Published on

January 4, 2026

Stablecoins are reshaping financial systems by offering a faster, cost-effective alternative to outdated banking processes. These digital currencies, pegged to fiat assets like the U.S. dollar, enable instant, 24/7 transactions, reducing fees and delays common in traditional systems like SWIFT or ACH. By June 2025, the stablecoin market reached $255 billion, with transaction volumes far surpassing those of Visa.

Key Benefits of Stablecoins:

Integration involves APIs, payment hubs, and ERP systems to connect stablecoins with existing financial tools. Businesses like SpaceX and Stripe already use stablecoins for treasury management and payments, citing reduced costs and improved efficiency. Regulatory clarity, such as the 2025 GENIUS Act, ensures stablecoin issuers maintain 1:1 reserves, making them a reliable option for businesses.

Stablecoins are transforming financial operations by bridging blockchain and banking, offering speed, security, and cost savings.

Traditional payment systems often rely on multiple intermediaries, which leads to added fees and delays [5]. Stablecoins simplify the process by enabling direct transactions on blockchain networks. What used to take days with traditional B2B payments can now be completed in mere minutes using stablecoins [5][7].

Take this example: Sending $200 from the U.S. to Colombia typically costs around $12.13 through traditional methods, but with stablecoins, the cost drops to just $0.01 [5]. Similarly, transferring $1,000 from Mexico to Vietnam can cost anywhere from $14 to $150 using traditional systems, while stablecoins make such transactions almost free [5]. In 2025, Stripe became the first major payment processor to offer stablecoin checkouts at a 1.5% fee, which is about half the rate charged by traditional credit card networks [5].

"Stablecoins are 'room-temperature superconductors for financial services,' where rather than lossless energy transmission, you get lossless value transmission." - Stripe [5]

Interestingly, businesses handling over $1 million in monthly cross-border payments are 92% more likely to adopt stablecoins compared to smaller companies [6]. SpaceX, for instance, uses stablecoins to manage its corporate treasury, particularly for repatriating funds from countries with volatile currencies like Argentina and Nigeria [5]. Moreover, the ability to operate 24/7/365, without being restricted by banking hours or batch processing schedules, gives businesses unmatched flexibility in managing cash flow and supplier payments [4][7].

This combination of speed and cost efficiency also lays the groundwork for improved transparency in digital transactions.

Blockchain technology ensures every stablecoin transaction is recorded permanently, creating a transparent and unchangeable audit trail that traditional systems can't replicate. Once a stablecoin transaction is settled, it’s final, eliminating the risk of chargebacks or settlement recalls that are common with card and wire networks [2]. This finality provides businesses with the assurance that payments won’t be reversed days or weeks later.

Regulated stablecoin issuers further enhance transparency by undergoing regular third-party audits or attestations of their reserves. This level of clarity is often missing in traditional banking systems [2][4]. For example, in June 2025, Circle, the issuer of USDC, applied for a national trust bank charter with the OCC to launch the "First National Digital Currency Bank, N.A." This move allows Circle to directly oversee $62 billion in reserves, ensuring 1:1 backing as required by the GENIUS Act, while providing complete transparency without relying on external custodians [4].

Modern stablecoin frameworks also integrate advanced technologies like Zero-Knowledge Proofs (ZKPs). These allow verification of compliance with KYC/AML requirements without exposing personal data [9]. This "compliance-by-design" approach enables real-time, on-chain monitoring via smart contracts, which can detect suspicious activities and generate instant reports - replacing the slow, manual processes of traditional systems [9].

"The stablecoin payment system... replaces time-consuming 'off-chain' manual reactive reviews - common practice today - with proactive real-time 'on-chain' algorithmic supervision." - Darrell Duffie, Professor of Management and Finance, Stanford University [9]

This secure and transparent foundation naturally supports automation through smart contracts.

Stablecoins bring programmability to transactions through smart contracts, ensuring funds are used exactly as intended [10]. These contracts can automate compliance checks, screening payments for AML and KYC issues, cross-referencing sanctioned entities via on-chain analytics, and executing instructions automatically [10][11].

The automation extends beyond compliance. Smart contracts streamline complex financial processes, such as atomic swaps and automated reconciliation. For instance, payments can be released only when specific conditions, like on-chain shipping confirmation, are met - minimizing manual errors and oversight [8].

