Published on

June 5, 2026

Deferred Sales Trusts (DSTs) provide a way to defer capital gains taxes when selling appreciated assets. Instead of paying taxes upfront, you can invest the full sale proceeds through a trust, potentially growing your wealth over time. However, DSTs come with setup and ongoing fees that can be substantial, and the benefits depend on the size of your gain, tax rates, and the length of your investment horizon.

Here’s the core takeaway:

DSTs can be a powerful tool but require careful cost-benefit analysis to ensure the tax savings outweigh the fees and trade-offs.

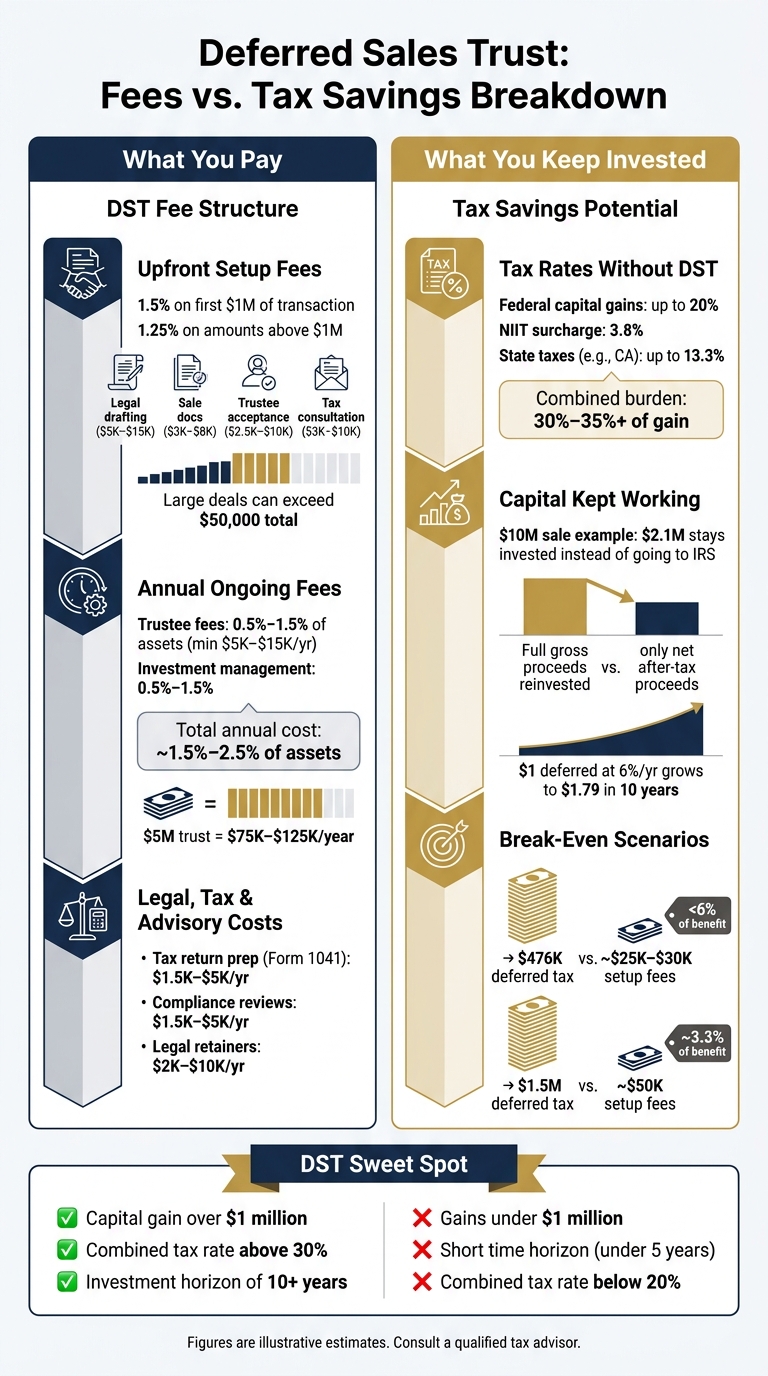

When considering a Deferred Sales Trust (DST), understanding its fee structure is essential to evaluate whether the tax-deferral benefits outweigh the associated costs. These fees fall into three main categories: upfront establishment fees, ongoing annual fees, and legal and advisory costs. Each category plays a role in determining the overall financial viability of a DST.

Setting up a DST involves an initial cost structure based on the transaction value. The fees are 1.5% of the first $1 million and 1.25% on amounts above that [9]. Importantly, these fees are only incurred if the transaction is successfully completed - if the deal falls through, there’s no charge [10].

