Published on

January 4, 2026

Expanding globally? Compliance is your first hurdle. Navigating international regulations can feel overwhelming, but it’s non-negotiable for sustainable growth. From tax laws to data privacy, each market brings unique challenges. Missteps are costly - Uber and Lyft paid over $500M in settlements between 2023 and 2024 for compliance failures.

Here’s the solution: Build a scalable compliance system. Key steps include:

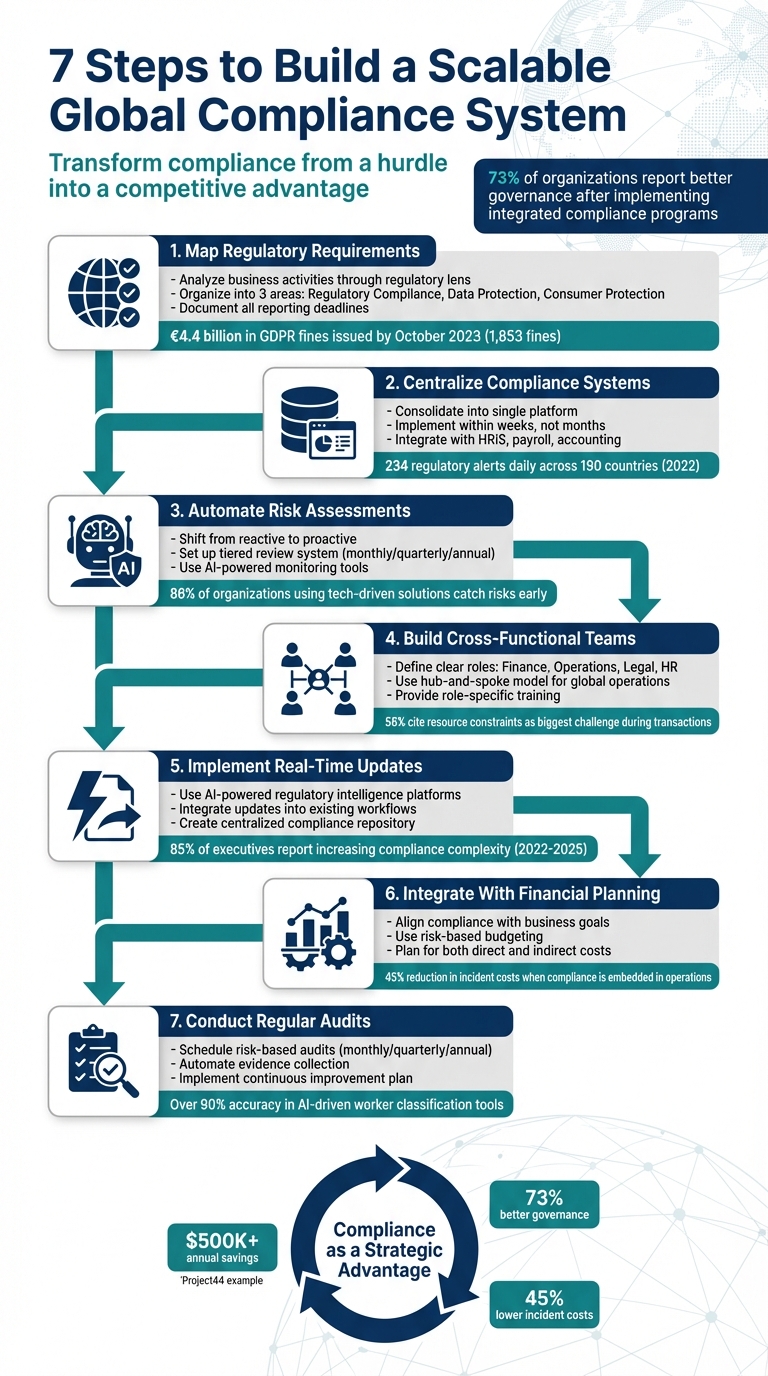

7-Step Framework for Managing Global Compliance in Scaling Businesses

The first step to building a scalable compliance system is figuring out which regulations apply to your business in every market you operate in. This means digging deep to understand the specific rules that impact your operations, industry, and overall business model.

