Published on

April 29, 2025

Withholding tax directly impacts cross-border M&A deals by influencing cash flow, deal valuation, and transaction timelines. It applies to payments like dividends, interest, and royalties, with rates varying by country and often reduced through tax treaties. For growth-stage companies, challenges include limited resources, tight deadlines, and navigating complex tax rules.

To manage withholding tax effectively:

For example, U.S. withholding tax rates range from 0% to 30%, but treaties like the U.S.-UK agreement can reduce these significantly. Proper planning and expert guidance ensure compliance and protect deal value.

Key takeaway: Early tax planning, treaty analysis, and expert advice are critical for minimizing withholding tax risks and maximizing M&A success.

Understanding withholding tax in cross-border M&A involves grasping a few key principles.

Withholding tax comes into play for certain cross-border payments in M&A transactions. Common examples include:

The rates for withholding tax depend on the type of payment and the countries involved. In the U.S., these rates range from 0% to 30%, with the default being 30% unless a treaty reduces it. The roles of the source and residence countries are crucial in determining these obligations.

The interaction between source and residence countries shapes withholding tax responsibilities:

For example, if a U.S. company acquires a foreign target, payments like interest or dividends sent back to the U.S. could face withholding taxes from the source country. This dynamic underscores the importance of tax treaties, which help clarify these obligations.

