Published on

December 11, 2025

Multi-entity reporting automation simplifies consolidating financial data across subsidiaries and business units, but it’s not without challenges. For U.S.-based growth-stage companies, scaling operations often leads to fragmented systems, inconsistent data, and manual processes that hinder accurate reporting. Key obstacles include:

Solutions focus on standardizing data models, automating intercompany workflows, integrating systems, enforcing governance, and phased implementation with training. These steps help companies move from manual processes to near real-time reporting, ensuring faster closes, accurate metrics, and compliance with U.S. GAAP. For growing businesses, external advisors like Phoenix Strategy Group can provide essential support in designing scalable, automated frameworks.

5 Key Challenges in Multi-Entity Reporting Automation and Solutions

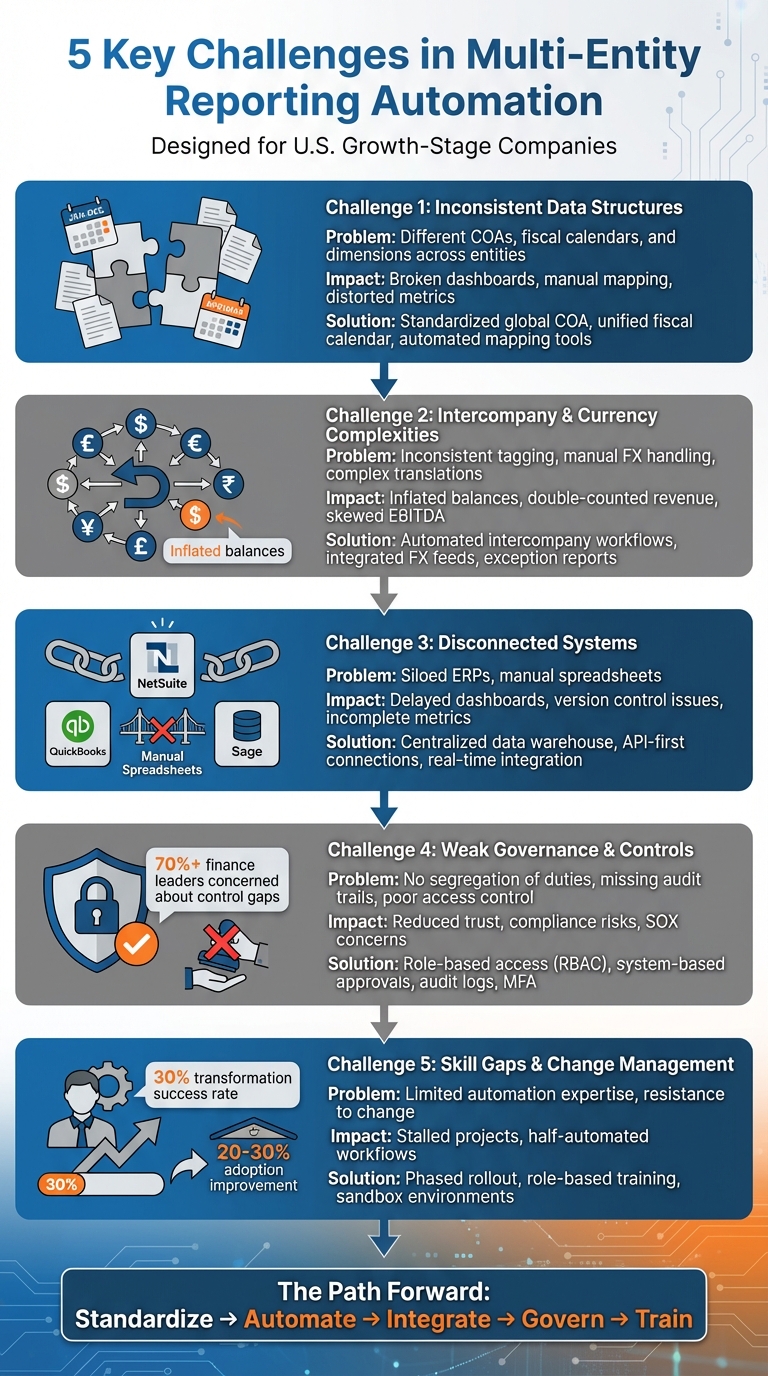

As companies in their growth phase expand - whether through acquisitions or launching new subsidiaries - they often inherit a patchwork of ERP systems. One entity might rely on NetSuite, another on QuickBooks, and yet another on Sage Intacct. Each system comes with its own Chart of Accounts (COA), complete with unique codes, naming conventions, and hierarchies. To complicate matters further, fiscal calendars often vary between entities, making it harder to align reporting periods. Additionally, dimensions such as departments, cost centers, product lines, and regions are typically created independently by each entity, leading to inconsistent labels and levels of detail. These differences arise because local finance teams prioritize their specific reporting needs, and when companies are acquired, their existing structures are often left untouched to minimize disruption.

These inconsistencies create operational headaches. Finance teams are forced to manually map each entity's local accounts to a standardized group structure during consolidation. If COAs change mid-year, automated reporting pipelines and dashboards often break, requiring time-consuming manual fixes. This slows down dashboard updates and delays management reports. Instead of analyzing performance, corporate finance teams end up spending their time troubleshooting structural issues. On top of that, inconsistent data structures distort key metrics like gross margin and EBITDA, making it harder to benchmark performance across entities and make informed strategic decisions.

