Published on

December 11, 2025

Venture debt offers startups a way to extend their runway without giving up more equity, but rising interest rates in 2025 have made this option more expensive. Here's what you need to know:

Understanding the trade-offs and costs involved in venture debt is critical for making informed financing decisions in today’s high-rate environment.

Venture debt is a loan specifically designed for startups that have already secured funding from institutional investors. Unlike traditional bank loans, which typically require collateral, steady revenue streams, or established profitability, venture debt focuses on a startup's growth potential and its backing from venture capital firms. These loans are structured as term loans, usually lasting between 1 and 5 years. They often include an initial 6–12 month period where only interest is paid, followed by monthly payments that cover both principal and interest.[6][7]

The amount of venture debt a startup can access is typically tied to its most recent equity raise, often ranging from 20–35% of that round. For instance, a startup that raises $10 million in a Series A round might secure between $2 million and $3.5 million in venture debt.[6] In addition to the loan itself, lenders usually receive warrants that equate to 0.5–1.5% of the company’s fully diluted equity. Borrowers also face upfront fees of about 1–2% and end-of-term fees ranging from 3–6%.[2][8][4] These terms highlight the key differences between venture debt and equity financing, which are explored next.

The main distinction between venture debt and equity financing lies in ownership and repayment. Equity financing involves issuing new shares, which dilutes the ownership of existing shareholders. Venture debt, on the other hand, causes minimal dilution - typically around 1% if the warrants are exercised.[2][8][4] For lenders, the primary return comes from interest payments and fees, rather than any significant equity gains.

However, venture debt does come with fixed monthly payments once the interest-only period ends. This can increase a startup's cash burn and demand stricter financial oversight. In contrast, equity funding doesn’t require repayments but comes at the cost of giving up more ownership. If a startup defaults on its debt, it may face accelerated repayment demands or other financial consequences. Equity investors, by comparison, share the downside risk and are only paid after creditors in a liquidation scenario. Given these trade-offs, startups often use venture debt strategically to fuel growth, as outlined below.

Startups often turn to venture debt to extend their financial runway after an equity round. This can provide an additional 6–18 months of capital, helping the company achieve key milestones like hitting revenue targets, refining product–market fit, or improving unit economics before a subsequent funding round.[1][8][6][7] For example, a U.S.-based SaaS startup that raises $12 million in a Series A round might secure a $3 million venture debt facility - roughly 25% of the equity raise. This loan could include a 12-month interest-only period, followed by 36 months of amortization at a rate of SOFR + 7%.[2][3][4][6] With these funds, the startup might scale hiring or amplify marketing efforts, potentially growing its annual recurring revenue from $2 million to $6 million in 18 months. This growth could support a higher valuation during the next equity round, even after factoring in the interest costs and minor dilution from warrants.

Other common uses for venture debt include funding growth initiatives like sales team expansion, marketing campaigns, launching new products, or entering new markets. It can also serve as a bridge to the next equity round, especially when a startup’s metrics are improving but market conditions make equity financing less attractive. Additionally, high-performing startups may use venture debt to bolster cash reserves, reducing the need to issue more equity and incur further dilution. Understanding these scenarios is key to evaluating how changes in interest rates might impact the overall cost of carrying this type of debt.

Venture debt interest rates are usually variable and tied to the broader economy, meaning they fluctuate as economic conditions shift. These loans are often pegged to a benchmark rate - like SOFR (Secured Overnight Financing Rate) - plus an additional spread, typically ranging from 6% to 9%. For example, a loan structured as SOFR + 7% could result in an effective rate of about 10–11%, depending on market conditions[1][4].

When the Federal Reserve raises rates, borrowing costs for startups increase almost instantly. Many venture debt agreements include an interest-only period of 6–12 months, during which companies only pay interest and not principal. However, a higher benchmark rate during this period directly impacts cash flow, increasing a startup's burn rate. By 2024–2025, total interest rates for venture debt generally range from 8% to 15% annually and can climb above 20% for higher-risk startups.

