Published on

May 16, 2026

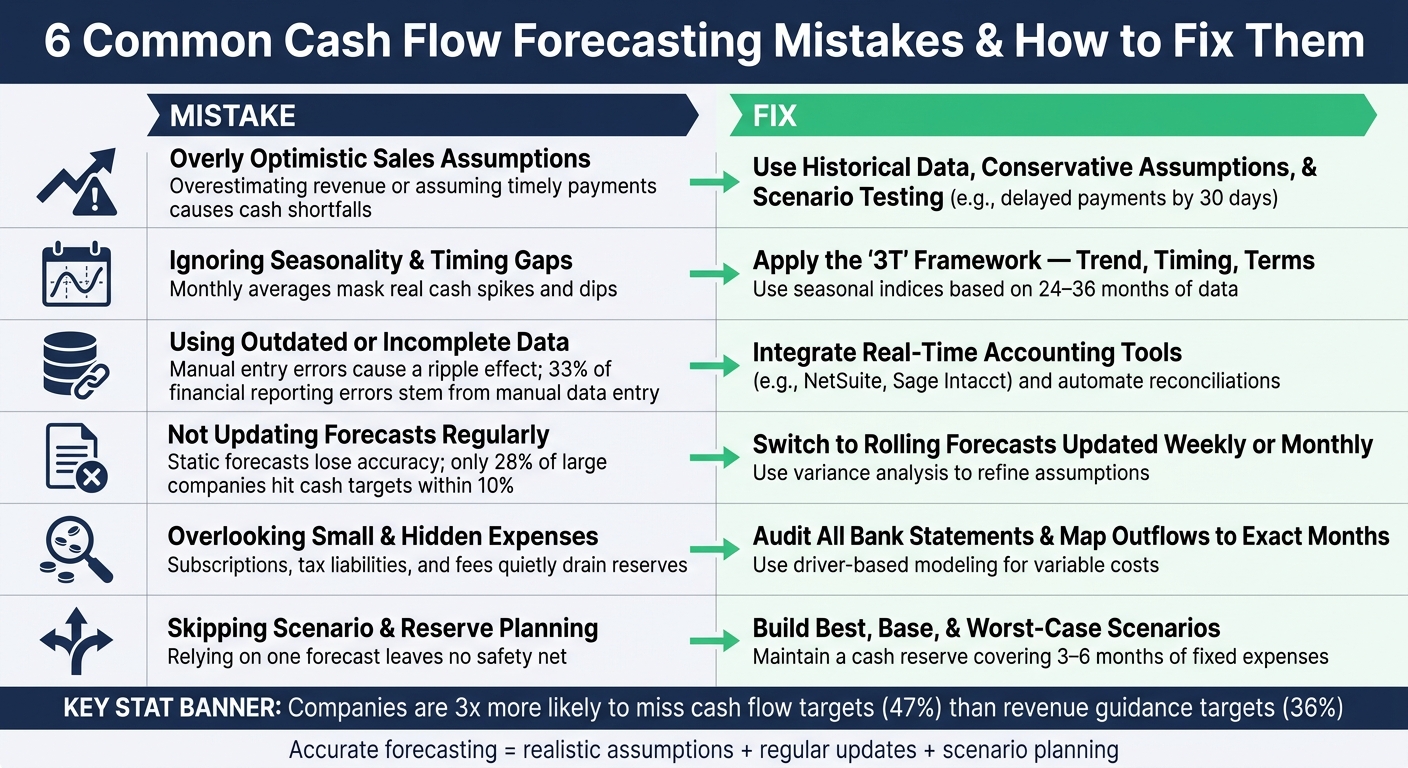

Cash flow forecasting is critical for managing a business's finances, especially during growth phases. However, many businesses make avoidable mistakes that can lead to financial trouble. Here are the six most common errors and how to address them:

Key Takeaway: Accurate forecasting requires realistic assumptions, regular updates, and planning for multiple scenarios. Avoid these pitfalls to safeguard your cash flow and support growth effectively.

6 Common Cash Flow Forecasting Mistakes & How to Fix Them

Many businesses fall into the trap of overestimating revenue, assuming timely payments, and overlooking customer churn. This creates forecasts that crumble when cash inflows don’t align with expectations.

