Published on

December 9, 2025

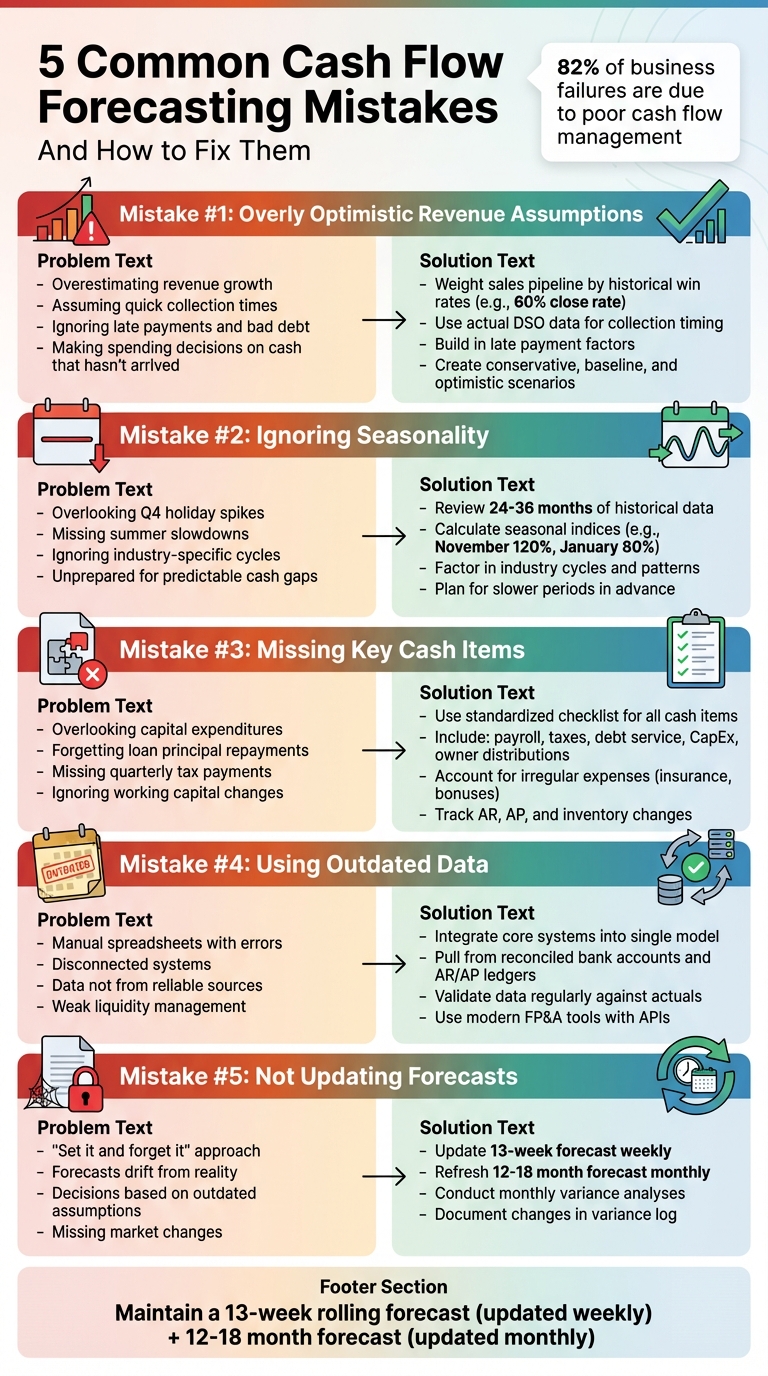

Cash flow forecasting is about predicting when cash enters and exits your business. It’s not just about profits - it’s about ensuring you have enough cash to pay bills, make payroll, and grow. Poor cash flow management is a leading cause of business failures (82% of cases), especially for companies in growth stages where upfront costs often outpace revenue collection.

Key Takeaways:

5 Common Cash Flow Forecasting Mistakes and How to Fix Them

Cash flow forecasting is a crucial task, but it’s surprisingly easy to get wrong. Mistakes like overly optimistic revenue predictions, ignoring seasonal trends, overlooking key cash items, relying on outdated data, and failing to update forecasts can turn a well-intentioned plan into a financial headache. These errors don’t just stand alone - they often amplify each other. For instance, pairing unrealistic sales expectations with missed tax payments and outdated figures can create a forecast that’s wildly out of sync with reality. Recognizing these pitfalls is the first step toward building a more reliable cash flow forecasting process.