Since 2022, Federal Reserve rate hikes have steadily driven up benchmarks like SOFR and the Prime rate, a trend that has extended into 2025. With the Prime rate sitting at around 8.5% or more, the cost of venture debt has risen accordingly. This keeps typical all-in rates within the 8–15% range, though some deals exceed this, especially for riskier borrowers. In this tighter financial environment, lenders have adjusted their strategies, becoming more selective about the startups they choose to fund.

Faced with higher interest rates, lenders have shifted their focus toward managing risk more carefully. They now prioritize startups with solid financial fundamentals, such as strong unit economics and predictable revenue streams. Companies with recurring revenue models, like SaaS businesses, often stand out. Additionally, lenders tend to favor startups backed by established venture capital firms and base loan sizes on a company's most recent equity raise.

To protect their investments, lenders are also enforcing stricter covenants. These might include requirements like hitting specific revenue targets, maintaining minimum cash reserves, or achieving certain milestones. For startups without clear paths to profitability or strong VC backing, securing venture debt has become far more challenging. These companies often face tougher terms - or may struggle to secure funding altogether.

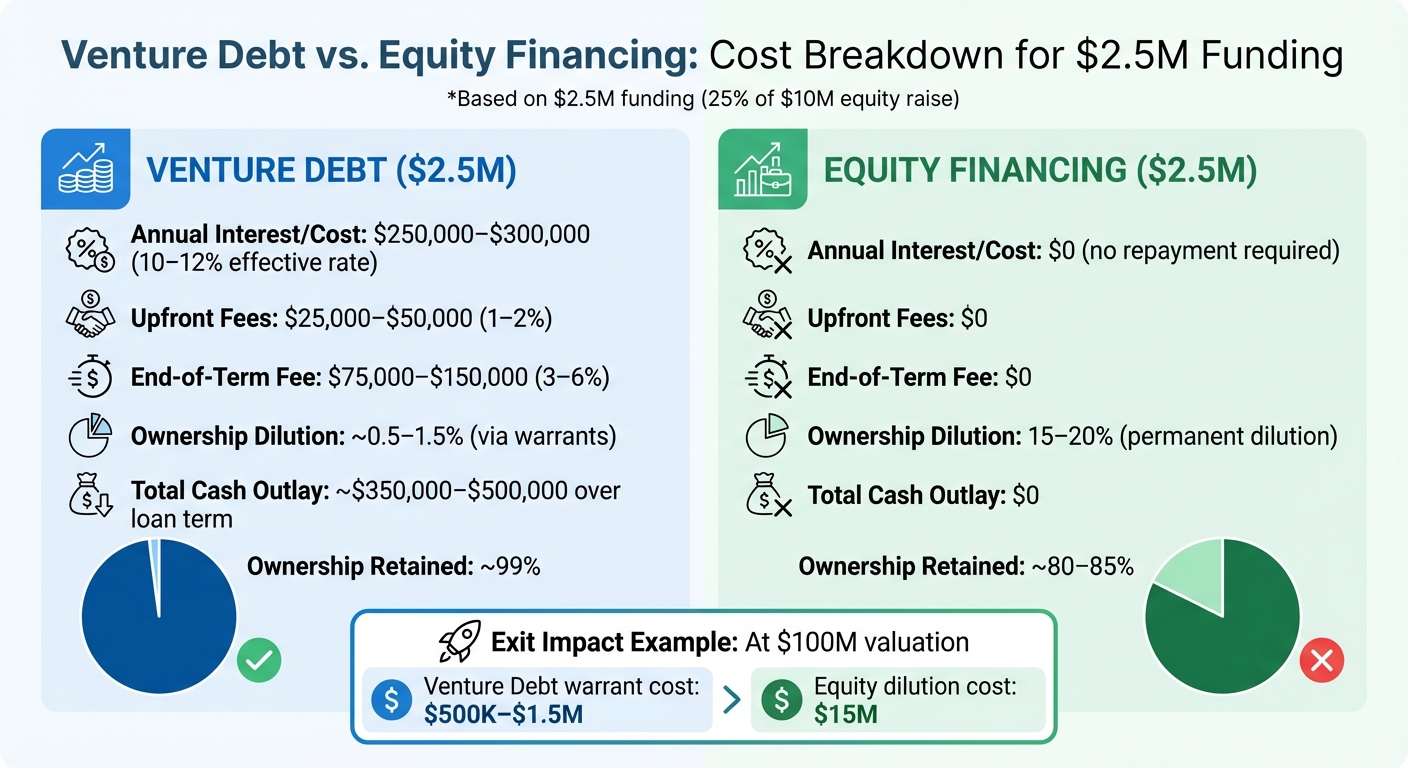

Venture Debt vs Equity Financing: Cost Comparison for $2.5M Funding

In today’s high-interest-rate environment, understanding the various costs tied to venture debt is essential for making smart financing choices. Venture debt typically involves four key cost components: cash interest, upfront fees, end-of-term payments, and warrants. Each of these plays a role in the overall expense of the loan. According to EisnerAmper, a common structure includes SOFR + 6–9% interest (resulting in an effective annual rate of about 8–15%), an upfront origination fee of 1–2% of the loan amount, an end-of-term fee of 3–6%, and warrants covering 0.5–1.5% of the company’s fully diluted equity [2].

Cash interest, which can be paid monthly or quarterly, is typically tied to benchmarks like SOFR or the Prime rate. For example, a rate of Prime + 7% could result in an all-in rate of 15–16% if Prime is around 8.5% in 2024–2025 [5]. The upfront fee is due at the time of closing, while the end-of-term fee is payable when the loan matures or if it’s repaid early. Warrants allow lenders to purchase equity at a fixed price, usually based on the valuation from your most recent funding round. If your company achieves a high valuation upon exit, the 0.5–1.5% warrant coverage could translate into a significant financial gain for the lender.