Start by analyzing your business activities through a regulatory lens. Work with legal advisors to translate your business model into regulatory terms. For instance, if your company processes payments, you’ll need to determine whether this requires an Electronic Money Institution license or authorization as a Payment Service Business [7]. Also, keep in mind that operational companies face stricter compliance requirements for production, distribution, and daily operations compared to holding companies [7]. This mapping process lays the groundwork for a structured and organized compliance strategy across multiple markets.

Next, assess the markets you’re currently in or plan to expand into. Are you operating in the U.S., EU, Asia-Pacific, or elsewhere? Identify where you’ll accept payments or serve clients [7]. To simplify this complex process, organize your findings into three key areas: Regulatory Compliance, Data Protection, and Consumer Protection [7]. This structure helps manage the overwhelming number of requirements while ensuring nothing critical is overlooked.

Be sure to document all reporting deadlines, including those for financial statements, tax filings like VAT and GST, payroll, and ESG disclosures [5]. For example, Australia is rolling out climate-related financial risk disclosures for about 1,800 companies starting in 2025 [4]. Meanwhile, GDPR enforcement has been intense - by October 2023, over 1,853 fines had been issued, totaling more than €4.4 billion, with severe violations leading to penalties of up to €20 million or 4% of annual revenue [7]. These examples highlight why precise mapping of requirements is so important.

To keep everything organized, create a central repository. Use tools like dashboards, calendars, or wikis to track country-specific deadlines and formats [5]. This prevents documentation from getting scattered across teams and ensures everyone knows what’s due and when. Pair this with a hub-and-spoke team model: a central team oversees global policies, while local compliance leads - sometimes called "embedded champions" - handle region-specific tasks, such as navigating local filing platforms and language requirements [5]. This setup strikes a balance between global consistency and local expertise.

After identifying your regulatory requirements, the next step is consolidating everything into a single, centralized system. This approach eliminates the chaos of scattered spreadsheets, fragmented email threads, and disconnected tools, which can make tracking compliance nearly unmanageable as your business grows. A centralized platform provides a clear, unified view across all jurisdictions, reduces inconsistencies, and ensures you maintain detailed audit trails [6]. It not only simplifies monitoring but also strengthens your global compliance strategy [6]. This foundational step is crucial for selecting the right compliance software.

The advantages of centralization are immediate and quantifiable. With centralized dashboards, you gain a clear view of potential risks, such as late attestations or expiring certifications, before they escalate into legal issues. For example, in 2022, businesses faced the challenge of managing 61,228 regulatory events across 190 countries, averaging 234 alerts daily [2]. Without a centralized system, staying on top of this overwhelming volume would be nearly impossible.

The software you select should act as your single source of truth for all policies and regulatory requirements [6]. Look for a platform that delivers real-time regulatory updates, covering at least 150 jurisdictions, and provides concise summaries of how changes affect your business [2]. Additionally, it should automatically generate localized documents, such as employment contracts and tax forms, all reviewed by regional legal experts to ensure compliance [2].

Another essential feature is AI-powered risk detection. The software should proactively identify issues like worker misclassification, expiring visas, or violations of minimum wage laws before they grow into significant problems. Seamless integration with your HRIS, payroll, and accounting tools is also a must [6].

When evaluating vendors, prioritize platforms that can be implemented quickly - ideally within weeks rather than months [10]. Begin automating high-risk areas with severe penalties, such as tax withholding, data privacy, and worker classification [6]. For instance, in 2019, BCG streamlined its operations by replacing four different payroll vendors across six countries with a single centralized platform. According to SEA-Payroll Manager Rajes Rajamorganan, this shift allowed employees to access payslips, background checks, and leave applications through one unified interface [2]. Similarly, Project44 reduced costs by approximately $500,000 annually by automating worker classification and addressing misclassification risks, as noted by People Specialist Chloe Riesenberg [2].

Once you've selected your compliance software, the next step is embedding it into daily workflows. Instead of adding extra steps, integrate compliance requirements directly into existing processes. For example, your contract management system should automatically enforce approval workflows, and your expense system should flag policy violations in real time [6].

The goal is to separate the "what" (the regulatory requirements) from the "how" (the workflows), ensuring the requirements remain consistent while allowing workflows to adapt as your organization evolves [6]. Building on the hub-and-spoke model from Step 1, your central team should define global policies, while local teams handle jurisdiction-specific requirements. This ensures global visibility for audits without stifling local operations [3][8].

