Published on

December 9, 2025

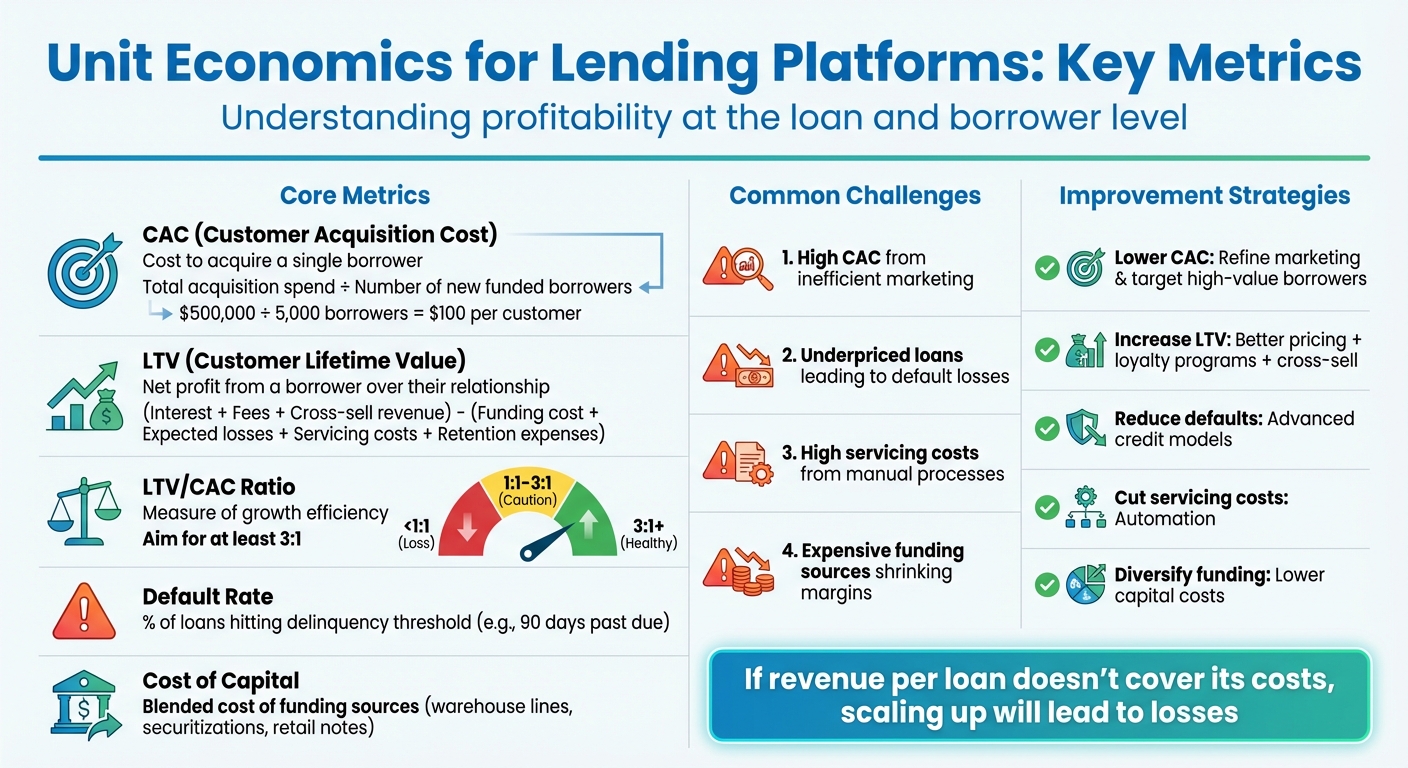

Unit economics breaks down the profitability of each loan or borrower, focusing on revenue sources (like interest and fees) and costs (such as defaults, funding, and customer acquisition). For lending platforms, understanding these metrics ensures growth is profitable, not a drain on resources. Here’s the key takeaway: If revenue per loan doesn’t cover its costs, scaling up will lead to losses.

