Published on

April 27, 2026

Environmental liabilities in M&A deals can lead to massive financial risks if not addressed properly. These liabilities include cleanup costs for legacy contamination, compliance violations, and the rising threat of emerging pollutants like PFAS. Buyers can face strict legal responsibility under CERCLA, even for issues they didn't cause. For example, 3M settled PFAS contamination claims for up to $12.5 billion in 2023, showing how these risks can devastate valuations.

Key Points You Need to Know:

Skipping thorough due diligence can result in legal, financial, and reputational fallout. Buyers and sellers must work together to address these risks early, using assessments, contracts, and insurance to safeguard investments.

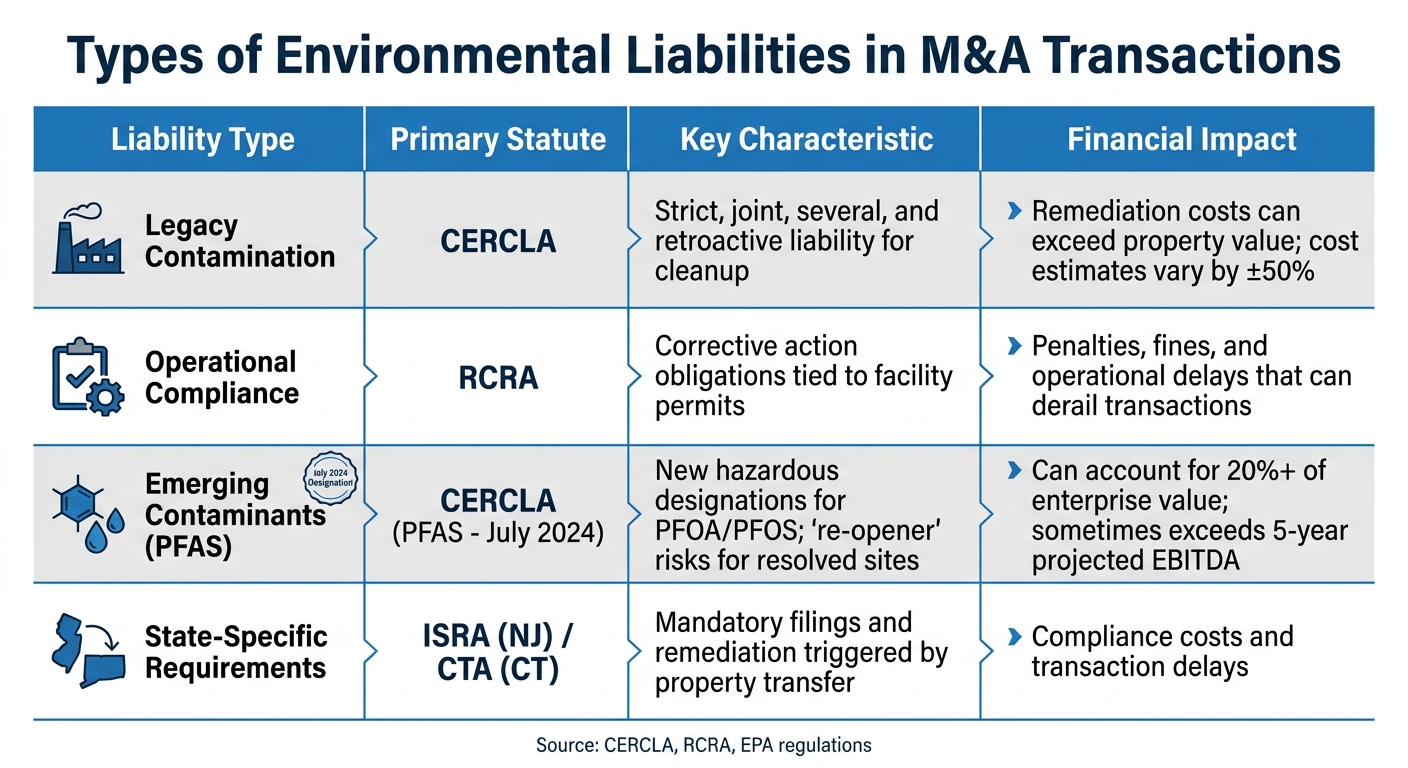

Types of Environmental Liabilities in M&A Transactions

Environmental liabilities in mergers and acquisitions (M&A) can significantly impact deal structures and require careful attention during due diligence. These liabilities generally fall into three main categories, each carrying distinct risks and financial implications.