Standardize data collection by using unified platforms that pull information directly from transaction records, HRIS, or accounting tools [8][9]. Centralized platforms can dramatically reduce manual documentation efforts, turning days of work into just hours, which speeds up onboarding and integration processes [2]. Map out your business processes to pinpoint where compliance checks are needed - whether at the close of a sales deal, during vendor onboarding, or when processing payments - and redesign those touchpoints to include compliance requirements seamlessly [6].

After centralizing your compliance systems, the next step is to shift from reactive to proactive risk management. Why? Because relying on manual tracking just doesn’t work at scale. It often leaves you scrambling to respond to issues instead of preventing them in the first place [6]. That’s where automation steps in - it identifies potential problems in real time, long before they show up in audits [6]. For instance, 86% of organizations using technology-driven risk solutions catch risks early enough to address them effectively [12].

Modern compliance is no walk in the park. Between 2022 and 2025, 85% of business executives reported a sharp rise in compliance complexity [3]. The numbers back this up: in 2022 alone, there were 61,228 regulatory events across 190 countries - an average of 234 alerts every single day [2]. Trying to keep up manually? Nearly impossible. But organizations leveraging technology are 30% more likely to mitigate third-party risks before they escalate [12]. This proactive approach lays the groundwork for more focused and effective risk assessments.

Begin by homing in on your highest-risk areas - those tied to the most severe penalties and the protection of your critical assets [6]. A tiered review system works well here. For example, high-risk areas like anti-corruption, export controls, and worker classification should be reviewed monthly. Medium-risk areas can be assessed quarterly, while low-risk areas may only need an annual review [6][13].

Automation plays a key role in monitoring three crucial triggers: regulatory updates, internal control breakdowns, and looming deadlines [6]. Take Zurich Insurance as an example. Operating in 210 countries with 56,000 employees, they adopted MetricStream BusinessGRC to centralize their compliance data. This move enabled faster responses to regulatory changes through automated, streamlined workflows [11]. Similarly, Guidewire used MetricStream’s platform to better distinguish between risks and issues, speeding up compliance processes and improving visibility for stakeholders [11].

Once your risk priorities are clear, the next step is to integrate continuous monitoring systems for real-time oversight.

Building on your risk assessments, automated tools provide the constant vigilance needed to stay ahead. Continuous Control Monitoring (CCM) systems are particularly effective. They continuously scan for potential issues - whether it’s spotting policy violations in transactions, identifying security risks in access controls, or flagging expiring certifications and visas before they become problems [6][11]. Advanced AI tools take this even further by performing horizon scanning and impact analysis, automatically tracking regulatory changes across hundreds of countries [2][11]. For example, AI-driven worker classification tools now boast over 90% accuracy in categorizing global workforces [2].

Automated notifications are another game-changer. Alerts can be set up for critical events, such as approaching contract renewals, expiring visas, or changes in local labor laws [2]. These real-time updates transform compliance from a periodic task into an ongoing process. The financial benefits are hard to ignore - Project44, for instance, saved about $500,000 annually in 2024 by implementing automated tools for worker classification and compliance. This significantly reduced the workload on their legal team [2]. Platforms like Pathlock specialize in CCM, offering real-time risk assessments across systems like SAP and Oracle, while MetricStream provides AI-powered analytics for continuous monitoring [14].

Automation can help identify risks early, but the real backbone of compliance lies in empowering people with clear roles and responsibilities. While automated systems flag potential issues, skilled cross-functional teams ensure these risks are addressed effectively. Problems arise when compliance functions operate in silos - finance assumes legal is handling regulatory updates, operations expects HR to manage training, and no one takes full ownership. This lack of coordination creates gaps that can lead to regulatory trouble. For instance, 20% of scaling companies face challenges with regulatory compliance during growth, while 56% cite resource constraints as their biggest hurdle during transactions [1].

Compliance isn't confined to one department - it spans across the entire organization. Finance oversees internal controls and disbursements, operations manage day-to-day processes, legal deciphers regulations, and HR leads training initiatives. Without collaboration, critical requirements can be overlooked. Closing these gaps transforms compliance from a burden into a strategic tool that supports better decisions in high-pressure situations [3].