Setting aggressive sales goals can lead to costly missteps, like over-hiring, overstocking, or expanding prematurely - all based on revenue that might not materialize. When payments are delayed, businesses often struggle to meet their financial obligations.

"One of the more common mistakes is to overestimate sales, which often leads to a cash shortfall." - Community Bank, N.A. [2]

Another hidden risk occurs when sales teams offer extended payment terms to close deals. As EY points out: "A typical example is a sales team that agrees to preferential sales terms - a longer period to pay - to close a deal. The team is rewarded for the win, but the easy payment term means the cash is not available until later." [3]

Data highlights the challenge: only 28% of large global companies achieve cash forecasts within 10% of their annual free cash flow targets. Additionally, businesses are three times more likely to miss cash flow targets (47%) compared to revenue guidance targets (36%) [3]. Rising financing costs - more than doubling since 2021 - make these errors even more costly.

The best approach is to base forecasts on historical data rather than overly optimistic projections. Use real payment histories to establish realistic collection timelines, factoring in the average Days Sales Outstanding (DSO) instead of assuming invoices are paid promptly. Don’t forget to account for historical churn rates to ensure recurring revenue forecasts are accurate.

Scenario testing can also help validate assumptions. Consider questions like: What if our two biggest customers delay payments by 30 days? Can we still meet payroll and pay suppliers? Bridging the gap between sales and finance is equally important, often requiring expert cash flow management. When sales teams understand how extended payment terms impact cash flow, they can make smarter decisions [3].

Here’s a quick summary of common pitfalls and how conservative adjustments can help:

| Assumption Area | Optimistic Trap | Conservative Approach |

|---|---|---|

| Sales Forecast | Over-hiring and over-purchasing based on revenue that doesn’t materialize [2] | Use historical trends and adjust for market conditions [4] |

| Payment Timing | Assumes all customers pay on time; ignores extended terms granted by sales [3] | Map inflows using actual AR aging and average collection days [4] |

| Customer Churn | Ignores lost recurring revenue, creating a silent gap in the budget [4] | Factor in historical churn rates and revenue shrinkage [3] |

Even the healthiest sales pipelines can hit roadblocks if cash timing isn't carefully managed. Seasonal revenue fluctuations, uneven billing cycles, and mismatched expense timing can create gaps between when revenue is earned and when cash is available. These challenges are especially tough for growth-stage companies. Ignoring these timing issues can lead to distorted forecasts and even supply chain disruptions.

Cash flow forecasts often rely on monthly averages, but these averages can mask the real spikes and dips that lead to cash shortages. As Model Reef emphasizes:

"Seasonality is the #1 reason 'average-based' forecasts fail: cash moves in spikes, not smooth lines." - Model Reef [5]

Seasonality impacts cash flow in several ways, such as collections timing, calendar payments, and working capital needs. For example, a retail business might have to spend on holiday inventory six to eight weeks before seeing the revenue from those sales. This lag can strain cash flow, especially for growth-focused companies that tend to invest in inventory or marketing well ahead of their cash inflows.

To address these timing gaps, it's crucial to align your forecast with actual cash movement instead of relying solely on smooth monthly averages. The "3T" framework can help:

Instead of manually adjusting forecasts, use seasonal indices to refine your assumptions. For instance, if historical data shows a 15% increase in receipts during Q4, incorporate that into your model. Analyzing 24–36 months of bank statements can help you spot consistent seasonal trends and filter out one-off anomalies. For businesses with significant intra-month fluctuations - like payroll, taxes, or collections - weekly forecasting might offer better accuracy.

| Seasonality Driver | Cash Flow Impact | Recommended Adjustment |

|---|---|---|

| Collections Timing | Customers may pay earlier or later around holidays or quarter-ends | Apply a seasonal index to the collection curve |

| Inventory Builds | Cash outflows occur 6–8 weeks before peak sales | Model working-capital indices tied to sales volume |

| Calendar Payments | Annual tax bills, bonuses, and vendor renewals create spikes | Use calendar-based spend profiles instead of monthly averages |

| Billing Cadence | Monthly vs. annual billing creates uneven inflows | Map receipts based on renewal cohorts and billing cycles |

For example, a large North American food and beverage company replaced its manual forecasting with an AI-powered model. This switch improved forecast accuracy to 96% and extended their reliable forecast horizon from one month to six months [1]. The real improvement came from modeling cash receipts instead of revenue, capturing when cash actually hit their accounts. For more insights on aligning forecasts with cash realities, check out Phoenix Strategy Group.

