Published on

February 12, 2026

Access to credit is a game-changer for SMBs, but many face rejection due to outdated evaluation models. AI is transforming credit risk assessment by analyzing real-time data like cash flow and utility payments, offering faster decisions, improved accuracy, and expanded access to funding. Here's what you need to know:

AI isn't just speeding up the process - it’s reshaping how SMBs secure the resources they need to grow. However, ensuring fairness, transparency, and regulatory compliance is key to successful implementation.

Traditional vs AI-Driven Credit Assessment for SMBs: Speed, Accuracy and Access Comparison

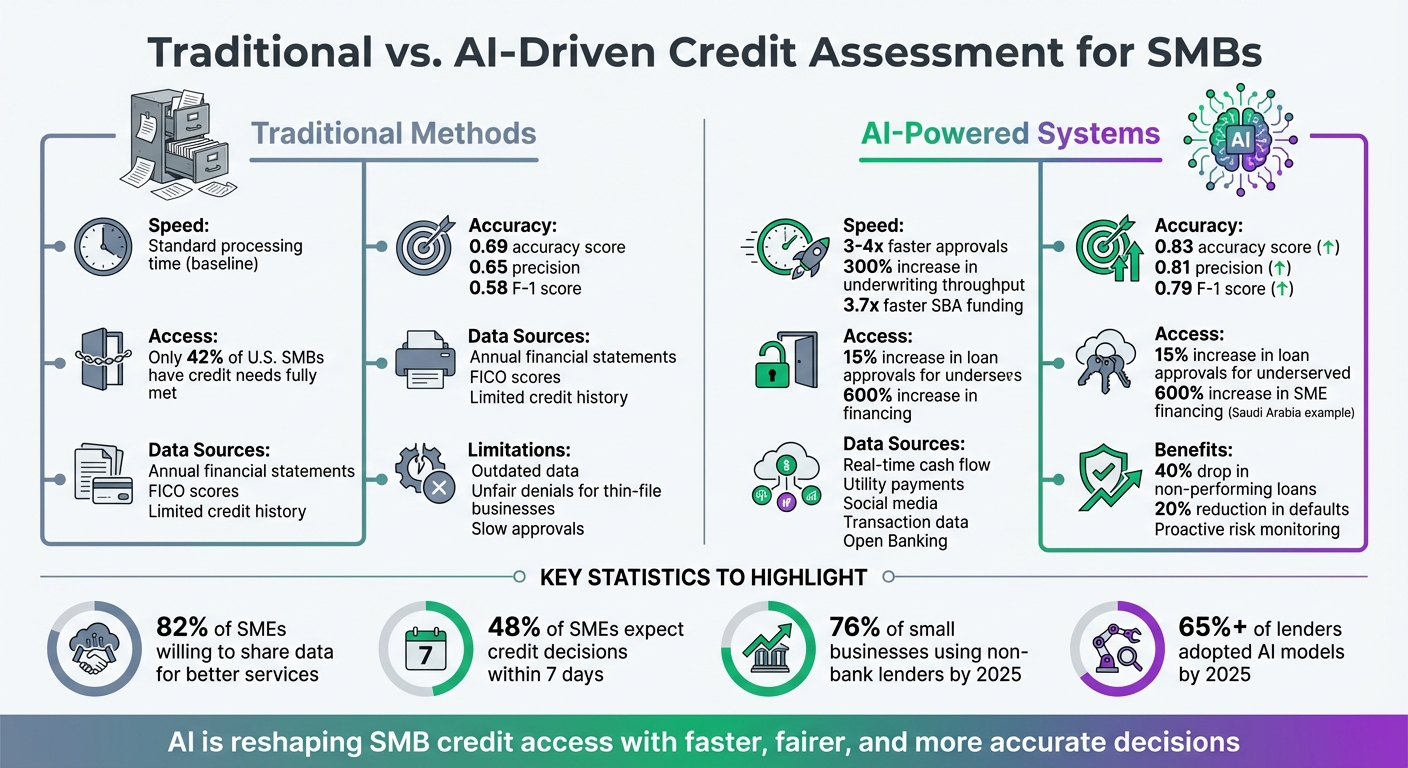

The move from traditional credit models to AI-powered systems brings noticeable improvements in three key areas: accuracy, speed, and access.

