Published on

March 21, 2026

When calculating Monthly Recurring Revenue (MRR), the key question is whether to include or exclude discounts. Here's the short answer: most SaaS companies exclude discounts to reflect the actual revenue received (Net MRR), while some include them to showcase potential revenue (Gross MRR).

Why does this matter? Reporting Net MRR offers a clearer picture of cash flow, aligns with financial standards like ASC 606, and builds trust with investors. However, using Gross MRR can highlight the full value of your subscription portfolio but risks inflating revenue figures.

Deciding how to handle discounts impacts forecasting, investor confidence, and churn analysis. For example, temporary discounts can lead to churn when they expire, making Net MRR more reliable for tracking real customer behavior.

Pro Tip: Normalize prepaid discounts (e.g., "pay for 10 months, get 12") across the subscription term to avoid revenue spikes. Tools like Phoenix Strategy Group’s platform can automate this process.

Monthly Recurring Revenue (MRR) represents the steady, predictable income a business expects to earn each month from active subscriptions [6][9]. Unlike revenue from one-time sales or fluctuating fees, MRR provides a reliable foundation for financial planning, especially for SaaS companies.

MRR helps businesses forecast cash flow, plan for growth, and manage budgets effectively [6][7][4]. Patrick Chen, Head of Marketing at Subskribe, highlights its importance:

"The beauty of subscription models is that revenue can compound over time... MRR is a critical tool in understanding how well your SaaS business is performing from month to month." [10]

For investors, consistent and growing MRR is a key metric for valuing a business and assessing its financial health during fundraising [4][10]. In fact, achieving a 10-20% MRR growth rate after hitting $1 million in ARR is often seen as a strong indicator for securing investment [6][10].

Understanding the elements that make up MRR is essential. Let’s break down the components that influence total MRR.

MRR is more than just a single figure - it’s a combination of different factors that reflect customer activity. It includes base subscription fees and recurring add-ons, but excludes variable fees unless they’re part of a predictable, capacity-based model [6][8][4].

Key factors affecting MRR include:

| MRR Component | Description | Impact on Total MRR |

|---|---|---|

| New MRR | Revenue from new customers acquired during the month | Increase |

| Expansion MRR | Additional revenue from upgrades or add-ons by existing customers | Increase |

| Reactivation MRR | Revenue from customers who resubscribe after churning | Increase |

| Contraction MRR | Revenue lost from downgrades or plan reductions | Decrease |

| Churn MRR | Revenue lost due to cancellations | Decrease |

To ensure accurate comparisons, all non-monthly contracts - such as annual or quarterly agreements - must be normalized into their monthly equivalent [7][3][9]. For example, if a customer pays $1,200 annually, divide that by 12 to calculate $100 MRR. This standardization keeps your MRR calculations consistent across all subscription types.

It’s critical to exclude one-time fees - like setup charges, onboarding costs, or professional services - since they aren’t recurring and don’t contribute to MRR [6][7][9]. Similarly, free trial users should only be included once they transition to paid subscriptions [7][8][4].