Additional costs may include draw fees (0.5–2.0%), prepayment penalties, and unused line fees [4][6]. Moreover, legal and due diligence expenses are often passed on to the borrower. A case study from Breaking Into Wall Street highlighted how even a modest 0.1% warrant coverage could boost a lender’s internal rate of return from a headline rate of 10–11% to about 12.4% IRR [4]. Knowing these cost layers helps you weigh them against the potential dilution from equity financing.

When deciding between venture debt and equity financing, it’s crucial to evaluate the trade-offs. In a high-rate environment, both options are more expensive than in the past. Venture debt allows you to retain ownership but requires regular cash payments, while equity financing avoids repayment but results in permanent dilution of your stake.

The table below provides a comparison, using the example of a startup that recently raised $10 million in equity and is considering $2.5 million in venture debt (a typical 25% add-on):

| Cost Factor | Venture Debt Cost ($2.5M) | Equity Financing Cost ($2.5M) |

|---|---|---|

| Annual Interest/Cost | $250,000–$300,000 (10–12% effective rate) [4][5] | None (no repayment required) |

| Upfront Fees | $25,000–$50,000 (1–2%) [2] | None |

| End-of-Term Fee | $75,000–$150,000 (3–6%) [2] | None |

| Ownership Dilution | ~0.5–1.5% (via warrants) [2] | 15–20% (permanent dilution at current valuation) [6] |

| Total Cash Outlay | ~$350,000–$500,000 over loan term | $0 |

| Ownership Retained | ~99% (minus small warrant dilution) | ~80–85% |

For startups burning through cash and not yet profitable, those monthly interest payments can put a strain on your runway. On the other hand, equity financing doesn’t require repayment but permanently reduces your ownership stake. For example, if your company exits at a $100 million valuation, a 15% equity dilution could cost you $15 million. In contrast, the warrant dilution from venture debt might only cost between $500,000 and $1.5 million [4][6]. Carefully modeling both scenarios under current market conditions can help you understand how each option affects your growth plans and potential exit outcomes.

