenance... that can materially affect free cash flow." - James Lynsard, Certified Business Appraiser, Simply Business Valuation [2]

Once you've calculated normalized EBITDA, the next step is to translate it into a valuation range. While the math itself is straightforward, the real challenge lies in selecting and fine-tuning the right multiple.

After determining your normalized EBITDA, you'll need to establish a realistic multiple. Start by collecting EV/EBITDA ratios from comparable companies. For each one, divide its enterprise value by its EBITDA to calculate the multiple. Once you've compiled the full set, remove the top and bottom 10% of the range. These outliers often represent unusual circumstances, such as distressed sales or premium-priced strategic acquisitions, which aren't reflective of typical market conditions [7].

What you're left with is your working range. To anchor your analysis, use the median multiple, not the average. A single high multiple can throw off an average, whereas the median provides a more balanced midpoint. Apply these multiples to your normalized financials to estimate enterprise value.

"Relative valuation isn't about what your business is worth in some abstract sense. It's about what other people have actually paid for businesses like yours, recently, in similar markets, for similar reasons." - Christoph Totter, Managing Partner, CT Acquisitions [7]

Once you've identified the median multiple, the next step is to multiply your normalized EBITDA by that figure to calculate enterprise value (EV). For example, if a precision machining shop has $3.8M in adjusted EBITDA and applies a 6.0x median multiple, the resulting enterprise value would be $22.8M [5]. This forms the foundation for further adjustments specific to private companies.

To convert enterprise value into equity value, subtract net debt and factor in working capital adjustments. For instance, if the business carries $2M in debt, the equity value would drop to $20.8M. These adjustments are critical during deal negotiations and can significantly impact the final valuation.

"The multiple applied to your adjusted EBITDA reflects how a buyer prices the risk and reliability of your future earnings." - Paul Weisinger, Principal and Director of Valuation, Rea Business Advisors [8]

Valuing a private company often requires specific adjustments to account for differences from public companies. Here are three common adjustments:

On the positive side, certain factors can enhance a valuation. For instance, specialized certifications like AS9100 (Aerospace) or ISO 13485 (Medical Devices) can boost multiples by 0.5x to 1.0x, as they attract a more competitive pool of buyers [4][5]. Additionally, manufacturers with domestic supply chains and integrated automation are currently commanding premiums, as these attributes signal resilience and lower operational risks [4].

Market comparables provide a snapshot of how your business stacks up against others in your industry. A below-average multiple often highlights specific operational challenges, such as over-reliance on a few customers, undocumented processes, outdated equipment, or dependence on key employees.

"A company generating $3 million of EBITDA with operational fragility may trade at a lower multiple than a $2.5 million EBITDA business that demonstrates resilience, scalability, and institutional quality." - Nick Fares, President, Summit Capital Advisors [14]

The table below shows how critical operational factors influence valuation:

| Factor | Strength | Weakness |

|---|---|---|

| Production Setup | Modular, scalable, automated [1] | Rigid, high capital expenditure needed for growth [1] |

| Customer Base | Diversified across industries [14] | Over 25% of revenue from a single client [7] |

| Revenue Type | Multi-year supply agreements (LTAs) [7] | Project-based work only [7] |

| Processes | Documented SOPs and quality systems [14] | Undocumented "tribal knowledge" [14] |

| Supply Chain | Domestic-heavy, with redundant sourcing [14] | Single-source or heavy reliance on overseas suppliers [14] |

Your business's sub-vertical position also plays a major role in valuation. For example, a general machine shop with $2 million in EBITDA might trade at a 4–6x multiple. In contrast, a medical device specialist with the same earnings could command an 8–12x multiple, thanks to certifications and a broader pool of potential buyers [15].

"The single biggest driver of manufacturing multiple variance isn't earnings size, it's sub-vertical positioning." - Christoph Totter, Managing Partner, CT Acquisitions [15]

Understanding your multiple can turn market comparables into actionable insights for business planning. For instance, if competitors with AS9100 or ISO 13485 certifications trade at 7–10x EBITDA while your business is valued at 4–5x, this gap highlights the potential return on investing in certifications 18–36 months ahead of a sale [15].