It’s common for growth-stage businesses to overestimate revenue and assume quicker collection times. They often expect rapid sales growth, shorter sales cycles, flawless customer onboarding, and perfect payment collections. But this optimism can lead to underestimating churn, applying unrealistic conversion rates, and ignoring historical data like late payments or bad debt.

The result? Spending decisions - such as hiring, inventory purchases, or marketing investments - are made based on cash that hasn’t arrived yet. This can lead to payroll issues, delayed vendor payments, and even scrambling for emergency funding. Brex highlights how startups often face cash crises when their forecasts don’t align with actual collections, making it tough to cover payroll or fund essential operations. As Phoenix Strategy Group puts it, "The failures always happen because - finance and revenue teams working in silos."[1]

Seasonal trends and business cycles are predictable, yet they’re often overlooked in cash flow forecasts. Whether it’s Q4 holiday spikes, summer slowdowns, or industry-specific cycles, ignoring these patterns can leave businesses unprepared. For example, retail and e-commerce businesses heavily tied to holiday shopping or B2B companies affected by fiscal-year budgeting often experience significant cash flow fluctuations.

Without accounting for these trends, companies may find themselves short on cash during slower periods, forcing them into short-term borrowing or sudden cost-cutting measures. A Techstars article highlights how poor revenue forecasting can lead to cash shortfalls, making it "nearly impossible" to manage expenses strategically or plan for growth.[4]

Some businesses focus so much on revenue, payroll, and rent that they overlook other critical cash outflows. These include capital expenditures like equipment or technology, loan principal repayments, quarterly tax payments, owner distributions, and working capital changes such as shifts in accounts receivable, accounts payable, and inventory.

These overlooked items can significantly impact cash flow. A company might report an accounting profit but still run out of cash because these hidden outflows weren’t factored into the forecast.[5]

Even the best forecasting models fall apart when they rely on bad data. Manual spreadsheets and disconnected systems often introduce errors, especially when data isn’t pulled from reliable sources like reconciled bank accounts or AR/AP ledgers. As EY points out, weak cash flow forecasting not only hampers liquidity management but also drives up financing costs and complicates long-term planning.[9]

Michael Mancuso, CIO of New Law Business Model, echoes this sentiment, saying: "Hire PSG if you want to make your life easier and have accurate data."[1] Keeping data current and accurate is essential for reliable forecasts.

Forecasts aren’t “set it and forget it” tools. Market conditions, sales, costs, and hiring plans can change quickly, especially for growing businesses. If forecasts aren’t updated regularly, they drift further from reality, leading management to make decisions based on outdated assumptions.

Phoenix Strategy Group recommends weekly reviews and refinements to forecasts, allowing companies to adjust for changing conditions and correct any initial errors.[1] For most U.S. growth-stage businesses, a monthly update of a 12–18 month forecast, paired with a rolling 13-week cash forecast refreshed weekly or biweekly, strikes a practical balance.[7][8] This cadence helps ensure decisions are based on the most accurate and up-to-date information available.

Understanding common pitfalls is just the beginning. The next step is creating a forecasting process that delivers real results. To do this, focus on these key steps: define clear objectives, organize accurate data, set realistic assumptions, connect your financial statements, and use the right tools and expertise. A dependable forecast system does more than crunch numbers - it aligns your projections with reality, helping you make smarter decisions.

Start by identifying the goals of your forecast. Are you ensuring payroll is covered next month, planning a Q2 hiring spree, or preparing for investor meetings? Each objective demands a different time frame and level of detail. For short-term liquidity needs, such as payroll or vendor payments, a 13-week rolling cash flow forecast updated weekly is ideal [8]. For strategic planning - like hiring, capital investments, or preparing board reports - use monthly forecasts that span 12–24 months [2]. If you're gearing up for a funding round or M&A discussions, you'll need multi-year, monthly projections to guide valuation and scenario planning [5].

Set measurable targets tied to your goals. For instance: "Maintain a minimum cash balance of $500,000", "Ensure a debt service coverage ratio of at least 1.25x", or "Extend runway through Q4 2026." These specific benchmarks will help you choose the right forecast time horizon and update frequency.

Accurate forecasts depend on clean, well-organized historical data. Key data sources include:

Organize this data consistently by category - such as SaaS revenue, payroll, marketing, and rent - and by time period (weekly or monthly). A helpful approach is creating a central data table where each row represents a transaction or summary line, with fields like Date, Category, Amount (USD), Cash In/Out flag, and Source System. Linking this table to your forecasting model reduces manual errors and streamlines updates [7].

The transition from historical data to future assumptions is where many forecasts falter. Begin by calculating historical averages and trends like monthly sales growth rates, days sales outstanding (DSO), and customer payment behaviors (e.g., enterprise vs. SMB) [4].