"The logic of tokenization rests on a deceptively simple idea: take assets that today are trapped in fragmented, permissioned, and often outdated infrastructure, and move them onto programmable, global settlement rails." - Rebank [8]

This programmability is already being adopted by major asset managers. Franklin Templeton’s OnChain U.S. Government Money Fund (BENJI) reached $750 million in assets under management by late 2025, utilizing public blockchains like Stellar, Ethereum, and Solana for tokenized shares [8]. Similarly, BlackRock's BUIDL fund, launched in 2024 on the Ethereum network, attracted $500 million in assets within months, proving that institutional-grade fund shares can be tokenized and traded seamlessly [8].

These advancements highlight how stablecoins are not just transforming speed and security but also driving operational efficiency in today's financial systems.

Stablecoins are transforming the way businesses handle payments, and integrating them effectively can unlock a host of benefits. Let’s explore some practical methods to make stablecoin adoption smoother.

APIs simplify the process of incorporating stablecoins by taking care of the behind-the-scenes blockchain operations. Instead of worrying about transaction signing, gas fees, or network execution, you can use APIs to link your current payment systems directly to stablecoin wallets.

One effective approach is virtual account generation. APIs can create local routing details - such as IBANs, sort codes, or ACH numbers - that act as a bridge between fiat and blockchain. When fiat currency is sent to these virtual accounts, the API converts it into stablecoins like USDC and deposits it into your business wallet. For example, in November 2025, the self-custodial wallet Ready adopted Due's fiat-to-stablecoin API, enabling users across 150+ countries to access stablecoins. Due’s API supports currencies like EUR, MXN, and BRL, converting local transfers into USDC with FX spreads of 0.2–0.7% and settling transactions instantly on-chain, bypassing centralized exchanges [15].

APIs often include webhooks for reconciliation, which notify your ERP system in real time when transactions occur - like when a transfer is received or USDC is credited. This eliminates the need for manual ledger updates and ensures your accounting stays in sync with blockchain activity. Plus, you can maintain full control of private keys through self-custodial wallets while leveraging the API provider’s infrastructure for technical tasks.

"The fiat-to-crypto on-ramp API isn't a feature anymore; it's table stakes."

- Due Team [15]

These API-driven solutions lay the groundwork for more centralized integration methods.

Payment hubs offer a centralized solution to connect traditional payment systems with blockchain networks. They handle fiat-to-stablecoin conversions, manage cross-chain transactions, and ensure funds reach their destination - whether the recipient uses blockchain or conventional banking.

A popular method here is the hybrid conversion model, often called the "stablecoin sandwich." In this setup, your business sends fiat to the hub, which converts it into stablecoins for quick on-chain settlement. The stablecoins are then converted back to fiat for the recipient. For instance, Deel partnered with BVNK in Spring 2024 to enable stablecoin payouts for contractors. By funding accounts in USD, EUR, or GBP and using auto-conversion, Deel facilitated over 10,000 contractors in 100+ countries to receive wages in USDC. This reduced settlement times from 3–5 days to near-instant, resulting in 125,000 successful payouts by mid-2025 [14].

Payment hubs also operate round the clock, eliminating delays caused by banking holidays or cut-off times. Their cross-border transaction fees range from 0.2% to 0.3%, a fraction of the 4–6% charged by traditional card networks [7][18][15].

Integrating stablecoins with ERP platforms like NetSuite or SAP allows businesses to map blockchain activities directly to their internal accounting systems. For instance, SAP's Digital Currency Hub connects ERP systems to blockchain payment rails, enabling treasury teams to manage stablecoin transactions without disrupting their existing workflows [12].

A critical feature here is automatic transaction categorization. By assigning unique wallet addresses to each customer, region, or revenue stream, you can automate transaction tracking and categorization. Unified dashboards provide a clear view of multi-chain funds, including details like vault balances and sub-wallet breakdowns.

For added security and governance, use policy-based approval flows with Multi-Party Computation (MPC) wallets. These systems allow businesses to set multi-tier approval requirements - for example, needing both CFO and COO approval for transfers exceeding $100,000 [16]. Real-time reconciliation tools further streamline operations by mapping on-chain transactions to internal ledgers. These tools use metadata and internal memos to ensure a 1:1 match with bank statements [16][17]. This kind of automation can save significant time and money, as a typical 1,000-person company spends around 100,000 hours annually on reconciliation tasks, costing $3–5 million in labor [16].

"Solutions like SAP's Digital Currency Hub bridge the gap between the core ERP and blockchain-based payment rails, so Treasury teams don't have to leave their existing payments ecosystem."

