Published on

January 12, 2026

Without QSBS, founders face a 23.8% federal tax rate on long-term capital gains. For a $10M gain, this could mean $2.38M in taxes. Proper planning ensures you don’t miss out on these tax savings.

Actionable Steps:

Bottom Line: QSBS offers immense tax savings for eligible businesses, but compliance is complex. Early planning and expert advice are essential to secure these benefits.

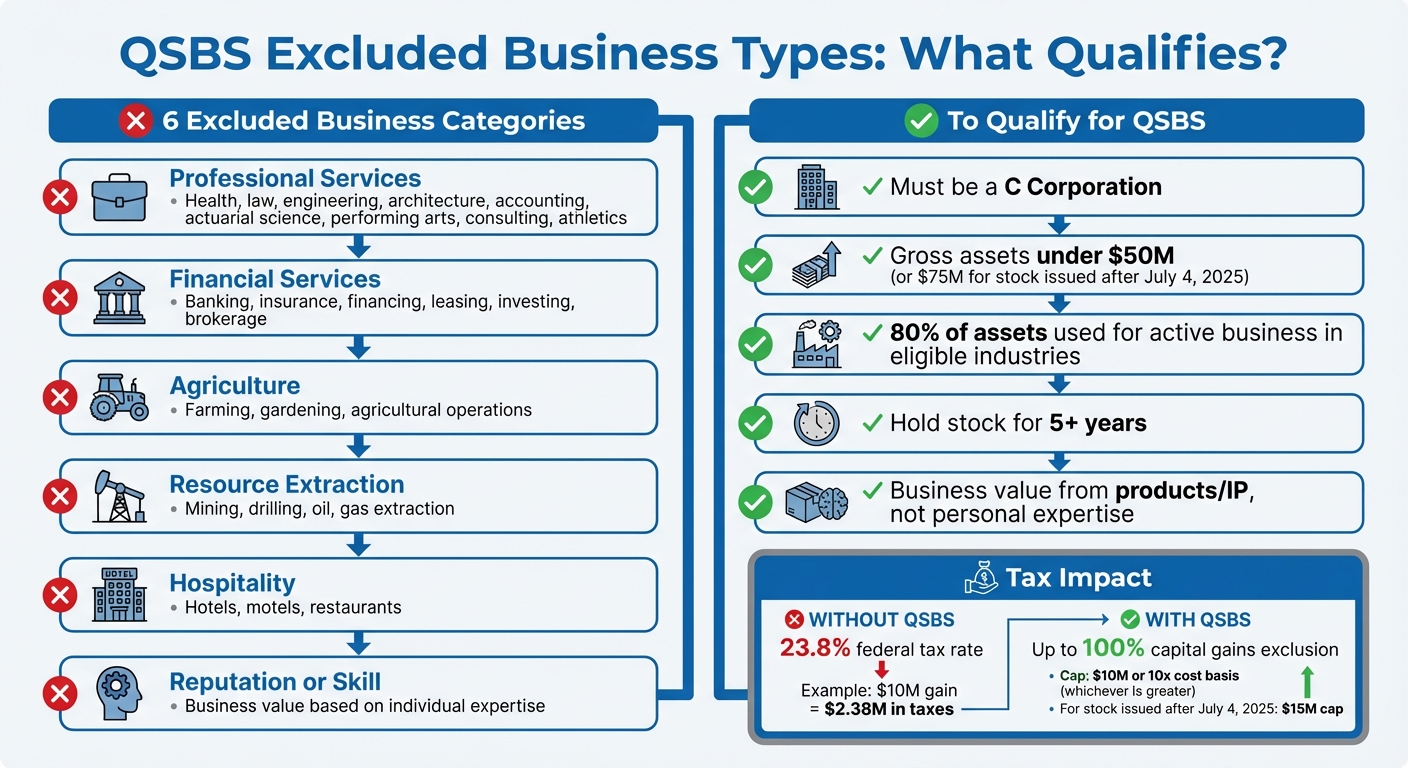

QSBS Excluded Business Types and Qualification Requirements

Under IRS Section 1202(e)(3), certain types of businesses are excluded from claiming Qualified Small Business Stock (QSBS) benefits. These exclusions aim to ensure that the tax advantages apply to growth-focused operating companies rather than service-based or passive businesses. Here are the six main categories that do not qualify:

Understanding these exclusions is essential because they directly impact your ability to claim QSBS tax benefits.

QSBS eligibility hinges on whether your company's value stems from tangible products or intellectual property rather than personal expertise. For instance, a robotics company that designs and manufactures automated machinery qualifies, as its value is tied to its products and intellectual property. On the other hand, a consulting firm advising clients on how to use those machines does not qualify, as its value is based on expertise rather than scalable assets [2].

"The distinction is between developing or producing technology (eligible) versus delivering health services (ineligible)."