Even the best-structured cash flow forecast can crumble if it's based on outdated or incomplete information. When you rely on AR/AP balances that haven’t been updated, overlook invoices, or use disconnected systems, you’re likely to end up with an inaccurate view of your cash position.

One major issue is the lack of communication between departments. For instance, sales teams might extend payment terms to close deals, but finance teams may still assume cash will arrive on schedule. This disconnect can lead to unexpected shortfalls. It underscores why keeping data up to date is critical for accurate forecasting.

Manual data entry only adds to the problem. As Community Bank N.A. points out:

"One wrong entry can have a ripple effect compounding the inaccuracy of all the financial reports that feed into a cash flow forecast." [2]

This ripple effect is more widespread than many finance teams realize. In fact, 33% of financial reporting errors stem from manual data entry [2]. And the consequences can be severe: over a seven-year period, only 28% of large companies' cash forecasts were accurate within 10% of their annual free cash flow targets. Moreover, companies are three times more likely to miss cash flow targets (47%) than revenue guidance targets (36%) [3].

Another challenge is aggregated forecasts. Overestimated inflows can offset underestimated outflows, giving a false sense of accuracy. This is particularly risky for growth-stage companies, where financing costs have more than doubled since 2021. The margin for error is much smaller in these scenarios [3].

The solution begins with integrating your forecasting tools with real-time accounting and operational data. Connecting systems like NetSuite, Sage Intacct, or Microsoft Dynamics 365 can eliminate data delays and errors. Automating reconciliations ensures your forecasts reflect real-time operations [6]. For growth-stage companies, having precise and timely data is essential to managing cash flow in unpredictable markets.

However, technology isn’t the only answer. Strong data governance is equally important. Teams across sales, procurement, and supply chain must take responsibility for the cash flow implications of their decisions. For example, a US retail company partnered with EY-Parthenon in 2024 to address data connectivity across $3.4 billion in inventory, AP, and AR. This effort improved visibility and reduced their liquidity buffer by up to $610 million [3]. Similarly, a national health services company linked operational teams directly to the finance forecasting process, cutting variances by $450 million to $535 million and saving $6 million in borrowing costs through better timing [3].

Peter Kingma, EY-Parthenon Principal, sums it up well:

"A company that has only a vague idea of when cash will be coming in and available for use, compared to when it must make payments to meet its obligations, will tend to stockpile cash or inventory as a hedge against uncertainty - and that is an extremely expensive way to manage risk." [3]

For growth-stage companies tackling these challenges, Phoenix Strategy Group offers data engineering and FP&A services designed to integrate financial and operational data into one reliable forecasting system.

Cash flow forecasts aren’t a “set it and forget it” tool. They need constant updates to reflect changing realities - whether it’s a deal closing, an unexpected expense, or a delayed payment. What worked in a forecast three months ago might no longer hold true today. As Community Bank N.A. explains:

"Forecasting should be a continuous activity with frequent adjustments that reflect where your finances are at any given point." [2]

Failing to update forecasts can lead to some serious consequences: emergency borrowing, missed opportunities for investment, and even tension with suppliers. For growing businesses, where working capital is often reinvested into hiring, purchasing, or development, outdated forecasts can be a significant risk. In fast-changing conditions, static forecasts quickly lose their relevance.

Even small errors in forecasting can snowball over time. For example, an overestimated collection in January could snowball into a cash shortfall by March. This is especially critical for growth-stage companies, where tight margins and extended receivable cycles make early detection of cash gaps essential. Spotting a gap six weeks in advance allows time to explore solutions. But finding out just six days before? That’s a scramble with limited options.

