Published on

June 22, 2026

If card payments depend on keys, PINs, chip checks, and message security, the payment HSM is the device doing that work.

I’d sum it up like this: a payment HSM keeps secret keys inside tamper-resistant hardware, runs PIN and EMV cryptography, supports tokenization, and helps payment systems meet PCI and EMV rules. It also affects day-to-day planning, because throughput, failover, deployment model, and audit controls all shape cost and uptime.

Here’s the article in plain English:

A simple way to think about it: if you process PINs, EMV cryptograms, P2PE data, or payment-message MACs, you usually need payment-grade hardware controls instead of software-only key handling.

The rest of the article explains where those controls fit, how they help stop bad transactions early, and what you need to plan for before volume grows.

Payment HSMs protect four core payment functions: PIN handling, EMV cryptography, tokenization, and key control. They keep secret keys inside a tamper-resistant cryptographic boundary, so applications never touch raw key material. Every sensitive payment action happens inside the device. If the hardware detects tampering, it can zeroize and erase secret material to limit exposure[1][5].

In day-to-day payment systems, these controls show up in different ways across PIN entry, chip checks, tokenization, and key transport. Payment HSMs also support the card-payment algorithms used in production systems and generate MACs to protect transaction integrity[7].

When a cardholder enters a PIN at an ATM or POS terminal, the PIN is immediately formatted into a PIN block under ISO 9564. The most common format is ISO Format 0, which uses the PAN. Some setups use ISO Format 4 with AES protection.

The HSM can translate PIN blocks between keys and verify PINs with PVV or offset methods, all without exposing the clear PIN[1][7]. This is part of PCI PIN Security[4].

EMV chip transactions depend on issuer master keys, or IMKs, stored in the HSM. During authorization, the HSM verifies the Application Request Cryptogram (ARQC) from the chip and generates the Application Reply Cryptogram (ARPC) for issuer verification[4].

That work supports chip-card authentication in issuer and processor setups. Put simply, the HSM helps confirm that the card and transaction data check out before approval moves forward.

Vaultless tokenization derives a token from card data and a secret key. That helps protect the PAN across its lifecycle, cuts down PCI DSS scope, and limits PAN storage[1][5].

This matters because fewer places storing the PAN usually means fewer places that can leak it. It's a simple idea, but in payments, that kind of separation goes a long way.

Payment HSMs generate strong keys and keep them under MFK/LMK control. Applications ask the HSM to perform operations by reference instead of handling the keys themselves. For key transport, ANSI TR-31 key blocks bind transported keys to their intended use[1][6].

The key types that matter most here are:

In DUKPT, the BDK and KSN derive a unique transaction key. That means if one transaction key is exposed, it does not expose the others[6]. The next section shows where these controls sit in issuer, merchant, gateway, and fintech transaction flows.

Payment HSMs show up at several points in the card payment flow. But they don't do the same job everywhere. An issuer uses an HSM one way. A merchant terminal uses it another way. Gateways, processors, and fintech platforms each lean on the HSM for a different part of the security chain.

Issuers use HSMs during card issuance to generate card data, manage PINs, and verify chip cryptograms during authorization. The same setup also supports digital issuance for mobile wallet provisioning with Apple Pay and Google Pay.

During an authorization request, the issuer HSM verifies the ARQC and generates the ARPC. That lets the issuer send back an authenticated response to the card transaction [4][7][5].

Once the card is issued, the HSM's job moves closer to data protection in transit. It helps protect payment data as it travels from the terminal to the processor and then to the issuer.

At the merchant side, HSMs help protect data at entry and at handoff. Terminals encrypt card data as it's entered. Processor HSMs then decrypt that data, handle PIN translation and MAC validation, and re-encrypt the PIN block under the next zone key before it moves forward [4][5].

Gateway HSMs also play a key role here. They tokenize PANs before the data moves deeper into the stack, which can reduce PCI DSS scope for both merchants and processors.