Bottom Line: Strong unit economics drive profitable growth. Focus on key metrics, address inefficiencies, and monitor data in real time to stay ahead.

Key Unit Economics Metrics for Lending Platforms

Core metrics help determine whether each loan or borrower contributes positively to a lender's bottom line. These metrics provide a practical way to evaluate the performance and profitability of individual lending units.

CAC is calculated by dividing the total acquisition spend by the number of new funded borrowers during a specific period [2][5][7]. This includes all expenses tied directly to acquiring new customers, such as:

However, it excludes broader costs like general branding efforts, public relations, or fixed overhead (e.g., long-term marketing leadership salaries) that don't scale with customer volume.

For instance, if a lender spends $500,000 in a quarter on performance marketing, referral bonuses, and onboarding verification to acquire 5,000 borrowers, the CAC would be $500,000 ÷ 5,000, or $100 per customer. Breaking down CAC by channel - like search versus affiliate marketing - can help shift resources toward the most cost-efficient channels without compromising credit quality.

LTV represents the net profit a lender expects to earn from a customer over the entire duration of their credit relationship [3][6]. It includes:

Revenue sources:

Costs:

The formula for LTV is:

LTV = (Total expected interest + fees + cross-sell revenue) – (funding cost + expected losses + servicing costs + retention expenses)

Failing to factor in defaults or servicing costs can lead to overestimating LTV, giving the false impression that certain customer segments are profitable when they are not.

The LTV/CAC ratio measures how efficiently a lender turns customer acquisition investments into profit. A ratio below 1:1 means the lender loses money on each customer before considering fixed costs, while a target of at least 3:1 is often considered healthy. If the ratio falls short, lenders might need to revisit pricing, risk management, or retention strategies before scaling marketing efforts. This metric is a key indicator for investors and credit providers to assess whether a lender's growth is both efficient and sustainable.

Default rate tracks the percentage of loans or borrowers that hit a specific delinquency threshold, such as being 90 days past due or reaching charge-off status [3][6].

Loss rate, on the other hand, measures the dollar amount of unrecovered principal (and sometimes accrued interest) as a percentage of the original loan balance. While the default rate reflects how often loans fail, the loss rate highlights the financial severity of those failures after recoveries. Together, these metrics are critical for evaluating underwriting quality, risk segmentation, and their impact on profitability.

Cost of servicing refers to the operational expenses tied to managing loans, calculated per active account, loan, or outstanding balance [3]. It includes:

Lenders often reduce servicing costs through automation, self-service tools, and streamlined early-stage collections.

Cost of capital is the blended cost of a lender's funding sources, such as warehouse lines, securitizations, or retail notes. Monitoring this cost ensures that the average annual percentage rate (APR) covers both the risk-adjusted yield requirements and operating margins. Since it directly impacts net margins and overall profitability, keeping a close eye on the cost of capital is essential for long-term success.

Even with clear profitability benchmarks from core unit metrics, platforms often face obstacles that make hitting those targets difficult. These challenges generally fall into four main areas, each affecting the key metrics previously discussed.

Spending too much on digital ads or running inefficient marketing campaigns can push customer acquisition costs (CAC) to unsustainable levels. For instance, if a platform pours money into paid search, social media ads, or affiliate partnerships without closely monitoring conversion rates by channel, the CAC might end up higher than the net contribution from a customer's first loan. When this happens, growth becomes a losing game. On top of that, misjudging risk can make these losses even worse.

Setting interest rates too low or using weak underwriting practices can create a dangerous mismatch between pricing and actual credit risk. If the annual percentage rate (APR) and fee structures fail to account for default risks, net yield takes a hit, which lowers both per-loan contribution margins and customer lifetime value. Worse yet, actual loss rates might far exceed projections, cutting into income from interest and fees after charge-offs and recoveries. High default rates also drive up costs for collections and recoveries, further straining unit economics. In extreme cases, a combination of high CAC and underpriced credit risk can flip what looks like a strong yield on paper into a negative risk-adjusted return - where the platform loses money on every additional loan, even before factoring in fixed costs. This issue often snowballs into other problems, like operational inefficiencies.