– Brady Weller [2]

Additionally, your company must devote at least 80% of its assets to active business operations. A shift toward non-qualifying activities or excessive passive investments could result in losing QSBS status [10] [12] [1] [4]. For example, if more than 10% of your company's net assets are in passive investments or over 10% of its gross assets consist of idle real property, it fails the active business test [7].

If your business falls into one of the excluded categories, you lose access to the substantial QSBS tax benefits. For stock acquired after September 27, 2010, eligible founders can exclude up to 100% of capital gains - capped at $10 million or 10 times the cost basis - from federal income tax [7] [9]. This translates to federal tax savings of up to 23.8% [7].

Without QSBS protection, founders are subject to the standard 20% long-term capital gains tax rate, plus the 3.8% Net Investment Income Tax. On a $10 million gain, this amounts to about $2.38 million in federal taxes, excluding any state taxes.

Misclassifying your business type can also increase audit risks. The IRS closely examines QSBS claims, particularly for companies operating in industries near the excluded categories. For example, healthcare technology businesses must clearly differentiate between developing medical devices (which qualify) and delivering patient care services (which do not) [2]. Errors in classification can lead to penalties, interest, and the loss of QSBS benefits.

The "reputation or skill" exclusion is another tricky area. Even if your business doesn’t fall into one of the explicitly excluded categories, the IRS may still disqualify it if its value is primarily based on individual expertise rather than scalable systems or products [6] [8]. This broad provision requires ongoing attention as your business evolves to ensure compliance.

Not all startup equity qualifies for QSBS (Qualified Small Business Stock) benefits. To meet the criteria, your company must be a domestic C corporation that adheres to strict asset tests and operates outside certain excluded industries [1][4]. Clearing up common misconceptions is essential when structuring your business to comply with QSBS requirements.

One frequent misunderstanding involves the holding period. Many founders mistakenly think the five-year clock starts when they receive an option grant or sign a SAFE note. In reality, the holding period only begins once you exercise those options or the note converts into actual stock [4][11]. As Chad D. Cummings, CPA, Esq., explains:

"Investors who rely on early note or SAFE dates for the holding requirement often miscalculate and sell prematurely, forfeiting the exclusion" [4].

This misstep - relying on early note or SAFE dates - can lead to premature sales and the loss of QSBS tax benefits [4][11].

Another risky myth is assuming that minimal consulting activities won’t affect your QSBS status. If excluded activities exceed 20% of your business’s value, your company could lose its eligibility [10]. The problem is compounded by the lack of a clear IRS definition for "consulting services", making it especially tricky for companies operating in ambiguous areas [10].

The risks multiply when a business combines qualifying and non-qualifying activities. While it’s possible to maintain QSBS eligibility with a mix of both, at least 80% of your company’s assets by value must be tied to qualified trades or businesses [1][3][4].

The distinction often hinges on how your business delivers value. Companies that provide tangible products or software (qualified activities) are typically eligible, while those relying heavily on individual expertise or services (excluded activities) are not [2][13]. For instance, a SaaS company generating revenue through subscription fees would qualify. On the other hand, an AI firm focused primarily on advisory work or custom consulting services might not. Similarly, a robotics startup manufacturing automated sorting machines would qualify, but a consulting firm helping clients optimize robotic workflows likely wouldn’t.

Tech companies with "software plus services" models are particularly vulnerable. If consulting becomes a significant portion of your revenue or operations, you risk crossing the 20% threshold and losing QSBS eligibility over time [4]. To avoid this, it’s essential to monitor your revenue streams and asset allocation closely. Regularly reviewing financial records and ensuring assets are tied to qualified activities can also be crucial, especially if your company faces an IRS audit [4].

If your business involves a mix of activities, you might still qualify for QSBS benefits. The secret lies in understanding your current standing and taking the right steps to ensure your company aligns with the rules.

Start by reviewing IRS Section 1202(e)(3) to identify any disqualified business types. Then, apply the 80% active business test. This test requires that at least 80% of your company’s assets by value are used in the active conduct of a qualified trade or business during most of your holding period [15]. Tax professionals generally interpret “substantially all” to mean between 80% and 95% of the total holding period [15].

Next, confirm your gross asset limit: $50 million for stock issued before July 4, 2025, and $75 million for stock issued afterward [14]. It’s critical to document these figures using third-party valuations and detailed financial records. This documentation will be essential if the IRS audits your QSBS claim.

Consider working with a tax advisor or fractional CFO to secure an annual QSBS attestation letter. This letter serves as a clear record of your company’s qualified small business status, providing reassurance for both investors and the IRS [1]. As Chad D. Cummings, CPA, Esq., explains:

"The rules are exceptionally technical, and seemingly minor operational or transactional decisions can inadvertently eliminate eligibility" [4].

These steps set the stage for restructuring strategies that can help protect your QSBS benefits.