Breaking down these costs further, the upfront fees typically include:

For larger, more intricate transactions, total setup costs can surpass $50,000 [3].

Timing is critical here. The trust must be established, and the asset transferred into it before the closing of the sale. Missing this step eliminates the possibility of tax deferral [9].

After the DST is established, ongoing fees are another key consideration. Trustee fees typically range from 0.5% to 1.5% of trust assets, with a minimum annual charge of $5,000 to $15,000 [10][7]. Investment management fees add another 0.5% to 1.5%, bringing total annual costs to approximately 1.5% to 2.5% of assets under management [10][9].

For a trust valued at $5 million, this translates to $75,000 to $125,000 per year. To avoid eroding the principal, the trust’s investments must generate returns that exceed these fees.

"The investment allocation is designed to pay for the recurring fees without reducing the overall rate of return sought by the client and the Trust." - My Deferred Sales Trust [8]

Larger trusts (over $5 million) often have room to negotiate tiered or declining rates, potentially reducing annual costs [10].

In addition to trustee and investment fees, there are ongoing professional costs related to legal and tax compliance. These include:

Other charges may arise for specific needs, such as:

"The administrative costs of establishing and managing a DST can be significant, often involving setup fees, trustee fees, and ongoing advisory costs. These expenses can detract from the tax savings benefits, particularly for smaller estates." - Matthew Erskine, Managing Partner, Erskine & Erskine [5]

It’s worth noting that most recurring fees tied to investment management and administration are deductible by the trust, while initial setup costs are usually capitalized. Discussing these distinctions with a tax advisor before closing is highly recommended [10].

Next, it’s important to compare these fee structures with the potential tax savings a DST might deliver.

Selling a highly appreciated asset without a deferral strategy can lead to a hefty tax bill. Federal long-term capital gains tax rates vary based on income: 0%, 15%, or 20%. Starting in 2026, the 20% rate will apply to single filers earning over $551,350 and married couples filing jointly earning over $613,700 [9]. On top of this, high earners face an additional 3.8% Net Investment Income Tax (NIIT) if their modified adjusted gross income (AGI) exceeds $200,000 (single) or $250,000 (joint), bringing the top federal rate to 23.8% [9].

State taxes can make the situation even more challenging. In California, for instance, state taxes can reach up to 13.3%, pushing the combined tax burden to over 30% or even 35% of the gain [11]. Depreciation recapture adds another layer of complexity - prior depreciation taken on real estate or business assets is taxed as ordinary income in the year of sale, regardless of whether a deferral strategy is used [9].

This is where Deferred Sales Trusts (DSTs) come into play, using the installment sale method to defer these taxes effectively.

DSTs work by turning the sale of an asset into an installment transaction. Here's how it works: the seller transfers their asset to an irrevocable trust before the sale closes. The trust then sells the asset and issues a promissory note to the seller.

Since the seller doesn't directly receive the sale proceeds, there's no "constructive receipt" to trigger immediate taxation [9]. Taxes are only recognized as the seller receives principal payments from the trust. The taxable portion of each payment is calculated using a gross profit ratio, which is the percentage of the sale price that represents the actual gain [11].

"Section 453 of the Internal Revenue Code embodies the congressional recognition of one simple concept: taxpayers...should be permitted to return gain from the sale of property for deferred payment obligations as those obligations are satisfied rather than when the obligations are received." - John L. Ruppert, DePaul Law Review [11]

One common approach is structuring the promissory note for interest-only payments. In this case, the trust pays the seller only the interest, leaving the principal - and the associated capital gains - untouched for as long as desired. This strategy enables long-term deferral [11].

With this deferred recognition in place, let’s look at what factors influence the size of the tax savings.

The tax savings from a DST depend on three main factors: the size of the deferred tax liability, the length of the deferral period, and the returns earned on the reinvested capital.

Unlike a direct sale, where only the net proceeds are reinvested, a DST allows the full gross proceeds to remain invested, which amplifies growth through compounding over time.

"The math is straightforward: a dollar saved in taxes today and invested for 10 years at a conservative 6% annual return becomes $1.79. That is the compounding power of tax deferral at work." - Dr. Jackie Meyer, CPA [9]

Another advantage is income smoothing. By spreading out the recognition of gains over multiple years, sellers may stay below the highest tax brackets, avoiding the steep rates that come with recognizing the entire gain in one year [9].

Take this example: In March 2026, a real estate investor named Dave sold a 128-unit apartment complex for $7.6 million. Without a DST, he faced a $1.1 million capital gains tax bill. By using a DST, Dave deferred the entire liability. Instead of sending $1.1 million to the IRS at closing, he kept that money invested, allowing it to generate additional income [12]. This approach doesn’t eliminate the tax but ensures the capital continues working for a longer period.