In card-not-present flows, HSMs support CVV2 verification, token processing, and 3-D Secure signing [4][1]. No card reader, no chip dip, no PIN pad - but the HSM is still doing quiet, behind-the-scenes security work.

In multi-tenant fintech setups, where one platform supports many card programs, HSMs use application partitioning so each client's keys stay logically isolated. That's a big deal. It means one platform can serve many customers without mixing their key material.

A single card transaction may touch different HSMs based on the channel. In a typical U.S. chip transaction, the mapping looks like this [4][5]:

| Stage | HSM Location | Task |

|---|---|---|

| Merchant/POS | Merchant environment | Encrypts the PIN block and card data using DUKPT-derived keys |

| Acquirer/Processor | Processor HSM | PIN translation; P2PE decryption; MAC validation |

| Payment network | Network HSM | Re-encrypts PIN blocks and other security data between zones |

| Issuer host | Issuer HSM | ARQC verification; PIN verification; CVV/CVC checking; ARPC generation |

For e-commerce, the PIN step drops out. Even so, issuer HSMs still handle CVV2 checks and token processing. Where these HSMs sit in the flow also affects fraud controls, authorization integrity, and day-to-day uptime.

Payment HSM Deployment Models: On-Premises vs. Hosted Cost & Control Comparison

Once an HSM sits in the transaction path, speed matters. In payments, trust has to be checked right away. Payment HSMs verify transaction cryptography in real time before fraud scoring. They run those checks first, and if a check fails, the transaction can be declined before it ever reaches a fraud model.

Payment HSMs serve as a tightly controlled trust boundary for payment cryptography. As a payment message moves between systems, the HSM generates or verifies a Message Authentication Code (MAC) with Zone Authentication Keys (ZAK) or Terminal Authentication Keys (TAK). If even one byte in an ISO 8583 message changes in transit, the MAC check fails and the transaction can be rejected. HSMs can also digitally sign payment messages or authorizations with keys stored inside the hardened boundary, which helps prove which party signed the message [3][4].

For chip transactions, issuer HSMs verify the ARQC to confirm the card is genuine and generate the ARPC to prove the issuer is genuine [4]. That means captured cryptographic data is useless outside the original transaction. DUKPT adds one more layer. Each transaction uses a new derived key, so captured cryptographic data can't be reused [4].

The fraud upside is simple: faster declines. When an HSM returns a pass/fail validation result, the authorization system gets a trusted answer at once. If the HSM check fails, the system can decline the transaction before fraud scoring even starts. In e-commerce, the HSM verifies CVV2/CVC2 before fraud scoring, which helps stop card-not-present fraud earlier in the flow [4].