Relying on manual processes or outdated technology can quietly undermine profitability by increasing per-loan costs. For example, using expensive call centers instead of self-service tools or failing to automate payment processing and loan servicing can drive up servicing costs to the point where they eat into the pricing margin of each loan. Without automation, operating expenses rise, squeezing contribution margins and making it harder to scale effectively.

High-cost or short-term funding can shrink unit margins significantly. Platforms that depend on high-yield notes, short-term warehouse lines, or equity funding often face a weighted average cost of capital (WACC) that’s close to or even higher than the net interest margin on their loans. For instance, financing a consumer installment portfolio at double-digit annualized rates through high-yield notes or revenue-sharing agreements leaves little room for profit after accounting for defaults, servicing costs, and CAC. Short-term funding lines add another layer of risk, as frequent refinancing or repricing can drive up funding costs, making previously priced loans less profitable. Equity funding, while sometimes necessary, comes with its own challenges - investors expect high returns, and dilution can limit the upside of each unit margin.

Addressing weak areas is key to increasing loan profitability.

High acquisition costs can be tackled by analyzing each step of the customer funnel to identify where potential borrowers drop off [3]. For example, if registration completion rates are low, simplify the onboarding process. Shorter forms, pre-filled information, mobile-friendly designs, and instant decisions can make a big difference. These improvements can reduce the cost per funded loan without requiring additional spending to attract more applicants.

Another effective approach is to use data analytics for smarter targeting. By creating audience segments based on historical repayment patterns and profitability, you can focus your ad spend on high-value customers. Bid more aggressively on segments with higher lifetime value and scale back on channels that attract less reliable borrowers [3]. This strategy directly improves the LTV/CAC ratio.

Boosting revenue per customer starts with personalized pricing. Adjust loan terms based on borrower risk - offering better rates to those with a strong repayment history [3][6]. Loyalty incentives, like lower interest rates, higher credit limits, or quicker approvals, can also encourage repeat borrowing.

Additionally, expand your product offerings. Introducing complementary products, such as credit lines or working capital loans, can increase revenue per borrower [6]. Combine these with active customer engagement to keep high-quality borrowers coming back, which naturally increases their lifetime value.

Default rates can be lowered by enhancing borrower assessment methods. Use scoring models that incorporate transactional data, behavioral patterns, and employment history. For example, open banking data can provide insights into income stability, overdraft events, and overall debt levels - details that traditional credit bureau models might overlook. This can help you approve more applicants while keeping default rates under control [3].

To cut servicing costs, automate routine tasks like payment reminders or balance inquiries. Digital tools such as in-app workflows, chatbots, or IVR systems can handle these efficiently. Self-service options for updating payment details or adjusting payment schedules also reduce call center volume, freeing up staff to handle more complex issues [3].

Diversifying funding sources is another way to improve unit economics. A mix of warehouse lines, forward-flow agreements, securitizations, and retail or peer investors can help reduce dependence on costly capital [3][6]. Use data from portfolio performance - such as vintage curves and cash flow trends - to negotiate better terms with lenders. For instance, strong performance data could help tighten lending spreads by 100–300 basis points during facility renewals. Aligning loan terms and durations with funding structures can also minimize mismatches and reduce unnecessary costs.

Real-time data integration is essential for making informed decisions quickly. Combine data from marketing, underwriting, servicing, and accounting systems into one platform. This allows leadership to act on insights daily or weekly, instead of waiting for month-end reports. For example, if delinquencies over 30 days suddenly spike in a specific channel, you can immediately adjust underwriting standards or pause underperforming campaigns. Dashboards that track metrics like CAC, LTV, default rates, and cost of capital turn unit economics into a dynamic tool rather than a static report [3].

Start by identifying your unit - whether it's per loan or per customer - based on where your revenue originates and where risks are incurred. For instance, many consumer lenders focus on per loan because pricing, risk, and servicing are tied to individual transactions. On the other hand, platforms that prioritize repeat borrowers often opt for a per customer model to account for cross-selling opportunities and lifetime value [3][6]. The right choice depends on where your key decisions are made and how revenue streams are structured.