When interest rates climb, pushing your total borrowing costs into the 10–15% range or higher, managing cash flow becomes critical. Start by creating a rolling 13-week cash flow forecast. This should account for every dollar coming in and going out, including monthly interest payments on your floating-rate facility. For example, if you're paying SOFR + 7% and SOFR is at 4.5%, your annual rate is 11.5%. On a $1 million draw, that’s roughly $9,583 per month. To stay ahead, test your liquidity under different scenarios - base, optimistic, and pessimistic - and aim to maintain a cash buffer that covers 6–12 months of runway.

Controlling expenses is just as important. Zero-based budgeting can help you justify every cost, while small adjustments - like negotiating 10–15% vendor discounts or trimming marketing spend by 20–30% - can make a big difference. SaaS companies, in particular, often find savings by optimizing cloud infrastructure usage, potentially freeing up thousands of dollars each month to cover debt payments. Norman Rodriguez, Founder and CEO of ElevateHire, shared his experience working with Phoenix Strategy Group during a tough financial period:

PSG saved my dream. They helped us get our financials in order and renegotiate our lending agreements, pulling us through a tough financial crunch.

By focusing on disciplined financial practices like weekly bookkeeping closes, real-time KPI tracking, and automated expense approvals, you can ensure you never miss an interest payment. Hitting performance milestones may even allow you to extend your interest-only period. These efforts not only stabilize cash flow but also improve your leverage when it’s time to renegotiate loan terms.

If your startup is meeting revenue or fundraising milestones, you can use that momentum to negotiate better loan terms. Rather than focusing on small rate reductions, aim for changes that provide more runway, like longer interest-only periods (9–12 months instead of 6) or back-loaded amortization schedules. These adjustments often add more value than shaving 50 basis points off your interest rate. For example, if your revenue has grown more than 20% year-over-year, you could request reduced upfront fees (from 1–2% to 0.5%) or negotiate lower warrant coverage - closer to 0.5% of fully diluted equity instead of 1.5%.

Before approaching lenders, prepare updated financials, cap tables, and growth projections. Show that you’re meeting or exceeding covenants, such as maintaining minimum cash balances or achieving ARR targets, and propose specific amendments like relaxed liquidity thresholds or a conditional 12-month extension on your interest-only period. Lenders are more likely to adjust terms when you present data-backed proposals alongside a proven track record of hitting milestones. Hiring a fractional CFO or a strategic finance advisor can give you an edge in these discussions. Firms like Phoenix Strategy Group specialize in helping startups model scenarios, prepare materials, and lead lender negotiations. If renegotiating terms doesn’t work, it may be time to explore other financing options.

If better loan terms aren’t achievable, alternative funding methods can help ease the burden of high debt costs. One option is revenue-based financing (RBF), where you repay a percentage of your monthly recurring revenue - typically 5–10% - instead of fixed interest payments. For a SaaS startup with steady revenue, a $1 million RBF facility at an 8% revenue share can be repaid faster during growth periods, without the rigid amortization schedules or covenants tied to traditional venture debt. RBF also avoids the 10–15% fixed interest and 3–6% end-of-term fees that increase your total cost.

Short-term bridge loans (3–12 months, with rates of 12–20%) are another option, especially if you’re close to securing your next equity round. These loans can help you navigate a covenant breach or temporary cash gap without committing to long-term debt. They’re most effective after a Series A round when you need $2–3.5 million (20–35% of your equity raise) and have a clear plan for repayment to avoid compounding fees. Some startups even combine RBF or bridge loans with venture debt to diversify their capital sources and reduce warrant coverage to 0.5–1%. With the support of firms like Phoenix Strategy Group, you can model these combinations to optimize your capital structure and avoid over-leveraging when interest rates are high.