The solution lies in creating a unified data model supported by robust integration tools. Start by implementing a group-level standard COA with consistent numbering, hierarchy, and naming conventions. This global COA should align with U.S. GAAP requirements for consolidated statements while leaving room for entities to address local or statutory needs without disrupting the overall structure. Each local account should map directly - either one-to-one or many-to-one - to a global account, with governance rules ensuring all accounts are properly mapped before consolidation.

To streamline reporting, adopt a shared fiscal calendar across the organization. A common approach is to use a 12-month period ending on a fixed date, such as December 31. All entities should report according to this calendar for consolidated management reporting. Additionally, establish global master lists for key dimensions - like departments, regions, and products - with standardized definitions and codes.

Modern integration tools can simplify COA mapping. These platforms connect directly to each entity's general ledger through APIs, pulling transaction-level data in real time or on a schedule. They automatically normalize the data into a central model using pre-built mapping tables and flag any new or unmapped accounts for review. This automation minimizes the risk of structural changes disrupting consolidation. Once the data is standardized in a central data warehouse or unified data layer, business intelligence tools can generate real-time dashboards and consolidated reports without relying on manual exports.

For mid-market companies that lack internal data engineering resources, Phoenix Strategy Group offers tailored services, including ETL pipelines, data warehouses, and analytics dashboards. Their fractional CFO and FP&A experts help design and implement standardized data models, enabling finance teams to scale their reporting capabilities efficiently.

Rolling out a standardized model works best in phases:

Governance is key to maintaining consistency. Assign ownership of the global COA and dimension definitions to the group finance team, while local controllers oversee the accuracy of mappings. Change management procedures should require proper approvals and documentation for any updates. Automated validations in consolidation tools can block unmapped accounts or invalid dimensions, generating exception reports for review. Regular quarterly audits and reconciliations can further prevent structural drift from undermining automation.