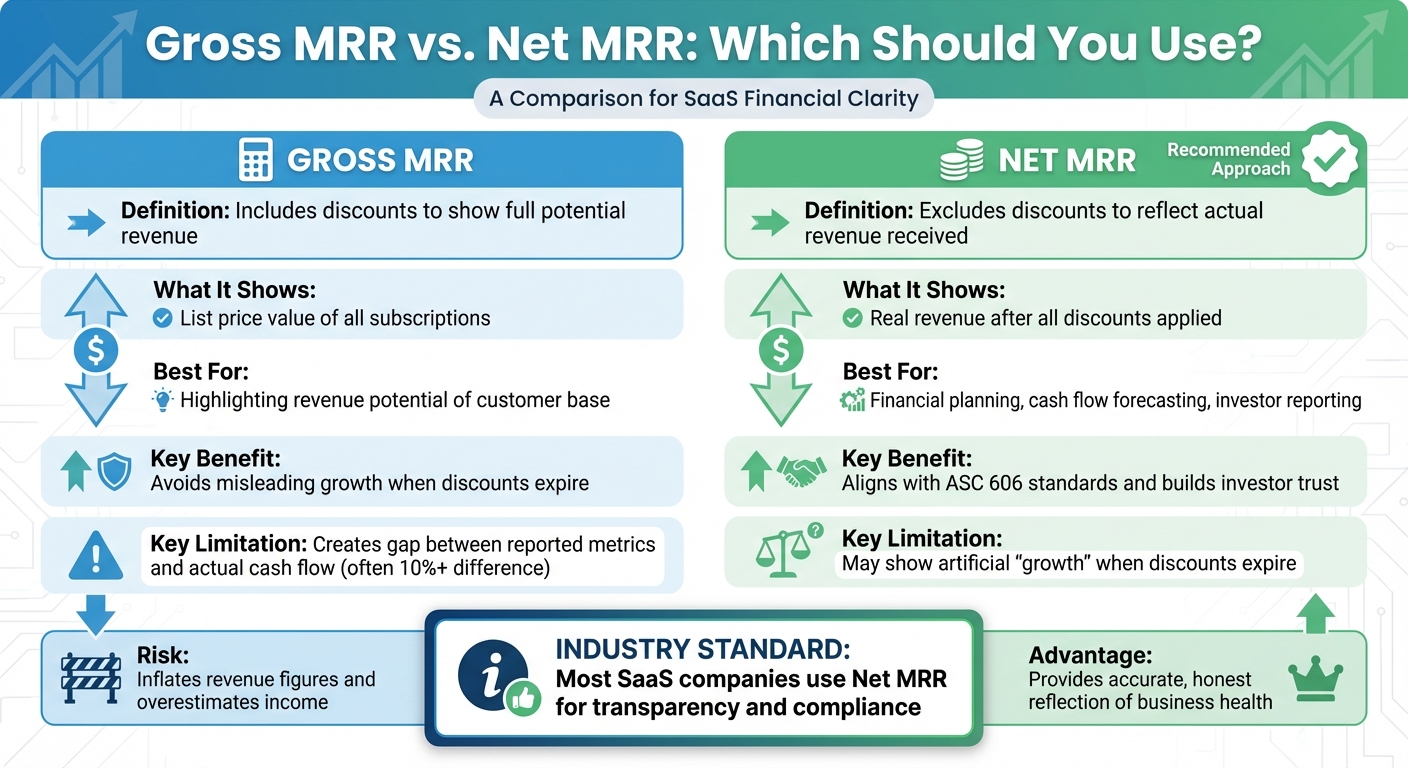

Gross MRR vs Net MRR: Key Differences for SaaS Companies

When it comes to managing Monthly Recurring Revenue (MRR), one of the trickiest decisions is how to handle discounts. Discounts are a common strategy in SaaS businesses, but they also create a challenge for finance teams. This choice has a direct impact on how revenue is reported to boards and investors.

There are two main ways to approach this: Gross MRR, which includes discounts to showcase the full potential revenue, and Net MRR, which excludes discounts to reflect actual cash received. Each method has its own implications for financial accuracy and decision-making. Let’s break down both approaches.

Some companies choose to report MRR on a gross basis because it highlights the full revenue potential of their customer base. This method shows what customers would pay if no discounts were applied, offering a snapshot of the subscription portfolio's theoretical value.

Another reason for using Gross MRR is that it avoids misleading revenue growth when discounts expire. For instance, in a net reporting model, the end of a temporary discount can look like revenue growth, even though it’s just the return to standard pricing - not an actual upsell.

The majority of SaaS companies lean toward excluding discounts from MRR. Net MRR provides a clearer picture of recurring revenue and aligns better with cash flow and standard financial reporting practices. Including discounts can create a mismatch between reported revenue and the cash actually received. In fact, companies transitioning from Gross to Net MRR often find a difference of 10% or more in their revenue figures[1].

There’s also the risk of churn when discounts expire. For example, if a customer faces a 25% price increase upon renewal, it could lead to dissatisfaction and higher churn rates.