Customer concentration is another key factor. If your top three customers make up more than 40% of your revenue, buyers will likely see this as a risk, often leading to earnout structures in deals [13]. Proactively reducing this concentration - by securing two or three new mid-size accounts - could increase your EBITDA multiple by 0.5 to 1.5 turns before entering negotiations.

Recurring revenue is also a powerful driver for higher multiples. Transitioning repeat customers from informal agreements to multi-year Long-Term Agreements (LTAs) with pricing escalators can add 0.5–1.5x to your EBITDA multiple [15]. Contracted revenue carries more weight than the same revenue on an informal basis.

By focusing on these targeted improvements, you can better position your business for future growth and maximize its value when it’s time to sell.

Turning these insights into results requires careful financial planning and expert guidance. Phoenix Strategy Group specializes in helping manufacturing companies leverage comparables data for strategic decision-making.

Their team takes care of the heavy lifting, including normalizing financials by adjusting for owner compensation, one-time expenses, and accounting differences. They also build detailed financial models that compare your business to relevant market transactions. This process doesn’t just provide a valuation - it identifies specific operational changes that can boost your multiple well before you go to market.

Market comparables ground your valuation in what buyers are actually paying, rather than relying on hypothetical numbers. For example, manufacturing multiples can range widely - from 3–5x SDE for a general machine shop to 8–12x EBITDA for a medical device contract manufacturer [13]. These variations reflect tangible differences in factors like risk, certifications, customer diversity, and operational performance.

This market-based perspective also emphasizes the importance of valuation adjustments. While EBITDA serves as a starting point, buyers zero in on adjusted EBITDA, which accounts for your reported earnings minus maintenance capex. Depending on your sub-vertical, maintenance capex can range from 3%–10% of revenue [13]. Ignoring this adjustment can lead to valuations that don’t hold up under buyer scrutiny.

Factors like your sub-vertical positioning, certifications (such as AS9100 or ISO 13485), customer concentration, and the reliability of recurring revenue all directly impact your valuation multiple. These aren’t just theoretical ideas - they’re actionable levers that can mean the difference between a 5x deal and a 9x deal.

"A high manufacturing business valuation is not given - it is built." - SeaRidge Advisory Inc [4]

There’s no one-size-fits-all approach when it comes to choosing the right multiple for valuing manufacturing businesses. The best metric depends heavily on your company’s stage of growth and overall profile. For instance, mature companies often lean on the EV/EBITDA multiple, which focuses on profitability. On the other hand, early-stage companies, where profits may be inconsistent, might find EV/Revenue a more fitting measure.

Beyond the company’s maturity, multiples can also vary depending on sub-vertical, business size, and overall quality. Key factors like customer concentration and the presence of recurring revenue streams can significantly influence valuation.

For those navigating these complexities, Phoenix Strategy Group offers advisory services to help you make informed decisions tailored to your unique business situation.

To prepare EBITDA for fair market comparisons, you need to adjust reported earnings to focus on consistent and recurring operations. Start by adding back non-recurring expenses, such as one-time legal fees or personal costs. Next, align owner compensation with market standards and address any differences in accounting practices, like how revenue is recognized or depreciation is handled. If stock-based compensation is part of the equation, factor that in as well. Finally, use trailing twelve-month (TTM) figures to smooth out seasonal fluctuations, ensuring your comparisons are as accurate as possible.

If you're looking to increase your manufacturing business's valuation, targeting a high-value sub-vertical is a smart move. One way to do this is by obtaining industry-specific certifications. For example, certifications like AS9100 for aerospace or ISO 13485 for medical devices can help position your business as a key player in lucrative markets.

Beyond certifications, focus on strengthening your financial profile. Here are a few ways to do that:

Additionally, make sure your working capital is running efficiently. Clean, reconciled financial records are also essential - they reduce perceived risks during due diligence, making your business more appealing to potential buyers or investors. A little preparation here can go a long way in securing a higher valuation.