Published on

May 3, 2026

Managing cash flow is the cornerstone of turning around distressed assets - assets tied to struggling companies or entities facing bankruptcy or default. These assets are often illiquid and undervalued, but with the right approach, they can deliver high returns. Here's what you need to know:

Key Takeaways:

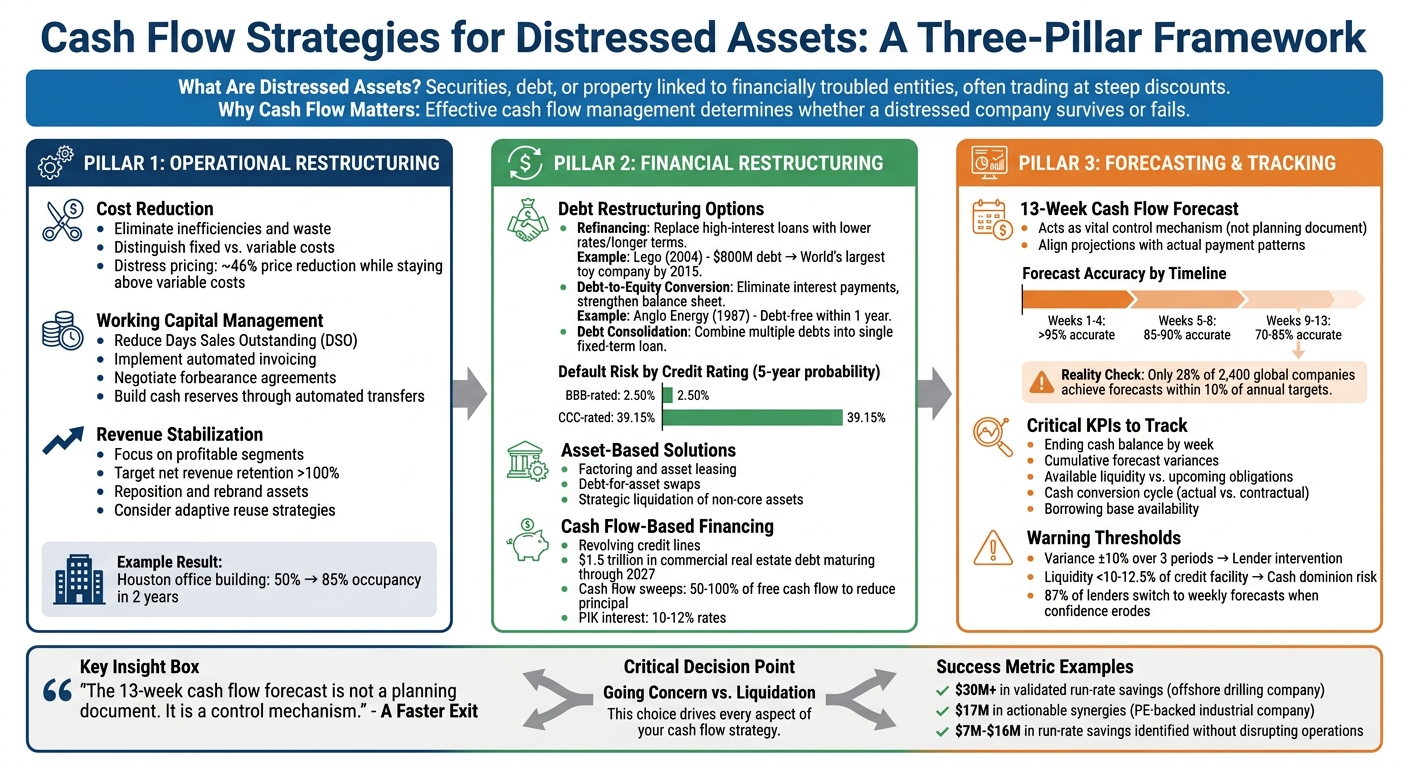

Three-Pillar Framework for Cash Flow Management in Distressed Assets

Reducing costs effectively requires a focus on eliminating inefficiencies and waste rather than making sweeping cuts that could harm operations. By streamlining property management processes and bringing in experienced teams, it's possible to improve occupancy rates while maintaining service quality.

