Published on

May 2, 2026

If you're running a 3PL business, knowing how to value your company is critical for planning growth, securing funding, or preparing for a sale. Valuation methods typically fall into three categories:

Key takeaways:

Understanding these methods helps you identify areas to improve - like diversifying your revenue, upgrading technology, or reducing founder dependency - to maximize your company's worth.

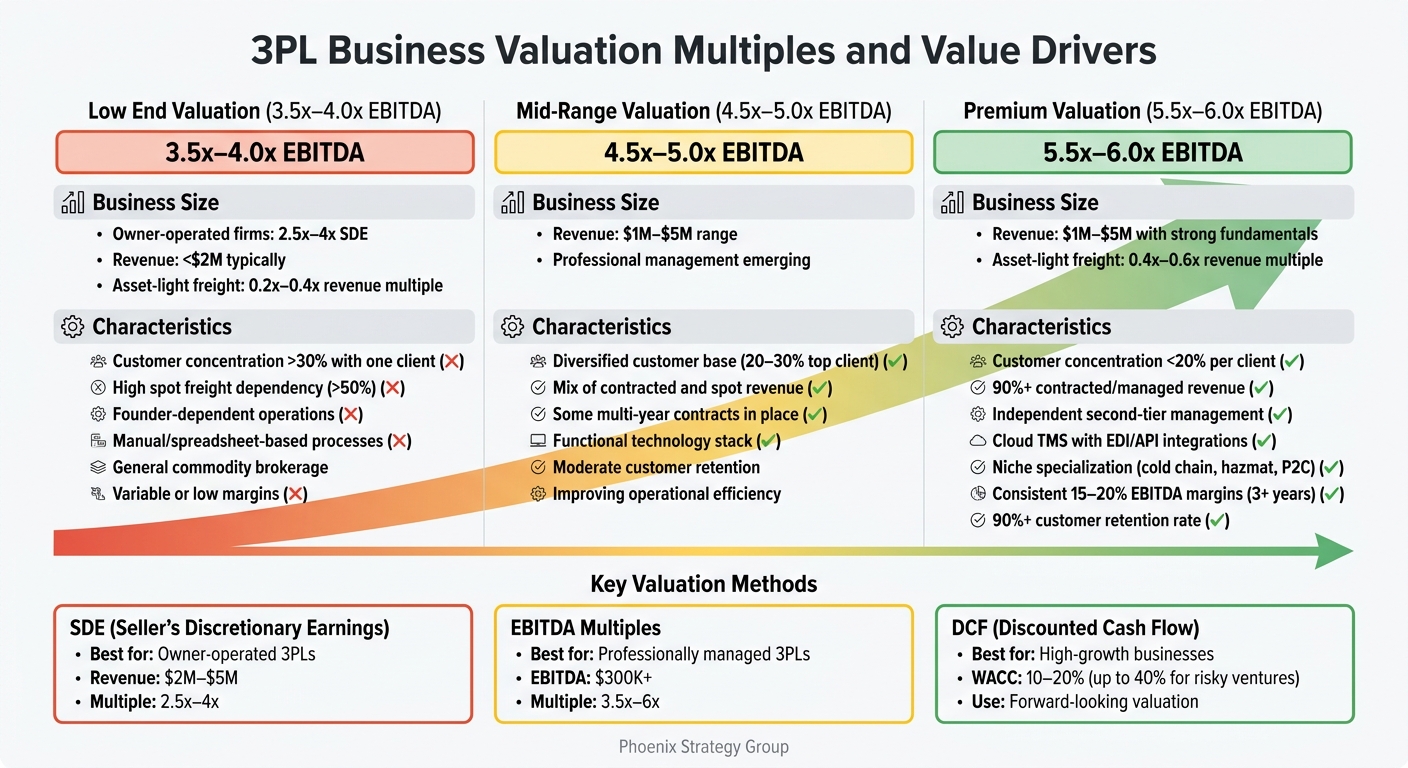

3PL Business Valuation Multiples and Value Drivers Comparison

Income-based valuation focuses on estimating the worth of your 3PL business by analyzing its future cash flow potential. The basic formula is straightforward: Value = Benefit divided by the Required Rate of Return [5]. Before diving into any valuation method, it's essential to normalize your financial statements. This step adjusts for one-time expenses, non-operating items, and discretionary owner benefits to reveal your business's actual operating performance [3][7].

"Normalization adjustments routinely move reported earnings by 15% to 40% in either direction."