Beyond liquidity, outdated forecasts create a strategic blind spot. Without regular updates, it’s hard to identify what’s causing cash flow issues - like slow-paying customers or seasonal sales dips. This lack of clarity forces decisions based on guesswork rather than data. That’s why rolling forecasts have become the go-to solution for maintaining agility.

The key to keeping forecasts relevant is regular updates. Instead of relying on static, annual models, switch to rolling forecasts that are updated weekly or monthly. Unlike fixed forecasts that end with the fiscal year, rolling forecasts continuously extend their horizon by adding a new period as each one concludes. This approach keeps your financial outlook fresh and actionable.

| Feature | Static Forecast | Rolling Forecast |

|---|---|---|

| Update Frequency | Periodic (Annual/Quarterly) | Continuous (Weekly/Monthly) |

| Data Basis | Historical trends | Real-time operational data + Actuals |

| Horizon | Fixed (ends at fiscal year-end) | Fluid (always looks 3–12 months ahead) |

| Accuracy | Decreases over time | Maintained through regular adjustments |

| Primary Use | Budgeting and goal setting | Liquidity management and strategic agility |

To further improve accuracy, incorporate regular variance analysis. This means comparing your forecasted numbers against actual cash inflows and outflows, then investigating any discrepancies. Over time, this process helps refine your assumptions and improves reliability. High-performing companies often achieve up to 90% quarterly accuracy when they consistently refine their forecasts [3].

For even better results, consider leveraging AI-based forecasting tools. These tools can boost accuracy to 96% while reducing manual effort by 30% [1]. This is especially helpful for growth-stage teams with limited resources. Phoenix Strategy Group, for instance, offers FP&A and data engineering services designed to help businesses build a real-time, rolling forecast system. With this infrastructure, you can keep your financial insights up-to-date - without adding a ton of extra work.

Tracking big-ticket expenses like rent or payroll is straightforward, but smaller recurring costs - such as annual software subscriptions, tax liabilities, transaction fees, or one-off bills - can quietly chip away at your cash reserves.

"Unexpected bills, tax liabilities, or annual subscriptions can punch a hole in your budget." - Cartesian FinOp Partners [4]

When small expenses pile up, they can throw off your cash flow projections, creating a disconnect between reported profits and actual cash on hand. A business might appear profitable on paper while struggling to cover day-to-day expenses. This happens because items like capital expenditures, loan repayments, and working capital fluctuations don’t show up on profit and loss statements but still drain cash.

"Profit is an accounting outcome, not actual money in the bank... A startup can show profit and still run out of cash." - Lior Ronen, Founder, Finro Financial Consulting [7]

Additionally, unexpected cost increases - like a sudden need for new hires or infrastructure - can wreak havoc on cash flow if not properly forecasted. Using driver-based modeling can help predict these outflows more accurately, ensuring you're prepared for growth-related costs.

Start by auditing your bank statements to identify every recurring and irregular expense. Then, map these outflows to the exact months they’ll occur. This step ensures your forecasts reflect when cash actually leaves your account, not just when expenses are incurred.

For variable costs tied to growth - like hiring or infrastructure - driver-based modeling is key. For example, link payroll increases to specific growth milestones and infrastructure spending to usage thresholds. This approach provides a clearer picture of when and how cash will be spent.

| Overlooked Item | Impact on Cash Flow | Solution |

|---|---|---|

| Annual Subscriptions | Large, sudden one-time outflows | Map specific renewal months in the forecast |

| Tax Liabilities | Significant quarterly or annual drains | Set aside reserves and include in mid-term models |

| Hiring Chunks | Sudden spikes in payroll and equipment costs | Tie hiring to specific growth milestones |

| AR Aging | Revenue is "earned" but cash is unavailable | Monitor weekly and use automated reminders |

| Inventory Bloat | Capital tied up in unsold stock | Track turnover and align orders with demand |

In addition to auditing, maintain a cash reserve covering 3–6 months of fixed expenses. This buffer can help absorb irregular or unexpected costs. Automating reconciliations is another critical step - manual bookkeeping errors often hide cash shortfalls, with nearly one-third of financial reporting mistakes stemming from manual data entry [2].

For growth-stage businesses, services like Phoenix Strategy Group’s bookkeeping and FP&A solutions can provide real-time insights into cash flow, helping you stay ahead of potential crises before they escalate.