For sales growth, analyze both year-over-year and month-over-month trends by product or channel. Adjust these figures based on factors like sales pipeline, team capacity, and marketing budgets rather than applying a flat percentage [5]. For collection cycles, use your average DSO as a baseline. For instance, if your current DSO is 55 days, assume 50–60 days unless you’re implementing changes like stricter payment terms or improved collections tools [6].

Classify expenses into fixed (e.g., rent, payroll) and variable (e.g., sales commissions, cloud usage fees). Model these as flat amounts, step-changes tied to hiring, or percentages of revenue, depending on their nature [5]. Consider U.S.-specific factors like payroll taxes, health insurance costs, and common vendor terms (Net 30/45/60). Analyze at least two years of historical data to identify seasonal trends, such as Q4 retail surges or summer slowdowns in certain industries [2][3]. Use this data to create seasonal indices (e.g., November at 120% of average, January at 80%) and factor in irregular expenses like annual insurance premiums or bonuses.

A strong forecast goes beyond cash flow - it integrates your income statement, balance sheet, and cash flow statement into one cohesive model. This approach minimizes errors and provides a full financial picture.

Start with a driver-based income statement forecast, incorporating assumptions for revenue, cost of goods sold (COGS), operating expenses, interest, and taxes [5]. Then, build detailed balance sheet projections. For example:

The cash flow statement ties it all together by reconciling net income to cash. Adjust for non-cash items like depreciation and stock-based compensation, account for changes in working capital, and include investing and financing activities [9]. Use checks like a cash roll-forward (beginning cash + net cash flow = ending cash) to ensure all statements align and your forecasted cash matches your bank balance [5].

Relying on manual spreadsheets or disconnected systems often leads to errors. Modern tools can streamline the process by automatically pulling and categorizing bank transactions, updating forecasts via APIs, and syncing with accounting systems to keep actuals aligned with projections [2][7]. Look for platforms that offer dashboards and scenario modeling to simplify reporting for management and boards [2][9].

For many growth-stage companies, fractional CFO and FP&A services can be game-changers. These experts can design tailored forecasting frameworks, build integrated models, and establish review processes. For example, Phoenix Strategy Group offers services like bookkeeping, fractional CFO support, and FP&A systems to help companies align their financial operations with growth goals.

As David Darmstandler, Co-CEO of DataPath, shared: "As our fractional CFO, they accomplished more in six months than our last two full-time CFOs combined. If you're looking for unparalleled financial strategy and integration, hiring PSG is one of the best decisions you can make." [1]

Getting cash flow forecasts right is essential for maintaining financial stability. Below, we’ll dive into how to fix common forecasting errors and improve your process.

Revenue forecasts often go wrong when they assume every deal in the sales pipeline will close. A better approach? Weight your pipeline using historical win rates. For example, if 60% of your late-stage deals typically close, forecast only 60% of that value. Also, separate new revenue from recurring revenue, as they have different ramp-up periods and sales cycles.

When it comes to collections, don’t just rely on invoice dates. Use actual payment terms and days sales outstanding (DSO). Analyze aging reports to see how invoices are collected - whether within 30, 60, 90, or even 120+ days - and apply those trends by customer type. Keep in mind that enterprise and international clients often have longer payment cycles. Build in a late payment factor by assuming only part of the billed amounts will arrive on time, and account for bad debt using historical write-off percentages. To stay prepared, create conservative, baseline, and optimistic scenarios for revenue and collections, and use the conservative case when planning your cash runway.

Lastly, adjust your forecast to reflect seasonal and cyclical patterns.

Straight-line forecasting ignores the natural ups and downs in your business. To capture these fluctuations, review 24–36 months of cash data and chart it to uncover trends. For example, you might notice Q4 holiday surges, Q1 budget freezes, or slower summers. Use these insights to calculate month-over-month and year-over-year changes, and apply seasonality factors. If December revenue is typically 130% of your monthly average while January drops to 80%, adjust your projections accordingly.

Don’t forget to factor in industry-specific cycles, like B2B budget planning seasons, weather impacts on construction, or school calendars. These insights allow you to forecast potential cash flow gaps during slower periods and plan accordingly.

Even the most accurate assumptions won’t help if you forget to include all cash events. Use a standardized checklist to ensure nothing gets missed. Make sure to account for:

A thorough checklist helps you avoid overlooking irregular or miscategorized items.

Accurate forecasting starts with clean, organized data. Relying on manual spreadsheets or scattered data sources increases the risk of errors. Instead, centralize your financial data by integrating core systems into a single forecasting model or FP&A tool. This reduces manual input and keeps your forecast aligned with real-time transactions. Ensure your system has clear assumptions and audit trails to track changes.