- Charles Brough, SAP Taulia [12]

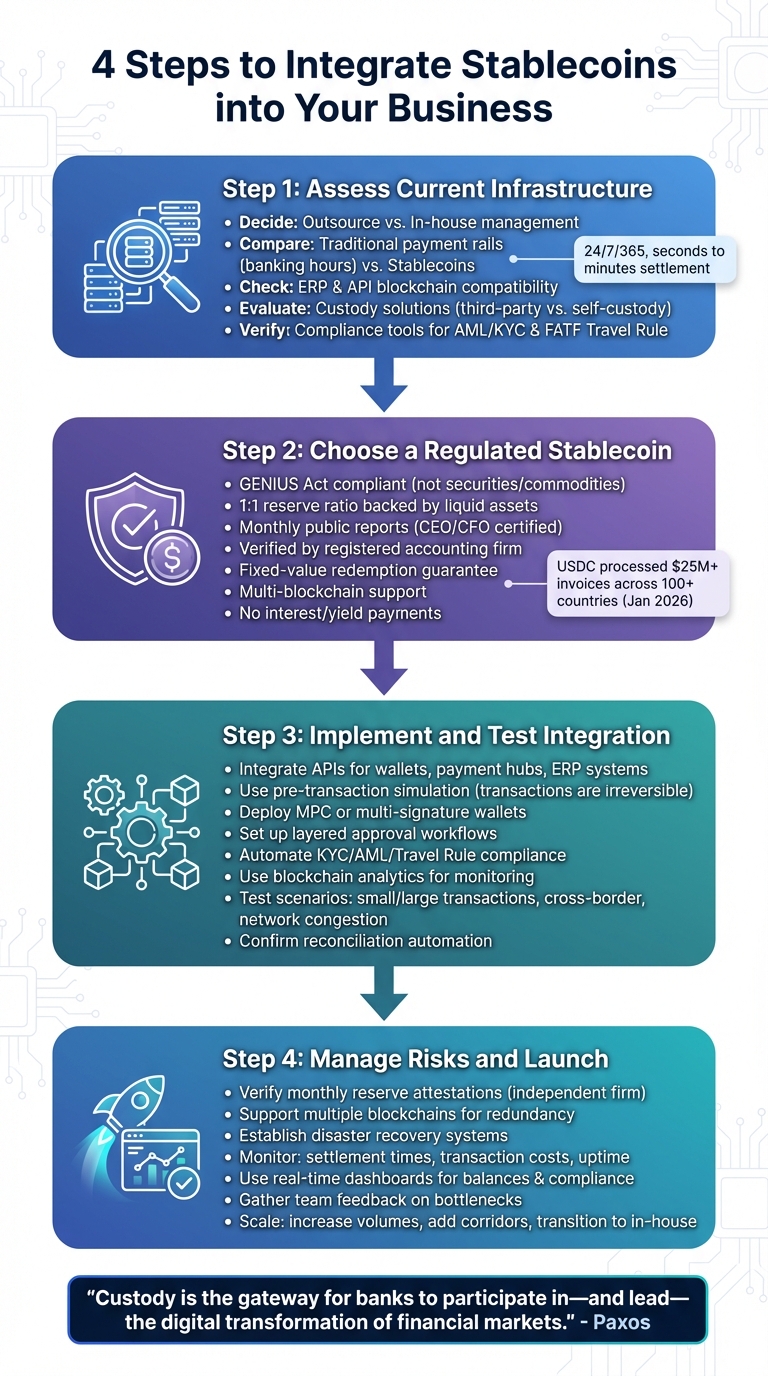

4-Step Process for Integrating Stablecoins into Business Operations

Start by evaluating your existing setup. Decide whether you’ll outsource operations - working with third-party providers to manage blockchain transactions - or handle everything in-house, including custody, execution, and treasury management. Outsourcing can get you up and running faster, but an in-house approach gives you more control as your expertise grows [17].

Next, compare your current payment systems to stablecoins. Unlike traditional payment rails that operate only during banking hours, stablecoins settle transactions in seconds or minutes and are available 24/7/365 [17][19]. Check if your ERP and API systems can connect to blockchain for seamless reconciliation [17]. Decide whether to use regulated third-party custody solutions or manage your own keys with internal infrastructure. Make sure your compliance tools can handle wallet monitoring, AML/KYC processes, and the FATF Travel Rule requirements for digital assets [17][1].

Once your infrastructure is ready, the next step is selecting a regulated stablecoin.