Legacy contamination refers to pollution from past activities - often decades old - that persists in soil, groundwater, or building materials. Under CERCLA, buyers can face strict, retroactive, and joint liability for these issues, even if they didn't cause the contamination. Often, these liabilities remain hidden until regulators step in or a Phase II environmental assessment reveals subsurface pollution. Remediation costs can be staggering, sometimes exceeding the value of the property itself, with cost estimates varying by roughly ±50% [3].

"Environmental liability is the hidden cost variable in manufacturing acquisitions. Contaminated soil, groundwater, or building materials discovered after closing can generate remediation obligations that dwarf the original purchase price." – Alex Lubyansky, M&A Attorney [3]

The financial burden isn't limited to cleanup expenses. Legacy contamination can lead to disruptions like enforcement actions, restrictive deed covenants, and long-term monitoring requirements. To address these risks, buyers often negotiate purchase price adjustments, contamination indemnities, or escrow accounts to cover future cleanup costs.

Regulatory compliance liabilities emerge from violations of environmental laws, including CERCLA and the Resource Conservation and Recovery Act (RCRA). Facilities governed by RCRA may have corrective action requirements that bind future owners [2]. Additionally, state-specific laws, such as New Jersey's Industrial Site Recovery Act (ISRA) and Connecticut's Transfer Act (CTA), impose additional obligations during ownership transfers. These can include mandatory filings, environmental evaluations, or cleanup measures [4].

While permit reviews and regulatory filings can help identify these issues, non-compliance can still result in penalties, fines, and operational delays, potentially derailing transactions.

Emerging contaminants, particularly PFAS (commonly referred to as "forever chemicals"), represent a growing concern. In July 2024, the EPA classified PFOA and PFOS as hazardous substances under CERCLA, making buyers potentially responsible for cleanup costs, even for contamination they didn't cause [5][7]. This new designation also introduces "re-opener" risks, where previously resolved Superfund sites may face renewed regulatory actions to address PFAS contamination [6].

The risk extends beyond chemical manufacturers to industries using firefighting foams (AFFF), specialized coatings, lubricants, or nonstick applications [6][7]. Complicating matters, most standard Commercial General Liability (CGL) policies exclude environmental coverage, leaving acquirers exposed to post-closing liabilities [7]. Despite this, fewer than 20% of insurance buyers hold specialized environmental policies, even though environmental liabilities can account for 20% or more of a property's total enterprise value [7]. In some cases, remediation costs have even surpassed the target company's projected EBITDA for the next five years [7].

| Liability Type | Primary Statute | Key Characteristic |

|---|---|---|

| Legacy Contamination | CERCLA | Strict, joint, several, and retroactive liability for cleanup. |

| Operational Compliance | RCRA | Corrective action obligations tied to facility permits. |

| Emerging Contaminants | CERCLA (PFAS) | New hazardous designations for PFOA/PFOS as of July 2024. |

| State-Specific | ISRA (NJ) / CTA (CT) | Mandatory filings and remediation triggered by property transfer. |

These challenges highlight the importance of thorough environmental assessments during the M&A process to mitigate risks and safeguard investments.

When it comes to mergers and acquisitions (M&A), environmental due diligence typically involves two key phases: a Phase I Environmental Site Assessment (ESA) to identify possible contamination risks, and a Phase II ESA to conduct sampling and quantify any issues found. These steps are not just regulatory checkboxes - they're critical for meeting requirements under CERCLA and for uncovering potential remediation costs that could heavily influence the deal's financials [3].

A Phase I ESA is a non-invasive process designed to identify Recognized Environmental Conditions (RECs). It relies on research, visual inspections, and interviews rather than physical sampling. To meet CERCLA liability protections, the assessment must comply with ASTM Standard E1527-21 (or E2247-23 for forestland and rural properties) and adhere to the EPA's All Appropriate Inquiries (AAI) standard [3].