Start by defining clear responsibilities: finance handles internal controls, operations oversees processes, legal interprets policies, and HR manages training [1][6]. For companies operating globally, a hub-and-spoke model works well. A central team can establish policies, while local leads - familiar with regional nuances - ensure compliance on the ground. These local liaisons are essential for spotting issues that a centralized team might miss. For example, Olympus faced $646 million in penalties under the FCPA for failing to monitor overseas operations effectively [16].

Communication is key. Establish dedicated channels, like a compliance committee, to bring stakeholders together regularly, ensure visibility, and align on priorities. To maintain objectivity, your compliance team should operate independently from the business units they oversee, with the authority to address issues without external pressure [10].

Once roles are clearly defined, equip team members with targeted training to reinforce their responsibilities. Tailor the training to specific roles: sales teams should learn about contract compliance and anti-bribery rules, finance teams focus on fraud prevention, managers review approval processes, and front-line staff learn to identify regulatory red flags [6][15].

The U.S. Sentencing Guidelines stress the importance of role-specific training, stating that organizations must "communicate periodically and in a practical manner its standards and procedures... by conducting effective training programs" [15]. Training should be an ongoing effort, not a one-time task. New hires should receive compliance training during onboarding, while existing employees benefit from annual refreshers and updates whenever regulations or internal policies change [1][6][15]. For global teams, offer training in local languages and include region-specific examples, such as South Korea's "Kim Young-ran Act" or Brazil's "Clean Companies Act" [16].

Make the training engaging and practical. Use real-life scenarios and case studies to help employees recognize warning signs and apply their knowledge [10][15]. Consider creating a digital "compliance corner" on your intranet, featuring on-demand training, simplified regulation summaries, and anonymous reporting tools. Focus on explaining the ethical why behind the rules, rather than just the regulatory what, to foster a culture of accountability [3].

| Training Focus | Target Audience | Key Content |

|---|---|---|

| Contract Compliance | Sales & Procurement | Anti-bribery, signature authority, trade terms |

| Fraud Prevention | Finance & Accounting | Disbursement controls, AML, recordkeeping |

| Data Privacy | All Employees (IT/HR focus) | GDPR/LGPD, data handling, breach reporting |

| Regulatory Red Flags | Front-line Operations | Spotting suspicious transactions, boycott requests |

Leverage automated systems to track training completion and policy sign-offs. This documentation can be invaluable during investor due diligence [3][6]. A well-structured team combined with tailored training creates the human framework necessary for scaling compliance effectively.

This approach not only reduces regulatory risks but also aligns with the strategies promoted by Phoenix Strategy Group, helping growth-stage companies scale with confidence and integrity.

To keep up with the constant stream of regulatory changes worldwide, relying solely on even the most skilled team isn't enough. Every day, global regulators issue thousands of alerts [2]. Trying to manually track these updates through government websites, legal bulletins, or industry associations is not just overwhelming - it’s inefficient. By the time you’ve identified a new regulation, analyzed its impact, and adjusted your processes, you might already be out of compliance. This is where technology steps in, transforming compliance from a reactive headache into a proactive advantage.

Regulatory intelligence (RI) platforms are game-changers. These tools, powered by AI, continuously scan global legal frameworks, government bodies, and industry associations to deliver tailored updates straight to your compliance dashboard [17]. Instead of drowning in irrelevant updates, these platforms focus on the specifics of your industry, regions, and operations.

For example:

If your company operates globally, tools like Deel's Compliance Monitor are invaluable. Deel keeps tabs on employment law changes - covering wages, pensions, and leave policies - across 150 countries. It also uses AI-driven worker classification tools with over 90% accuracy [2]. In 2025, North American esports company EEG utilized Deel to onboard 48 team members across 20 countries, cutting what used to take days of manual compliance work down to just a few hours with automated workflows [2].

"Regulatory intelligence is no longer optional - it's a necessity for businesses seeking to thrive in today's complex regulatory environment." - Regology [17]

However, receiving updates is just the first step. The real challenge is embedding these insights into your day-to-day operations.