Venture debt is essentially a term loan tailored for VC-backed companies, typically structured over 2–4 years. It often starts with a 6–12 month interest-only period, followed by amortization. U.S. startups commonly use this option to extend their runway after a Seed, Series A, or Series B funding round, to fund growth initiatives like expanding sales or marketing efforts, or to provide a financial cushion while preparing for the next equity raise. One of its biggest advantages? It’s less dilutive. Instead of giving up 10–20% more equity in another funding round, founders only pay interest, fees, and issue warrants that usually represent about 0.5–1.5% of fully diluted equity - far less than a traditional equity round.

The overall cost includes a floating cash interest rate (often tied to SOFR or WSJ Prime, plus 6–9%, equating to roughly 10–15% annually in recent deals), upfront and draw fees (0.5–2% of the loan amount), end-of-term fees (typically 3–6% of the principal), and the smaller warrant grants. To make venture debt work for your company, it’s critical to align it with your growth strategy and maintain flexibility in your operations.

When interest rates are high, the decision to take on venture debt requires extra scrutiny. Start by creating a 12–24 month cash flow forecast that accounts for current SOFR or Prime levels. Include multiple scenarios - downside, base, and upside - to ensure you can comfortably meet repayment obligations. Instead of focusing solely on lowering the interest rate, prioritize optimizing the loan structure. Negotiate for features like a longer interest-only period, flexible draw schedules, and covenants that align with your company’s performance metrics.

If the interest rates seem too steep relative to the benefits, consider alternatives. You might explore refinancing to extend terms or adjust covenants, look into revenue-based financing or short-term bridge loans, or even raise a smaller equity round to reduce debt reliance. While venture debt can still be a valuable tool, it’s crucial to avoid using it as a band-aid for unresolved issues like excessive burn rates or stalled growth. Address those challenges first, then leverage debt to amplify initiatives that are already working. Taking these steps ensures you’re building a solid foundation before layering on additional financial commitments.

Navigating these complexities can be daunting, but expert advisors like Phoenix Strategy Group can provide the guidance startups need. Their services include financial planning support, such as creating detailed cash flow forecasts and tracking covenant compliance. They specialize in building integrated 3-statement models and monitoring covenant headroom in real time, giving startups the tools to negotiate better loan terms or refinance existing debt.

If financial challenges arise, Phoenix Strategy Group can step in to renegotiate lending agreements. They help secure extended interest-only periods, relaxed covenants, or revised repayment schedules - often preventing small issues from escalating into bigger problems. By combining financial expertise with a focus on unit economics and strategic planning, they equip growth-stage companies with the clarity and systems needed to navigate venture debt effectively. This allows founders to focus on scaling their businesses with confidence.

When interest rates climb, so does the cost of venture debt. Lenders usually increase their rates to match the higher borrowing costs, leaving startups with heftier interest payments. This added expense can put pressure on cash flow and chip away at profitability.

If your startup depends on venture debt, it’s crucial to take a close look at how these rising costs fit into your financial plan. Review your debt agreements and explore strategies to better manage cash flow, ensuring you can handle the impact without jeopardizing your operations.

Venture debt is a financing option where startups borrow money that must be repaid with interest. This approach helps founders secure funds without giving up a large portion of their ownership. On the other hand, equity financing involves selling shares of the company to investors in exchange for capital. While this doesn’t require repayment, it does dilute ownership stakes.

For startups, venture debt can be a practical way to extend their financial runway or fuel growth without sacrificing too much equity. That said, managing repayment obligations carefully is crucial to avoid putting unnecessary financial pressure on the business as it grows.

Startups can weather the storm of high-interest rates by focusing on smart financial planning and keeping a sharp eye on cash flow. This means tracking every expense, finding ways to boost revenue, and staying on top of your debt obligations.

Another key move? Work with lenders to secure better loan terms and nurture strong relationships with financial partners. These efforts can ease the pressure of rising rates. On top of that, using reliable forecasting and budgeting tools can help you stay ahead of potential financial hurdles and manage debt more effectively.

By blending financial strategies with day-to-day operational planning, startups can strengthen their financial footing and rely less on debt, even when the economy gets tough.