Published on

May 5, 2026

Personalization is transforming how financial companies retain customers. Here's why it matters:

Personalization works because it shifts from generic offers to tailored solutions based on real-time data, such as spending habits, life events, and preferences. This approach not only increases customer satisfaction but also builds trust and long-term loyalty. The key is using data intelligently, applying AI for real-time insights, and ensuring consistency across all channels.

By using AI, real-time data, and predictive analytics, financial companies can identify at-risk customers, deliver timely recommendations, and scale personalization effectively. This strategy is no longer optional - it's the key to staying competitive in the evolving financial landscape.

The ROI of Personalization in Financial Services: Key Statistics

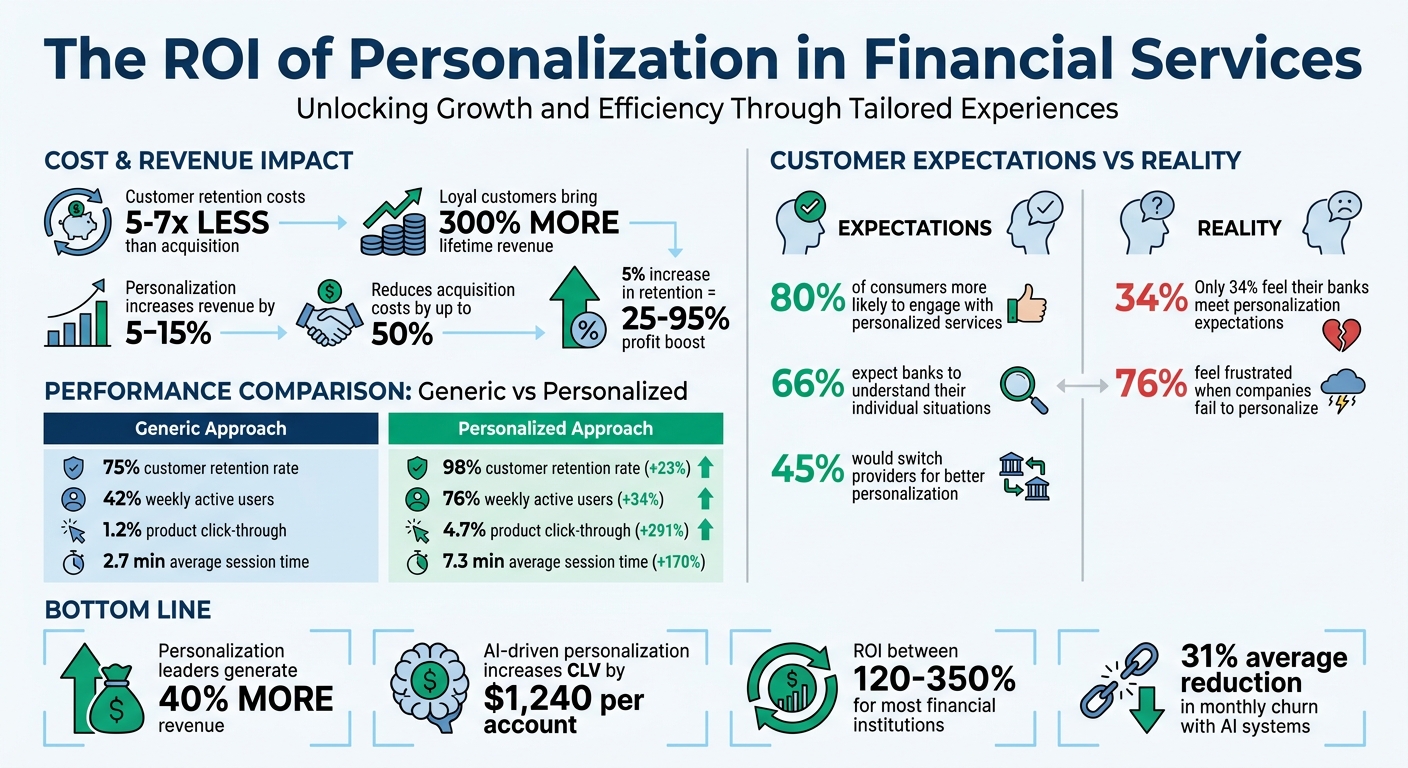

Growth-stage financial companies often face a tough battle with high churn rates, which directly impact profitability. The numbers paint a concerning picture: 25% of U.S. households are considering switching their primary financial institution, and 44% of consumers have already made a change recently [6][10]. For companies trying to grow, this constant turnover creates a financial drain that’s hard to manage.