Regularly validate your data. Compare forecasted cash balances with actual bank balances, check that accounts receivable aging matches forecasted collections, and confirm payroll registers align with planned amounts. These checks catch errors early and build trust in your numbers.

To keep your forecasts accurate, adopt a rolling review process. Maintain a 13-week rolling forecast updated weekly and a 12- to 18-month forecast refreshed monthly. Conduct monthly variance analyses to compare actual results against forecasts and adjust assumptions as needed.

Break down variances in collections, payroll, vendor payments, taxes, and capital expenditures. Identify whether differences are due to timing or unexpected changes, and update your assumptions. For example, if collections are consistently delayed by 15 days, adjust your DSO assumption. Document these findings in a variance log and review them regularly with your leadership team. Engaging cross-functional teams - like sales, operations, and HR - ensures the forecast becomes a collaborative tool, not just a finance exercise.

For businesses in growth mode, consulting with financial advisors can be invaluable. Firms like Phoenix Strategy Group specialize in financial and strategic planning, offering cash flow forecasting support to help businesses stay on track as they scale.

A cash flow forecast is a key tool for guiding decisions around spending, hiring, investing, and fundraising. It’s important to remember that cash flow - not profit - keeps the lights on. Salaries, vendor payments, and bills are all paid with cash, and the timing of that cash flow can heavily influence investor confidence [5]. By leveraging these insights, businesses can better manage their cash runway and make informed strategic decisions.

Your cash flow forecast can pinpoint when your business might run out of money under different scenarios. Creating three projections - base, downside, and upside - can help you understand how changes in revenue, collections, or spending could impact your runway [5][7][8]. To stay ahead, start planning your next funding round 6–12 months before your forecasted cash depletion date, especially given the typical timelines for U.S. fundraising.

History has shown that companies with strong cash forecasting and liquidity management were better equipped to handle disruptions like COVID-19. They made faster strategic decisions and avoided the higher funding costs that often arise during economic downturns [9]. For example, Phoenix Strategy Group has helped portfolio companies raise over $200 million in the past 12 months by using forecasts to secure higher valuations and align teams around critical growth milestones [1].

Once you’ve analyzed your forecast, the next step is to align your day-to-day operations with these financial insights.

Your cash flow forecast should directly shape decisions around hiring, inventory purchases, and vendor payment terms. It’s worth noting that hiring immediately impacts cash flow, even though the revenue generated by new employees might not materialize for 3–6 months. Similarly, infrastructure investments often require upfront payments with delayed revenue recovery [3][5][8].

To avoid cash flow crunches, link hiring plans to forecasted revenue and cash availability. Factor in realistic ramp-up times for new employees and the costs of benefits. If downside scenarios show a tighter runway, consider delaying or phasing out hiring plans. Additionally, translate your forecast into monthly targets for revenue, collections, hiring, and expenses - and regularly review these targets against actual performance [4][7]. A rolling 13-week cash flow forecast, updated weekly, can be especially effective for managing short-term liquidity [8].

David Darmstandler, Co-CEO of DataPath, highlighted the value of financial expertise: "As our fractional CFO, they accomplished more in six months than our last two full-time CFOs combined. If you're looking for unparalleled financial strategy and integration, hiring PSG is one of the best decisions you can make." [1]

By tying forecasts directly to operations, you’ll also set the stage for stronger discussions with your board, lenders, or potential acquirers.

Accurate forecasts combined with operational insights form the backbone of effective communication with boards, lenders, and M&A prospects. These stakeholders expect cash flow forecasts that are clearly tied to your profit and loss statement (P&L) and balance sheet. Missing or unclear cash bridge explanations can raise red flags during financing or M&A processes [5][9].

For board meetings, present a detailed cash bridge covering 12–24 months. This should outline financing needs and how funds will be allocated - whether for headcount, product development, or market expansion [5][7][9]. Scenario analysis can also be a powerful tool in board reports, showcasing funding requirements and strategic options under different market conditions [5][7][9].

Lenders, on the other hand, focus on your ability to generate steady cash flow to service debt. Highlight projected EBITDA, operating cash flow, and debt service coverage ratios (DSCR), supported by realistic assumptions around revenue, margins, and collections. Include a working capital schedule to show how accounts receivable, accounts payable, and inventory impact cash flow. Sensitivity analyses, such as the impact of a 20% revenue drop or slower collections, can further demonstrate your preparedness to handle financial shocks [5][7][9].