Once you've defined your unit, create a detailed model. This should account for revenue sources like interest income (APR, average balance, loan tenor), origination and servicing fees, and any additional charges. On the expense side, include marketing and onboarding costs, payment processing, servicing, collections, and funding costs. Don’t forget to factor in risk metrics like approval rates, default rates by vintage, loss given default, and recovery rates [3][6]. With this model in place, embed these metrics into your daily workflows to guide informed decision-making.

Unit economics should influence every aspect of your operations - from marketing and risk management to servicing and collections. Establish integrated data systems that consolidate information from these areas to generate the key metrics outlined earlier. Use these insights to set actionable KPIs and targets. Regularly review progress through weekly check-ins and monthly planning sessions to improve metrics like CAC, LTV, default rates, and cost of capital [2][4]. For platforms aiming to streamline this process, specialized financial advisory services can offer valuable support.

Bringing in financial experts can help fill internal gaps and tackle challenges effectively. For example, Phoenix Strategy Group (https://phoenixstrategy.group) offers fractional CFO services, FP&A, and data engineering to help lending platforms establish strong unit economics frameworks. Their approach includes integrating finance with revenue operations to ensure that unit economics metrics drive growth - not just track performance. They also develop dashboards for real-time monitoring and translate forecasts into operational targets aligned with business goals [1]. For companies dealing with complex financials or aiming to scale efficiently, partnering with experienced advisors can often deliver results more quickly than building in-house capabilities.

Unit economics are the backbone of scalable and profitable lending. Without a solid grasp of key metrics - like customer acquisition cost (CAC), customer lifetime value (LTV), default rates, servicing costs, and the cost of capital - growth becomes more of a gamble than a calculated move. These metrics work together, so focusing on one while ignoring the others can create unintended problems.

The good news? Weak unit economics can be fixed. For example, if your CAC is too high, you can shift spending to higher-ROI channels or simplify your customer acquisition funnel. Struggling with high default rates? Sharpen your credit models, tighten underwriting standards, or adjust pricing to better match risk. Operational inefficiencies can often be tackled by automating collections and servicing processes. And if your funding costs are eating into profits, building strong performance data can open doors to cheaper options like warehouse lines or securitizations. Each of these challenges is an opportunity to make meaningful improvements.

Take a close look at your metrics using the most recent data. Focus on one or two impactful changes - maybe cutting a poorly performing channel, refining credit policies for unprofitable segments, or tweaking pricing to better reflect funding costs and risk levels. Set alerts for critical thresholds, such as an LTV/CAC ratio dropping below 2:1, so you can act quickly. Make it a habit to review your metrics regularly - monthly at a minimum - and hold weekly check-ins to keep your team aligned. When the right numbers are in front of a focused team, better performance naturally follows.

Lending platforms can reduce their Customer Acquisition Cost (CAC) by adopting a few smart strategies:

These methods allow platforms to bring in new customers more efficiently while keeping an eye on profitability.

Improving the LTV/CAC ratio (Lifetime Value to Customer Acquisition Cost) is a critical focus for lending platforms looking to achieve sustainable growth. Here are some practical strategies to help:

By putting these strategies into action, lending platforms can improve their LTV/CAC ratio, paving the way for greater profitability and steady growth. For expert guidance in crafting and executing growth strategies, companies like Phoenix Strategy Group offer tailored support.

Lending platforms handle high default rates by relying on a mix of smart risk management strategies and streamlined operations. They utilize sophisticated credit scoring models and data analytics to better evaluate borrower risk, often integrating unconventional data sources to enhance accuracy in their predictions.

To minimize losses, many platforms spread their risk by diversifying loan portfolios. This way, defaults in one area can be counterbalanced by steady performance in others. On top of that, they cut costs by automating tasks and using technology to keep overhead low. By striking a careful balance between managing risk and running efficiently, these platforms can stay profitable, even when conditions are tough.