Sometimes, targeted investments can yield better long-term results than basic cost-cutting measures. For example, upgrading HVAC systems or modernizing lobbies can enhance tenant satisfaction, reduce future maintenance costs, and lower vacancy rates. Additionally, buyers can tap into existing infrastructure and operational efficiencies to make distressed assets more profitable.

Understanding the distinction between fixed and variable costs is especially important in tough market conditions. One useful approach is "distress pricing", where prices are set just above variable production costs to maintain cash flow for covering fixed expenses like rent, insurance, and salaries. Investopedia points out that a price reduction of about 46% can still generate profits as long as prices stay above variable costs, emphasizing that this is only a temporary measure while operations adjust [7].

For post-acquisition strategies, the focus should be on managing costs and working capital effectively to stabilize cash flow. Debra Henderson Morgan, Managing Director at CohnReznick, highlights the importance of assuming liabilities that could create immediate value:

"A buyer might want to assume those liabilities that would ultimately be advantageous from both an economic and operational standpoint, thereby creating value on day one" [6].

Once operational costs are under control, the next step is optimizing working capital.

After addressing operational costs, managing working capital becomes essential for ensuring liquidity. At its core, working capital is the difference between current assets and current liabilities, and its efficient management can be the difference between survival and failure for a business [9].

To improve liquidity, consider reducing Days Sales Outstanding by implementing automated invoicing systems and offering early payment discounts. Simplifying invoice processing and scheduling payments strategically can help secure discounts and maintain strong relationships with suppliers.

For distressed real estate assets, challenges like tenant vacancies, deferred maintenance, or overdue taxes often arise. In such cases, negotiating forbearance agreements or loan modifications can provide immediate financial relief [8]. Regular expense audits can help identify non-essential spending, while setting up automated recurring transfers to build reserves creates a financial buffer for downturns or new investments. Additionally, planning for seasonal fluctuations - by adjusting inventory, staffing, or marketing - can prevent predictable cash flow issues [9].

Once costs and working capital are optimized, the focus shifts to revenue stabilization and growth. Concentrating on profitable segments while cutting underperforming areas is key [10][11]. For businesses in growth stages, net revenue retention should exceed 100%. If it falls below 90%, immediate corrective action is needed [11].

A great example of a successful turnaround is J.Crew, which emerged from Chapter 11 bankruptcy in 2020 under Anchorage Capital's ownership. Led by CEO Jan Singer, the company's strategy revolved around three pillars: offering "iconic, timeless products", enhancing the brand experience to strengthen customer connections, and prioritizing e-commerce to counter declining foot traffic [10]. As Singer explained:

"Looking forward, our strategy is focused on three core pillars: delivering a focused selection of iconic, timeless products; elevating the brand experience to deepen our relationship with customers; and prioritizing frictionless shopping" [10].

In the real estate sector, repositioning and rebranding can significantly improve asset performance. For instance, between 2023 and 2025, an investor in Houston acquired a half-empty office building in the Energy Corridor for under $90 per square foot. By rebranding, upgrading amenities, and targeting energy and tech tenants, occupancy rose from 50% to over 85% in two years. This repositioning led to a profitable exit with a strong internal rate of return (IRR) [5]. RealNex emphasizes the importance of focusing on future potential when marketing distressed assets:

"When marketing distressed assets, it's not about the current condition - it's about the future potential. Paint a picture of what the property could be post-turnaround" [5].

Another effective strategy is adaptive reuse, which involves converting underperforming assets into spaces that meet current market demands. Examples include transforming outdated office buildings into life sciences labs, multifamily housing, or co-working spaces. This approach can unlock new value when traditional methods fail to deliver adequate returns [5].

Improving liquidity often goes beyond operational changes. Financial restructuring plays a crucial role in stabilizing cash flow and ensuring long-term viability.