The GENIUS Act (passed in July 2025) clarified that U.S. payment stablecoins are not classified as securities or commodities [21]. Focus on stablecoins issued by authorized entities like bank subsidiaries, federally approved non-banks with OCC charters, or state-chartered issuers operating under federal-equivalent standards [21][20].

Look for issuers maintaining a 1:1 reserve ratio backed by high-quality liquid assets such as U.S. currency, insured deposits, or short-term U.S. Treasury securities (maturing in 93 days or less) [20]. Ensure they provide monthly public reports on reserve compositions, certified by their CEO and CFO, and verified by a registered public accounting firm [21][20]. For example, in January 2026, Acctual used USDC to process over $25 million in invoices across 100+ countries at low costs and high speed [19].

Confirm that the issuer guarantees stablecoin redemption at a fixed value and that reserves are held in segregated, bankruptcy-remote accounts [20][17]. Choose stablecoins operating on multiple blockchains to avoid vendor lock-in and ensure sufficient liquidity [19][17]. Note that under the GENIUS Act and MiCAR, regulated issuers cannot pay interest or yield on stablecoin holdings [20][1].

Once you’ve selected the right stablecoin, it’s time to integrate and test it.

Integrate the stablecoin using APIs for wallets, payment hubs, and ERP systems. Before going live, simulate transactions to ensure everything works as expected. Since blockchain transactions are irreversible, use pre-transaction simulation tools to avoid errors [2]. Strengthen security by adopting Multi-Party Computation (MPC) or multi-signature wallets to prevent single points of failure in private key management [13][2]. Set up layered approval workflows to improve oversight and governance [2].

Automate compliance by embedding KYC, AML, and Travel Rule data collection into your processes [2]. Use blockchain analytics tools to track wallet activity and flag sanctions or suspicious behavior [2]. Test various scenarios, including small and large transactions, cross-border payments, and network congestion, to ensure your system is robust. Additionally, confirm that reconciliation tools can automatically align on-chain transactions with your internal ledgers.

Finalize your risk management strategies. Verify monthly reserve attestations with an independent accounting firm [3][20]. Support multiple blockchains to balance speed, cost, and reliability across different regions [2], and establish redundant systems for disaster recovery [13][2].

Once live, monitor key metrics like settlement times, transaction costs, and system uptime. Use real-time dashboards for wallet balances, transaction flows, and compliance alerts. Gather input from treasury and finance teams to identify and address operational bottlenecks. As your confidence grows, scale up by increasing transaction volumes, adding new payment corridors, or transitioning from outsourced to in-house management [17].

"Custody is the gateway for banks to participate in - and lead - the digital transformation of financial markets."

The GENIUS Act, signed into law on June 18, 2025, classifies permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act (BSA) [22]. For businesses adopting stablecoins, this means implementing a comprehensive anti-money laundering (AML) program, conducting regular risk assessments, and designating a compliance officer [22]. These requirements are designed to ensure stablecoin adoption aligns with strict regulatory standards.

To meet compliance obligations, businesses must establish a Customer Identification Program (CIP) to verify account holders, especially for higher-value transactions [22]. For accounts or transactions identified as higher risk, applying Enhanced Due Diligence (EDD) measures is crucial [22].

Sanctions compliance is another critical area. Businesses need a program that checks customers against sanctions lists and has the tools to block, freeze, or reject prohibited transactions [22]. Additionally, maintaining detailed records of customer identification and transactions is essential to fulfill retention requirements [22]. Partnering with regulated issuers and utilizing institutional-grade custody solutions can help minimize compliance risks [23].

Automated tools play a key role in monitoring transactions, identifying unusual activity, and maintaining clear audit trails. Multi-signature wallets can further enhance transparency [23]. The industry is moving toward "radical transparency", with near real-time attestations by auditors and cryptographic proof of reserves becoming more common [25].

To manage risks effectively, set up systems to monitor liquidity buffers and concentration risks. These systems should also address potential information gaps associated with blockchain-based assets [25]. If stablecoins operate across multiple blockchains, your monitoring infrastructure must be capable of tracking cross-chain activity [25].

The GENIUS Act mandates that stablecoin issuers maintain liquid reserves at a 1:1 ratio to issued coins. These reserves must consist of U.S. currency, insured deposits, or Treasury securities maturing within 93 days [20][22]. Issuers are required to publish monthly reserve composition reports on their websites. These reports must be certified by the CEO and CFO and reviewed by a registered public accounting firm [20][22].