Once data models are standardized, the next big hurdle is managing intercompany transactions and foreign exchange (FX) issues to achieve smooth, real-time reporting. For multi-entity organizations, intercompany transactions - like loans, management fees, and inventory transfers - can quickly become a headache. The problem gets worse with inconsistent tagging or free-text entries, which make automated matching and elimination nearly impossible. On top of that, when different entities post these transactions to various general ledger accounts, it creates a need for manual mapping rules, adding more complexity to the process.[5][2][3]

Currency translation only adds to the challenge. Organizations need to maintain accurate FX rates, remeasure transactions at the right levels, and handle currency translation for consolidation under U.S. GAAP. This involves distinguishing between functional and reporting currencies and calculating cumulative currency adjustments for equity. It’s a delicate balancing act that leaves little room for error.[2][3]

When intercompany balances remain unreconciled, they can inflate assets and liabilities, double-count revenues and expenses, and distort key cash and liquidity metrics. Poor FX handling compounds the issue, skewing EBITDA and other critical performance indicators, which can mislead both management and investors - especially when internal rates vary across transactions.[3][4][5]

Missteps in identifying an entity’s functional currency can lead to incorrect remeasurement of monetary balances, resulting in misstated FX gains and losses on the income statement. Additionally, unresolved intercompany cash or loan movements can misstate net debt and interest coverage ratios, complicating covenant monitoring and investor reporting.[2][5]

The best way forward is to automate intercompany workflows and integrate FX feeds. Start by defining transaction types - such as loans, fees, allocations, and transfers - with clear account mappings. Require entities to consistently tag their counterparts to enable auto-elimination. Incorporating automated FX rate feeds ensures consistent rates for transaction remeasurement and period-end translation, aligning with U.S. GAAP.[7][1][4][2]

A well-configured consolidation system can automatically match and eliminate reciprocal balances like intercompany accounts receivable/payable, interest income/expense, and intercompany revenue/cost of goods sold. Exception reports can flag unmatched or out-of-balance pairs, so teams focus on fixing anomalies rather than reconciling everything manually.[7][2][6]

Policies for average versus closing rates should be clearly defined - average rates for income statement items and closing rates for balance sheet items, as outlined in ASC 830. These rules should be codified in the system to ensure accuracy. The system should also support identifying functional currencies at the entity level, calculating cumulative currency adjustments in equity for foreign operations, and eliminating intercompany profit in inventory or fixed assets until those profits are realized externally.[2][3]

Many companies start by tackling their largest intercompany flows - like headquarters-to-subsidiary management fees or major trading relationships - and setting up matching and elimination rules for these transactions. Smaller items can still be reconciled manually as the system scales.[3]

For growth-stage companies without dedicated data engineering resources, working with advisors like Phoenix Strategy Group can be a game-changer. They combine fractional CFO services, FP&A expertise, and data engineering to design scalable intercompany frameworks. These advisors can integrate local ERPs with consolidation systems, automate processes to meet U.S. GAAP standards, and deliver reliable, real-time metrics that are crucial for fundraising and investor reporting. By building on standardized data models, this type of automated framework ensures accurate, consolidated metrics that organizations can trust.

Many U.S. growth-stage companies face a common issue: disconnected systems. This often happens due to acquisitions, rapid growth, or isolated purchasing decisions. For instance, one part of the company might use QuickBooks, another relies on NetSuite, and yet another on Sage. Add to that separate payroll platforms, revenue recognition tools, accounts payable systems, and you’re left with a tangled web of tools. Each entity might also have its own bank portal, corporate card provider, and operational systems, leading to multiple logins and inconsistent data formats.

This lack of connectivity forces finance teams to spend hours each week manually pulling data from various systems and trying to make sense of it in outdated spreadsheets. These manual processes are not only time-consuming but also prone to errors. As companies grow and add new entities, accounts, or products, these spreadsheets often break, creating even more chaos. To make matters worse, when multiple people share and edit these spreadsheets, version-control issues arise, leaving teams unsure which file is the most accurate for financial reporting.

Disconnected systems don’t just slow things down - they make it nearly impossible to get accurate, up-to-date financial insights. When each system updates on its own schedule and data is manually pulled, key numbers like cash balances, accounts receivable, or revenue can vary depending on who accessed the data and when. Instead of real-time updates, dashboards often refresh weekly or even monthly.