When operational adjustments aren't enough, restructuring debt can reduce cash strain and maintain creditor relationships.

Debt refinancing replaces high-interest or short-term loans with options offering lower rates or extended repayment terms. This approach eases monthly payment obligations, freeing up cash for operations [4]. A great example is Lego's turnaround in 2004. Facing a $238 million net loss and $800 million in debt, CEO Jorgen Vig Knudstorp renegotiated with lenders to secure lower interest rates and longer repayment periods. By 2015, Lego had become the world’s largest toy company by revenue [4].

Another strategy is converting debt into equity. This eliminates interest payments and strengthens the balance sheet [12][4]. For instance, in 1987, investor Martin Whitman acquired $14 million in debt and stock from Anglo Energy, a struggling oil service company. He led the firm through bankruptcy and orchestrated a debt-for-equity deal, leaving the company debt-free within a year [12].

Debt consolidation simplifies cash flow by combining multiple high-interest debts into a single loan with fixed terms [4]. During negotiations, it's critical to address secured creditors first, as they hold the power to foreclose on assets and disrupt operations if left unpaid [4]. Brett Burgan of CohnReznick explains the delicate nature of restructuring:

"Distressed valuation is where the science of valuation truly meets the art of the specialty" [2].

Credit ratings significantly influence default risks. For example, over five years, BBB-rated bonds have a 2.50% default probability, while CCC-rated bonds face a staggering 39.15% probability [13]. Understanding these risks helps businesses choose the right restructuring approach.

Next, we’ll look at how factoring and leasing can provide immediate liquidity.

When quick cash is needed, turning non-core assets into liquidity can be an effective solution. Selling underperforming or non-essential assets not only generates capital but also eliminates inefficiencies [4].

Debt-for-asset swaps allow companies to reduce debt by exchanging physical assets - like property, inventory, or equipment - with creditors [4]. This strategy lowers leverage without requiring cash payments. For manufacturing firms, optimizing supply chains and clearing excess inventory can also improve cash flow [4].

Liquidation, though often a last resort, can sometimes unlock hidden value. For example, Lego's recovery involved selling non-core assets and outsourcing production, which helped the company regain profitability and position itself for future growth [4]. However, distressed assets typically sell at deeply discounted prices, so liquidation should be approached cautiously [13].

Other creative options include barter arrangements with suppliers, which conserve cash by trading goods or services, and negotiating advance payments from customers to bridge short-term liquidity gaps [4]. Before pursuing asset sales or swaps, it’s essential to verify cash flows, legal ownership, and any encumbrances tied to the assets [4].

Securing new financing for distressed assets often depends on demonstrating reliable future cash flows [4][13]. However, assets rated CCC or lower typically face higher interest rates to offset bankruptcy risks [13][1].

Revolving credit lines and short-term loans tied to projected cash flows offer flexibility during financial recovery. Long-term debt provides more breathing room compared to short-term obligations, which can create immediate pressure [14]. Unfortunately, traditional lending options often disappear during financial distress, pushing companies to explore alternatives like private equity, mezzanine debt, or specialized distressed debt funds [4][13][1].

The commercial real estate sector illustrates the growing demand for distressed financing. Roughly $1.5 trillion in commercial real estate debt faces maturity through 2027, with delinquency rates in office and multifamily properties expected to hit 7-10% by mid-2026 [15]. A common trend is "amend-and-extend", where lenders grant two- to three-year maturity extensions to avoid forcing liquidation [15].

Additional strategies include cash flow sweeps, where 50-100% of free cash flow is used to reduce debt principal [15]. Payment-in-Kind (PIK) interest options, often set at 10-12%, can also preserve immediate cash by capitalizing interest payments [15]. For U.S.-based assets, Article 9 of the Uniform Commercial Code allows private sales of business assets within 60-90 days, achieving 75-90% recoveries while avoiding the costs and stigma of bankruptcy [15].

As Oaktree Capital Management notes:

"Distressed debt opportunities... may be, in some cases, 'good companies with bad balance sheets'" [1].