– Lorenzo Nourafchan, Fractional CFO, Northstar Financial Advisory [2]

The choice of valuation method depends on your 3PL's size and structure. Smaller, owner-operated businesses often use Seller's Discretionary Earnings (SDE), while mid-sized companies lean on EBITDA multiples. For businesses undergoing rapid growth or significant operational changes, Discounted Cash Flow (DCF) analysis provides a forward-looking perspective that complements historical data. Here’s a closer look at each method.

SDE is designed to measure the total economic benefit for owner-operators. It includes everything from the owner's salary and benefits to discretionary expenses like personal travel or perks above market rates. This approach is commonly used for smaller 3PLs, particularly those generating $2 million to $5 million in revenue where the founder is deeply involved in daily operations [1].

Typical SDE multiples for small regional freight brokerages range from 2.5x to 4x [1]. However, every adjustment must be well-documented with invoices or payroll records. Buyers will scrutinize these details during due diligence, and any unsupported claims can damage credibility [1]. To prepare for a sale, start normalizing your financials 12 to 24 months in advance to ensure all add-backs are fully substantiated [1][2].

For larger or professionally managed 3PLs, EBITDA multiples become the preferred method. EBITDA, which stands for Earnings Before Interest, Taxes, Depreciation, and Amortization, adjusts for a market-rate salary for a general manager, making it suitable for businesses that can operate without direct founder involvement [2].

Companies with annual revenue between $1 million and $5 million typically sell for 3.5x to 6x EBITDA [1]. Premium multiples - ranging from 5.5x to 6x - are reserved for businesses with consistent EBITDA margins of 15% to 20% sustained over three or more years [1]. The quality of revenue also plays a critical role. Contracted managed freight revenue tends to fetch higher multiples compared to more volatile spot brokerage revenue [1].

DCF analysis projects your business's future cash flows and discounts them back to their present value using your Weighted Average Cost of Capital (WACC) [2][4]. This method is particularly useful for businesses anticipating major changes, such as securing long-term contracts or launching new distribution centers [8]. For private 3PLs, WACC generally falls between 10% and 20%, though smaller or riskier businesses may require discount rates as high as 25% to 40% [2].

"DCF is the most theoretically rigorous method and the most assumption-sensitive. Move the discount rate from 15% to 12% and the valuation jumps roughly 30%."

– Lorenzo Nourafchan, Fractional CFO, Northstar Financial Advisory [2]

While DCF provides a detailed, forward-looking valuation, it’s often used alongside EBITDA multiples to cross-check assumptions. If the results from these two methods differ significantly, it’s a red flag that either the DCF assumptions or the multiple needs revisiting [2]. This dual approach helps ensure a more accurate and balanced valuation.

Market-based valuation methods rely on actual transaction data from comparable 3PL businesses, offering a grounded perspective on what buyers are willing to pay. These methods serve as a practical complement to income-based approaches, providing benchmarks rooted in real-world deals. For instance, if a buyer paid 4.5x EBITDA for a regional freight broker with similar characteristics, that multiple can act as a reference point [6].

Finding the right comparables involves more than just matching revenue figures. It requires identifying businesses with similar regional presence, service niches, and operational models [1]. For example, a cold chain specialist in the Northeast operates quite differently from a general freight broker in Texas, even if both generate similar revenues. Typically, asset-light freight brokerages trade at revenue multiples of 0.4x to 0.6x, while asset-heavy carriers often fetch lower multiples, ranging from 0.2x to 0.4x [10].

Since no two 3PLs are identical, adjustments for revenue quality are essential. A company with a primarily contracted revenue base will generally command a higher valuation than one heavily reliant on volatile spot market transactions [1]. Customer concentration is another critical factor. For example, if a comparable business has no customer contributing more than 20% of its revenue, but your top client accounts for 35%, your valuation may need to be discounted. High customer concentration (above 30%) can reduce valuations by 1x to 2x [1].

For businesses with revenues between $1 million and $5 million, EBITDA multiples typically range from 3.5x to 6x [1]. Smaller, owner-operated firms with less than $2 million in revenue often sell at 2.5x to 4x Seller's Discretionary Earnings (SDE) [1]. Notable transactions include C.H. Robinson's $220 million acquisition of Prime Distribution Services in March 2020, which enhanced its retail consolidation and warehousing capabilities [13]. Similarly, DHL Group's July 2023 acquisition of MNG Kargo secured a strong position in Turkey’s growing domestic parcel and e-commerce market [11][13].

These comparisons highlight how operational specifics influence valuation multiples, as explored further below.