AI excels at spotting patterns that traditional scoring methods often miss. Instead of relying solely on outdated financial records, AI evaluates real-time data like cash flow, utility payments, social media activity, and supply-chain interactions to create an always-updated financial picture [1][7].

For instance, in October 2024, Nigar Karimova, a researcher from Columbia University, compared an AI-based Random Forest model with a traditional Delphi model using data from Azerbaijani SMEs. The AI model showed a leap in accuracy from 0.69 to 0.83, improved precision from 0.65 to 0.81, and boosted the F-1 score (a measure of reliability) from 0.58 to 0.79 [3]. Similarly, between 2016 and 2019, fintech lenders like Funding Circle and LendingClub used machine learning models to predict delinquencies more effectively than traditional FICO or VantageScores, particularly in areas with high unemployment where conventional models often fall short [7].

AI also reduces human error by automating tasks like extracting data from tax returns, bank statements, and credit reports [6].

"AI should handle the work that doesn't require human intelligence, so your underwriters can focus on decisions that do." - Kristiane Mandraki, VP of Growth + Market Intelligence at Praxent [6].

By enhancing accuracy, AI naturally streamlines the loan approval process.

AI tools drastically speed up loan approvals, delivering results 3–4 times faster than traditional methods. Some systems achieve SBA funding speeds that are 3.7 times faster than the industry average [6]. Lenders using custom AI tools have reported a 300% jump in underwriting throughput [6].

This speed comes from AI’s ability to instantly classify, validate, and sort documents while flagging errors for review [6]. Applications that meet basic criteria can be processed automatically without human intervention. Instead of waiting for underwriters to manually input data or resolve discrepancies, AI extracts key fields and handles inconsistencies on its own [6]. Human review is only required for flagged exceptions, which are presented with clear evidence and references.

The combination of faster processing and improved risk evaluation creates opportunities for broader credit access.

AI doesn’t just make processes faster - it also opens the door for businesses that traditional models often overlook. By leveraging alternative data sources like utility payments, invoice factoring, and trade credit, AI develops thorough risk profiles for "thin-file" businesses that lack extensive credit histories [1].

Additionally, AI provides proactive risk management by monitoring transactional data in real time. This allows lenders to detect potential issues early, rather than waiting for annual financial reviews [2][8]. This real-time oversight is a core benefit of fractional CFO services, which help businesses maintain lender-ready financials year-round. With this continuous monitoring, lenders can reduce default risks while extending credit to more businesses, including those previously deemed too risky.

Using AI for credit assessment isn't without its hurdles. These challenges, though daunting, are opportunities to refine and innovate solutions. Here's a closer look at the main obstacles.

Small businesses often lack the financial transparency of larger corporations, making it tougher for lenders to evaluate their creditworthiness with traditional data alone [4]. Many small and medium-sized businesses (SMBs) have limited credit histories, which results in insufficient data for accurate risk modeling [8]. On top of that, traditional models relying on annual financial statements often work with outdated information by the time decisions are made [8].

One way forward is through alternative data. Lenders are turning to sources like invoice payment behavior and real-time transaction data accessed via Open Banking [4][8]. Instead of building these capabilities in-house, many lenders are finding it more efficient to partner with vendors who specialize in sourcing and enriching transaction data.

"Traditional decisioning frameworks have typically relied on outdated financial data which has limited the ability to accurately assess customer risk, particularly the 'thin-file' population."