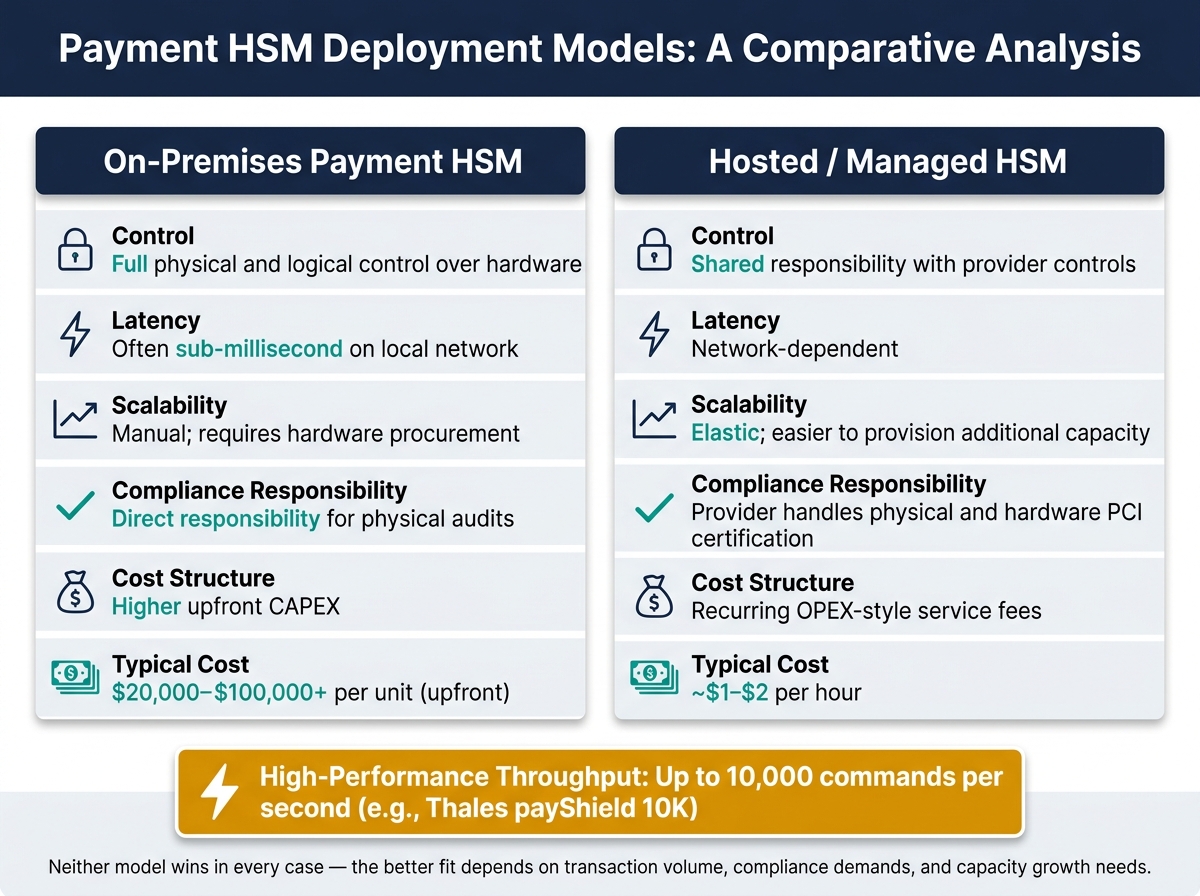

After fraud checks, the next issue is scale. Can the HSM keep up during peak authorization volume? Sizing an HSM deployment is not just about security. It's also about day-to-day operations. High-performance units like the Thales payShield 10K can handle up to 10,000 commands per second (CPS) [2][7]. Even so, peak transaction periods can still create bottlenecks, and an undersized HSM cluster can hurt transaction success rates.

Production setups should run HSMs in at least high-availability (HA) pairs. If one unit fails during a fault or maintenance event, the second can keep processing without interruption [4][7].

On-premises and hosted HSMs each come with tradeoffs around control, latency, scaling, and cost:

| Operating model | Control | Latency | Scalability | Compliance responsibility | Cost structure |

|---|---|---|---|---|---|

| On-premises payment HSM | Full physical and logical control over the hardware | Often sub-millisecond on a local network | Manual; scaling requires hardware procurement | Direct responsibility for physical audits | Higher upfront CAPEX plus ongoing staffing, facilities, and support |

| Hosted or managed HSM | Shared responsibility with provider controls | Network-dependent | Elastic; easier to provision additional capacity | Provider handles physical and hardware PCI certification | Recurring OPEX-style service fees |

On-premises hardware usually costs $20,000 to $100,000+ per unit in upfront CAPEX [4]. Cloud-based HSM services generally run about $1 to $2 per hour on an OPEX model [4]. Neither option wins in every case. The better fit depends on transaction volume, compliance demands, and how much capacity you may need to add over time.

For growth-stage companies, HSM infrastructure can become a real budget item. Security spend often fades into the background when things work well, then gets a lot of attention when they don't. It helps to model HSM spend against payment volume growth, peak load, and PCI audit cycles.

