Published on

May 2, 2026

FinTech valuations directly shape your exit strategy. Whether you're planning for an acquisition or IPO, understanding the factors that drive valuation - like revenue multiples, growth rates, and buyer preferences - can mean the difference between a lowball offer and a premium deal. For example, Payments companies average 7.7x revenue multiples, while Lending platforms typically trade at 2.6x. Metrics like the Rule of 40 (growth rate + EBITDA margin) and Net Revenue Retention (NRR) are crucial benchmarks that buyers use to assess your company's worth.

Key insights include:

To maximize your valuation:

Timing also matters - prepare 12–24 months ahead to align your exit with favorable market conditions. Buyers now value efficient growth and operational resilience over pure expansion. With proper preparation, you can secure a lucrative exit.

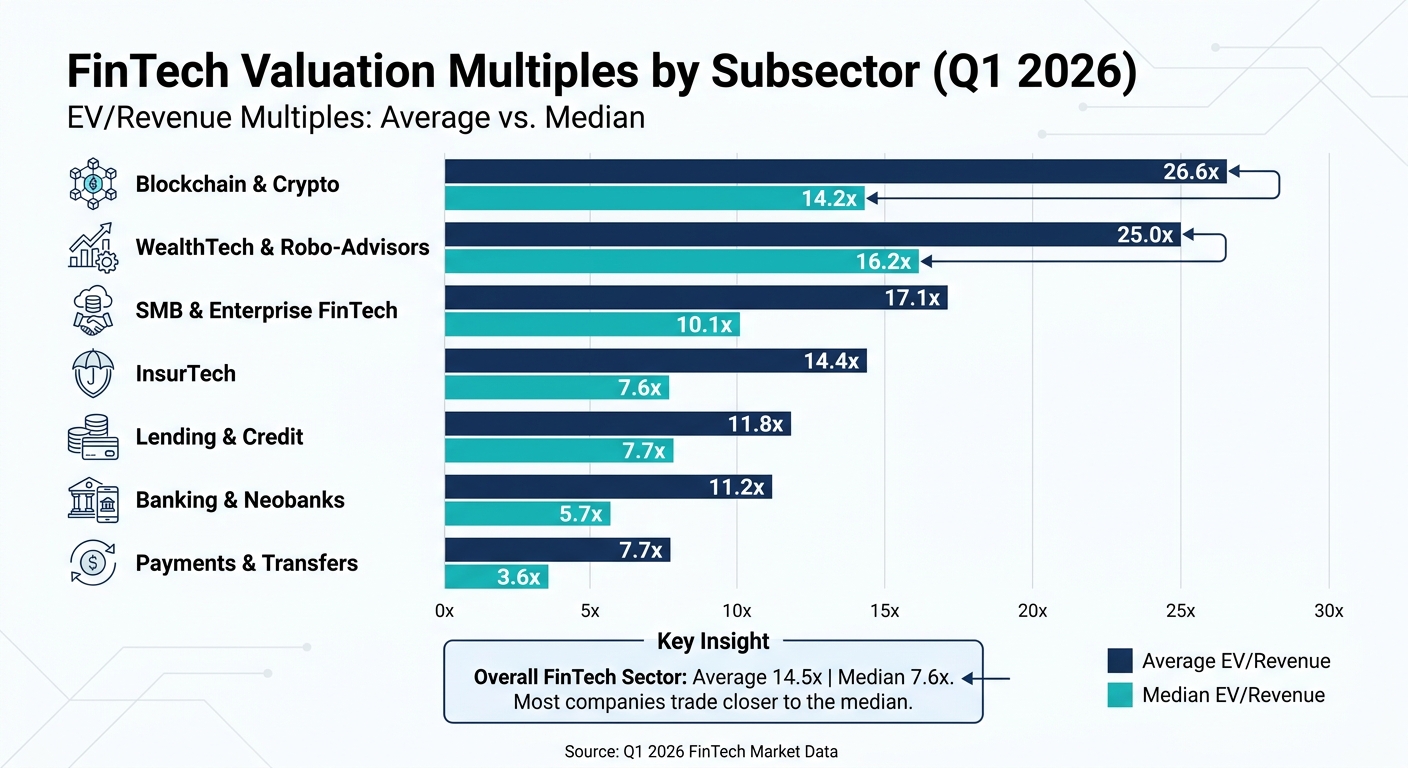

FinTech Valuation Multiples by Subsector Q1 2026

Valuations in the FinTech world hinge on key financial and operational metrics, which ultimately shape exit value. Knowing which metrics are most impactful in your specific FinTech niche allows you to focus on what will maximize your company’s worth.