The key is leveraging tangible assets as collateral to secure financing, even when current cash flows are negative [6].

After implementing strategies to restructure operations and financing, the next step is ensuring precise measurement and forecasting to maintain strong cash flow control. For companies in distressed situations, keeping a close eye on cash inflows and outflows is essential to managing liquidity risks effectively.

In challenging financial situations, the 13-week cash flow forecast acts as a vital control tool. Its effectiveness depends on aligning cash receipt projections with actual customer payment patterns rather than relying solely on contractual terms. For instance, if customers typically pay 45 days late, forecasts should reflect that reality.

To create a reliable forecast, use invoice-level details for the first four weeks and historical trends like Days Sales Outstanding (DSO) and Days Payable Outstanding (DPO) for weeks 5–13. Separating fixed obligations - such as payroll, rent, and debt payments - from discretionary spending helps identify areas where liquidity can be preserved quickly. A structured weekly schedule can improve forecast reliability: gather data on Monday, update models on Tuesday and Wednesday, review variances on Thursday, and report to stakeholders on Friday.

Forecast accuracy naturally declines over time. For example, projections are typically over 95% accurate for weeks 1–4, drop to 85–90% for weeks 5–8, and fall to 70–85% for weeks 9–13. A study by EY-Parthenon found that only 28% of 2,400 global companies achieved cash forecasts within 10% of their annual free cash flow targets. In Debtor-in-Possession (DIP) financing, a variance of 10–15% can even lead to a default event [3].

"The 13-week cash flow forecast is not a planning document. It is a control mechanism." – A Faster Exit [3]

Before starting, establish the opening bank balance using actual statements, including restricted cash and sweeps. Classify each receipt as "committed", "expected", or "hopeful", and maintain updated scenarios - base, upside, and downside - to manage liquidity risks transparently.

Once the forecast is in place, the focus should shift to tracking key metrics that help identify potential liquidity issues early.

Accurate forecasting is just one piece of the puzzle. Tracking specific Key Performance Indicators (KPIs) ensures continued liquidity control. Among the most critical KPIs is the ending cash balance by week, which acts as a primary survival metric. It's also crucial to monitor cumulative variances between actual results and forecasts over time, as trends in these variances can be more telling than week-to-week fluctuations. Keeping an eye on available liquidity - cash and credit versus upcoming obligations - can help spot potential "liquidity cliffs" four to eight weeks ahead.

Another important metric is the cash conversion cycle, measured based on actual customer payment timelines rather than contractual terms, to avoid what experts call "collection timing fantasy." Additionally, tracking the borrowing base availability ensures you know how much can be drawn against assets before triggering lender intervention. Maintaining control also means ensuring actual receipts hit 80–90% of forecasted amounts and disbursements stay within 110–120% of the budget.

Persistent variances of ±10% over three consecutive periods can prompt lenders to shift from monitoring to direct intervention. If liquidity dips below 10–12.5% of the credit facility, lenders may take direct control of bank accounts through "cash dominion", limiting spending to a pre-approved 13-week plan. According to one study, 87% of direct lending funds - typically updated monthly - switch to weekly 13-week forecasts when confidence in profit and loss statements erodes [3].

"A proactive forecast is a signal of control. A reactive one is a signal of concern." – A Faster Exit [3]

When a company faces the challenge of distressed assets, having the right financial guidance can make all the difference between recovery and further decline. Phoenix Strategy Group specializes in offering advisory services tailored to businesses dealing with cash flow issues during operational and financial restructuring. Their work focuses on stabilizing and improving cash flow in these high-pressure situations.

Phoenix Strategy Group provides fractional CFO services and FP&A systems specifically designed for environments with distressed assets. Their strategy revolves around creating custom cash flow forecasting models and employing an Integrated Financial Model. This model synchronizes real-time data, allowing businesses to track performance efficiently and maintain both operational and financial stability.