– Jared Chebib, Partner, Financial Services Consulting, EY [8]

AI models often operate as "black boxes", generating decisions that lack clear explanations. This becomes a significant issue when borrowers want to know why their credit applications were denied. To address this, companies like QuickBooks Capital adopted tools like SHAP (Shapley Additive Explanations) in their machine learning models. For instance, in July 2019, QuickBooks implemented an XGBoost model with SHAP to make credit decisions more transparent. The result? A projected 20% drop in loan defaults and a 42% reduction in "bad outcomes" for high-risk applications [9].

Another approach is the use of monotonic constraints in AI models. These constraints ensure intuitive relationships, such as higher income leading to lower risk scores. Research has shown that XGBoost models with monotonic constraints outperform traditional scorecard models by 7% in predictive accuracy [9]. Additionally, linking AI model features to standardized Adverse Action reason codes provides clear and compliant explanations for credit denials [9].

Transparency isn't just a technical issue - it's a regulatory one too. Compliance with laws like the Equal Credit Opportunity Act (ECOA) and the Fair Credit Reporting Act (FCRA) requires lenders to provide clear and accurate reasons for credit denials within a set timeframe (30 to 90 days) [11]. The Consumer Financial Protection Bureau (CFPB) has emphasized that lenders can't sidestep these obligations by claiming their AI systems are too complex to explain.

"A creditor cannot justify noncompliance with the ECOA and Regulation B's [adverse action] requirements based on the mere fact that the technology it employs is too complicated or opaque to understand."

– Consumer Financial Protection Bureau [11]

Ethical concerns, such as bias in AI models, add another layer of complexity. AI systems can unintentionally use data proxies that result in discriminatory outcomes against protected groups [12][13]. To combat this, lenders should regularly test for bias, document their models' logic and assumptions, and establish human oversight to review and adjust AI-generated results as needed [13]. Independent validations conducted annually can also ensure models remain aligned with both the institution's risk profile and current regulations [10].

| Regulatory Framework | Key Requirement for AI | Primary Oversight Body |

|---|---|---|

| ECOA (Reg B) | Specific statement of reasons for credit denial | CFPB |

| FCRA (Reg V) | Disclosure of information sources (credit reports/third parties) | CFPB / FTC |

| BSA/AML | Model validation and risk mitigation for monitoring systems | FinCEN / Federal Banking Agencies |

| ISO/IEC 42001 | Governance and management systems for AI | International Organization for Standardization |

Tackling credit risk challenges with AI requires a clear and structured approach. It starts with building a strong data infrastructure, followed by selecting the right AI tools, and ensuring continuous monitoring to keep everything running smoothly and accurately.

A solid data foundation is the backbone of any AI-driven system. Did you know that 82% of small and medium-sized enterprises (SMEs) are willing to share their data with banks in exchange for better financial services? [2] That’s a lot of valuable, real-time data waiting to be utilized. The key is moving away from outdated annual financial statements and focusing on real-time transactional data that reflects the current state of a business [2].

Start by identifying manual bottlenecks, like misclassified documents or manual data entry, and look for ways to automate these processes [6][15]. For example, automated AI tools can validate documents instantly, rejecting incorrect submissions and guiding borrowers on what’s missing [6].

For many SMBs, it’s more cost-effective to partner with vendors who specialize in sourcing and enriching transaction data rather than building these capabilities from scratch [2]. Open Banking APIs are a practical way to access real-time customer data, even if the customer’s primary banking relationship is with another institution [2]. Make sure your infrastructure includes field-level lineage, which tracks every decision back to its source document. This creates an automated audit trail that meets regulatory standards [6].

These improvements highlight the importance of having a robust data system in place [3]. Once your data foundation is set, it’s time to move on to selecting the right AI solutions.

Partnering with the right experts is key. With 48% of SMEs expecting faster "credit as a service" and 55% needing access to funds within seven days, speed and precision are non-negotiable [2]. This is where specialized partners with expertise in SMB lending workflows, SBA requirements, and compliance come into play [6].

The best AI solutions are modular and flexible, allowing you to update credit policies or integrate new data sources quickly [2]. Look for systems that support dynamic segmentation by industry or risk score and allow policy updates in hours instead of months [6]. Tailored AI tools can significantly speed up approvals, making them an essential part of your implementation strategy [6].