This delay becomes a bigger problem at the group level. Consolidated metrics like revenue, EBITDA, or cash burn can be incomplete or inconsistent because different entities sync their data at different times. As a result, dashboards lose credibility as the single source of truth. CFOs often fall back on static Excel reports for board meetings or lender updates, which are less dynamic and harder to maintain. In fast-moving industries like subscription SaaS or e-commerce, leadership may only realize critical issues - like liquidity concerns or shrinking margins - when it’s too late to act.

The fix? Build a unified data system that pulls information from all ERPs, bank portals, and operational tools into one centralized hub, such as a cloud data warehouse. This hub should use standardized schemas and mappings to ensure consistency across all data sources. Key features of this approach include API-first connections to core systems, near-real-time or scheduled updates (e.g., hourly for bank or billing data, daily for ERP trial balances), and standardized dimensions for entities, accounts, and currencies.

Start by cataloging all the systems your company uses - ERPs, bank portals, billing platforms, CRM, payroll tools, and others - and identify the key metrics each system provides. Focus on setting up API-based connectors for the most critical systems to automate data collection. Avoid relying on manual CSV uploads or emailed files. Scheduled updates for high-priority data, like bank transactions or revenue systems, help keep dashboards current without overloading systems or driving up costs.

To ensure accuracy, embed validation and reconciliation checks into the integration process. This might include reconciling record counts by entity, validating trial balances to confirm that debits and credits align, and running variance checks against prior periods to spot anomalies. Cross-system checks, such as comparing bank feed balances to cash accounts in the general ledger, can catch missing or duplicate data. Maintaining detailed logs - tracking data sources, extraction times, transformation rules, and user overrides - ensures transparency and supports SOX compliance by making changes auditable.

For companies without in-house data engineering resources, working with advisors who specialize in financial systems and data integration can be a game-changer. Partners like Phoenix Strategy Group can help design automated reporting systems, set up validation checks, and train internal teams. By doing so, they deliver a single, governed reporting environment that simplifies monthly closes, board reporting, and covenant monitoring. This centralized approach not only improves data accuracy but also equips leadership with reliable, real-time insights to make informed decisions.

Automating multi-entity reporting without putting strong controls in place - like strict role-based access and clear segregation of duties - can introduce serious risks. Often, automated systems fail to separate responsibilities effectively. For instance, the same person might prepare journal entries, review them, and approve them, all without system-enforced workflows. Instead, approvals might happen via email, leaving no audit trail behind.

Audit trails are another common weak spot. If someone changes a foreign exchange rule, updates an intercompany elimination mapping, or overrides a KPI calculation, there’s often no record of who made the change, when it happened, or why. In a multi-entity setup, these issues can quickly spiral out of control. With more entities, currencies, and users in the mix, unauthorized changes become harder to track during month-end closes or SOX testing. A survey sponsored by Workiva revealed that over 70% of finance leaders are worried about control gaps in their financial reporting systems, with particular concern over access control and audit logging [5].

Weak controls don’t just increase the chances of errors - they also erode confidence. When stakeholders can’t see who’s responsible for approvals or the history behind the numbers, they start questioning the accuracy of consolidated metrics. Missing audit trails and poor access controls make it tough to prove that reports come from a controlled, reliable source, as required under U.S. GAAP and SOX Section 404. This lack of trust often pushes finance teams back to old habits, like rechecking calculations in spreadsheets, maintaining shadow systems, or overriding automated outputs. As a result, the efficiency benefits of automation disappear, and inconsistencies between dashboards, board presentations, and official filings become more likely.

For U.S. companies gearing up for an IPO or sale, poor governance in automated systems can be a deal-breaker. Buyers and underwriters closely examine the quality of earnings and the strength of the reporting environment. While well-governed automation can add value, weak controls can delay deals or even lower valuations. Auditors now expect more than just manual reviews - they want evidence that automated controls are properly designed and functioning. This includes system logs, documentation of configurations, and proof of approvals [5].