The reasons behind this churn aren’t hard to pinpoint. Customers often leave because of impersonal interactions, subpar service, and one-size-fits-all products that don’t meet their specific needs [9][10]. While 66% of customers expect their bank to understand their individual financial situations, only 34% feel those expectations are being met [10]. This disconnect is even more pronounced among younger consumers who, accustomed to the tailored experiences of platforms like Netflix and Amazon, now demand similar personalization from their financial providers.

For growth-stage companies, the stakes are even higher. Operating with tight budgets, these businesses often pour significant resources into acquiring new customers just to maintain their existing base. The problem? Irrelevant offers not only waste 10% to 30% of marketing budgets but also erode customer trust by making people feel misunderstood [5][9]. Addressing these issues is essential to reducing churn and improving profitability.

The cost of customer churn is a harsh reality for growth-stage companies. The gap between acquisition costs and retention savings can make or break profitability. Personalization offers a clear solution: increasing customer retention by just 5% can boost profits by 25% to 95% [9]. Banks that excel in personalization retain 98% of their customers annually, while those that don’t see retention rates drop to 75% [10]. That 23-percentage-point difference translates directly into revenue, with personalization leaders generating 40% more revenue than their less-tailored competitors [10].

| Metric | Generic Approach | Personalized Approach | Impact |

|---|---|---|---|

| Customer Retention Rate | 75% | 98% | +23% |

| Weekly Active Users | 42% | 76% | +34% |

| Product Click-Through | 1.2% | 4.7% | +291% |

| Average Session Time | 2.7 minutes | 7.3 minutes | +170% |

Beyond retention, churn also affects marketing efficiency. For companies with limited resources, wasting funds on ineffective campaigns means missing opportunities to invest in critical areas like product innovation or hiring.

The financial implications make it clear: generic approaches don’t cut it in today’s competitive landscape.

Generic financial products fail because they don’t address the complexities of modern money management. On average, consumers hold 5 to 7 financial accounts across multiple institutions, creating fragmented data that prevents any single provider from gaining a full understanding of their needs [11]. As a result, personalization efforts often rely on basic demographic data - like age or location - offering little insight into what customers actually require in real time.

This disconnect becomes obvious in daily interactions. Imagine a customer who just applied for a mortgage but keeps getting irrelevant personal loan ads, or someone who consolidated their debt only to receive credit card offers they no longer need. These contextual mismatches show that the institution isn’t truly paying attention [11].

Modern customers expect their financial providers to anticipate their needs and offer relevant solutions, not generic promotions [11]. When banks fail to do so, customers are quick to leave. Over 40% of Americans now use non-traditional digital banking providers, and 65% of Millennials hold fintech accounts [6]. In an industry built on trust, failing to understand customer needs - or mishandling their data - can be especially damaging. Only 37% of consumers believe that brands responsibly secure and use their data [12]. This highlights the growing demand for tailored financial solutions as a way to build trust and improve retention.

Personalization turns basic customer interactions into meaningful relationships. By anticipating individual needs - whether it's saving for a home, planning for retirement, or managing debt - financial institutions can create a sense of partnership (often guided by a fractional CFO) rather than just a service relationship [14]. This approach helps build emotional connections, which is crucial in a world where customers often juggle multiple financial providers [1][14]. It also opens the door to better understanding customer behavior and using data to craft tailored experiences.

The stats are hard to ignore. 80% of consumers are more likely to choose a company that offers personalized experiences [5][7]. In financial services, 50% of customers specifically want institutions to use their preferences to shape their experience [2]. Personalization doesn't just enhance satisfaction - it can boost retention by up to 30% [4][15]. Companies that do it well not only retain customers but also see revenue growth of 5% to 15% while cutting acquisition costs by up to 50% [5][15].

This isn’t just theory; it works in practice. For instance, one financial institution implemented an AI-powered personalization system that improved millions of customer interactions, significantly increasing conversion rates [2].

Personalized experiences succeed because they align with how people make decisions. When customers feel understood, they're 78% more likely to return and recommend the business to others [12]. But effective personalization goes beyond demographics - it taps into psychographics, uncovering values, anxieties, and decision-making styles that drive behavior [7].

Take two 35-year-olds with similar incomes. One might be focused on retirement savings, while the other prioritizes legacy planning for their family. A one-size-fits-all approach misses the mark, but personalized messaging can address their unique goals [7]. This matters because 76% of consumers feel frustrated when companies fail to provide tailored experiences, and 45% would switch providers for better personalization [12].