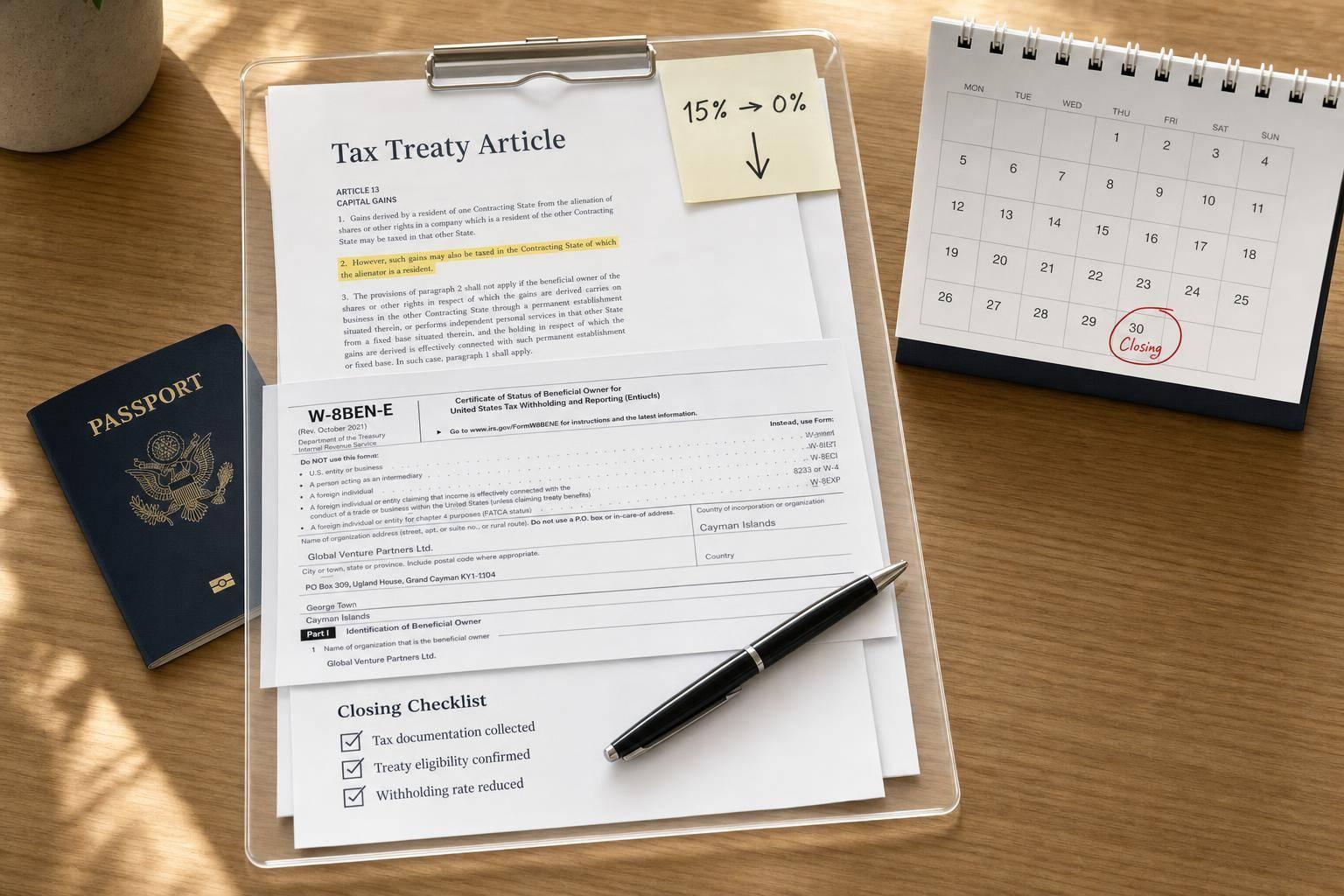

Double Taxation Avoidance Agreements (DTAAs) play a critical role in managing withholding tax exposure. These agreements between countries can reduce withholding tax rates and provide clear guidelines for tax treatment, helping businesses avoid being taxed twice on the same income.

Here’s how DTAAs can impact M&A transactions:

| Benefit | Impact on M&A Transactions |

|---|---|

| Lower Rates | Reduces statutory withholding rates, saving costs |

| Certainty | Provides clear rules for structuring deals |

| Relief Mechanisms | Prevents double taxation with credits or exemptions |

| Dispute Resolution | Offers processes to resolve tax-related disagreements |

For instance, while the U.S. standard withholding tax rate is 30%, specific treaties, like the U.S.-UK tax treaty, may significantly reduce these rates. Under certain conditions, interest payments could drop to 0%, dividends may range from 5% to 15%, and royalties could also be reduced to 0%.

To take full advantage of these treaty benefits, companies should evaluate applicable agreements early in the deal-planning phase. This helps identify tax-saving opportunities and ensures compliance with all requirements.

Cross-border M&A deals often involve payments that are subject to withholding tax. While dividend and interest payments are common triggers, other payments - like contingent earnouts and royalties for intellectual property (IP) - also come into play.

For example, in 2023, a Japanese company acquired a California-based SaaS firm and faced a 30% withholding tax on $12 million in IP royalty payments.

Here are some key payment types that may trigger withholding:

| Payment Type | Standard Rate | Common Scenarios |

|---|---|---|

| Earnout Payments | 10% on principal | Deferred payments and contingent earnouts |

| Royalty Payments for IP | 30% | Licenses, patents, and technology transfers |

*Installment sale rules often apply to earnout structures.

These payment categories highlight the importance of understanding U.S. withholding tax rules.

U.S. tax laws impose specific rules depending on how a transaction is structured. For instance, in 2024, a German company purchased manufacturing assets in Texas. This asset purchase triggered a 21% withholding tax on $8 million of recaptured depreciation. Had the deal been structured as a stock sale, the tax rate could have dropped to 5% under the U.S.-Germany tax treaty.

FIRPTA (Foreign Investment in Real Property Tax Act) adds another layer of complexity. According to IRS data, FIRPTA withholdings totaled $4.7 billion in 2023, an 18% rise from 2022. These rules apply when at least 25% of a target company’s value is tied to U.S. real property interests.

Beyond statutory rates, how assets are classified can further influence withholding obligations.

The way assets are classified and allocated in a deal can significantly impact withholding taxes. A 2025 biotech acquisition highlights this: $15 million initially categorized as IP payments was reclassified as consulting agreements, reducing withholding liability by $1.2 million through treaty exceptions. For growth-stage companies, such strategies can be pivotal during exit planning.

Here’s how different asset types are treated:

| Asset Category | Treatment | Opportunities |

|---|---|---|

| Tangible Assets | Based on location | Depreciation strategies |

| Intellectual Property | 30% on royalties | Possible treaty rate reductions |

| Goodwill | Generally exempt | Flexible allocation |

| Inventory | Usually exempt | Adjustments for working capital |

"The IRS collected $290 million in M&A-related penalties in FY2024, with 63% stemming from improper FIRPTA compliance", according to recent IRS Enforcement Statistics.

For earnout structures, installment sale rules often require 10% withholding on principal payments and 30% on imputed interest. A 2024 Delaware Court ruling (Case 1:24-cv-00345) upheld tax-free treatment for $7 million in escrow holdbacks tied to representations and warranties, offering opportunities for strategic structuring.