Net MRR has become the go-to standard for most SaaS companies. Accurate handling of discounts is critical, and many subscription analytics platforms, such as ChartMogul, default to reporting MRR net of discounts. This ensures data integrity and aligns with accounting standards like ASC 606, which requires discounts to be factored into the transaction price and spread across the subscription term.

Finance teams are also leveraging catalog metadata to separate promotional ARR from contracted ARR. This approach ensures that board reports reflect the company’s true, sustainable revenue base[5].

Here’s a quick comparison of the two methods:

| Reporting Method | What It Shows | Best For | Key Limitation |

|---|---|---|---|

| Gross MRR | Full list price value of subscriptions | Highlighting potential revenue | Creates a gap between reported metrics and actual cash flow |

| Net MRR | Actual revenue after discounts | Financial planning, cash flow forecasting, investor reporting | May show artificial "growth" when discounts expire |

When it comes to managing MRR (Monthly Recurring Revenue), the type of discount you offer can significantly influence your reporting. In fact, discount types can skew revenue figures by as much as 10% or more, so understanding their impact is crucial[1].

Temporary discounts are short-term offers, such as "20% off for the first three months." These discounts should only affect Net MRR during the promotional period. Once the discount ends, the full subscription price is recorded as Expansion MRR.

On the other hand, permanent discounts apply for the entire duration of a subscription. For example, if a customer has a lifetime 20% discount, their MRR should always reflect the discounted rate. Reporting the full price would create an inaccurate picture of your revenue.

"Reporting Customer C at $500 MRR [when they have a lifetime discount] would be a misrepresentation. They have a lifetime discount and you're never expected to receive that much revenue from them." - Jordan van Everdingen, ChartMogul[1]

Consider this: two customers paying $80 per month - one with a temporary discount and one with a permanent discount - might generate the same cash flow today, but they require different reporting approaches. Keeping track of discount expiration dates ensures temporary adjustments don’t get mistaken for permanent reductions.

Prepaid discounts, like "pay for 10 months, get 12", offer upfront savings but require careful normalization. For example, this type of discount effectively reduces the cost by 16.7% over the subscription period[11]. While the cash is collected upfront, the service is delivered over time, which means MRR should reflect monthly revenue, not the lump sum.

To calculate this properly, you divide the total payment by the subscription period. If a customer pays $1,000 for a 12-month plan, the MRR would be $83.33 per month - not $1,000 in the first month and $0 thereafter. This normalization ensures compliance with ASC 606 standards[12] and prevents artificial revenue spikes or drops in your reporting.

Breaking down discount types highlights how they influence Gross and Net MRR:

| Discount Type | Gross MRR | Net MRR | Reporting Impact |

|---|---|---|---|

| Temporary (3 months at 20% off) | $100 | $80 | Gross inflates cash flow; Net reflects accurate revenue, with Expansion MRR added after the discount ends. |

| Permanent (20% off) | $100 | $80 | Gross overstates revenue potential; Net provides a realistic view of long-term revenue. |

| Prepaid (12 months for price of 10) | Spike in month 1 | $83.33/month (normalized) | Normalization smooths revenue and ensures compliance with ASC 606. |

With 78% of SaaS businesses offering some form of discounting[1], the gap between Gross and Net MRR can be significant. Companies that transition from Gross to Net reporting often find their actual recurring revenue is over 10% lower than previously thought - an adjustment that can impact investor confidence if not managed carefully.

Here are two scenarios that demonstrate how discounts influence Monthly Recurring Revenue (MRR) calculations. These examples use normalization formulas to ensure revenue reporting stays precise and compliant.

Imagine a quarterly subscription priced at $300 before any discounts. This plan includes a fixed discount of $6 per month and a 10% percentage discount.

The formula looks like this:

MRR = ((Quarterly Amount ÷ 3) − Fixed Discount) × (1 − Percentage Discount)

It's important to exclude any taxes from the quarterly amount before starting. For instance, if the total payment was $330 (including $30 in tax), subtract the tax to get a base of $300. When multiple discounts apply, always start with the fixed discount, followed by the percentage discount.

Now, let’s look at a scenario involving prepayment discounts and revenue normalization.