To rebuild trust and improve compliance, a solid governance framework is essential. Treat the automated reporting process as a controlled system, not a black box. Start with role-based access control (RBAC), ensuring each user has only the access they need. For example, accountants at the entity level might have full posting rights for their own legal entity but only read-only access to consolidated reports. Meanwhile, corporate consolidation teams could post group eliminations but not alter source-ERP ledgers. Access should be limited by entity, account group, and function (e.g., view, prepare, approve, post, configure) and reviewed quarterly, with logs kept for SOX compliance.

Next, enforce system-based approval workflows for critical processes like manual journal entries, consolidating adjustments, intercompany eliminations, and restatements. Set clear thresholds - for instance, entries over $100,000 could require controller approval - and align these workflows with U.S. GAAP documentation standards. Make sure the system tracks key details, such as who made changes, when they occurred, and why. These logs should be easily accessible for both internal and external audits, providing a clear trail from dashboards back to transactions.

Additionally, create a group-wide adjustment policy that defines acceptable scenarios (e.g., timing adjustments, FX remeasurement, or management overrides), the required documentation, and approval levels. Implement automation to block unauthorized entries or escalate them for higher-level review. Strengthen data security with multi-factor authentication (MFA), least-privilege access, and encryption for all financial data, whether in transit or at rest. Regularly review user access lists to remove or downgrade access for employees who leave or change roles, ensuring compliance with SOX/ICFR standards.

For growing companies lacking in-house expertise, partnering with specialized advisors can be a game-changer. Phoenix Strategy Group helps U.S. businesses align advanced technologies with sound governance, offering services like bookkeeping, fractional CFO support, FP&A, data engineering, and M&A advisory. By combining technical know-how with well-designed policies and training, they help companies create scalable governance models that keep up with complexity while earning the trust of auditors, investors, and leadership teams.

Finance teams accustomed to manual spreadsheet workflows often face significant hurdles when transitioning to automated, data-driven systems. This shift isn't just about mastering new tools - it demands a complete overhaul in how work gets done. For example, accountants skilled in U.S. GAAP may find themselves unprepared to handle API integrations, data pipelines, or multi-entity consolidation platforms. Without expertise in configuring automated eliminations, foreign exchange (FX) rules, or validation logic, teams often depend on a handful of experts, creating bottlenecks that slow progress.

The complexity grows in multi-entity setups, where each entity might operate using different tools or follow distinct local practices. Efforts to unify these under a standardized automation platform can face resistance, delaying adoption. At the same time, finance leaders often underestimate the time and effort required for redesigning processes, documenting workflows, and conducting user acceptance testing. When roles and responsibilities in the new system aren't clearly defined, confusion can spread, further stalling progress.

Poor change management can derail automation initiatives, leaving projects incomplete and only partially automated. According to McKinsey, only about 30% of digital transformation efforts fully meet their goals, but strong change management can make projects up to three times more likely to succeed. Without it, organizations may automate only a fraction of their intended processes - such as consolidations - while leaving tasks like intercompany matching or FX translation reliant on manual spreadsheets. This creates "half-automated" workflows that fail to deliver the expected efficiencies.

When executives lose confidence in automated reports, they often revert to manual processes, erasing any time savings. Studies by Deloitte, PwC, and Gartner reveal that over 60% of CFOs and more than 70% of finance leaders cite skill gaps and resistance to change as major obstacles to modernizing finance and advancing automation. These challenges can lead to stalled projects, user burnout, higher turnover, and even auditor concerns over undocumented changes and weak controls.

Addressing these issues requires a thoughtful, structured approach that includes phased implementation and targeted training.

A phased rollout strategy, combined with tailored, hands-on training, can effectively bridge skill gaps and reduce resistance to change. Successful automation initiatives often start small, deliver quick wins, and expand gradually. For example:

Training plays a critical role in this process and should be practical and role-specific. Here's how to approach it:

Accenture highlights that companies investing in reskilling and upskilling as part of their automation efforts see adoption rates improve by 20–30%, along with a higher return on investment compared to one-time training sessions.

