Published on

March 9, 2026

Securing funding for an e-commerce business comes down to two main options: debt financing and equity financing. Each has its strengths and trade-offs, and the right choice depends on your goals, cash flow, and growth stage.

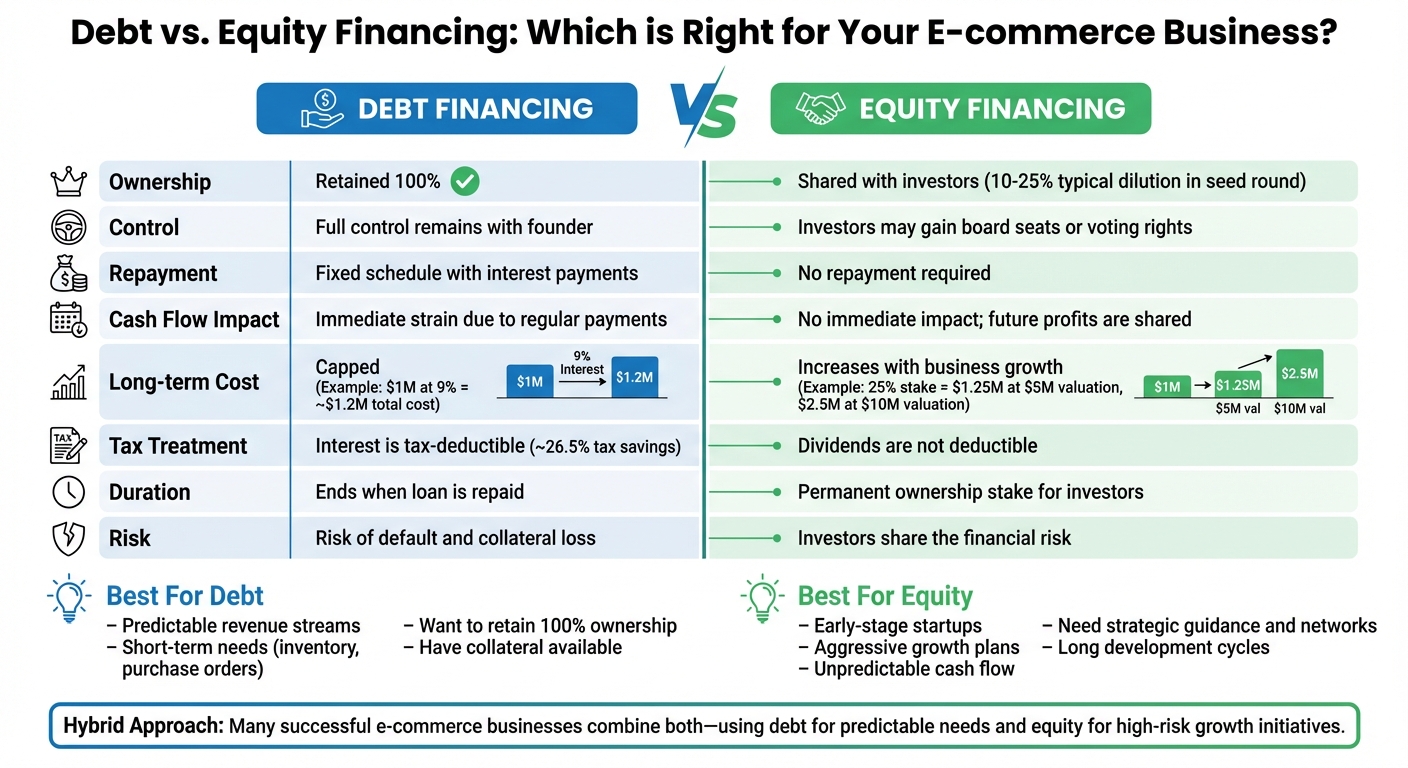

Key Differences:

Quick Comparison:

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Ownership | Retained 100% | Shared with investors |

| Control | Full control | Investors may gain influence |

| Repayment | Fixed payments | None |

| Cash Flow Impact | Immediate strain | No immediate impact |

| Long-term Cost | Capped | Increases with business growth |

For many businesses, a hybrid approach - combining debt for predictable needs and equity for high-risk growth - offers balance. Work with fractional CFO services to align funding with your goals and cash flow capacity.