In this case, a customer prepays $1,000 for a 12-month subscription under a "pay for 10 months, get 12" deal. Normally, a full-price annual subscription would cost $1,200, meaning the customer saves $200 with this discount.

To normalize the revenue:

This approach aligns with ASC 606 guidelines, avoiding revenue spikes and ensuring consistency. For annual plans, applying a 1/12 ratio spreads the revenue evenly across the year. If a customer starts mid-month, use a proration factor to adjust for the partial service period while keeping the main calculation method intact.

"Reporting MRR net of discounts provides a more accurate and honest reflection of the health of your subscription business. By reporting on real, recurring revenue, you can make smarter decisions based on what customers are actually paying." – Jordan van Everdingen, ChartMogul

These examples highlight the importance of carefully applying discounts to ensure MRR reporting is both accurate and meaningful.

The way you account for discounts in your Monthly Recurring Revenue (MRR) calculations can shape the accuracy of your financial reporting. It's not just a technical detail - it directly influences forecasting, investor trust, and how well you understand churn risks.

When you calculate MRR net of discounts, you're presenting the actual revenue customers pay - not the hypothetical amount if they were charged full price. This distinction is critical for accurate forecasting. As SaaS investor David Skok puts it:

"MRR is the lifeblood of a subscription business. It allows founders to forecast growth, plan hiring, and ultimately communicate value to investors with confidence" [13].

While reporting net MRR might feel uncomfortable at first, it builds trust with investors who will uncover discrepancies during due diligence anyway. Companies that consistently report high-quality MRR growth - net of discounts - often achieve valuations 2-3x higher than those with inconsistent or inflated revenue numbers [13].

| Metric Component | Including Discounts (Gross) | Excluding Discounts (Net) |

|---|---|---|

| Forecasting | Overestimates cash flow; creates potential "revenue gaps" | Offers realistic, actionable revenue projections |

| Investor Trust | Risks discrepancies of 10% or more during due diligence | Builds trust through transparency and accuracy |

| Expansion MRR | Understates growth when discounts expire | Reflects true growth from existing customers |

By reporting net MRR, you not only enhance forecasting but also lay the groundwork for analyzing churn more effectively.

One overlooked risk is the "price shock" customers experience when their discount ends. For example, a customer facing a 25% price hike at renewal is statistically less likely to renew, even if the product's value remains unchanged [1]. This makes tracking churn by discount status a key priority.

Segmenting customer cohorts by discount status allows you to measure how discounted customers behave differently. If you're only reporting gross MRR, you might miss this entirely. When a discounted customer churns after their promotion ends, it can appear as standard churn in your reports. But if you've been tracking net MRR, the impact of the discount's expiration becomes clear, enabling you to craft retention strategies that address this issue [5].

Managing discounts effectively doesn't just improve forecasting - it drives smarter financial decisions overall. Aligning your discount management with ASC 606 standards and accurate cash flow reporting is essential for maintaining strong financial oversight in SaaS.

Phoenix Strategy Group offers tools that simplify this process. Their Monday Morning Metrics platform provides real-time insights into net MRR, automatically tracking discounts and separating promotional revenue from core contracted revenue. This ensures your board reports reflect actual revenue, preventing surprises during fundraising or M&A discussions.

The platform integrates with your billing system to capture critical discount details, such as expiration dates, enabling you to model scenarios like the financial impact of discount expirations on future quarters. By automating discount tracking, you reduce errors from manual spreadsheets and free up time to focus on strategic decisions backed by accurate data.

Even experienced finance teams can make mistakes when calculating Monthly Recurring Revenue (MRR), especially when discounts are involved. These errors can inflate your metrics, mislead investors, and throw off your forecasts. To ensure accurate financial reporting, it’s crucial to identify where things go wrong and take steps to correct them.

One common misstep is failing to subtract discounts when calculating revenue. MRR should reflect what customers are actually paying, not the full list price of a subscription [1].

Another frequent issue is double-counting. This can happen when upgrade revenue is added without removing the original subscription amount or when new and expansion revenue from the same contract are counted twice. This type of miscalculation can artificially boost growth metrics [14].