The Rule of 40 is a critical benchmark for premium valuations. It’s calculated by adding your revenue growth rate to your EBITDA margin. If the result is 40 or higher, you’re in elite territory. Companies hitting this mark often trade at 7.3x revenue or higher, with premiums ranging from 50% to 100% above the median [2]. This metric reflects a balance between profitability and growth - an attribute buyers now prioritize. However, only 10–15% of FinTech companies currently achieve this threshold [1][2].

For SaaS-based FinTechs, Net Revenue Retention (NRR) is another vital metric. An NRR above 120% shows that your existing customers are spending more over time, which is highly attractive to buyers. Additionally, an LTV/CAC ratio (lifetime value to customer acquisition cost) of 5:1 is considered ideal. On the flip side, churn rates for SaaS FinTechs were averaging about 3.5% monthly as of early 2026 [2].

Revenue quality also plays a big role. Buyers differentiate between "Compounding Revenue", seen in software-driven models like WealthTech, and "Processing Revenue", tied to transaction volume, such as in payments. For instance, WealthTech companies averaged 25.0x EV/Revenue in Q1 2026, while payments companies averaged a much lower 7.7x [5].

The market has shifted its focus from pure growth to efficient growth, emphasizing profitability alongside expansion. This means many FinTechs, once valued solely on revenue, are now being judged on EBITDA, as buyers demand proof of cash generation [2].

Scalability is a key driver of higher valuation multiples. On average, FinTechs command 4.5x EV/Revenue, significantly higher than the 1.8x seen for traditional banks. This advantage comes from the technological leverage FinTechs possess, which legacy systems can’t replicate [2]. Capital-light models, such as SaaS platforms and API-driven services, often secure multiples 2–3x higher than capital-intensive businesses like balance-sheet lenders [1].

Regulatory compliance is another crucial factor. Banking licenses, money transmitter licenses, and insurance charters serve as structural barriers to entry, enhancing a company’s appeal to buyers [1][2]. Compliance with frameworks like the EU’s Digital Operational Resilience Act (DORA) and Markets in Crypto-Assets (MiCA) can also reduce risks during due diligence. However, smaller firms often face valuation discounts of 50–70% due to the high costs of achieving compliance [2].

Founder dependency can also drag down valuation. Companies where the founder is the primary technical or compliance resource often face discounts of 15–30% [2]. Building a management team or leveraging fractional CFO services to operate independently is key to maximizing exit value.

Integration of AI is becoming a must-have for top-tier valuations. Companies with proprietary data assets - such as unique credit datasets or fraud detection models - stand out because these assets make their AI capabilities defensible [1]. Proper data collection, processing, and ethical protection are increasingly viewed as differentiators for predictive analytics, fraud prevention, and dynamic pricing [7].

When combined with financial metrics, these non-financial factors significantly shape how FinTech valuations are determined.

Beyond financial and operational drivers, market-specific dynamics play a major role in valuations. The FinTech vertical you operate in can dramatically impact your valuation range. For example, in Q1 2026, the average EV/Revenue across the FinTech sector was 14.5x, but the median was only 7.6x. This discrepancy highlights how a few high-performing outliers skew the averages [5].

"The average is not the market. The overall average EV/Revenue is 14.5x but the median is 7.6x. Most fintech companies trade closer to the median."

- Lior Ronen, Founder of Finro Financial Consulting [5]

| FinTech Subsector | Avg. EV/Revenue (Q1 2026) | Median EV/Revenue (Q1 2026) |

|---|---|---|

| Blockchain & Crypto | 26.6x | 14.2x |

| WealthTech & Robo-Advisors | 25.0x | 16.2x |

| SMB & Enterprise FinTech | 17.1x | 10.1x |

| InsurTech | 14.4x | 7.6x |

| Banking & Neobanks | 11.2x | 5.7x |

| Lending & Credit | 11.8x | 7.7x |

| Payments & Transfers | 7.7x | 3.6x |

The table above illustrates the wide variation in valuation multiples across subsectors. Blockchain and WealthTech companies command the highest multiples, while payments platforms trade at much lower valuations, even when generating higher revenues.

