Published on

May 18, 2026

ESG compliance is now a must-have for M&A deals. In 2026, regulations like the CSRD (Corporate Sustainability Reporting Directive), CSDDD (Corporate Sustainability Due Diligence Directive), and U.S. state-level climate laws are reshaping how mergers and acquisitions are structured, priced, and finalized. These frameworks demand stricter reporting, supply chain oversight, and data accuracy, making ESG a financial and regulatory priority.

For mid-market companies, ESG gaps can impact valuations and post-closing costs. Buyers now prioritize ESG due diligence to avoid risks like inaccurate emissions data or supply chain liabilities. Adopting global standards like ISSB (IFRS S1 & S2) and building audit-ready systems are critical steps to align with these evolving regulations.

Bottom Line: ESG is no longer optional in M&A. Addressing it early in the process can protect against financial penalties, ensure compliance, and enhance deal value.

Top ESG Regulatory Frameworks for M&A in 2026: CSRD vs CSDDD vs U.S. State Laws

CSRD, CSDDD, and new U.S. state-level climate laws are reshaping ESG compliance in mergers and acquisitions (M&A). These changes are making ESG factors a key financial consideration for deal teams.

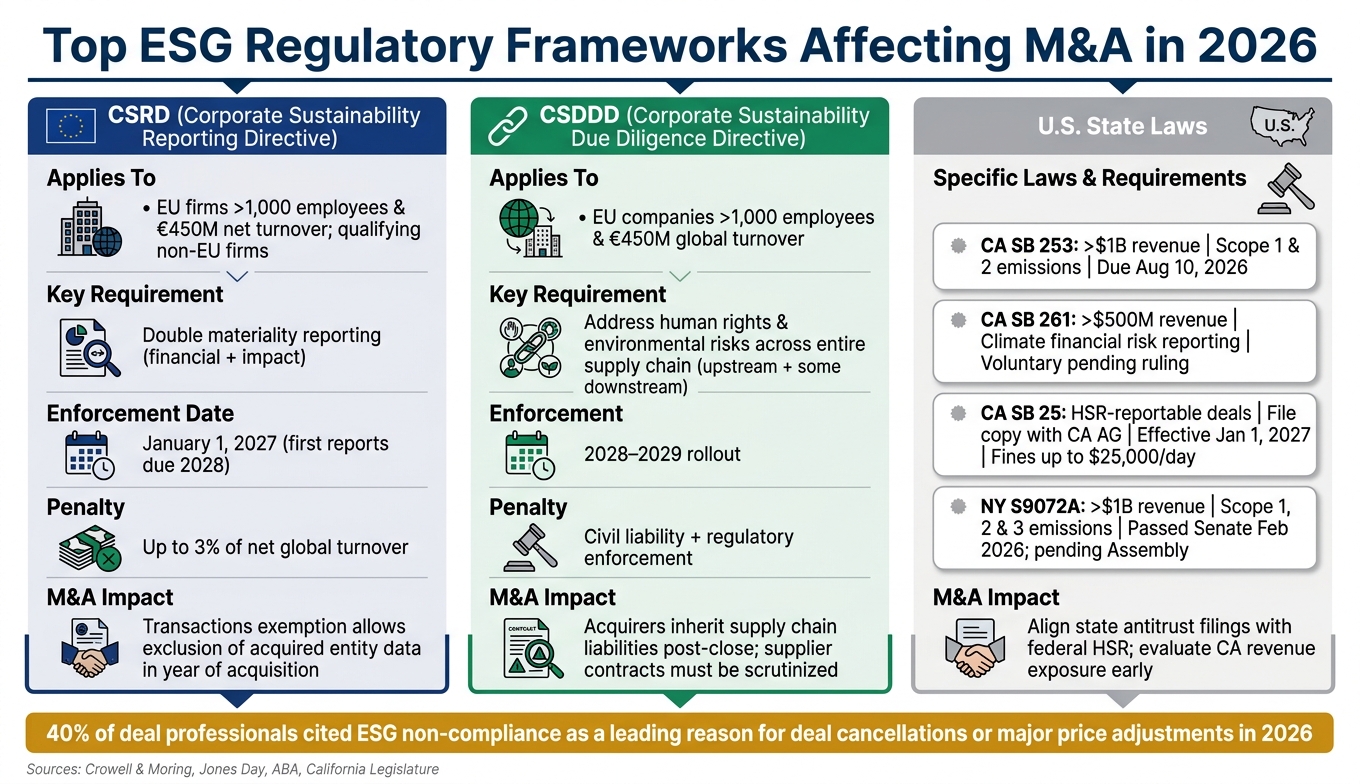

Starting in March 2026, the CSRD will apply to EU firms with over 1,000 employees and €450 million in net turnover. Non-EU firms meeting similar thresholds, based on EU revenue and subsidiary size, will also be subject to these rules. However, the Omnibus I Directive (Directive (EU) 2026/470) is set to significantly reduce the number of companies impacted, limiting the directive to only the largest firms.

"The Omnibus I Directive has finally been adopted and will enter into force on 19 March 2026. The text substantially raises the thresholds applicable to the Corporate Sustainability Reporting Directive (CSRD)... limiting their application to the largest companies only." - Crowell & Moring LLP[8]

One notable update is the transactions exemption. If a company acquires a new entity mid-year, it can exclude that entity's data from its sustainability report for that year. This change has major implications for how M&A teams assess a target's ESG preparedness. Reporting under the CSRD begins on January 1, 2027, with the first reports due in 2028. Non-compliance could result in penalties of up to 3% of net global turnover[8].

The CSRD also introduces the concept of double materiality, requiring companies to disclose not only the financial risks posed by ESG issues but also the impact of their operations on society and the environment. This dual focus adds another dimension to ESG assessments during M&A.