For growth-stage companies lacking in-house expertise, Phoenix Strategy Group offers advisory services tailored to both financial and technical needs. Their approach combines fractional CFO services, FP&A, bookkeeping, and data engineering to create custom data models, rollout plans, and training programs. These solutions are designed to prepare companies for funding or exit events, ensuring systems are audit-ready and aligned with U.S. GAAP and investor expectations.

Automating multi-entity financial reporting means creating a system that brings together standardized data models, automated processes, centralized integration, and robust governance. Without addressing issues like inconsistent charts of accounts, complex intercompany eliminations, disconnected ERPs, weak controls, and skill gaps, companies will remain bogged down in outdated month-end batch consolidations instead of achieving seamless, decision-ready reporting in USD. This strategy tackles the challenges of fragmented data, intercompany hurdles, siloed systems, and control weaknesses.

To make the leap from batch consolidations to real-time reporting, start by implementing a unified chart of accounts and data model across all entities to establish a single source of truth. Layer on automated intercompany rules and FX translation, and create a centralized, real-time data integration system to keep dashboards continuously updated. Strengthen this framework with role-based access, audit trails, and approval workflows to ensure that automation enhances controls rather than weakening them. These steps work together as a cohesive system, transforming scattered spreadsheets into reliable, actionable financial insights.

For U.S. growth-stage companies, the stakes are even higher. Investors, lenders, and acquirers expect timely and accurate USD-consolidated financials that comply with U.S. GAAP standards. A phased approach - starting with core entities and gradually expanding to advanced FP&A - minimizes risks, builds internal confidence, and delivers quick wins, like shortening the close cycle. Companies that invest in these capabilities now will be better prepared for rapid growth, funding rounds, and potential exits. On the other hand, those who stick with spreadsheets will continue to face trade-offs between speed and accuracy.

Collaborating with experts like Phoenix Strategy Group ensures that consolidation efforts align with U.S. GAAP and meet the expectations of stakeholders.

The way forward requires more than just technical upgrades - it demands a well-thought-out strategy. Evaluate your current data structures, intercompany processes, and system landscape. Develop a phased roadmap, invest in targeted training, and work with advisors who understand both the financial and technical aspects of automation. By taking these steps, organizations can transform multi-entity reporting from a time-consuming chore into a continuous competitive edge.

To keep financial data consistent across various entities, businesses can use a unified data model with standardized formats and definitions, such as those aligned with GAAP reporting. This approach ensures financial reporting remains accurate and comparable.

Automation tools and data engineering techniques, like ETL pipelines, play a key role in simplifying data integration and transformation. These tools ensure that all entities follow the same standards. By focusing on data consistency, companies can make better decisions and navigate compliance requirements more easily.

Managing intercompany transactions and handling foreign exchange (FX) processes efficiently calls for a blend of the right technology and consistent practices. A great starting point is to adopt centralized systems that allow for real-time data sharing across all entities. This approach not only boosts transparency but also helps cut down on manual errors.

For smoother operations, consider using automated reconciliation tools. These tools can quickly match transactions, reducing discrepancies and saving time. Standardizing transaction protocols across your organization is another way to simplify workflows and ensure consistency.

When it comes to managing FX risks, advanced FX management software is a game-changer. Such tools can track currency fluctuations and offer hedging strategies, helping to shield your business from the impact of market volatility.

To ensure robust governance and effective controls in automated reporting systems, businesses should adopt role-based access controls. This approach limits access to sensitive data, ensuring only authorized personnel can view or manage it. Regular audits and automated validation checks play a crucial role in quickly spotting and resolving any irregularities. Clear policies and thorough documentation are also key, providing transparency and ensuring consistency throughout the reporting process.