Trust plays a huge role here. Financial decisions are deeply personal, and customers expect their bank or financial institution to understand their current needs - not just rely on outdated data. For example, recognizing a recent mortgage inquiry or a shift in savings behavior can make messaging feel relevant and timely [1].

"The financial partner with personalization that respects the customer's changing needs, goals, and privacy builds trust and enhances engagement" [1].

Consistency across all channels is just as important. Imagine receiving personalized recommendations through a mobile app, only to be treated generically by a human advisor. That disconnect erodes trust and undermines the effort behind personalization [14][7]. Ensuring seamless data flow between digital platforms and in-person interactions is key to maintaining credibility.

Understanding these psychological drivers sets the stage for using data analytics to refine and scale personalization.

Personalization thrives on smart use of data. By combining transactional data (like spending habits and payment patterns), behavioral data (such as feature usage and communication preferences), and digital interaction data (like search queries and navigation behavior), institutions can get a full picture of each customer’s financial situation [7].

The shift from static to dynamic profiling is a game-changer. Instead of relying on what a customer did years ago, modern systems use real-time signals to understand current intent. For example, if someone recently browsed mortgage rates, that’s far more relevant than knowing they opened a savings account three years ago [2]. This approach ensures that recommendations are timely and aligned with immediate needs.

Banks like Capital One are already leading the way. Their AI system analyzes over 100 million customer interactions, detecting life events like job changes or relocations. It then adjusts credit limits or suggests products accordingly, boosting customer engagement by 40% and reducing churn [15]. Similarly, DBS Bank uses an AI-driven engine to deliver 2 million personalized recommendations each month, such as advising customers on better investment opportunities. This effort led to a 33% increase in sales of investment products [15].

To make this work, financial institutions must integrate data across systems to create a Single Customer View [7]. Without it, conflicting messages from different platforms can frustrate customers and defeat the purpose of personalization.

"Loyalty will be based on how often a consumer relies on their financial institution's digital app for insight and advice" [14].

| Data Category | Specific Data Points | Purpose in Personalization |

|---|---|---|

| Transactional | Deposits, withdrawals, payment frequency | Identifies cash flow cycles and lifestyle habits |

| Behavioral | Feature usage, call center topics, login patterns | Highlights unmet needs and preferences |

| Digital | Click patterns, search queries, session duration | Reveals immediate customer intent |

| Psychographic | Risk tolerance, values, decision-making style | Shapes the tone and focus of advice |

The goal isn’t to gather endless amounts of data - it’s to use the right data to make interactions helpful, not invasive. 53% of consumers expect their financial provider to use their data for personalization, but the key is transparency and delivering real value [7]. When done right, this builds trust and lays the foundation for long-term loyalty.

Creating personalized financial experiences doesn’t have to break the bank. Growth-stage companies can achieve this by focusing on a methodical, scalable approach. The key lies in connecting different systems, spotting potential issues early, and delivering tailored recommendations at the right time.

Start by integrating data from core banking systems, CRMs, mobile apps, and advisor tools. Use real-time data pipelines with ETL processes and APIs to ensure a smooth flow of information between platforms. Building a Single Customer View is essential - this means consolidating customer profiles, standardizing data formats, and reconciling identifiers across all interaction points. For example, a customer starting an application on their phone should be able to seamlessly complete it at a branch.

AI and machine learning play a crucial role here, analyzing customer behavior and triggering personalized recommendations automatically. Adding psychographic intelligence allows you to craft messages that resonate with individual customer motivations and risk preferences. Many companies can deploy these foundational systems in as little as 3 to 6 months using cloud-based platforms, which also offer flexibility as your needs grow. Keep in mind that AI-powered customer retention systems typically cost between $80,000 and $400,000 annually, with an additional 20%–35% for integration and engineering costs [6][17].

"The gap between what customers expect and what banks deliver continues to widen. Your institution needs a systematic approach that unifies customer data, applies behavioral intelligence, and deploys AI-driven automation." - Psympl

Once your systems are unified, the next step is identifying customers who might be at risk of leaving.

Don’t wait for a customer to call and close their account - act early by monitoring for warning signs. Track behaviors like declining login activity, reduced transaction volumes, or unusual balance trends over 30-, 60-, and 90-day periods to spot potential issues before they escalate [6].

Assign churn risk scores to your customers and create automated response strategies tailored to their risk levels:

Predictive analytics can improve product adoption by 10%–15% [5] and can identify churn risks with over 85% accuracy [16]. To make these insights actionable, build dynamic customer profiles that reflect life changes, recent interactions, and evolving financial goals. For high-net-worth clients, automated alerts should prompt personal follow-ups to ensure these relationships receive the attention they deserve [6].