The CSDDD takes ESG compliance beyond reporting by requiring companies to actively address human rights and environmental risks across their entire supply chain. This includes the company’s own operations, upstream suppliers, and some downstream partners like distributors[4]. For acquirers, this means potential liability for supply chain violations post-acquisition.

"The CSDDD has regulatory enforcement requirements and civil liability for violations." - Debra Gatison Hatter, Partner, American Bar Association[5]

The directive applies to EU companies with more than 1,000 employees and €450 million in global turnover. Enforcement will roll out between 2028 and 2029[4]. Even if a target company isn’t directly subject to the CSDDD, it may still face compliance pressures through contractual obligations with CSDDD-covered partners. This makes it essential for deal teams to scrutinize supplier contracts for ESG-related clauses during due diligence. By focusing on supply chain risks, the CSDDD has added complexity to the M&A process.

In the U.S., California is leading the charge with SB 253, which requires companies with over $1 billion in annual revenue doing business in the state to report Scope 1 and 2 emissions by August 10, 2026. Scope 3 reporting will follow in 2027[9][10]. The threshold for California-based sales is set at approximately $757,000, meaning even companies headquartered elsewhere may fall under this law[10].

California’s SB 25, effective January 1, 2027, adds another layer of complexity. It requires companies involved in HSR-reportable transactions to file their federal notification with the California Attorney General if state-specific thresholds are met. Non-compliance could lead to fines of up to $25,000 per day[11][12]. Other states, like Colorado and Washington, have enacted similar laws, and New York’s version (NY S9072A) is currently awaiting final approval[10][12].

| Law | Revenue Threshold | Key Requirement | Status (May 2026) |

|---|---|---|---|

| CA SB 253 | > $1 Billion | Annual Scope 1 & 2 emissions reporting | Enforceable; first report due Aug 10, 2026 |

| CA SB 261 | > $500 Million | Biennial climate financial risk reporting | Voluntary; pending Ninth Circuit ruling |

| CA SB 25 | HSR-reportable | Copy of HSR filing to CA Attorney General | Effective January 1, 2027 |

| NY S9072A | > $1 Billion | Annual Scope 1, 2, & 3 emissions reporting | Passed Senate Feb 2026; pending Assembly |

For mid-market M&A teams, these laws emphasize the need to align state antitrust filings with federal HSR submissions and evaluate California revenue exposure early in the process. These regulatory developments are already shaping the way due diligence is conducted, as we’ll explore further in the next section.