As card programs grow, control needs often shift from basic encryption to dedicated hardware. Most companies don't begin with a payment HSM. They start with software-based controls and move to dedicated hardware when the risk profile or compliance rules change. Common triggers include PIN processing, EMV cryptogram generation and verification, and point-to-point encryption (P2PE) [4][1].

For issuers, generating EMV keys, verifying ARQC, generating ARPC, and handling PINs require HSM-grade key protection under EMVCo and PCI PIN rules [4]. For processors and acquirers, MAC verification and PIN translation are core tasks. Merchants and fintechs often begin with tokenization, then expand into key management, PIN, and EMV workloads.

A stricter PCI review is often what forces the move. When key management controls fall short of PCI DSS or PCI PIN rules, the fix usually leads to dedicated HSM hardware. A common path is to start with tokenization, add key management, and then move into PIN and EMV workloads [1].

In card payments, security controls matter only when people run them the right way. Once the HSM sits in the payment flow, governance decides whether those controls hold up in an audit and keep working as volume grows.

Compliance in payment HSM setups is about day-to-day operation. PCI PIN rules keep cleartext PINs inside the HSM. PCI DSS key-management controls also require HSM-backed protection for cardholder data and keys across the full key lifecycle. PCI PTS HSM v5.0 pushes device-security key rules further. In PCI PTS HSM v5.0, released in May 2026, device-security keys must use at least 128-bit effective strength, and Triple DES (TDES) is no longer allowed for device security purposes [8]. That change sets a higher bar for device-security key strength and lines up with newer cloud and multi-tenant deployment needs.

Auditors don’t stop at the written policy. They look at the operating controls too. Dual control means at least two authorized security officers must be present for sensitive tasks like loading a Master Key, and split knowledge means no single person ever holds a complete cleartext key [4]. Those rules shape how key ceremonies are planned, run, and documented.

Each key ceremony needs a clear audit trail from creation through retirement. Send HSM logs to a SIEM so unusual cryptographic activity can be flagged in real time [1][4]. Application logs should also be scrubbed of sensitive HSM responses and PIN block data before they leave the secure environment [4]. If that step gets skipped, trouble can spread fast.

Key separation matters just as much. Separate keys by business unit, partner, and environment. A single BDK should never be reused across different business units or partners [9]. A tiered key hierarchy helps keep a compromise boxed into one business unit, partner, or environment instead of the full network [4]. Enable tamper response and zeroization [4]. Weak key control can expose transactions and make the impact of a breach much worse.

With the control model in place, the next job is turning it into daily discipline. Payment HSMs protect card transactions by keeping keys, PINs, and cryptographic checks inside a tamper-resistant boundary. Match the deployment model to transaction volume and compliance needs, use HA pairs, enforce dual control and split knowledge, and keep key ceremonies auditable.

You need a payment HSM when your system handles sensitive cryptographic tasks that need a tamper-resistant root of trust. That includes PIN processing, EMV key management, and point-to-point encryption.

It’s also required to meet standards like PCI DSS, PCI PIN, and PCI P2PE when you process card payments, mobile wallets, or transaction signing.

Payment HSMs help cut fraud by keeping sensitive cryptographic work inside a tamper-resistant hardware boundary. That means encryption keys and PINs never appear in clear text.

They also take care of key management, digital signing, and EMV chip validation inside that same protected environment. In plain English, they help block unauthorized access, enforce strict access controls, and protect transaction integrity, while also supporting compliance with PCI DSS and FIPS.

It depends on your requirements and where your business is right now.

On-premises HSMs give you full control. They can also deliver lower latency for high-volume transactions and give your team more room for custom integrations.

Hosted HSMs make more sense if you want to cut upfront hardware costs, reduce day-to-day complexity, and get to market faster. The provider also takes care of maintenance and PCI certification. The tradeoff is simple: you depend more on the provider’s infrastructure.