A notable gap exists between private round valuations (averaging 16.4x) and public market valuations (averaging 5.9x), creating potential exit challenges for late-stage founders [5]. North American FinTech companies also tend to command higher multiples, averaging 6.4x compared to the global average of 4.4x [1]. Strategic acquirers often pay 15–30% premiums over private equity firms due to their ability to leverage revenue synergies and market access [1].

Finally, embedded finance - offering financial products through non-financial platforms like e-commerce sites - commands higher valuations thanks to reduced customer acquisition costs [1]. The global FinTech market is on track to hit $460.76 billion by 2026 [2], with venture capital funding reaching $51.8 billion in 2025, a 27% year-over-year increase [6].

FinTech exit multiples have seen a noticeable decline, dropping from 7.7x in 2021 to a range of 3.7x–7.4x by 2025–2026 [2]. This shift highlights a change in buyer focus, moving away from "growth at all costs" to prioritizing operational resilience and sustainable business models [9].

A close eye on your subsector's performance is essential. For instance, blockchain infrastructure companies boast 17.3x revenue multiples, while lending platforms lag far behind at 2.6x [2]. This underscores the importance of not only tracking broader market trends but also understanding how your specific niche is valued. Strategic acquisitions made up 78% of FinTech exits in 2025, further emphasizing the role of targeted market dynamics [8].

Regulatory milestones can also create opportunities for exits. Competitor acquisitions and discussions at the board level often signal a heating market [10].

Macroeconomic trends play a significant role as well. For example, central bank interest rate cuts can improve the valuation landscape for financial services companies [11]. Even in a selective market, private equity firms had amassed over $3.6 trillion in dry powder by 2025, with a strong preference for mature FinTechs showing stable cash flows [2]. Additionally, the IPO market made a comeback in 2025, with notable exits from Klarna, Chime, and Circle signaling renewed public market interest [2].

These factors collectively highlight the importance of syncing your company's readiness with favorable market conditions to optimize your exit timing.

To achieve a successful exit, you need to align your company’s internal readiness with the external market environment. With the broader market conditions in mind, preparing your business 12–24 months ahead is critical to ensure your financial performance and brand narrative are in sync with market opportunities [8].

Start by maintaining flawless financial records. Use accrual accounting - standard for FinTechs valued above $1M [2]. Clearly separate recurring revenue from one-time fees, and ensure your cap table is up-to-date and accurate. Keeping clean books and thorough documentation allows you to act quickly when market opportunities arise [3][10].

Another key factor is reducing reliance on founders. Companies overly dependent on their founders face 15–30% valuation discounts [2]. Build a strong management team or hire a fractional CFO to ensure your business can operate independently. Audit your intellectual property to confirm that all developer agreements assign IP to the company, and verify that your regulatory licenses are current and transferable [2].

Your unit economics must also be ready for scrutiny. Target an LTV/CAC ratio of at least 3:1 (ideally 5:1) and a CAC payback period of under 12 months [2]. Strong Net Revenue Retention (above 120%) demonstrates a solid product-market fit and reduces dependence on acquiring new customers [2]. Hitting the Rule of 40 - where your revenue growth rate plus EBITDA margin equals 40% or more - positions you for revenue multiples of 7.3x or higher [2].

Finally, timing is everything when negotiating. Aim to exit when you have at least 18 months of runway, not just six [10]. In fact, nearly 30% of secondary sales in the first half of 2025 were purchased at a premium to the most recent equity financing round, proving that exits from a position of financial strength secure better deals [10].

Having clean and accurate financial records is non-negotiable when it comes to positioning your FinTech for acquisition. Buyers want clarity, not uncertainty. Start by switching to accrual-basis accounting - this is the go-to method for FinTechs valued over $1 million [2]. Unlike cash-basis accounting, accrual accounting aligns revenue with the period it’s earned, giving buyers a more accurate view of your financial health.