Alerts alone won’t ensure compliance. The key is incorporating these updates directly into your workflows. Instead of relying on email chains or manually updating policies, integrate compliance rules into the systems you already use. For instance:

Creating a centralized compliance repository can also make a huge difference. By uniting finance, legal, and HR data in one place, you eliminate the visibility gaps caused by scattered spreadsheets and departmental silos [1][3]. Customizable dashboards allow compliance officers to focus on critical updates, avoiding alert fatigue. Meanwhile, trigger-based notifications can automatically inform department heads of relevant regulatory changes, helping them make strategic adjustments before new rules take effect [1][17].

For growing companies, this proactive approach is crucial. Between 2022 and 2025, 85% of business executives reported increasing complexity in compliance requirements [3]. At the same time, 56% of organizations cited resource constraints as their biggest challenge during transactions [1]. Leveraging technology allows small teams to handle global compliance demands without needing to grow their headcount, turning what might seem like a hurdle into a competitive edge. This seamless integration of real-time updates ensures compliance supports, rather than hinders, expansion into new markets. Phoenix Strategy Group specializes in helping growth-stage companies implement scalable compliance systems that align with their global ambitions.

Compliance isn't just about avoiding penalties - it can be a powerful tool for driving value during expansion. Surprisingly, only 16% of companies currently treat compliance as a core, strategic function. Yet, organizations that weave compliance into their daily operations see incident costs drop by 45% [18]. By aligning compliance with your broader business objectives, you set the stage for smoother growth and fewer surprises.

Compliance should be part of the conversation from the very beginning of any strategic planning process. Whether you're gearing up for a product launch or entering a new market, regulatory requirements should be seamlessly integrated into workflows. Tools like automated expense alerts, contract approval triggers, and KYC checks can make this process far less cumbersome.

If you're using a hub-and-spoke model to manage global operations, it’s crucial to balance consistency with local regulatory nuances. Establishing a single source of truth for compliance data can close visibility gaps and streamline decision-making. When critical information - like finance, legal, or HR data - is scattered across spreadsheets, it becomes nearly impossible for leadership to assess risks effectively, especially during investor due diligence. As Jack McCullough, Founder and President of the CFO Leadership Council, explains:

"One of the clearest gaps I notice is between governance and finance systems. Organizations that close this gap gain speed, credibility and control in transactions - advantages that often determine whether a deal creates value or not" [6].

Think of compliance costs as investments in your company’s long-term stability. Planning ahead can help you avoid hefty fines, back taxes, or expensive litigation. However, over half of organizations - 56%, to be exact - cite limited resources as their biggest challenge during transactions [6].

The financial stakes are high. For example, setting up a legal entity in a foreign country can exceed $210,000 per jurisdiction [2]. Yet, smart planning can lead to significant savings. In September 2025, Project44, under the guidance of People Specialist Chloe Riesenberg, saved around $500,000 annually by switching to Deel Contractor of Record. This automated worker classification and compliance across multiple jurisdictions, saving their legal team countless hours [2]. Similarly, SiteMinder managed a workforce of 52 employees across 11 countries by using centralized HR and compliance platforms, delaying the need to establish costly local entities [2].

When building financial forecasts, factor in both direct costs - such as setup fees, legal counsel, and software - and indirect ones, like increased insurance premiums or the need for specialized talent. A risk-based budgeting approach can help you allocate resources to areas with the most significant compliance risks, such as data privacy, anti-money laundering, or payment regulations.

To support these efforts, firms like Phoenix Strategy Group work with growth-stage companies to create financial models that treat compliance as a strategic investment. This ensures that expansion plans include realistic budgets for meeting regulatory requirements in every target market, making compliance a cornerstone of sustainable growth.

Keeping up with compliance requirements has never been more challenging, making regular audits a must [3]. These audits help identify gaps early, ensuring your systems stay aligned with regulatory standards. Think of it as a proactive measure - fixing issues before regulators step in. When paired with centralized and automated compliance systems, audits become a powerful tool to maintain consistent alignment.

Not all risks are created equal, so your audit schedule should reflect that. High-risk areas might need monthly reviews, while medium-risk areas can be checked quarterly, and low-risk zones annually [6]. This risk-based approach ensures your resources are directed to where they’re needed most.