Once you’ve identified at-risk customers, the focus shifts to delivering timely and relevant recommendations.

Life events - like buying a home, having a child, changing jobs, or retiring - are prime opportunities to offer tailored financial products [6]. Use real-time behavioral data to guide these offers. For instance:

The first 90 days are especially critical. During this period, structured onboarding should include mobile app setup, direct deposit activation, personalized product suggestions, and satisfaction surveys. Customers who engage during this window are 58% less likely to churn within the first year [17]. Systems should also be configured for immediate responses - for example, if a customer checks mortgage rates online, follow up with relevant communication that same day instead of letting weeks pass [16]. Personalized, timely offers can generate up to three times the returns of generic campaigns [6].

"Personalization in banking is no longer about delivering more messages. It is about delivering the right information, at the right moment, in a way customers understand and trust." - The Financial Brand

While automation is key to scaling personalization, human oversight is equally important. Regular manual reviews ensure that recommendations remain empathetic and relevant, especially during times of economic uncertainty. Additionally, maintain consistency across all channels. If a recommendation is triggered on a mobile app, it should also be accessible to branch staff and call center agents to preserve customer trust and provide a seamless experience.

Tracking the right metrics is key to understanding how personalization impacts customer loyalty and revenue.

One of the clearest indicators of personalization success is the churn rate. Personalized services consistently outperform generic approaches in retaining customers, as shown by retention metrics [10]. Another essential metric is Customer Lifetime Value (CLV), which is crucial for long-term financial planning. AI-driven personalization can increase the average CLV by $1,240 per account [17]. Additionally, improving customer retention by just 5% can lead to profit increases ranging from 25% to 95% in the banking sector [10].

Engagement metrics tell a similar story. Personalized content can boost Click-Through Rates (CTR) on product recommendations by 20%–30%. Similarly, personalized emails often result in a 29% increase in open rates and a 41% jump in click-to-conversion rates [5]. For customer sentiment, tools like Net Promoter Score (NPS) and Customer Satisfaction (CSAT) provide valuable insights. Advanced personalization strategies can lead to a 20-point improvement in NPS [10]. Moreover, 72% of banking customers say personalized experiences are highly important to their loyalty [10]. These metrics highlight the long-term value of tailored financial recommendations.

Once personalization strategies are in place, measuring their impact with precision is critical. Real-time data plays a huge role in evaluating success. For instance, predictive churn scoring, which analyzes 40–80 behavioral signals like login frequency, transaction patterns, and support interactions, can generate real-time churn probability scores [17]. Machine learning models outperform traditional methods by being 43% more accurate and can predict revenue for 12-, 24-, and 36-month periods within the first 30 days of a customer’s lifecycle [17].

It’s also essential to compare performance against industry benchmarks. Personalization strategies have been shown to cut customer churn by 10%–31% [8][17], improve cross-selling rates by 20%–30% [8], and boost sales conversion rates by 10%–15% [13].

A compelling example comes from a digital lending fintech in 2026. With $38 million in revenue and 65,000 active borrowers, the company implemented a targeted AI engagement sequence during a 60-day activation window. This initiative reduced 90-day churn by 28% in under six months, preserving around $2.1 million in annualized revenue [17].

"We had been told for two years that we needed to invest in AI retention tools, but we had no idea which problem to solve first... We implemented a targeted AI engagement sequence... and reduced 90-day churn by 28% in under six months."

- Rachel Okonkwo, Chief Revenue Officer, $38M digital lending fintech [17]

Most financial institutions report a return on investment (ROI) between 120% and 350% from personalization efforts [10]. For mid-market fintechs with 20,000 or more accounts, the median payback period is typically 8–14 months [17]. To calculate preserved revenue, use this formula:

(Baseline Churn - New Churn) × Average Annual Revenue Per User.

For example, a mid-sized firm reducing churn by 10% can preserve $40 million in annual revenue [8]. These figures emphasize the value of real-time performance tracking and the financial benefits of personalization.

Scaling the benefits of personalized engagement requires advanced tools like automation and AI. Manually delivering tailored experiences to thousands - or even millions - of customers is simply not feasible. Automation and AI make this possible by analyzing massive data sets and triggering the right actions at precisely the right time.