For example, when working with an offshore drilling company struggling with severe liquidity challenges, Phoenix Strategy Group evaluated cost structures across various areas, including administrative functions and supply chain operations. This analysis uncovered over $30 million in validated run-rate savings [16]. In another case, the team partnered with a private equity-backed industrial products and services company, identifying $17 million in actionable synergies and operational improvements that immediately bolstered cash flow [16].

In addition to their advisory services, Phoenix Strategy Group offers technology solutions that provide real-time financial insights. Their tools, such as the Weekly Accounting System and Monday Morning Metrics, ensure financial data is always up-to-date and actionable. These tools help businesses maintain a disciplined approach to forecasting and cash flow management.

The firm's proprietary data engineering capabilities further enhance their offerings by integrating disparate financial systems and streamlining reconciliation processes. This allows management teams to quickly pinpoint liquidity opportunities and act decisively. These tools are essential for implementing the strategies the firm develops, ensuring clients can execute plans effectively.

Phoenix Strategy Group’s expertise has delivered measurable results for its clients. In one instance, their analysis identified $7 million to $16 million in run-rate savings for a distressed business, all without disrupting core operations [16]. These improvements not only boosted cash flow but also provided the flexibility necessary for a successful turnaround strategy.

Handling distressed assets calls for a completely different mindset when it comes to managing cash flow. Traditional approaches often fail to account for the heightened risk of failure that distressed assets face. The methods outlined here - whether it's operational restructuring, debt refinancing, scenario-based forecasting, or liquidity management - are built around one undeniable truth: the biggest risk is losing all future cash flows entirely [13].

The decision to either maintain operations as a going concern or move toward liquidation is pivotal. This choice drives every aspect of your cash flow strategy. Proactive management allows you to stay ahead - whether that means negotiating forbearance, restructuring obligations, or stabilizing revenue streams - before external forces push you into a rushed liquidation at unfavorable prices [2][8]. Techniques like adjusting discount rates through bottom-up unlevered betas, running simulation analyses with probability distributions, or tracking cash-burn ratios can help you understand a range of potential outcomes instead of relying on overly optimistic forecasts [13].

By focusing on these strategies, business owners can take actionable steps to safeguard their cash flow and steer their assets toward recovery.

Proactive cash flow management isn't just important - it’s essential. Start by deciding whether to operate the asset as a going concern or prepare for liquidation. This decision shapes everything from how you value the asset to your restructuring priorities [2]. Update your discounted cash flow (DCF) models to account for the likelihood of distress. For instance, CCC-rated bonds carry a distress probability of 51.38% over ten years, making it critical to factor in such risks [13].

Reassess your cash flow forecasting. Instead of relying on single-point estimates, use probability distributions for key variables like revenue growth and operating margins. This approach reduces the risk of overestimating asset values or underestimating potential vulnerabilities.

For businesses navigating liquidity challenges, tools like Phoenix Strategy Group's Integrated Financial Model and Weekly Accounting System offer real-time insights and precise forecasting. Fractional CFO services and specialized financial advisors can provide the expertise needed to stabilize cash flow and guide distressed assets toward recovery. In situations like these, having the right support can make all the difference between turning things around and further decline.

Deciding between turning a business around or liquidating it comes down to weighing its ability to recover against the severity of its financial struggles. A turnaround might make sense if the company has a reasonable debt load, operates efficiently, and shows potential for future profits. On the other hand, liquidation becomes the logical choice when the company’s assets fall short of covering its liabilities, leaving asset sales and closure as the most practical path forward.

Key factors to consider include analyzing cash flow, assessing the company’s position in the market, and comparing the value of liquidating its assets to the value it could achieve by continuing operations.

A 13-week cash flow forecast breaks down weekly cash inflows and outflows, serving as a vital tool for tracking liquidity and ensuring operational efficiency. It should include variance rules to highlight any deviations from expected figures, making it easier to identify and address potential issues. This approach becomes especially crucial when managing distressed assets, where precise cash management can make all the difference.

When navigating financial challenges, two key metrics stand out for evaluating cash flow:

Both indicators are essential for understanding liquidity levels and ensuring the business can continue operating effectively during tough times.