Break down your revenue streams into categories like recurring subscriptions, transaction fees, interchange, licensing, and professional services. Why? Recurring revenue stands out as the most attractive to buyers, thanks to its predictability [2]. Make it crystal clear how much of your income falls into this category. Additionally, track key metrics like ARR/MRR, churn, NRR, LTV/CAC, and gross margins over the trailing twelve months (TTM) - these are the numbers buyers scrutinize when determining valuation.

Balancing growth and profitability is essential before you hit the market. Companies growing at 20–40% annually with proven profitability often secure valuations around 7.9x revenue. On the other hand, slower-growing companies (under 20%) typically trade at just 3.9x [2]. This valuation gap makes it worth the effort to optimize both growth and margins ahead of an exit.

Once your financials are in order, the next step is to focus on operational scalability.

Buyers want to see that your business can grow without a proportional jump in costs. One key indicator? Net Revenue Retention (NRR) above 120%. This signals that your existing customers are spending more over time, reducing your reliance on acquiring new customers to fuel growth [2].

Your unit economics also need to hold up under scrutiny. Aim for an LTV/CAC ratio of at least 3:1, with 5:1 being the gold standard. Keep your CAC payback period under 12 months [2]. For software-driven models, gross margins of 80% or higher show you can scale efficiently [2]. Additionally, annual churn rates below 7% are a strong benchmark for SaaS-based FinTechs [2].

Another factor that can impact valuation? Founder dependency. If your business is overly reliant on the founder for technical expertise or key relationships, expect a valuation discount of 15–30% [2]. To avoid this, build a management team capable of running the business independently. A great example is AutoRek, which rebranded in 2025 to target the North American market. The company revamped its website, secured six major clients, and boosted revenue by 21% in just a year, all of which strengthened its position for a potential exit [8].

Improving these metrics not only enhances your current performance but also sets you up for a higher valuation when it’s time to sell.

Internal improvements are important, but external validation can seal the deal. Third-party audits confirm the accuracy of your financial data and metrics, giving buyers confidence and strengthening your negotiation position [3]. Technical due diligence helps uncover potential risks - like outdated systems, reliance on key individuals, or poor documentation - while assessing your ability to scale and deliver sustainable returns post-acquisition [3].

Regulatory compliance is another area that can significantly boost valuation. Frameworks like DORA (EU), MiCA, or U.S. state money transmitter licenses are not just regulatory checkboxes - they’re assets that can take years and significant investment to replicate. If you already have these in place, they become a competitive advantage that justifies premium pricing [2]. Make sure all developer and contractor agreements assign intellectual property to the company and that regulatory authorizations are current and transferable [2].

Finally, prepare a well-organized data room with detailed metrics on NRR, LTV/CAC, and churn segmented by customer type. This reduces friction during due diligence, making it easier for buyers to validate your claims and move quickly to an offer. The smoother the process, the less room there is for buyers to negotiate down due to uncertainty [2].

Your deal structure choices can significantly shape the final outcome of your exit. Even if the headline valuation looks impressive, the way the deal is structured can determine what you ultimately take home. Between 2023 and 2025, M&A accounted for 73.7% of venture-backed exits in the U.S., whereas IPOs made up just 3.8% [4]. This means most FinTech founders will need to weigh options like cash versus equity, earnouts, and other payment structures that directly impact their payout.

Choosing the right structure isn't just about chasing the largest number - it’s about balancing risk, timing, and control.

"Expect deal structures that include seller notes and earn-outs rather than all-cash offers at this market stage"

- Thomas Smale, CEO of FE International [2]

The deal you choose affects not only how much you receive but also when you receive it and the risks involved. Below, we explore common deal structures and their impact.

The type of deal you select plays a big role in both your liquidity and risk exposure.