Before rolling out these solutions, ensure they align with your business model. Translate your vision into a streamlined credit policy that reflects your risk appetite [2]. This process requires collaboration across departments - business, risk, and technology teams need to work together to balance trade-offs effectively [2]. A phased approach is often the safest route. Start with a pilot program targeting high-risk or high-value borrowers to identify gaps before scaling up to your full portfolio [17].

Once your AI system is up and running, consistent monitoring is essential to adapt to market changes and maintain performance. AI-driven monitoring uses real-time data to identify risks, such as sudden drops in sales, within days instead of waiting for quarterly reports [17]. During the early stages, establish governance controls like incremental rollouts and automated "circuit breakers" to manage risks [14].

Regularly recalibrate your models using recent customer and performance data to ensure they stay relevant in changing market conditions [2]. This not only maintains the quality of decisions but also helps avoid new risks. For instance, a bi-annual model validation process has been shown to reduce default rates by 15% [16]. Additionally, configure your system to analyze both individual borrower data and broader industry trends, like tariff hikes or supply chain issues, to avoid misinterpreting systemic problems as borrower-specific failures [17].

| Implementation Phase | Key Action Items | Expected Impact |

|---|---|---|

| Data Infrastructure | Integrate Open Banking; automate OCR for tax/bank docs | Eliminate manual data mapping; reduce errors [6][2] |

| Solution Selection | Choose specialized SMB lending AI; ensure policy flexibility | 3-4x faster funding; policy updates in hours instead of months [6] |

| Monitoring/Optimization | Implement model risk management; establish version control; recalibrate models | Audit readiness; consistent decision-making; lower risk [6][14] |

Transparency is critical. Your AI system should include tools that justify credit decisions to both regulators and customers [3][2]. An automated audit trail that logs every lending decision and update will help you stay compliant with state and federal regulations [17]. For SMBs navigating complex growth-stage challenges, working with advisory firms like Phoenix Strategy Group (https://phoenixstrategy.group) can simplify the process. These firms specialize in data engineering and financial infrastructure, ensuring your system aligns with both operational goals and regulatory standards.

AI is reshaping how credit decisions are made for small and medium-sized businesses (SMBs), making the process quicker and more accessible. Three key trends are driving this transformation.

AI is moving beyond traditional credit scores, tapping into unconventional data sources like emails, social media, and supplier networks to create actionable insights. For example, in 2025, Bank of America used AI models that incorporated utility payments and social media activity, leading to a 15% increase in loan approvals for underserved groups and a 40% drop in non-performing loans [16].

Real-time cash flow analytics are now evaluating factors like income fluctuations and spending patterns, outperforming static credit scores like FICO [20]. By 2025, over 65% of lenders had adopted AI models that utilized nontraditional data, improving risk prediction accuracy by an estimated 20% [16].

Saudi Arabia's Vision 2030 program highlights the potential of these innovations. Between 2018 and 2025, AI-powered tools drove a 600% increase in SME financing, cutting loan decision times from 49 days to almost instant [19]. AI agents now handle tasks like document verification and portfolio monitoring, allowing financial teams to focus on strategic decisions [18][19].

These developments are paving the way for AI to play an even larger role in expanding credit access and promoting fairness.

AI is also helping to bridge the gap for SMBs that have traditionally been underserved by financial institutions. Currently, only 42% of U.S. SMBs have their credit needs fully met [1]. Machine learning models can identify patterns in data that human analysts might overlook, enabling better risk predictions even for businesses with limited credit histories [1][4].

From 2016 to 2019, fintech lenders like Funding Circle and LendingClub used AI-driven credit scoring to increase loans in areas with high unemployment and bankruptcy rates. Their models were better at predicting delinquencies over 12- and 24-month periods compared to traditional credit scores [7]. U.S. banks that adopted AI during this time expanded lending to underserved areas, offering lower interest rates and experiencing fewer defaults than banks relying on traditional methods [5].