Here’s what the process generally involves:

"A compliant Phase I ESA is required to establish All Appropriate Inquiry under CERCLA, which is the threshold condition for innocent landowner, contiguous property owner, and bona fide prospective purchaser liability defenses."

– Alex Lubyansky, M&A Attorney [3]

To qualify as an EP, individuals typically need a professional license (e.g., PE or PG), a relevant degree with at least three years of experience, or over 10 years of specialized expertise. The main goal of a Phase I ESA is to identify RECs. It’s worth noting that a Phase I ESA is valid for AAI purposes for 180 days from the site visit date. After that, updates are required, and after one year, a completely new assessment becomes necessary.

For older properties, it’s a good idea to include separate checks for asbestos, lead-based paint, mold, and radon. Also, ensure the EP examines nearby industrial sites, as groundwater contamination can migrate. If the property appears in regulatory databases, reviewing agency files can clarify whether the listing involves an active enforcement case or a resolved issue [3].

| REC Classification | Definition | Implication |

|---|---|---|

| Recognized Environmental Condition (REC) | Evidence of a current or past release needing further investigation. | Requires Phase II testing. |

| Historical REC (HREC) | A past release that has been resolved to regulatory standards. | Lower risk; Phase II may not be needed. |

| Controlled REC (CREC) | A release managed through risk-based remediation, often with land use controls in place. | Requires ongoing monitoring and compliance. |

When RECs are identified in a Phase I ESA, a Phase II ESA is the next step. This phase involves physical sampling and lab analysis to measure contamination levels in soil, groundwater, and vapor. Common methods include soil borings, groundwater monitoring wells, and vapor sampling, especially for contaminants like chlorinated solvents or petroleum hydrocarbons [3].

"Phase II soil and groundwater sampling is triggered by Recognized Environmental Conditions in the Phase I report. Skipping Phase II when RECs exist exposes the buyer to undisclosed contamination that can generate six- or seven-figure remediation obligations."

– Alex Lubyansky, M&A Attorney [3]

Skipping Phase II can leave buyers vulnerable to CERCLA liability as a potentially responsible party. In properties with long industrial histories, it’s rare to see a completely "clean" Phase I report. If you do, double-check its thoroughness. When Phase II uncovers contamination hotspots, additional testing may be needed to map the full extent of the issue. The data gathered is invaluable for estimating remediation costs, which at this stage can vary by ±50%.

Completing both phases ensures compliance with AAI requirements, enabling buyers to qualify for the Bona Fide Prospective Purchaser (BFPP) defense. This allows the acquisition of properties with known contamination without inheriting federal cleanup liability, provided post-acquisition obligations are met [3]. These steps are essential for integrating environmental risks into M&A valuation and strategy.

For tailored guidance on incorporating these due diligence practices into your M&A plans, reach out to the experts at Phoenix Strategy Group.

After identifying environmental risks through thorough assessments, the next step is figuring out who will bear the costs and how to shield both parties from unexpected expenses. Using a mix of well-crafted contracts and specialized insurance can help ensure these liabilities are handled effectively. This approach can mean the difference between a successful deal and one derailed by unresolved liability issues.

Allocating environmental risks often starts with detailed contractual protections. Environmental indemnity clauses are agreements where the seller compensates the buyer for costs tied to pre-existing contamination, such as cleanup expenses or regulatory fines. These clauses must clearly define their scope (what types of contamination are included), duration (how long the indemnity applies), and financial limits (the maximum amount the seller will pay) [8].

Unlike standard M&A warranties that usually last 18 to 36 months, environmental indemnities often extend for several years. This is because issues like contamination can take a long time to emerge. For instance, contaminants like PFAS may only become apparent over time due to slow groundwater migration [8][9]. Setting aside funds in an escrow account or using holdbacks from the purchase price can provide immediate financial resources for addressing these issues [8][4].

Contracts may also include mechanisms to limit liability claims. A de minimis clause prevents claims below a certain dollar threshold, while a basket clause groups smaller claims together, requiring the seller to pay only if the total exceeds a specific amount. Additionally, a cap sets an upper limit on the seller's liability [9]. Buyers in high-risk transactions often prefer tipping baskets, which make the seller responsible for the entire amount once the threshold is crossed, ensuring full recovery [9].