Growth-stage companies should work with advisors like Phoenix Strategy Group to navigate M&A complexities and ensure compliance with U.S. tax regulations.

When dealing with cross-border M&A transactions, both buyers and sellers need to meet specific IRS requirements to handle withholding taxes properly. Buyers are responsible for filing the necessary IRS tax forms within the required deadlines. On the other hand, sellers must provide proof of tax residency and claim any treaty benefits they qualify for. It's crucial to work with tax professionals to ensure residency documents are accurate and IRS filings are completed on time.

Using treaty benefits can help companies reduce tax liabilities. To make the most of these benefits:

These steps can help businesses minimize taxes while setting up the deal in the most efficient way.

The structure of a transaction - whether it's a stock purchase, asset sale, or merger - can have different tax outcomes. To navigate this:

The M&A advisory team at Phoenix Strategy Group emphasizes the importance of early treaty and regulatory analysis during the planning stage. Their financial modeling services are designed to help growth-stage companies structure deals that meet tax obligations while aligning with U.S. regulations.

Cross-border M&A transactions often run into major withholding tax challenges. Misunderstanding treaty provisions or failing to properly document tax residency can lead to the default 30% U.S. withholding rate being applied instead of lower treaty rates.

Delays in submitting required forms can result in penalties and reduce the overall value of a deal. Tax authorities enforce strict deadlines, and missing them can have serious consequences for transaction outcomes.

Double taxation is another issue and can happen when:

The next section offers practical advice to help growth companies tackle these issues effectively.

To handle withholding tax complexities, growth-stage companies must take early action. Conducting thorough due diligence early on can help manage tax obligations and improve exit outcomes.

Here are some ways companies can reduce withholding tax challenges:

Documentation Management

Strategic Planning

Partnering with skilled financial advisors can make a big difference in navigating these challenges. For example, Phoenix Strategy Group’s M&A advisory team helps growth companies establish thorough due diligence processes and create efficient post-deal integration plans to maximize exit value.

Preparing early and keeping accurate records are essential for managing withholding tax. Companies should focus on building reliable accounting systems and ensuring financial data is well-organized and easy to access for compliance purposes.

Navigating withholding tax in cross-border M&A requires a clear strategy. Early tax planning and thorough due diligence are key for growth-stage companies aiming to minimize liabilities and maximize exit value.

Keeping accurate records and structuring deals carefully can help reduce tax risks. Using relevant tax treaties alongside strategic deal planning can also lower withholding tax obligations. Having expert support ensures compliance and improves tax outcomes during transactions.

For growth companies, building a solid financial foundation, maintaining detailed documentation, and consulting with experts are critical steps. This approach helps avoid double taxation, missed deadlines, and ensures transactions deliver the best possible value.

Tax treaties between countries can play a significant role in reducing withholding taxes during cross-border mergers and acquisitions. These treaties often include provisions that lower or eliminate withholding tax rates on dividends, interest, and royalties paid between entities in the two countries.

To benefit from a tax treaty, businesses typically need to meet specific requirements, such as demonstrating tax residency in one of the treaty countries and providing proper documentation to the relevant tax authorities. Consulting with financial and strategic advisors, like Phoenix Strategy Group, can help businesses navigate these requirements and maximize potential tax savings.

When structuring a cross-border M&A deal, minimizing withholding tax is a critical consideration to optimize the transaction's financial outcome. Key factors to evaluate include:

Consulting with a qualified tax advisor or M&A specialist is essential to navigate the complexities of international tax laws. Firms like Phoenix Strategy Group can provide expert guidance on structuring deals effectively while aligning with your financial and strategic goals.

Growth-stage companies often encounter withholding tax compliance challenges in cross-border M&A deals due to differences in tax regulations between countries, limited internal expertise, and complex documentation requirements. These issues can lead to unexpected tax liabilities, delays, or even penalties.

To address these challenges, businesses should prioritize thorough due diligence to understand applicable tax treaties, local laws, and withholding rates. Engaging experienced advisors, such as Phoenix Strategy Group, can also help ensure compliance by leveraging their expertise in M&A support and financial strategy. Proactive planning and accurate record-keeping are key to mitigating risks and ensuring a smooth transaction.