Audits, however, shouldn’t stop at reviewing written policies. They need to dig deeper - verifying that your team is actually following the procedures in place [15]. For global businesses, this means extending audits to your international supply chain, especially sub-suppliers in regions known for labor or trade violations [13][15]. To make this process smoother, consider automating evidence collection. By integrating documentation capture into daily workflows, you’ll have a centralized repository of proof, ready to go whenever auditors need it [6]. The insights gained from these audits should directly inform and improve your compliance processes.

Audit findings shouldn’t just sit on a shelf - they’re your guide to immediate action. Compare your current practices to the required standards [6][19], delegate tasks with clear deadlines, and review outcomes after major audit cycles [3]. After each audit, hold a post-review session to pinpoint what caused delays, what worked well, and where improvements are needed [3]. These insights can help you refine your processes for the future.

Rich Mullen, Partner at Wilson Sonsini, emphasizes the value of these ongoing efforts:

"Companies can do a lot of things day-to-day to improve readiness for a potential transaction, many of which would probably make life easier running the company absent a deal" [6].

Managing global compliance lays the groundwork for steady, long-term growth. As your business expands across borders, compliance transforms into a strategic tool that unlocks market opportunities, earns investor confidence, and protects your reputation. And the data supports this: 73% of organizations report better governance after implementing integrated compliance programs, while 45% see reduced incident costs when compliance becomes part of daily operations [18]. These findings highlight the importance of the seven integrated steps you can use to turn compliance into a competitive advantage.

The steps outlined in this guide function as a cohesive system. Centralized management provides a single source of truth, and when paired with automation, shifts compliance efforts from reactive problem-solving to proactive risk management. By involving cross-functional teams, compliance becomes embedded in every area of the business - whether it’s sales contracts, HR processes, or financial planning - rather than being isolated within a single department.

While technology is essential, it isn’t the sole solution. The best strategies combine automated tools for repetitive tasks with human expertise for more nuanced decisions. For instance, AI tools can classify workers with over 90% accuracy [2] and flag regulatory risks in real time [6][20]. However, these insights still require human interpretation to ensure resources are allocated effectively.

To maintain a strong compliance framework, continuous monitoring and regular audits are crucial. In today’s fast-changing regulatory environment, these aren’t optional - they’re necessary. Strengthening the connection between governance and finance not only speeds up transactions but also enhances your credibility.

Focus on high-priority areas like data privacy, payments, and anti-corruption as a starting point, then scale your systems as your business grows. With the right structure in place, compliance shifts from being a challenge to a competitive advantage - helping your business move faster, build trust, and stay prepared for whatever comes next.

Centralizing compliance management offers businesses a single source of truth for handling regulatory requirements. This not only streamlines processes but also significantly reduces the chance of errors. By bringing together data collection and reporting across different jurisdictions, companies can eliminate manual hand-offs and disjointed systems. The result? Smoother audits, timely filings, and improved oversight.

Another benefit is how it simplifies responding to regulatory changes. Updates can be rolled out globally in a matter of minutes, cutting costs and reducing the risk of penalties. Centralization also boosts transparency and governance - key elements for building investor confidence and easing due diligence during funding rounds or mergers and acquisitions.

For companies in their growth phase, a centralized compliance system lays a scalable foundation for expansion. Entering new markets becomes faster and easier by configuring existing rules, without having to start from scratch. This approach aligns with Phoenix Strategy Group's expertise in helping businesses expand efficiently while maintaining strong compliance systems.

Automation shifts compliance from being a reactive chore to a proactive strategy by keeping a constant eye on transactions, customer data, and regulatory limits in real time. It catches potential problems early, cuts down on manual mistakes, and helps businesses keep up with ever-changing rules across different regions.

By automating time-consuming tasks like regulatory reporting, AML/KYC checks, and tax calculations, finance teams can save a lot of time while ensuring precision. On top of that, automated systems create a centralized hub for compliance data, allowing for consistent controls, quicker risk identification, and effortless audit trails. For growing businesses, this approach not only reduces risks but also enables efficient, scalable operations without piling on extra costs.

Ensuring compliance is woven into your financial planning and everyday operations is a smart move to shield your business from hefty fines and potential legal troubles. It not only promotes accurate financial reporting but also builds confidence among investors and offers a clear framework for managing risks efficiently.

When compliance becomes part of your processes, it lays the groundwork for expanding globally, handling intricate regulations, and achieving steady growth in a competitive landscape.