When neither party wants to assume long-term liability, environmental insurance can shift the risk to a third-party insurer, making it easier to move forward with the deal [11]. Pollution Legal Liability (PLL) policies cover claims for bodily injury, property damage, and cleanup costs, regardless of whether the contamination was known at the time of purchase [4][11]. Meanwhile, Remediation Cost Cap policies protect against cleanup costs exceeding initial estimates, typically kicking in after expenses surpass 100% to 125% of the projected amount [11].

Premiums for these policies generally range from 2% to 8%, reflecting the potentially high costs of remediation [11]. This might seem steep, but it’s worth considering that cleanup costs can vary widely - from $140,000 to over $30 million, depending on the site. Additionally, environmental violations led to over $1.3 billion in penalties in 2023, according to the EPA [10]. For sellers, especially those retiring or dissolving their businesses, insurance offers a way to avoid long-term indemnification obligations. Buyers, on the other hand, gain a reliable recovery option backed by an A-rated insurer, which is often more dependable than relying on a seller who may become financially unstable in the future [11].

However, it’s essential to carefully review policy exclusions. Many insurers won’t cover "known contamination", "intentional acts", or emerging pollutants like PFAS, which often require separate policies at a higher cost [11]. Additionally, underwriting can take 90 to 120 days if new environmental assessments are required, so planning ahead is critical [11]. When paired with contractual safeguards, environmental insurance creates a robust strategy for managing risks in M&A deals. To tailor these protections to your specific needs, Phoenix Strategy Group offers expertise in integrating environmental risk management into your broader transaction strategy.

Environmental risks can significantly impact enterprise value, sometimes influencing up to 10% of final valuation multiples in heavy industry M&A transactions [12]. Environmental assessments are no longer just a box to check; they now play a critical role in shaping financial models. Deal teams must incorporate findings on contamination and regulatory risks directly into their financial calculations, rather than relegating them to footnotes.

This requires early collaboration between environmental consultants and financial advisors. For example, if a Phase II environmental assessment uncovers $25 million in soil cleanup costs, but the target company has only allocated $8 million for it, the $17 million gap must be addressed. This could involve setting up escrow accounts, adjusting the purchase price, or restructuring the deal [12]. Without such coordination, buyers risk inheriting unforeseen liabilities, which can directly affect valuation and pricing strategies.

The growing focus on forward-looking risks, such as carbon taxes and decarbonization mandates, adds another layer of complexity. These factors are no longer hypothetical - they directly affect cash flow projections. For instance, a $7.3 million annual remediation cost, when discounted at 8%, could reduce a target’s enterprise value by $68 million [12]. Similarly, environmental regulations that shorten the lifespan of assets, like a coal-fired power plant whose operational timeline is cut from 2040 to 2030, could lead to $150 million in impairment charges [12].

Environmental assessments have evolved into essential components of financial modeling. When contamination is identified, remediation costs are no longer treated as abstract risks - they are factored directly into the purchase price. For example, ongoing expenses like groundwater treatment or hazardous waste disposal are integrated into Discounted Cash Flow (DCF) models, reducing profitability and, ultimately, the buyer's offer.

But the financial impact doesn’t stop at cleanup costs. Stranded asset risks, caused by regulatory changes, can lead to significant write-downs. For instance, a high-carbon boiler expected to operate until 2038 might face forced retirement by 2028, resulting in a $25 million write-off [12]. To account for these uncertainties, sensitivity analyses are essential, especially for carbon-intensive assets under regulatory pressure.

Market trends highlight the financial weight of environmental factors. Research shows that 83% of M&A buyers are willing to pay more for companies with strong ESG credentials, while 67% push for price reductions when sustainability weaknesses are identified [1]. Recent high-profile cases have demonstrated how such liabilities can drastically shift valuations [1]. This underscores the importance of treating environmental risks as financial variables that demand board-level attention, not just compliance checkmarks.

Deal structures also influence liability exposure. In asset purchases, buyers can limit their risk by isolating legacy contamination within the seller’s entity. On the other hand, stock purchases transfer the target’s entire environmental history - including potential unquantified liabilities - to the buyer [1]. Financial and environmental advisors must work together to evaluate these options and select the structure that minimizes long-term costs.