Debt vs Equity Financing Comparison for E-commerce Businesses

Choosing between debt and equity financing goes beyond just securing funds - it’s about understanding how each option impacts your ownership, control, and daily operations. These two approaches follow completely different paths, and knowing their distinctions is critical for e-commerce founders.

Let’s break it down further.

Debt financing allows you to keep full ownership of your company. When you borrow money, the lender has no claim to your business equity. Once you repay the loan principal and interest, the relationship ends. This means you maintain complete control over your company and all future profits. For founders, this can be a major advantage.

Equity financing, on the other hand, involves giving up a portion of ownership. Selling shares to investors means they own a percentage of your business permanently. For example, raising $500,000 by selling 20% equity means those investors will always own that share - and they’ll also be entitled to 20% of future profits, dividends, and exit proceeds. As Lior Ronen, Founder of Finro Financial Consulting, puts it: "Selling equity means giving up a share of ownership, which can affect control and decision-making in the company" [7].

Another key difference is how these funding options influence control. Debt lenders don’t interfere with your day-to-day decisions. Equity investors, however, often seek a say in major decisions, especially venture capitalists who may negotiate for board seats or voting rights. While this can provide strategic guidance, it also means you’re no longer the sole decision-maker.

Beyond ownership and control, repayment terms and cash flow effects play a big role in distinguishing these financing options.

Debt financing comes with fixed, regular payments that can strain your cash flow. Whether it’s a traditional loan with monthly payments or revenue-based financing with daily deductions, these obligations start immediately. This can put pressure on your cash flow, regardless of how your sales perform.

Equity financing doesn’t require repayment. Investors aren’t looking for monthly checks - they’re betting on your company’s long-term growth and eventual success through acquisition or IPO. This approach keeps your cash flow free for reinvestment in areas like marketing, inventory, or product development. However, the trade-off is permanent: you’re sharing future profits. For example, if your business generates $300,000 in annual profit and you’ve given up 10% equity, you’ll be giving away $30,000 every year - indefinitely [4].

Here’s a quick comparison of the two:

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Ownership | Founder retains 100% | Ownership is shared with investors |

| Control | Full control remains with founder | Investors may gain board seats or voting rights |

| Repayment | Fixed schedule with interest | No repayment required |

| Cash Flow Impact | Immediate strain due to regular payments | No immediate impact; future profits are shared |

| Duration | Ends when loan is repaid | Permanent ownership stake for investors |

| Tax Treatment | Interest is often tax-deductible | Dividends are not deductible |

Tax treatment is another factor to consider. Interest payments on debt are usually tax-deductible, which can reduce your taxable income and improve your net cash flow [1][8]. Equity distributions, however, are not deductible - you’re sharing profits after taxes have already been paid.

Understanding these differences can help you determine the best way to fund your e-commerce growth. Each option has its own set of benefits and challenges, and the right choice depends on your business goals and financial situation.

Debt financing can fuel growth for e-commerce businesses, but it comes with trade-offs that impact financial decision-making. Given the unique cash flow challenges in e-commerce, understanding these pros and cons is essential.

Debt financing offers several advantages that make it appealing for e-commerce businesses:

Ownership Retention: One of the biggest perks is that you keep full control of your business. Unlike equity financing, lenders don’t take a stake in your company.

"With debt financing, you don't have to give up any ownership of the business you've worked so hard to build. This means you still receive all proceeds if you decide to sell in the future" [1].

Tax Advantages: Interest payments on business loans are typically tax-deductible, which can reduce your taxable income and improve your overall cash flow [1].

Quick Access to Capital: Loans can often be secured quickly, sometimes within 24 to 48 hours, especially with lenders specializing in e-commerce. For example, invoice factoring can provide fast funding for large purchase orders without giving up equity [1].

Predictable Repayments: Fixed repayment schedules make it easier to budget and plan. Once the loan is paid off, the obligation ends, and you retain all future profits.

However, these benefits come with challenges that require careful consideration.

Cash Flow Strain: Regular loan repayments must be made regardless of how well sales are going. This can put pressure on your liquidity, especially during slow periods, and limit funds available for growth.

"It's a burden on your company's cash flow. You're responsible for paying every month, no matter what" [1].

Risk of Default: Missing payments can lead to severe consequences, such as losing collateral or damaging your credit score. For loans over $350,000, the Small Business Administration often requires collateral [3].