This foundation sets the stage for evaluating how these savings compare to the costs of implementing a DST in the next section.

DST Fees vs. Tax Savings: When Do the Numbers Add Up?

To decide if a Deferred Sales Trust (DST) is worth it, compare the immediate tax liability to the total fees and lost compounding over time. Start with three key numbers: your total immediate tax bill (federal, NIIT, and state), the present value of DST fees over the holding period, and the potential growth on the capital you keep invested rather than paying taxes upfront.

Here's a table that models a high-gain scenario to illustrate this:

| Metric | Immediate Sale (No DST) | Deferred Sales Trust |

|---|---|---|

| Sale Price / Gain | $10,000,000 / $7,000,000 | $10,000,000 / $7,000,000 |

| Estimated Tax Rate | 30% (combined) | 30% (deferred) |

| Immediate Tax Due | $2,100,000 | $0 |

| Initial Capital Invested | $7,900,000 | $10,000,000 |

| Est. Lifetime Fees (PV) | $0 | $400,000 |

| PV of Future Tax | $0 | $1,400,000 |

| Net Financial Benefit | Baseline outcome | +$300,000 + investment growth |

(Source: Data synthesized from AcquiTeam [10])

A DST doesn’t erase your tax bill but allows $2.1 million to stay invested instead of going to the IRS right away. Even after accounting for fees and the present value of future taxes, the numbers can favor deferral - particularly over longer timeframes. This framework helps identify cases where DSTs can provide a net financial edge.

DSTs often make sense when three factors align: a large capital gain, a high tax rate, and a long investment horizon.

Deferred tax liability grows significantly over time, but the minimum threshold for DSTs to make sense is $1 million in net proceeds and at least $1 million in capital gains [9]. Below this level, the setup costs can eat away at the potential benefits. But above this threshold, the math starts to work in your favor. As Dr. Jackie Meyer, CPA, explains:

"For a $2 million gain with a 20% federal rate plus 3.8% NIIT, the deferred tax liability is approximately $476,000. On a transaction of that size, setup fees in the range of $25,000 to $30,000 represent less than 6% of the deferred tax benefit." [9]

Now consider a $5 million capital gain taxed at a 30% combined rate. The deferred tax liability hits $1.5 million, making even $50,000 in setup fees look relatively small [10]. This advantage becomes even more pronounced in high-tax states like California, where state income tax can reach 13.3%. In such cases, a combined tax burden exceeding 33% means more capital remains in the trust to grow over time [3].

Time is a critical factor too. A DST held for more than 10 years allows the deferred tax to compound significantly. For example, at a conservative 6% annual return, $1 deferred today grows to $1.79 in 10 years [9]. This doesn’t even account for the drag caused by an immediate tax payment, which would reduce your investable base.

DSTs aren’t always the best choice. They can fall short when the fees outweigh the benefits, particularly in cases involving small gains, short time horizons, or lower tax rates. Here’s why:

For larger transactions, there’s an additional consideration: IRC § 453A. This rule imposes an interest charge on deferred tax liabilities when installment obligations exceed $5 million in a single tax year [14]. For high-value deals, this added cost must be factored into your break-even analysis.

When evaluating a Deferred Sales Trust (DST), it’s not just about the numbers. Beyond fees and tax benefits, there are several non-financial aspects that can significantly impact whether a DST aligns with your goals. These factors often shape how effective and practical this strategy is for your exit planning.

A DST operates under the framework of IRC §453 as an installment sale strategy, not as a formally recognized trust type. This distinction introduces legal risks, especially since the IRS has flagged certain installment sale arrangements for potential abuse. In fact, some have even made it onto the IRS's "Dirty Dozen" list of abusive tax schemes [2][6].

Timing plays a key role here. The DST must be set up, and the asset transferred, before the sale closes. Afterward, ongoing compliance requires collaboration between a tax attorney, trustee, and registered investment advisor, which adds to the complexity - and cost.

State-specific laws can also complicate matters. For instance, California doesn’t recognize installment sale treatment for DSTs. This means sellers in California might still face full state income tax liability, even if they use a DST [2].

One of the biggest trade-offs with a DST is the loss of direct control. Once the trust is funded, it becomes irrevocable. You no longer own the asset or the sale proceeds. Instead, you receive a promissory note entitling you to scheduled principal and interest payments [9].

While you can advise the trustee on investment decisions, the ultimate control lies with them. This means you won’t have the flexibility to access a lump sum or redirect funds on demand [6].