For M&A discussions, forecasts play a crucial role in supporting your valuation narrative. Use them to highlight your growth trajectory, margin improvements, and unit economics. Demonstrating that your business can meet post-acquisition performance targets without liquidity issues strengthens your position. Phoenix Strategy Group, which has facilitated over 100 M&A transactions, specializes in helping founders prepare for exits by implementing due diligence systems and maximizing deal value [1].

Lauren Nagel, CEO of SpokenLayer, shared her experience: "PSG and David Metzler structured an extraordinary M&A deal during a very chaotic period in our business, and I couldn't be more pleased with our partnership." [1]

Finally, ensure you have a clean, well-documented 3-statement model (P&L, balance sheet, and cash flow). Reconcile cash flow from net income, clearly outlining non-cash items, working capital changes, and financing flows. A polished model with detailed support schedules can significantly boost lender confidence, improve deal terms, and attract buyer interest [5][9].

Cash flow forecasting isn’t just a numbers game - it’s a critical tool for keeping your business on solid ground. It helps you manage hiring, spending, and fundraising decisions while ensuring you have enough cash to cover daily operations. The truth is, profit on paper doesn’t always mean cash in the bank. You could be growing revenue while struggling to pay your team or vendors if collections slow down, capital expenses stack up, or working capital shifts catch you off guard.

To avoid these common pitfalls, steer clear of overly optimistic revenue projections, ignoring seasonality, leaving out key cash items, relying on outdated data, or updating forecasts too infrequently. These missteps can lead to cash shortages, strained relationships with lenders, and stunted growth. The good news? The fixes are simple: base assumptions on historical data, account for seasonal trends, include all cash flows, improve data accuracy, and maintain a rolling forecast that you revisit regularly - ideally every month.

The benefits of solid cash flow forecasting are clear. It helps you understand how long your cash will last under different scenarios, pinpoint when to kick off your next funding round, and approach board meetings, banks, or potential acquirers with confidence. Businesses that treat forecasting as an ongoing process - updating it regularly, tying it to daily operations, and using scenario planning - are better equipped to handle uncertainty, avoid costly last-minute decisions, and turn risks into opportunities.

What does this look like in practice? Start by creating or upgrading a rolling 13-week cash flow forecast. Review your assumptions to ensure they’re realistic and align the forecast with your leadership team’s regular discussions. Make cash flow a permanent agenda item, not an afterthought. If your team doesn’t have the time or expertise to build a robust forecasting system, Phoenix Strategy Group can help. Their financial experts design integrated cash flow models that connect your P&L, balance sheet, and cash flows - turning forecasts into actionable dashboards, hiring strategies, and funding milestones tailored to your growth stage.

Investing in better cash flow forecasting is one of the smartest moves you can make to safeguard liquidity and grow sustainably. By treating it as a core business discipline, you’ll navigate challenges more smoothly, grow with fewer surprises, and be in a stronger position when it’s time to raise capital or plan your next big step.

Many businesses face challenges when it comes to cash flow forecasting, often due to a handful of recurring mistakes. One of the biggest culprits? Overly optimistic revenue projections. When forecasts rely on assumptions that are too rosy, it’s easy to underestimate potential cash shortages, leaving businesses scrambling to cover gaps. The key here is to base your projections on realistic, data-backed assumptions.

Another common misstep is overlooking irregular expenses or seasonal trends. For instance, periodic costs like annual insurance premiums or the inevitable slowdown in sales during certain times of the year can throw off your forecast if not accounted for. On top of that, failing to update your forecast regularly as new data comes in can leave you blindsided by unexpected changes.

To steer clear of these issues, make sure your forecasts are rooted in accurate historical data and are revisited frequently. For businesses in growth stages, seeking expert financial guidance - like fractional CFO services or FP&A support - can be a game-changer. These resources can provide deeper insights and help fine-tune your forecasting approach.

Seasonal trends can have a big impact on cash flow, causing shifts in both revenue and expenses at certain times of the year. Take retail businesses, for instance - they often experience a surge in sales during the holiday season, but then grapple with slower months afterward.

To navigate these ups and downs, it's important to dig into historical data and fine-tune your forecasts. This way, you can prepare for leaner periods and make the most of your resources during busy seasons.

Keeping your cash flow forecasts updated is essential for staying on top of your business's financial well-being. It enables you to spot potential cash shortages ahead of time, adjust for unexpected costs, and make smarter decisions that promote both growth and stability.

By regularly reviewing and revising your forecasts, you can factor in shifts in revenue, expenses, or market trends. This way, your projections stay relevant and useful. Taking this proactive step helps you sidestep unpleasant surprises and stay ready to tackle challenges or seize opportunities as they come your way.