"Debt has a fixed, non-negotiable claim on your cash flow. If you miss a payment, the consequences are severe and can include bankruptcy" [5].

Restrictive Loan Terms: Many loans come with covenants - conditions like maintaining a specific debt-to-equity ratio or cash reserves. Violating these terms can result in immediate repayment demands, reducing your financial flexibility [5].

| Key Benefits | Drawbacks |

|---|---|

| Retain Ownership: No equity dilution [1] | Cash Flow Pressure: Fixed repayments even during slow sales [1] |

| Tax Deductibility: Interest payments reduce taxable income [1] | Default Risk: Missed payments can lead to collateral loss [1] |

| Lower Long-term Cost: Often cheaper than equity financing [5] | Restrictive Terms: Loan covenants can limit flexibility [5] |

| Fast Funding: Access capital quickly, sometimes within 24–48 hours [1] | Collateral Requirements: May need assets as security [3] |

The choice to use debt financing depends on the specific needs of your business.

"Use equity to fund uncertainty and potential, and use debt to fund certainty and execution" [5].

Debt financing works best in scenarios with predictable revenue, like fulfilling confirmed orders or restocking inventory with proven sales performance.

Next, we’ll explore the benefits and challenges of equity financing for e-commerce.

Equity financing involves trading ownership in your business for capital, which can ease cash flow pressures and drive growth. Here, we’ll break down the advantages and disadvantages of this funding route to help you weigh its fit for your e-commerce business.

Access to Large Capital Pools

Equity financing enables businesses to secure significant funding based on future potential rather than current assets. For instance, angel investors typically contribute between $25,000 and $500,000, while Small Business Investment Companies (SBICs) often invest between $100,000 and $5 million [2][3].

No Repayment Pressure

Unlike loans, equity financing doesn’t involve monthly repayments. Investors earn returns through dividends or by selling their stake later, allowing you to reinvest cash flow into critical areas like inventory, marketing, and product development [1][3]. This approach provides breathing room for growth without immediate financial strain.

Guidance and Networking

Equity investors often bring more than just money to the table. They can offer mentorship, strategic advice, and access to valuable networks, all while sharing the business risk [3][4].

"Equity investors assume the risk when they choose to invest, which means your business assumes less liability." – Victoria Sullivan, Payability [3]

Operational Freedom

Unlike bank loans, equity financing doesn’t come with restrictive covenants or interest payments. This flexibility allows you to focus on long-term strategic decisions based on your growth plans rather than worrying about credit scores or loan terms [3][4][6].

While these benefits are attractive, equity financing isn’t without its challenges.

Reduced Ownership

The primary downside is ownership dilution. In a typical seed round, founders might give up 10% to 25% of their company [5]. Over time, the value of this equity could grow significantly, making the initial trade-off feel costly.

"Equity isn't free. Every percentage point you give up today could be worth 10x more down the line." – Jacob Paduch, Aplo Group [6]

Loss of Autonomy

Equity investors often gain influence over major decisions, sometimes securing board seats or pushing for specific strategies. This can limit your control and even create pressure to pursue exits like sales or IPOs [9][2][5].

Time-Intensive Process

Raising equity funding can be a lengthy endeavor. Between identifying investors, pitching, undergoing due diligence, and negotiating terms, the process can take months, delaying access to the funds you need.

| Key Benefits | Drawbacks |

|---|---|

| Large Capital Access: Up to $5M+ based on growth potential [2][3] | Ownership Dilution: Founders may lose 10%–25% in a seed round [5] |

| No Repayments: Frees up cash flow for reinvestment [1][3] | Loss of Control: Investors may demand board seats and influence decisions [9][2] |

| Investor Expertise: Gain mentorship and strategic networks [3][4] | Exit Pressure: Investors may push for sales or IPOs [2][5] |

| Risk Sharing: Investors share the financial burden [3][4] |

"Equity costs more than debt. Although you aren't paying interest payments, selling equity requires you to give up a portion of your company." – Julianne Pepitone, Shopify [2]

Choosing between equity and debt financing depends on your business’s stage and specific needs. In the next section, we’ll dive into the costs of each approach to help you make an informed decision.