Once you’ve confirmed your eligibility, you might need to explore restructuring strategies to separate qualified activities from excluded ones. This is especially important if your business mixes activities that could jeopardize your QSBS status.

One option is a Type D divisive reorganization. This approach splits your corporation into two entities - one focused on qualified activities (like software development) and the other on excluded activities (such as consulting services). In a 1998 Private Letter Ruling (9810010), the IRS ruled that stock in these resulting entities could still qualify as QSBS, provided each entity meets the gross assets test independently [16].

Alternatively, you can modify your business operations. For example, shifting from a service-based model to one centered on product delivery can help maintain QSBS eligibility. A biotech company might prioritize drug development over patient care, or a robotics company might focus on selling hardware instead of consulting on workflows [2].

If your business has subsidiaries, retaining more than 50% ownership can enable "look‐through" treatment. This means a subsidiary’s assets can be proportionally counted toward the active business test [15].

Navigating these complexities requires expert guidance, and that’s where Phoenix Strategy Group stands out. Their Fractional CFO and FP&A services help founders stay QSBS-compliant from the start, focusing on the 80% active business test and gross asset thresholds tied to your stock issuance date. They also handle contemporaneous valuations and detailed documentation, ensuring your QSBS status holds up during audits.

When it’s time to plan an exit, Phoenix Strategy Group’s M&A advisory services can optimize your tax benefits. They can guide you on strategies like gifting QSBS to family members or trusts to spread the $15 million exclusion cap across multiple taxpayers [5]. They also help with Section 1045 rollovers, which let you defer gains by reinvesting proceeds into new QSBS within 60 days if you need to sell before the five-year holding period [1].

For businesses with complex models, like those combining software and services, Phoenix Strategy Group provides real-time data tracking to monitor revenue and asset allocation. This is crucial for identifying and addressing compliance risks before they threaten your QSBS eligibility. Their expertise helps you strategically separate qualified and excluded activities, safeguarding your benefits every step of the way.

The Qualified Small Business Stock (QSBS) exclusion isn't just a tax planning tool - it’s a way to secure major tax savings. For shares issued on or after July 4, 2025, investors can exclude up to $15 million (or 10 times their cost basis) from federal capital gains taxes [1].

But here’s the catch: there’s no room for error. As Peyton Carr, Co-Founder of Keystone Global Partners, emphasizes:

"Small technical details often determine eligibility, and retrospective qualification is impossible if conditions weren't properly established at issuance" [11].

For instance, if your company transitions from selling software products to offering consulting services, or if it surpasses the $75 million gross asset limit during a funding round, your shares could lose their QSBS eligibility permanently [1].

To avoid surprises, it’s critical to confirm your compliance now. Start by checking your company’s C-corporation status, ensuring at least 80% of assets are tied to qualifying activities, and keeping a close eye on your financials to avoid disqualification [1]. Share repurchases, even small ones, can also jeopardize eligibility, so they need to be tracked carefully [7]. Additionally, certain states, including California, Pennsylvania, and Alabama, do not honor the federal QSBS exclusion, which could impact your tax planning [11].

Given the complexity of Section 1202, expert guidance is essential. Firms like Phoenix Strategy Group offer Fractional CFO services to help monitor compliance, track asset thresholds, and document business activities. Their M&A advisory team can also assist in structuring transactions - whether through Section 1045 rollovers or timing your holding period strategically - to preserve your tax benefits [1][8].

Don’t wait. Taking the right steps now can safeguard millions in potential tax savings.

To qualify for QSBS, your business must be structured as a U.S. C‑corporation. The company's gross assets need to stay under $50 million both before and immediately after the stock is issued. Additionally, at least 80% of the company's assets must be actively engaged in a qualified trade or business - excluding industries such as financial services, hospitality, or those generating passive income. The stock must be issued directly to the original holder and retained for a minimum of five years. Maintaining thorough records of stock issuance dates and how assets are used is crucial for meeting these requirements and simplifying the qualification process.

The IRS relies on IRC §1202(e)(3) to identify businesses that are not eligible for QSBS (Qualified Small Business Stock) benefits. In general, a domestic C-corporation won’t qualify if its primary trade or business falls into certain excluded categories. These include industries such as health services, law, accounting, engineering, financial or investment activities, farming, oil and gas, hospitality, passive investments, personal-service firms, and specific types of real estate operations.

If your business operates in one of these restricted sectors, its stock won't qualify for QSBS benefits. For founders, it’s essential to grasp these rules when structuring your company or planning future exits.

If your business currently engages in a mix of qualifying and non-qualifying activities, restructuring could open the door to QSBS benefits. By isolating the qualifying operations and converting your business into a C-corporation, strategies like reorganizations, conversions, or recapitalizations can help you meet the active-business and asset-use criteria.

Careful planning is key when restructuring to minimize or eliminate non-qualifying activities. Working with professionals who specialize in QSBS rules can ensure your business is set up to maximize these potential advantages.