Overlooking the importance of multiple scenarios can leave your cash flow plan fragile and unprepared for unexpected challenges.

Many growth-stage companies rely on a single forecast, essentially betting everything on one outcome. But in business, things rarely go exactly as planned. For instance, a key customer might delay payment, or an essential piece of equipment could break down right before a critical period. Without alternative scenarios, you're left without a safety net when things go wrong.

Relying solely on a single forecast makes your business vulnerable to sudden economic changes or unforeseen delays that can quickly render your assumptions outdated [1][4]. For growth-stage companies, the difference between reported profits and actual cash flow can be striking. A forecast that looks promising on paper might hide potential cash flow issues if it doesn’t factor in late payments, unexpected hiring needs, or slower-than-expected sales.

Without testing your forecast against multiple potential outcomes, you’re unlikely to identify cash flow gaps until they’ve already turned into full-blown problems [4]. This is where having a solid contingency plan becomes critical.

To avoid being caught off guard, build at least three forecast scenarios: best case, base case, and worst case. These should include different assumptions about revenue timing, customer payment schedules, and unexpected costs. This approach gives you a realistic range of possibilities, rather than a false sense of security. Combining multi-scenario planning with conservative assumptions and regular updates (as discussed earlier) strengthens your financial strategy.

In addition to scenario planning, establish a minimum cash reserve. Aim to cover 3–6 months of fixed expenses, leaning toward the higher end if your business operates in a cyclical industry or relies on long payment terms [4].

"Aim for 3–6 months of fixed expenses in reserves. If your business is cyclical or has long payment terms, lean toward the upper end." - Cartesian FinOp Partners [4]

Another useful tool is sensitivity analysis. For example, model the impact of your top customer delaying payment by 45 days or a 15% increase in a critical input cost. This kind of analysis helps you understand how individual variables could affect your cash flow, enabling you to allocate reserves more effectively and avoid surprises [1].

If this feels overwhelming, consider working with experts like Phoenix Strategy Group. Their fractional CFO and FP&A services are designed to help growth-stage companies build robust multi-scenario financial plans, ensuring you can make informed decisions even when the unexpected happens.

Cash flow forecasting is essential for growth-stage companies aiming to maintain financial health and scale effectively. However, common missteps like overly optimistic projections, ignoring seasonality, relying on outdated data, overlooking hidden costs, and focusing on just one scenario can quickly drain cash reserves and stall progress.

"Accurate financial forecasting can provide an essential roadmap to building a successful business." - Curt Mastio, Managing Partner, Founder's CPA [8]

The good news? These challenges can be addressed with consistent practices. Using conservative projections, maintaining rolling forecasts, ensuring clean and updated data, and planning for multiple scenarios are all strategies that should become part of your regular financial routine - not just emergency measures. By sticking to these principles, businesses can improve forecast reliability while paving the way for sustainable growth.

Need help navigating cash flow management? Phoenix Strategy Group offers fractional CFO services, FP&A expertise, and tools for real-time cash flow tracking to help your company avoid cash gaps and build stronger financial systems.

To create a rolling cash flow forecast, start with your current financial data to estimate future cash positions. Gather essential details like your recent bank statements, accounts receivable, and accounts payable. Then, use a straightforward approach: list your expected cash inflows and outflows on a weekly or monthly basis. Regular updates are key to keeping your forecast accurate and flexible as circumstances change.

To manage late payments or shifts in terms, start by using practical assumptions for receivables and adjusting your projections accordingly. Keep a close eye on accounts receivable aging on a weekly basis and strictly enforce credit terms to maintain control. Automation can also be a game-changer, helping you speed up collections and reduce delays.

Create rolling cash flow forecasts that factor in timing differences, and make sure to update them regularly using real-time data. Additionally, scenario planning for potential payment delays can help keep your forecasts aligned with actual customer payment patterns. This way, you’re prepared for any unexpected shifts.

The right cash reserve for your business depends on its specific needs and the industry you’re in. However, a common rule of thumb is to keep enough to cover 3 to 6 months of operating expenses. This cushion helps ensure you have the liquidity to tackle unexpected challenges and stay steady during unpredictable periods.