When weighing financing options, it's crucial to dig deeper than just the surface-level costs. Debt financing offers predictable, tax-deductible interest payments, while the cost of equity financing grows as your company becomes more valuable. This difference highlights a key contrast: debt's expenses are capped, but equity's costs can climb sharply.

"The long-term cost of equity isn't paid in interest, it's paid in ownership." – ConnectCPA [10]

One major advantage of debt is the tax shield it provides. For example, if your business pays $50,000 annually in interest and is subject to a 26.5% corporate tax rate, you'd save approximately $13,250 in taxes. That reduces your net annual cost to $36,750 [10]. Equity financing, on the other hand, doesn't offer this benefit - dividends and profit distributions are not tax-deductible [10][12].

Equity financing also introduces uncertainty. As Alexandre Leclerc, Senior Director at BDC, puts it: "The true cost of equity financing is uncertain, as it's hard to predict how much investors will ultimately earn from selling their shares" [12]. For instance, offering a 25% stake in your business today might seem straightforward, but if your company reaches a $5 million valuation, that stake could cost you $1.25 million - or $2.5 million at a $10 million valuation.

"Debt costs less overall - IF your cash flow can support it." – ConnectCPA [10]

To make this clearer, let’s compare a $1 million financing scenario using debt and equity.

Below is a comparison of raising $1 million through debt at 9% interest versus offering a 25% equity stake:

| Factor | Debt Financing ($1M at 9%) | Equity Financing ($1M for 25%) |

|---|---|---|

| Annual Cash Outlay | $90,000 (Interest) | $0 |

| Tax Benefit | ~$23,850 (at 26.5% tax rate) | None |

| Net Annual Cost | ~$66,150 | $0 |

| Ownership Retained | 100% | 75% |

| Cost at $5M Exit | ~$1.2M | $1,250,000 (25% stake value) |

| Cost at $10M Exit | ~$1.2M | $2,500,000 (25% stake value) |

| Control | Full independence [11] | Shared with investors [12] |

This table highlights a vital takeaway: debt financing has a capped cost, whereas equity financing becomes more expensive as your business grows. For instance, if your company reaches a $10 million valuation, the 25% equity stake you issued could cost you $2.5 million - more than double the cost of debt financing [10][13].

That said, debt requires consistent payments, regardless of fluctuations in sales or revenue. Understanding these cost dynamics is essential for aligning your financing strategy with your business's cash flow and growth goals. A fractional CFO can provide the expert analysis needed to navigate these complex trade-offs. By carefully analyzing these factors, you can make a more informed decision that supports your long-term objectives.

Debt financing works best when your e-commerce business has consistent cash flow and a solid revenue track record. Lenders aren’t just looking for optimistic projections - they want to see steady sales over time. This reassures them that you’ll meet repayment obligations, even during slower months. If your business generates reliable monthly revenue and solid profit margins, debt financing can be a smart way to fuel growth without giving up ownership. These conditions make debt financing a helpful tool for managing operational cash flow.

It’s particularly useful in situations like preparing inventory for peak seasons, scaling up a successful marketing campaign, or fulfilling a large retailer order. For instance, CROSSNET used debt financing through invoice factoring to fund a significant order while keeping full ownership of the business [1].

Once you’ve demonstrated steady revenue, the next important factor is collateral. This plays a big role in securing favorable loan terms. Traditional bank loans and SBA 7(a) loans - offering amounts up to $5 million with repayment periods of 7 to 25 years - typically require collateral like equipment, real estate, or high-value inventory [3]. The SBA even guarantees up to 85% of these loans, though collateral is usually mandatory for loans exceeding $350,000 [3]. Asset-backed loans, for example, often provide between 40% and 80% of the asset’s value, depending on how easily it can be liquidated [6].

One major advantage of debt financing is that it allows you to retain full control of your business. You won’t have to dilute your equity or share decision-making power. As Victoria Sullivan from Payability points out:

"The most important question to ask before getting debt financing is how likely you'll be able to make your repayment obligations" [3].

It’s essential to calculate your debt-to-equity ratio before taking on new debt. A high ratio could signal that additional liabilities might be tough to manage [1]. Keeping a close eye on this ratio can help you make informed decisions about taking on debt.

The timing of debt financing also matters. In 2022, Icelandic Glacial Water used short-term bridge financing while waiting for a longer equity raise to close. CFO Raymond Thu explained:

"We had to balance our needs between those efforts versus driving the business" [1].