"The traditional approach often fails to capture the full picture of an SME's creditworthiness, leading to unfair assessments and missed opportunities." - Kiara Taylor, Journalist [1]

AI also supports lending in remote areas by enabling banks to extend credit where they lack physical branches [5]. By early 2025, 76% of small businesses turned to non-bank lenders for faster, AI-enabled credit approvals [20]. These tools are closing the credit gap for millions of SMBs.

As concerns about opaque AI decisions grow, explainable AI (XAI) is stepping in to provide clarity and ensure compliance. XAI tools like SHAP and LIME help make complex machine learning models more transparent, offering clear explanations for credit decisions [21][13].

In 2025, JPMorgan Chase implemented XAI models that improved credit decision accuracy by 25% while maintaining full regulatory compliance [16]. For SMBs, this means understanding why a particular credit rating was assigned and identifying areas for improvement [4]. For lenders, XAI ensures decisions are fair and free from unintended biases [21][1].

Regulations are pushing for more oversight, with an emphasis on human-in-the-loop systems and ethical AI reviews [13][1]. For instance, Barclays introduced an AI system in 2025 that monitored credit portfolios in real time, identifying risks 30% faster than manual methods [16]. As transparency becomes a priority for both regulators and SMBs, XAI will be essential for building trust and staying compliant.

AI is reshaping how small and medium-sized businesses (SMBs) access credit and manage risk. Traditional credit models, which often rely on outdated financial statements and limited credit histories, have left only 42% of U.S. SMBs with their financing needs fully met [1]. By analyzing real-time cash flow, transaction data, and even social media activity, AI creates a more complete picture of a business's creditworthiness.

The benefits are striking. AI can speed up loan approvals - boosting underwriting throughput by as much as 300% - while reducing costs, improving risk predictions, and expanding access to capital [6][8]. These efficiency gains also help address earlier challenges around data quality and transparency.

"AI should handle the work that doesn't require human intelligence, so your underwriters can focus on decisions that do."

– Kristiane Mandraki, VP of Growth + Market Intelligence, Praxent [6]

Despite its potential, successfully integrating AI into credit assessment comes with challenges. High-quality data, clear decision-making frameworks, and consistent human oversight are critical to ensuring fair and accurate outcomes. Human review remains essential to test and correct AI conclusions, minimizing the risk of bias or discriminatory practices [1]. On the other hand, SMBs can strengthen their digital presence and use Open Banking tools to share real-time data with lenders. Meanwhile, lenders should focus on adopting explainable AI frameworks to build trust and align with fair lending practices [8].

AI-driven credit assessment isn't just about faster loan approvals. It’s about creating a more inclusive and efficient financial system that helps businesses grow and thrive in today's digital economy.

For SMBs looking to tackle these challenges and harness AI effectively, Phoenix Strategy Group (https://phoenixstrategy.group) provides advisory services to help build strong data infrastructures, tailor AI solutions, and navigate complex regulations with confidence.

To improve AI-powered loan decisions, it's important to provide detailed financial information that showcases your company's overall financial health and cash flow. This might include bank statements, tax documents, and records of payments to and from customers or suppliers.

You can also include less conventional data, such as transaction patterns or trade credit history, to give lenders a broader understanding of your business. Submitting timely and standardized data ensures that AI systems can deliver precise and fair credit evaluations, which is especially helpful for businesses with short or limited credit histories.

To determine whether an AI credit decision is fair and explainable, start by assessing the transparency of the model's decision-making process. Tools like SHAP (SHapley Additive Explanations) can help provide clear insights into how the model arrives at its decisions. Additionally, it's crucial to conduct fairness diagnostics. This involves checking whether approval rates are consistent across different protected groups to ensure compliance with fair lending regulations and avoid discriminatory outcomes.

To stay compliant while using AI in SMB lending, lenders should focus on a few key actions:

By prioritizing these practices, lenders can uphold both legal and ethical standards in their operations.