Close collaboration between financial and environmental advisors is essential for managing risks effectively. Environmental experts should be involved early in the deal process - not just as a final due diligence step, but as active participants in shaping pricing and deal structure [1]. For instance, if consultants uncover PFAS contamination or Superfund site obligations, financial teams need precise cost estimates to adjust valuation models. Failing to quantify these liabilities early can leave buyers exposed to costly surprises post-acquisition.

This partnership also extends to reviewing contractual protections. Financial advisors must ensure that indemnity clauses can withstand CERCLA’s joint and several liability rules, which could hold buyers responsible for 100% of cleanup costs, even for minor contributions [1]. Additionally, Pollution Legal Liability (PLL) insurance policies often exclude known conditions identified during due diligence. Joint reviews of these policies by financial and environmental teams are critical to identifying coverage gaps [12]. Considering that fewer than 20% of insurance buyers currently purchase specialized environmental policies, such reviews are increasingly important [1].

Post-acquisition, integrated teams prioritize immediate compliance actions to avoid shutdowns or hefty EPA fines. For example, 90-day compliance sprints can address urgent regulatory filings [12]. Teams also conduct sensitivity analyses on DCF models, projecting scenarios like a 10-year reduction in the lifespan of carbon-intensive assets to understand potential downside risks. By late 2025, 70% of S&P 500 companies had tied executive compensation to ESG performance metrics, reflecting the growing importance of environmental considerations in strategic decision-making [12].

Phoenix Strategy Group specializes in M&A advisory services that integrate environmental risk assessments into financial analysis. By quantifying liabilities, adjusting valuations, and structuring deals to account for both historical contamination and future risks, they help buyers make informed decisions and avoid post-closing surprises.

Protecting deal value and avoiding costly surprises post-closing requires careful attention to environmental due diligence. Under CERCLA's retroactive, strict, and joint liability rules, buyers can be held fully responsible for cleanup costs tied to legacy contamination - even if they had no role in causing it. Skipping thorough assessments leaves buyers vulnerable to liabilities that can lead to financial write-downs, legal battles, and breaches of fiduciary duty.

The financial risks are substantial. Recent high-profile settlements highlight the enormous potential costs, especially since fewer than 20% of insurance buyers currently secure specialized environmental insurance policies [1]. These numbers emphasize the importance of integrating technical and financial due diligence into the deal process.

Engaging environmental and financial advisors early can help refine pricing and deal structure. For instance, a Phase I Environmental Site Assessment conducted under ASTM E1527-21 standards can establish the "innocent landowner defense", while Phase II sampling provides clarity on actual remediation expenses before commitments are finalized [13]. This approach ensures contamination risks are properly accounted for in purchase price adjustments, indemnities, and escrow agreements.

Experts agree on the critical role of environmental diligence:

"Environmental diligence is the single most consequential legal workstream in a manufacturing acquisition" – Alex Lubyansky, Esq., Acquisition Stars [13]

The impact on valuation is clear. With 83% of M&A buyers willing to pay premiums for strong ESG credentials and 67% seeking discounts for environmental shortcomings, the quality of due diligence directly affects deal outcomes [1]. Boards must ensure these processes are robust, as they play a key role in identifying material risks before they escalate into post-closing challenges.

Environmental concerns, such as a property's contamination history or the presence of hazardous substances like PFAS, can lead to liability under CERCLA. The law places responsibility on current property owners for contamination, even if they had no role in causing it or were unaware of its existence. Because of this, conducting thorough legal and environmental due diligence is crucial during mergers and acquisitions to uncover any potential liabilities.

A Phase II Environmental Site Assessment (ESA) comes into play when a Phase I ESA uncovers recognized environmental conditions (RECs). Essentially, it's the next step to dig deeper - both literally and figuratively.

This process involves collecting and analyzing samples of soil, groundwater, or other materials from the site. The goal? To confirm whether contamination is present and, if so, to figure out how far it has spread. It's a critical step in ensuring that any environmental risks or liabilities are thoroughly understood, especially during the due diligence phase of a property transaction or development project.

Buyers assess the pricing of PFAS and other newly recognized contaminants by considering their presence, potential environmental liabilities, and regulatory risks. With growing awareness and the classification of these chemicals as hazardous substances becoming more common, buyers are taking a closer look and may adjust valuations to reflect these concerns.