Errors in time-based recognition are another pitfall. For example, using the contract close date instead of the live start date can inflate metrics before services are even delivered. Ben Murray, Founder of The SaaS CFO, highlights the importance of accurate timing:

"ARR assumes continuity. Churn is analyzed separately... ARR reflects what exists today, not what management hopes will happen" [15].

Temporary discounts can also cause problems if their expiration metadata is missing. Without automated expiration rules, one-time discounts may unintentionally carry over into renewals, reducing long-term ARR [5]. Additionally, incorrect General Ledger (GL) mapping - such as posting discounts to Cost of Goods Sold (COGS) instead of contra-revenue accounts - can compromise audit accuracy [5].

To avoid these errors, precise and consistent calculation methods are essential. Start by normalizing all billing cycles to a monthly period. For example, divide annual contracts by 12 or quarterly contracts by 3 to standardize subscription terms [1].

Only include active and non-renewing subscriptions in your MRR total. Exclude accounts with "Future" or "In Trial" statuses, as well as nonrecurring fees like setup charges, one-time fees, and taxes [2].

Always recognize MRR based on live start dates rather than booked dates. This ensures revenue growth metrics are not inflated before services are delivered. For mid-month upgrades, remember to subtract the old MRR from the new total to avoid double-counting [14].

Accurate accounting practices also play a critical role. Ordway Labs advises:

"Discounts should post to contra-revenue accounts, never to COGS or expenses. Catalog coding ensures the right GL mapping, ensuring accurate financial reporting" [5].

Platforms like Phoenix Strategy Group's Monday Morning Metrics can help automate these processes. By normalizing billing cycles, applying discount expiration rules, and ensuring proper GL mapping, these tools centralize subscription data from CRM and billing systems into a single source of truth. This reduces manual errors and enhances the accuracy of board reporting.

Leaving discounts out of MRR calculations ensures you're working with the actual revenue customers pay, giving a clearer picture of your recurring income. This approach prevents inflated growth numbers and highlights potential churn risks when discounts expire. As Jordan van Everdingen, Director of Sales at ChartMogul, puts it:

"Reporting MRR net of discounts provides a more accurate and honest reflection of the health of your subscription business" [1].

With 78% of SaaS companies offering discounts, many discover discrepancies of over 10% in their MRR when they switch from gross to net reporting [1]. The data also shows that businesses with a Net Retention Rate above 100% see median growth of 49.5%, compared to just 9.2% for companies with an NRR between 60–80% [1].

Aligning your billing cycles, subtracting discounts, and using contra-revenue accounts not only adheres to ASC 606 standards but also ensures your financial reports are accurate and audit-ready. This kind of standardization improves metrics and strengthens long-term financial strategies.

Tools like Phoenix Strategy Group's Monday Morning Metrics platform simplify this process by automating discount tracking, applying expiration rules, and centralizing subscription data. This gives finance teams the insights they need to make informed decisions.

Gross MRR represents the total recurring revenue generated before factoring in any discounts, downgrades, or adjustments. It’s essentially the raw figure that shows how much revenue your subscriptions are bringing in.

On the other hand, Net MRR reflects the actual revenue after accounting for discounts, downgrades, or other deductions. This number provides a more realistic view of your business's earnings.

By excluding discounts from MRR calculations, you prevent inflating your revenue figures. This approach ensures a more accurate and transparent understanding of your financial performance.

When dealing with temporary discounts in Monthly Recurring Revenue (MRR), it’s essential to adjust for accuracy once the discount period ends. Simply put, exclude the discount amount after it expires.

For instance, if a customer was paying a reduced rate due to a promotion, update their MRR to reflect the full, standard rate once the discount concludes. This approach ensures your MRR reflects the actual, ongoing revenue you can reliably predict, rather than being skewed by short-term offers.

When dealing with prepaid deals, it's important to adjust them into Monthly Recurring Revenue (MRR) by allocating the total revenue evenly across the subscription period. Each month, a fraction of the prepaid amount transitions from deferred revenue to recognized revenue. This ensures that MRR accurately represents the revenue generated from the continuous delivery of services.