With the mandates set by CSRD and CSDDD, ESG due diligence has shifted from being a "nice-to-have" to a regulatory must. Ignoring it during mergers and acquisitions (M&A) can lead to significant headaches after the deal closes.

"Acquirers who skip sustainability diligence risk expensive post-close surprises: inherited emissions data gaps, weak controls over sustainability metrics, missing contractual rights to collect supplier data, and unexpected reporting obligations." - Aidan Lawes and Olga Gidalevitz Ph.D., Jones Day [7]

A thorough ESG review focuses on three core areas: environmental, social, and governance. Here's a breakdown of the key data points to scrutinize and the sources to verify them:

| ESG Pillar | Key Data Points | Verification Sources |

|---|---|---|

| Environmental | Scope 1, 2, and 3 emissions; energy intensity; physical climate risk | Utility bills, logistics contracts, facility reports [2] |

| Social | Wage parity; supply chain integrity; health and safety (ISO 45001) | HR records, supplier audits, litigation logs [2] |

| Governance | Board independence; anti-corruption policies; data privacy (GDPR) | Board minutes, policy history, training logs [2] |

One essential framework to apply across all three pillars is double materiality. This concept evaluates not only how ESG factors influence a company’s financial performance (financial materiality) but also how the company’s operations impact the environment and society (impact materiality) [6]. This dual approach aligns with the ESRS framework under CSRD and should guide every due diligence process.

Beyond ticking boxes on a checklist, deal teams must also confirm the accuracy of past ESG claims and commitments.

Overlooking historical ESG risks can be costly. A target company might have made public sustainability promises - perhaps in investor presentations or marketing materials - that have yet to be fulfilled. These unkept commitments can lead to unexpected costs or tarnish the buyer's reputation [7].

To avoid these pitfalls, source traceability is key. Every ESG claim in the data room should be backed by precise documentation, including the exact document, page, and paragraph [6][14]. For instance, if a company claims a 30% reduction in Scope 2 emissions, verify this against actual utility bills rather than relying on summary reports. Additionally, check whether the target uses standardized methodologies like the GHG Protocol for emissions calculations or if it relies on rough estimates that might not withstand regulatory scrutiny [7].

"ESG issues are gaining prominence in M&A deals and deals can fall through if ESG issues crop up." - Adrian Tüscher, Partner, Head KPMG Law Switzerland [13]

The numbers speak for themselves: 40% of deal professionals cited ESG non-compliance as a leading reason for deal cancellations or major price adjustments in 2026 [14]. For mid-market buyers, this statistic is a clear warning to address ESG considerations before signing a letter of intent.

Once due diligence uncovers ESG risks, the findings must shape the deal terms. It’s not enough to leave these insights buried in the due diligence report - they need to influence the Share Purchase Agreement (SPA). This means including specific warranties, representations, and indemnification clauses to address identified sustainability risks [13].

For example, closing conditions can require the target to resolve issues like missing emissions or supplier data before the deal is finalized. Similarly, Transition Service Agreements (TSAs) should mandate clear ESG data-sharing protocols to minimize liabilities after the deal closes. By embedding ESG risks into quantifiable deal terms, buyers can better protect themselves from unexpected challenges.

Mandatory ESG due diligence is just the starting point. To ensure smooth cross-border transactions, companies need a standardized approach to ESG reporting. This is especially critical when integrating ESG risks into deal terms, as both parties must be on the same page. Enter the International Sustainability Standards Board (ISSB), which provides a universal framework for ESG reporting.