This allowed the company to maintain operations without losing momentum during the capital-raising process.

Equity financing can be a smart move for e-commerce startups aiming for aggressive growth, especially when expanding into new markets or launching innovative products. It’s particularly useful when long development cycles delay revenue generation. This strategy prioritizes growth potential over immediate profitability, allowing you to focus on scaling while sharing the risks with investors.

For early-stage e-commerce brands, traditional loans can be tough to secure due to limited collateral or credit history. Equity financing, however, hinges on the strength of your business idea and market potential rather than physical assets. This makes it an appealing option for startups that might not be profitable yet but show strong future prospects. It’s also a good fit for businesses with unpredictable cash flow, as it doesn’t rely on steady income streams.

Seasonal businesses - like those with revenue spikes during Black Friday or Cyber Monday - can benefit significantly from equity financing. Unlike debt, which requires fixed monthly payments, equity financing involves sharing profits only when the business is doing well. Jay Jung, Founder of Embarc Advisors, highlights this advantage:

"Equity financing eliminates the risk of default, as there are no fixed repayment schedules. This makes it an attractive option for businesses in early or volatile stages where cash flow predictability is low" [11].

Beyond easing financial strain, equity financing can provide strategic perks. Investors, such as angel investors or venture capitalists, often bring mentorship, industry connections, and operational support - resources that traditional lenders don’t offer. Take Bokksu, for example. This Japanese snack subscription startup, founded in 2015, used equity funding from venture capital firms to invest in market research and product development. This support helped Bokksu grow into a niche leader by covering essential costs during its rapid expansion phase [14].

However, it’s important to weigh the trade-offs. As Joe DiSanto, Founder of Play Louder, points out:

"Essentially, you're taking on a partner who now owns a portion of the company" [11].

If you’re willing to trade some control for growth capital and strategic guidance, equity financing can be an effective way to focus on scaling without the added pressure of fixed loan repayments. It’s a choice that allows you to reinvest your resources directly into growth rather than servicing debt.

E-commerce brands that thrive often take a strategic approach by blending debt and equity to meet their unique business needs. Jacob Paduch, Founder of Aplo Group, captures this philosophy perfectly:

"The most sophisticated operators? They understand that it's not an 'either/or' question; it's about structuring capital in a way that aligns with the long-term goals of the business" [6].

By combining the strengths of debt and equity, a hybrid model maximizes financial flexibility. Debt works best for predictable, short-term needs like inventory purchases or working capital. For example, asset-backed loans typically provide a loan-to-asset value of 40% to 80%, depending on the liquidity of the collateral. These loans are especially useful for financing purchase orders tied to inventory turnover cycles [6]. Equity, on the other hand, is better suited for high-risk, long-term investments such as product development, market expansion, or hiring senior leadership - initiatives that won't immediately generate cash flow to cover debt payments.

A hybrid approach also helps manage timing issues. For instance, when a business needs cash but is in the middle of a lengthy equity funding round, short-term debt can act as a bridge. This ensures operations and growth can continue uninterrupted while equity negotiations are finalized [1].

Before adding debt to an equity-heavy structure, it’s crucial to calculate your debt-to-equity ratio (total debt divided by shareholder equity). This ratio helps gauge whether your business can handle its liabilities without overextending itself. Over-leveraging can create cash flow challenges, especially when debt payments are due regardless of sales performance [1]. Partnering with lenders who understand e-commerce-specific hurdles - like delayed marketplace payments or seasonal inventory needs - can make managing this balance much smoother. Ultimately, aligning your capital structure with your long-term growth objectives is key to sustainable success.

Deciding between debt and equity financing is a pivotal moment for any company. Jared Sorensen of Preferred CFO emphasizes the weight of this choice:

"The question of equity versus debt financing is more than a financial calculation; it's a fundamental decision about your company's trajectory, culture, and ultimately, who holds the keys" [5].

This is where financial advisors step in to provide critical guidance.

Advisors conduct in-depth scenario analyses to evaluate your ability to manage debt repayments, even during challenging times [15][11]. They break down essential metrics like your interest coverage ratio and the potential dilution of your cap table [16]. For example, they can help you manage timing issues, such as securing short-term financing to keep operations running smoothly while waiting on funds from a longer capital raise.