As Mallon FitzPatrick, CFP®, AEP®, CLU® of Robertson Stephens points out:

"While a credible tax planning tool, the DST lacks explicit IRS endorsements, which may concern some clients. This opacity... requires trust in the credibility of promoters." [6]

For individuals used to managing their own capital, this lack of liquidity and control can feel restrictive, especially if financial circumstances change unexpectedly.

The success of a DST largely depends on how well the trust’s investments perform. To meet the payment obligations outlined in the promissory note, the portfolio must generate returns that exceed recurring fees, which typically run around 1.5% of assets [8].

If the investments underperform, it could jeopardize the trust’s ability to make the required payments. Matthew Erskine of Erskine & Erskine highlights this risk:

"If investments perform poorly, the trust may not generate the anticipated yield, impacting the seller's income stream and the trust's ability to make the required installment payments." [5]

Unlike a traditional installment sale, where the risk is tied to the buyer’s creditworthiness, a DST shifts the risk to market performance. While diversification within the trust's portfolio can reduce some risks, any surplus growth stays in the trust, limiting your immediate access to funds [4].

To address these risks, sellers should work closely with the trust’s registered investment advisor. Completing a risk tolerance questionnaire can help ensure the portfolio is designed to cover both interest and principal payments. Regular reviews - typically two to four times a year - can further refine the strategy and adjust for market conditions [8].

Considering these non-financial factors alongside fees and tax implications provides a clearer picture of whether a DST is the right fit for your situation.

A Deferred Sales Trust (DST) can help defer taxes, but it’s not a one-size-fits-all solution. Whether a DST fits your situation depends on the financial calculations and how comfortable you are with the trade-offs outlined earlier.

Start by calculating your tax exposure. Combine federal capital gains tax rates (up to 20%), the 3.8% Net Investment Income Tax (NIIT), and any state taxes. In high-tax states, this can exceed 30%. For example, on a $2 million capital gain, your deferred tax liability could reach roughly $476,000. Compare this with setup fees, which typically range from $25,000 to $30,000 for a transaction of that size [9].

Next, model the long-term financial impact. Deferring taxes and investing those savings can lead to significant growth. For instance, a dollar saved today and invested at 6% annually would grow to $1.79 over 10 years [9]. This compounding effect is the main financial advantage of a DST. However, if your gains are less than $1 million, the setup fees and administrative complexity may outweigh the benefits.

You’ll also need to consider non-financial factors, like whether you’re comfortable giving up immediate liquidity and accepting the control and investment limitations that come with a DST. Timing is another critical factor - once you’ve constructively received the proceeds, the DST option is no longer available [9][1]. By carefully analyzing both the numbers and these broader trade-offs, you can ensure your decision aligns with your overall exit strategy and long-term goals.

Dr. Jackie Meyer, CPA of TaxPlanIQ, emphasizes the importance of proactive planning:

"The question of what happens to the tax liability when you sell a business should not come up at the closing table. It should be something an accountant raises two to five years before a client is even thinking about exiting." [9]

Once you’ve evaluated the potential benefits, the next step is incorporating a DST into your broader exit strategy. Ideally, this process should start two to five years before your planned exit. This allows time to model various outcomes, assemble a team (including a tax attorney, trustee, and investment advisor), and explore alternative strategies.

Partnering with an experienced financial advisor can make this process smoother. For example, Phoenix Strategy Group specializes in helping business owners model exit scenarios, test assumptions, and integrate tax deferral strategies like DSTs into a comprehensive plan. Starting early can turn a reactive exit into a carefully planned strategy that aligns with your long-term financial goals.

A Deferred Sales Trust (DST) can be a practical option when dealing with capital gains of more than $500,000. However, it's important to note that setting up and maintaining a DST comes with considerable expenses. The initial setup costs can range anywhere from $5,000 to $50,000, and there are ongoing annual fees for services like trustee management, accounting, and investment oversight. For this approach to be worthwhile, the deferred tax savings need to be reinvested wisely, generating returns that exceed these costs over time.

There’s no fixed timeline for breaking even with a Deferred Sales Trust. It ultimately hinges on whether the long-term benefits of tax deferral and compounded returns surpass the initial setup costs (typically 1.25%-1.5% of the transaction value) and ongoing annual fees (around 1.5%). For high-net-worth individuals with substantial capital gains, it's essential to model their unique situation to determine if the trust’s growth can outpace these expenses over time.

Yes, you might still owe state taxes. A Deferred Sales Trust (DST) allows you to defer federal capital gains taxes under IRC Section 453 by spreading the gains through installment payments. However, state tax laws differ, and using this structure doesn’t automatically mean you’ll defer state-level taxes. To get a clear picture of your tax responsibilities, it’s best to consult a qualified tax advisor who understands your state’s rules regarding installment sales and trust distributions.