The ISSB has introduced two key standards: IFRS S1 (general sustainability disclosures) and IFRS S2 (climate-related disclosures). As of June 2025, 36 jurisdictions had adopted or were finalizing these standards, and today, 40 jurisdictions - representing nearly 60% of global GDP - require alignment with ISSB guidelines [15].

For mid-market deal teams, this shift is significant. The ISSB framework consolidates earlier standards like TCFD, SASB, and GRI into a single, streamlined system [1]. Instead of juggling multiple frameworks, companies can now establish one ISSB-compliant data platform that satisfies the demands of most major markets.

"The ISSB intends the standards to serve as a global baseline, helping companies navigate the global reporting landscape." - Latham & Watkins [15]

Adopting ISSB standards isn't just a good idea - it’s becoming essential. For instance, California’s Climate-Related Financial Risk Act (SB 261) recognizes ISSB-aligned reporting as compliant [15]. Similarly, in the UK, the upcoming Sustainability Reporting Standards (UK SRS), based on IFRS S1 and S2, will be available for voluntary use by 2026, with mandatory adoption for listed companies under review by the FCA [3]. For mid-market companies pursuing cross-border deals, ISSB compliance is quickly shifting from a recommendation to a requirement.

ESG ratings are increasingly shaping how buyers assess a target’s risk profile and determine whether a valuation premium is warranted. A company with well-organized ESG data signals to potential acquirers that it’s ready for integration, reducing the likelihood of post-close surprises. Strong ESG data is also becoming a key driver in acquisition decisions, as buyers prioritize targets with measurable sustainability performance and governance structures.

However, ESG ratings aren’t foolproof. A lack of consistency across rating agencies creates challenges for deal teams.

"ESG metrics and ratings agencies continue to play a critical role in evaluating performance, but the lack of standardisation among the ratings agencies presents ongoing challenges." - Global Legal Insights [4]

A high rating from one agency doesn’t guarantee the full picture. Buyers should cross-check ratings with primary sources, such as facility management reports, utility bills, HR records, and supplier audits, rather than relying solely on the rating itself [6]. Overlooking ESG weaknesses can lead to unexpected remediation costs and additional reporting obligations after the deal closes [16]. This is why ESG findings are increasingly factored into Quality of Earnings (QoE) analyses and adjustments to purchase prices.

Here’s a closer look at where ESG ratings might fall short and how to verify the data:

| ESG Area | What Ratings May Miss | Primary Data to Verify |

|---|---|---|

| Emissions | Methodology inconsistencies or estimates | Utility bills, logistics contracts |

| Supply Chain | Risks beyond Tier 1 suppliers | Supplier audits, procurement contracts |

| Governance | Policies created just before due diligence | Board minutes, policy version history |

ESG ratings can be a helpful starting point, but they shouldn’t be the final word. Verifying data ensures ratings are reliable and equips deal teams with the insights needed to negotiate effectively. This extra layer of diligence strengthens the foundation for ESG considerations in M&A.

Creating audit-ready ESG data systems is crucial for meeting compliance standards. These systems should have clear documentation and traceability, similar to SOX-style internal controls [1][7]. Each ESG metric must be backed by verifiable source documents, like utility bills or HR records, ensuring your data room can withstand regulatory reviews [6].

"Disclosures based on ad hoc processes, manual spreadsheets, or unverified assumptions may fail under regulatory scrutiny, assurance, or litigation." - Jones Day [7]

Leveraging AI-powered analysis platforms can drastically cut mid-market due diligence timelines, reducing the process from three weeks to just five days [6]. For deal teams working under tight deadlines, this time-saving advantage is invaluable.

By establishing these robust data systems, you're setting the stage for stronger governance - a critical component in managing ESG risks effectively.

While solid data systems are essential, they need to be paired with strong governance practices to ensure their effective application. Before closing a deal, assess whether the target company has a well-functioning ESG committee at the board level, independent board members, and an ethics framework that includes whistleblower protections and anti-bribery training [6][2].

It's also vital to check whether the company uses standardized methodologies for tracking Scope 1, 2, and 3 emissions data. Weak controls in these areas can lead to costly post-close remediation [7].