Advisors also introduce financing options tailored to your business model. For e-commerce companies, revenue-based financing is an option that adjusts repayments based on seasonal sales fluctuations [15]. They can guide you through more intricate tools like mezzanine financing or convertible notes, which combine elements of both debt and equity. Additionally, before you approach lenders or investors, advisors often recommend preparing three years of financial statements and forecasts to present a clear path to profitability [15].

The numbers highlight the importance of expert advice: about 70% of businesses secure bank loans, often within weeks. In contrast, only 2.5% land angel investments (a process that can take 2 to 6 months), and just 1% secure venture capital funding [15]. Advisors leverage their networks to provide warm introductions to investors, which are far more effective than cold pitches. They also encourage building these relationships 6 to 12 months before funding is actually needed [15].

Specialized advisory services, like the capital optimization system offered by Phoenix Strategy Group, can further refine your capital structure strategy. Their fractional CFO services are tailored for e-commerce founders tackling challenges like inventory costs and delayed payouts [1][6]. They also perform unit economics analyses to determine which initiatives are best funded with debt - such as predictable growth efforts - and which, like high-risk international expansions, may require equity [15].

When it comes to fundraising, Phoenix Strategy Group helps founders weigh the pros and cons of debt versus equity. Debt allows you to retain ownership but comes with repayment obligations, while equity provides access to significant capital and expertise at the cost of dilution [1][6]. By working with advisors who specialize in e-commerce, you gain a partner who can align your funding strategy - whether debt, equity, or a combination - with your long-term goals. This comprehensive approach ensures your capital structure supports your vision for growth.

Choosing the best funding model for your e-commerce business comes down to finding the right balance between ownership, cash flow, and long-term growth. Debt and equity financing each serve distinct purposes depending on your business's stage. For startups with limited revenue, equity funding offers access to capital without the immediate burden of repayment. On the other hand, established businesses with steady cash flow often turn to debt financing to cover inventory and operational costs while maintaining full ownership.

Your cash flow should play a central role in this decision. Debt financing requires consistent payments, which can be a challenge during slower sales periods. Equity, while freeing up cash for reinvestment, comes with the long-term trade-off of ownership dilution as your business grows in value.

"The brands that win aren't the ones that raise the most; they're the ones that make the smartest capital decisions along the way."

- Jacob Paduch, Aplo Group [6]

For many businesses, a hybrid approach - combining debt and equity - strikes the right balance, offering both financial flexibility and ownership retention.

Working with financial advisors who understand the unique challenges of e-commerce - such as managing inventory, dealing with marketplace payout delays, and navigating seasonal sales fluctuations - can help you build a funding strategy that supports your goals. Ultimately, aligning your funding model with your growth stage and cash flow capacity is essential for driving sustainable success.

Choosing between debt financing and equity financing comes down to key factors like your cash flow, growth stage, and appetite for risk.

Debt financing allows you to keep full ownership of your business, but it comes with the responsibility of regular repayments. These payments can put pressure on your cash flow, especially if your revenue is inconsistent. On the other hand, equity financing doesn’t require repayments, which can ease financial strain. However, it means giving up a portion of ownership and, often, some level of control over your business.

Many businesses opt for a mix of both approaches, aiming to balance growth opportunities with manageable risk. To make the right choice, take a close look at your debt-to-equity ratio and the cost of capital - these metrics can provide valuable insights into the best path forward.

When assessing your ability to handle debt payments, it's crucial to dive into a few key financial metrics. Start with your debt-to-equity ratio, which shows how your total liabilities stack up against your shareholder equity. This ratio offers insight into how responsibly you're using debt - keeping it balanced is a good sign.

Next, pay close attention to your cash flow. Consistent, positive cash flow ensures you have the means to meet your debt obligations without strain. Finally, monitor your debt service coverage ratio (DSCR). This metric compares your net operating income to your debt payments, giving you a clear picture of how well you're positioned to manage both current and future debt.

A hybrid debt-and-equity plan works well for businesses looking to combine the tax advantages and flexibility of debt with the freedom from repayment obligations that equity offers. This strategy is particularly appealing for growth-stage companies that want to scale up without giving up control or putting too much pressure on their cash flow. It's also a smart choice for businesses with unpredictable revenue streams, as it helps balance risk while ensuring adequate funding for both expansion and day-to-day operations.