Here’s a quick comparison of the two deal types:

| Feature | All-Cash Deal | Cash-Plus-Equity Deal |

|---|---|---|

| Payout Timing | Immediate at closing | Immediate (cash) + Delayed (equity) |

| Risk Level | Low (guaranteed value) | Moderate (market/stock risk) |

| Valuation Impact | Lower headline price | Potential for higher total value |

| Founder Liquidity | High | Partial (subject to lock-ups) |

| Control After Exit | None | Minimal (as minority shareholder) |

Your decision depends on factors like your confidence in the buyer’s future success and your need for immediate cash. If you trust the acquiring company’s growth potential and can handle market exposure, a cash-plus-equity deal might yield a higher total return. On the other hand, if you prefer certainty or a clean exit, an all-cash deal is the safer route.

Earnouts are performance-based payments designed to bridge valuation gaps between buyers and sellers [4]. These deals include an upfront payment at closing, with additional payments tied to specific, measurable milestones. In the FinTech sector, these milestones often relate to regulatory achievements - like obtaining e-money licenses or securing key banking partnerships - rather than just revenue targets [6].

While earnouts can help close deals, they come with risks. Your payout depends on future performance, which may be influenced by factors beyond your control, especially if you’re not staying with the company post-acquisition. To protect your interests, it’s essential to define milestones clearly, measure them precisely, and establish firm timelines. Instead of vague goals like "final regulatory approval", aim for specific benchmarks such as "application filed" or "initial completeness response received" [6].

In 2025, global FinTech VC funding reached $51.8 billion, reflecting a 27% year-over-year increase [6]. However, this influx of capital often comes with stricter governance and more complex regulatory requirements.

"More capital does not equal simpler terms - it often means heavier governance and more detailed regulatory contingencies"

[6]

Understanding how these contingencies influence your earnout structure is crucial for securing a fair deal while minimizing risks.

Even the most promising FinTech companies can see their exit value take a hit due to avoidable mistakes. These errors often arise from rushing the process, misunderstanding buyer priorities, or neglecting due diligence preparation. The difference between a successful exit and a disappointing one often hinges on steering clear of a few key pitfalls. Let’s break down the most common missteps that can hurt your valuation.

Jumping into the market before your company is fully prepared can significantly hurt its valuation. One major red flag is high founder dependency - when the founder is the go-to person for technical decisions, compliance, or client relationships. This reliance can lead to valuation discounts of 15% to 30% because buyers want to see a business that operates smoothly without constant founder involvement.

Another critical factor is your financial reporting. Buyers expect accrual-basis accounting for FinTech companies valued above $1 million. Mixing recurring revenue with one-time income creates confusion, signaling a lack of operational maturity and making it harder for buyers to gauge your business quality.

Regulatory readiness is non-negotiable. Non-compliance with frameworks like DORA (Digital Operational Resilience Act) or MiCA (Markets in Crypto-Assets Regulation) can be a deal breaker during due diligence. Companies lacking up-to-date, transferable licenses or audit-ready compliance documentation may face valuation discounts as steep as 50% to 70%.

Lastly, your financial runway matters. A company with 18 months of cash reserves has far more negotiating power than one with just six months on hand.

Chasing a high valuation without carefully examining the deal terms can backfire. A high price tag won’t mean much if the deal includes provisions like full-ratchet anti-dilution clauses or multiple liquidation preferences (e.g., 2x). For instance, a 1x participating preference can drastically reduce your payout compared to a 1x non-participating preference. Always model potential payouts under various scenarios to ensure the deal terms align with your financial goals.

Revenue quality also plays a crucial role. For example, in the payments sector, using gross revenue instead of net revenue (after deducting interchange and processing fees) can inflate your valuation by over 300%. This kind of misrepresentation can mislead both you and potential buyers.

"A fintech startup valuation that uses Stripe or Adyen as comparables for a consumer lending company is fundamentally flawed."

- 409A Valuation for Fintech [12]

Valuation multiples also vary widely across FinTech subsectors. For instance, blockchain infrastructure might trade at 17.3x revenue, while lending platforms often trade at just 2.6x revenue due to their higher risk profiles. Ensure your deal structure reflects your exit strategy to avoid losing value.

Buyers come prepared with detailed checklists covering financial, legal, and operational transparency. Falling short of these expectations can delay the process and lower your valuation. In 2025, global FinTech VC funding hit $51.8 billion, accompanied by stricter governance standards and more demanding due diligence from investors.