AI systems can analyze 40–80 behavioral signals in real time, such as transaction frequency, login patterns, and customer sentiment during support interactions. This rapid analysis generates real-time churn probability scores, helping businesses predict and act on customer behavior almost instantly [17]. With this capability, financial institutions can decide which products or offers to present based on data from as far back as two years or as recent as two seconds ago [2].

The real advantage here is scale. Automation allows companies to deliver personalized content to millions of customers without driving up operational costs [18]. Specialized fintech engagement tools outperform generic marketing platforms because they are designed to interpret financial-specific signals, such as a drop in direct deposit activity or reduced savings rates [17]. These tools can improve churn prediction accuracy by 38 percentage points compared to general-purpose solutions [17].

One standout example involves combining first-party data with AI-driven campaigns to create tailored web experiences and coordinated outreach. This approach has successfully converted millions of potential customers into active users.

Taking automation one step further, real-time AI enhances customer engagement even more. AI agents, leveraging Large Language Models (LLMs) and Retrieval-Augmented Generation (RAG), act as personalized guides. These systems use complete customer profiles to deliver interactive, tailored experiences [2]. More importantly, they can identify signs of disengagement 18–45 days before a customer might drop off [17]. Acting early during this window is critical since save rates are 3.1 times higher compared to late-stage win-back efforts [17].

For example, First Horizon Bank uses AI algorithms to track individual behaviors and demographics. CMO Erin Pryor explained the impact:

"AI's ability to analyze internal data produces predictive insights, which marketing can use to understand our clients' needs better. This information allows us to personalize messages based on the client's preferences" [19].

This approach has led to more efficient ad spending and improved support during client interactions.

The results speak for themselves. Companies using AI-driven retention systems report an average 31% reduction in monthly churn within the first year [17]. Additionally, these systems can boost 90-day activation rates by 34% [17]. For mid-market fintech companies managing 20,000+ accounts, AI retention platforms typically cost $80,000–$400,000 annually, with an additional 20–35% for integration and engineering [17].

Personalization has become essential for growth-stage financial companies looking to stay competitive. Companies that excel in this area see 40% more revenue from personalized activities compared to their peers, while also cutting customer churn by 10–15% [8]. Retaining customers is far more cost-effective than acquiring new ones, giving these companies a financial edge and helping them move beyond simple transactions to become lifelong financial partners.

But the benefits of personalization go beyond just saving money. It helps financial institutions build trust and foster emotional loyalty - something that can't be easily disrupted by competitors offering better rates [6]. As we've discussed, personalized financial experiences not only help retain customers but also deepen engagement across multiple products. For growth-stage companies, this approach drives higher deposit rates, reduces delinquencies, and boosts overall customer interaction [3]. The result? A "halo effect" where each additional personalized product doesn't just add value - it amplifies the lifetime value of every customer relationship. As Sarah Lee, AI Analyst at Number Analytics, explains:

"The future of banking belongs to institutions that can transform data into meaningful, personalized experiences that address customers' unique financial needs" [8].

With unified data systems and AI-powered insights, the roadmap for personalization is clear. Companies that prioritize it now - using advanced analytics and automated engagement tools - will create a competitive advantage that's hard for generic providers to match. The tools are ready, and customers expect it. The real challenge is deciding how quickly you'll make personalization the centerpiece of your retention strategy.

To create meaningful personalization in financial services, start with first-party data. This includes details like account activity, product usage patterns, and transaction history. These data points provide a clear picture of customer behavior and preferences.

But don't stop there - dig deeper into psychographic data. This involves understanding factors such as customer motivations, risk tolerance levels, and how they prefer to communicate. These insights allow for a more complete understanding of your audience.

By integrating advanced tools like AI and predictive analytics, you can analyze these data sets effectively. The result? Tailored customer experiences that boost engagement, build loyalty, and improve retention. Plus, this approach can set your financial brand apart in an increasingly crowded market.

To make personalization feel natural rather than intrusive, use information that customers have freely provided. This could include their purchase history or preferred ways of being contacted. Be upfront about how their data is being used and ensure that your efforts to personalize align with what they actually need or want.

For example, offering tailored suggestions - like tips based on spending habits or specific life milestones - can make interactions feel more helpful rather than pushy. The key is to focus on consent, relevance, and open communication. By doing so, you can build trust while steering clear of crossing any boundaries.

When it comes to showing the value of personalization, two metrics stand out: customer retention rate (CRR) and repeat purchase rate. These metrics provide a clear picture of how well personalization efforts are fostering customer loyalty and encouraging repeat purchases. By tracking these figures, businesses can better understand how their strategies are influencing long-term customer relationships and driving growth.