The table below highlights the key governance areas to focus on during due diligence:

| Governance Focus Area | Key Oversight Practices | Red Flags for Deal Teams |

|---|---|---|

| Board Structure | Evaluate independence, diversity, and the presence of an ESG committee | Lack of ESG expertise at the board level |

| Ethics & Conduct | Examine whistleblower policies and anti-bribery training | History of regulatory issues or weak internal controls |

| Supply Chain | Audit Tier 1 and Tier 2 suppliers for risks related to human rights and environmental impact | Missing risk clauses for suppliers in high-risk jurisdictions |

| Data Privacy | Confirm compliance with GDPR and ISO 27001 standards | Past data breaches or lack of cybersecurity measures |

After completing due diligence, turn your findings into a 100-day action plan. This plan should address gaps in data collection, governance structures, and reporting obligations to prevent future liabilities [6].

Managing ESG compliance while navigating M&A transactions can be challenging for mid-market teams. Phoenix Strategy Group specializes in helping growth-stage and mid-market companies tackle these challenges head-on.

Their services include fractional CFO support, data engineering, FP&A systems, and M&A advisory, providing a one-stop solution for financial modeling and operational groundwork. Whether you're preparing for an acquisition, conducting due diligence, or integrating a newly acquired company, Phoenix Strategy Group ensures that your systems meet regulatory standards and withstand scrutiny.

ESG compliance in mergers and acquisitions has moved from being optional to absolutely essential. By 2026, frameworks like the CSRD and SFDR will be fully enforced, with non-compliance carrying tangible financial penalties. As discussed earlier, while thorough due diligence and structured ESG frameworks are vital, the final integration phase can make or break the process.

"For a target company, non-compliance is no longer just a reputational risk; it is a financial liability that can lead to significant fines and restricted access to capital markets." [2]

For mid-market deal teams, the message is clear: start early and stay thorough. This means cross-checking supply chains against CSDDD requirements, validating public ESG claims with internal data like utility bills or HR records, and assigning a financial value to risks - whether as a price adjustment, remediation cost, or post-close CapEx.

The regulatory environment remains complex, particularly in the U.S., where state-level mandates in places like California and Illinois diverge sharply from federal rollbacks. This fragmented landscape highlights the need for global standardization. Leveraging ISSB standards as a baseline for reporting offers a consistent benchmark, especially as 36 jurisdictions worldwide had adopted or were finalizing ISSB adoption by June 2025 [4].

A strong ESG framework isn't just about avoiding risks - it can actively enhance value. Companies with solid ESG practices often enjoy lower capital costs, higher exit multiples, and better access to green financing. The groundwork you lay now in areas like data systems, governance, and reporting directly impacts your company's valuation during negotiations.

Phoenix Strategy Group specializes in helping mid-market companies build the financial and advisory infrastructure needed to meet these evolving standards. From data engineering to M&A advisory, starting with the right systems ensures you maximize deal value, whether you're selling or acquiring.

The Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD) are not directly applicable to U.S. companies engaged in mergers and acquisitions (M&A). These regulations are tailored for businesses operating within the European Union, emphasizing sustainability and due diligence obligations specific to that region.

The most frequent ESG red flags that can affect deal prices or even lead to closures include greenwashing, failure to comply with strict sustainability reporting laws, unresolved risks within the supply chain, and criminal liabilities linked to ESG violations. With regulators ramping up their focus on these issues in 2026, addressing them thoroughly during M&A due diligence is more important than ever.

To prepare swiftly for an emissions and supplier data audit, it's crucial to establish a strong data collection and verification system that aligns with ESG standards such as CSRD and ESRS. Start by reviewing key documents like supplier contracts, energy bills, and HR records to confirm the accuracy of sustainability claims. Make sure all ESG data is traceable and well-organized. Focus on meeting double materiality assessment requirements and ensure you're ready for third-party assurance by verifying that emissions and supply chain data are both accurate and thoroughly documented.