To meet these expectations, audit your intellectual property and licensing. Make sure every developer and contractor agreement explicitly assigns IP to your company, and confirm that all money transmitter or banking licenses are current and transferable. Buyers will also want clear documentation of your AML/KYC workflows, custodial relationships, and cross-border data flows.

Investors often include termination rights in term sheets if specific licenses or approvals aren’t secured. Negotiate these rights into measurable milestones - such as "application filed" or "initial completeness response received" - instead of vague outcomes like "final regulatory approval."

Prepare a data room early with trailing 12-month metrics like Net Revenue Retention (NRR), LTV/CAC ratios, and your Rule of 40 score. Meeting the Rule of 40 threshold can boost your valuation, as companies achieving it typically trade at 7.3x revenue or higher.

Finally, with the shift from revenue-based to EBITDA-based valuations in 2025–2026, buyers are focusing more on cash flow and operational efficiency. If your financials don’t show a clear path to profitability, expect buyers to apply steep discounts - or walk away entirely. Detailed preparation for due diligence is no longer optional; it’s a must for securing the best valuation.

FinTech founders aiming for successful exits need to focus on early preparation, precise timing, and a deep understanding of their subsector's valuation metrics. Start early - ideally 12–24 months before entering the market. This gives you time to shift to accrual-basis accounting, minimize founder dependency, and establish professional-grade financial reporting. Valuation metrics vary across subsectors: for example, blockchain infrastructure companies are valued at 17.3x revenue, while lending platforms are at 2.6x. Knowing your benchmarks is key [2].

The 2026 market prioritizes efficiency over unchecked growth. Companies that meet the Rule of 40 often secure premium multiples, with valuations 50–100% higher than the median [2]. Strong unit economics are crucial, as they show buyers that your business generates cash effectively and retains customers without relying heavily on founders.

Regulatory compliance is another critical factor. Non-compliant companies can face valuation discounts of 50–70% during due diligence [2]. Additionally, businesses overly dependent on their founders may see discounts of 15–30%. Building a capable management team that operates independently is essential to avoid these pitfalls [2].

To prepare for a successful exit, take action now. Transition to accrual-basis accounting if you haven’t already, review intellectual property assignments, and set up a data room with 12 months of metrics, including ARR/MRR, churn, and Rule of 40 performance. Ensure your compliance frameworks are well-documented, and verify that all regulatory licenses are current and transferable. These steps demonstrate operational maturity and make the due diligence process smoother.

For founders looking to maximize their valuation or prepare for an exit, partnering with experienced advisors can make a significant difference. Consider working with Phoenix Strategy Group (https://phoenixstrategy.group), which specializes in growth-stage FinTech companies. Their services include fractional CFO support, FP&A systems, and M&A advisory, all tailored to help you navigate subsector benchmarks, prepare for due diligence, and achieve premium valuations. With thorough preparation and expert guidance, you can confidently approach the market and secure the exit your business deserves.

In the FinTech world, buyers focus on factors like revenue quality, regulatory compliance, and valuation multiples unique to your niche. For instance, payments companies often see valuations in the range of 4–6x revenue, whereas AI-driven platforms can fetch much higher multiples, often exceeding 10x revenue. Knowing these industry standards can make a big difference when positioning your business for a successful sale.

To gauge if you're ready for an exit within the next 12–24 months, take a close look at a few key areas. Start with your strategic narrative - does your story resonate with potential buyers and showcase your long-term vision? Next, assess your financial performance; strong, consistent numbers can make all the difference. Don't overlook operational readiness - this includes ensuring your processes and systems can scale smoothly.

You’ll also want to evaluate your valuation metrics and market position. Are they competitive and appealing? Finally, confirm you've hit essential milestones like regulatory compliance, building a scalable infrastructure, and achieving notable customer growth. These factors not only influence your valuation but also determine how attractive your business is to potential buyers.

Earnouts and cash-plus-equity deals offer a way to potentially increase your payout by linking payments to future performance. This approach ensures that everyone involved has aligned incentives. However, these deals can come with challenges, such as delayed payments or the uncertainty of meeting performance goals. The specifics of the deal dictate how much of your payout is secured upfront versus contingent on achieving future milestones.