"By 2026, regulatory clarity and supervisory posture - not raw technical innovation - will be the main determinants of which stablecoins scale."

- Ram Rastogi, Digital Payments Expert [25]

Issuers approved at the state level with more than $10 billion in total issuance must transition to federal supervision within one year [20][22]. Those exceeding $50 billion are required to prepare annual audited financial statements [20]. Additionally, the GENIUS Act prohibits stablecoin issuers from offering interest or yield to holders [20][22]. Businesses should test their compliance systems through pilot projects and consult legal experts to stay ahead of evolving regulations, including the upcoming California Digital Financial Assets Law, which takes effect on July 1, 2026 [23][24].

The stablecoin market reached a staggering $300 billion in value by September 2025, with transaction volumes hitting $23 trillion in 2024. These numbers highlight a major shift in how cross-border payments, treasury operations, and supplier settlements are conducted [27][26][10].

Successfully integrating stablecoins into business operations demands careful planning and thorough testing. Companies need to evaluate their existing infrastructure, choose regulated stablecoins with verified reserve backing, and deploy secure custody solutions like multi-signature wallets or multi-party computation (MPC) technology [13][2]. Since stablecoin transactions are irreversible, conducting pre-transaction checks is crucial to avoid costly mistakes [2]. A well-executed integration not only minimizes risks but also transforms outdated financial systems into modern, efficient operations.

"Stablecoins are not just a peripheral option for banks, but have become a crucial strategic necessity." - Crypto.com Research [4]

As discussed earlier, strong AML/KYC and monitoring systems are non-negotiable. Navigating regulations such as the U.S. GENIUS Act and the EU's MiCA requires specialized knowledge. Businesses must implement detailed compliance programs, maintain robust transaction monitoring, and ensure their systems can adapt to ever-changing regulatory landscapes.

Given the complexities involved, expert guidance can be invaluable. Phoenix Strategy Group provides specialized advisory services to help businesses manage financial transformations and integrate digital assets. With expertise spanning fractional CFO services, FP&A systems, and data engineering, Phoenix Strategy Group can assist in evaluating stablecoin applications, building secure infrastructures, and ensuring compliance. Whether you're handling cross-border payments, upgrading treasury operations, or preparing for institutional digital asset adoption, their support can mean the difference between a seamless transition and costly errors. Visit Phoenix Strategy Group to explore tailored financial solutions for your stablecoin integration journey.

Stablecoins significantly reduce the costs associated with cross-border payments by removing the need for multiple intermediaries, like correspondent banks. Instead of relying on traditional systems, transactions occur directly on blockchain networks, which come with much lower fees.

Beyond cutting costs, this approach also speeds up settlement times. The result? A faster, more efficient way to handle global transactions compared to conventional methods.

Businesses in the United States exploring stablecoins must carefully address a range of regulatory requirements to stay compliant. Issuers are generally required to secure the necessary licenses, ensure reserves are entirely backed by cash or high-quality liquid assets, and maintain these reserves in separate, auditable accounts. On top of that, they must establish strong anti-money laundering (AML) and Know-Your-Customer (KYC) protocols, as mandated by the Bank Secrecy Act.

Consumer protection is another key focus for regulators. This includes providing clear information about redemption rights and potential solvency risks, along with implementing safeguards like stress-testing and robust cybersecurity measures. Companies are also expected to follow global best practices, such as conducting regular audits and adhering to interoperability standards. Due to the intricate nature of these requirements, many businesses turn to experts for help in adapting their financial operations to meet these shifting regulations.

Phoenix Strategy Group steps in to assist growth-stage companies by creating compliant workflows, overseeing treasury operations, and preparing the necessary documentation for smooth stablecoin integration.

Stablecoins function on public blockchains, where every transaction is permanently recorded on a time-stamped ledger. This transparent system enables businesses to establish real-time audit trails while giving regulators direct access to transaction data. By reducing the need for opaque intermediaries, stablecoins make it easier to monitor asset pricing and liquidity, providing companies with a clear, up-to-date snapshot of their financial standing.

When it comes to security, stablecoins are safeguarded by cryptographic keys, ensuring that only individuals with the private key can access the funds. To prevent unauthorized access, companies must adopt robust custody measures, such as multi-signature controls and effective key management systems. By pairing these cryptographic protections with transparent, auditable transaction records, stablecoins offer a stronger defense against fraud and bolster operational resilience for businesses.