Several factors determine where a 3PL business falls within the EBITDA multiple range of 3.5x to 6x. Revenue quality is a major consideration: businesses with contracted managed freight revenue are seen as more stable and secure, while those relying on spot revenue face significant discounts due to volatility [1]. Companies with a substantial portion of their margins tied to multi-year service agreements typically achieve higher multiples.

Customer diversification also plays a role. Maintaining a top customer share below 20%–25% can add 0.5x to 1.5x to the EBITDA multiple [1]. Premium multiples of 5.5x to 6x are often reserved for businesses with 90% or higher customer retention and consistent EBITDA margins of 15% to 20% over several years [1].

Technology infrastructure is another key driver. A modern, cloud-based Transportation Management System (TMS) with EDI integrations and real-time tracking capabilities signals scalability and operational efficiency, which can boost valuation [1]. On the other hand, reliance on manual or spreadsheet-based processes may suggest higher labor costs and limited growth potential [1][12].

Management depth also impacts valuation. Businesses with experienced second-tier management teams are less dependent on founders, which reduces risk and supports higher multiples. Conversely, founder-dependent companies may see their multiples reduced by 1x to 2x [1]. Additionally, niche specialization in areas like cold chain logistics or hazmat transport can create competitive advantages that justify premium pricing [1]. The global 3PL market, projected to reach $1.6 trillion by 2025 and grow at a CAGR of 10.1% through 2035, reflects strong demand for such specialized capabilities [9].

| Valuation Tier | EBITDA Multiple | Key Characteristics |

|---|---|---|

| Low End | 3.5x – 4.0x | Customer concentration >30%, founder-dependent, high spot freight dependency |

| Mid Range | 4.5x – 5.0x | Diversified customer base, some multi-year contracts, functional technology stack |

| Premium | 5.5x – 6.0x | Niche specialization (hazmat/cold chain), 90%+ retention, 15–20% consistent margins |

For expert guidance on market-based valuation methods and tailored financial strategies, consider reaching out to Phoenix Strategy Group (https://phoenixstrategy.group), which specializes in helping growth-stage companies prepare for exits and scale effectively.

When it comes to valuation, the asset-based approach focuses on the tangible investments a company has made in its operations. For businesses that rely heavily on physical assets - like warehouses, fleets, or specialized equipment - these assets often set a baseline for valuation, especially in distressed sales scenarios [15][10]. For instance, industrial property appraisals can complement EBITDA-based enterprise valuations [14]. Let’s take a closer look at how working capital and capital expenditures (CapEx) influence these valuations.

The condition of a company’s physical assets plays a big role in determining its purchase price. If infrastructure is outdated - think deteriorating roofs, malfunctioning dock levelers, or worn-out racking systems - buyers may lower their offers significantly, deducting repair costs during due diligence [14]. On the flip side, facilities with specialized features like cold storage, hazmat compliance, or bonded warehouse status often fetch higher valuations because these features create significant barriers for competitors [1][14]. For example, cold-storage facilities can command valuations ranging from $50 to $150 per square foot, far exceeding the values of standard warehouse spaces [10].

Owning assets also affects financing options and revenue multiples. Physical assets can serve as collateral for loans, such as SBA 504 loans, which may require as little as 10% equity. However, this model typically results in lower revenue multiples - around 0.2x–0.4x, compared to 0.4x–0.6x for asset-light businesses [10][14]. Factors like high depreciation, ongoing maintenance costs, and greater working capital demands contribute to this disparity. For instance, trucks are usually valued at 50% to 75% of their market replacement cost, depending on their age and maintenance history [10].

A key step in valuation is normalizing working capital, which involves distinguishing between maintenance CapEx (to keep assets operational) and growth CapEx (to expand capacity) [14]. Deferred maintenance can drag down valuation, as buyers often subtract near-term capital needs directly from the purchase price. To avoid this, sellers should consider addressing infrastructure updates 18–24 months prior to selling [14].

Technology investments also play a major role. Companies lacking modern systems signal potential future capital needs and integration challenges [1][14]. Additionally, clean, accrual-based financials are critical for verifying add-backs and securing SBA 7(a) financing. Lenders carefully examine whether non-recurring or one-time expenditures have been properly added back to EBITDA during normalization [1][14].

Operational maturity is another important factor that influences valuation. Financial transparency is essential for EBITDA normalization, which involves adding back expenses like owner compensation, personal costs, and one-time charges to reveal the true economic benefit [1]. Businesses with commingled finances or inconsistent reporting often run into challenges during this process, raising doubts among lenders during SBA underwriting [1].

3PLs that maintain steady EBITDA margins of 15–20% over three or more years are often able to secure multiples of 5.5x to 6x [1]. The depth of management also matters significantly. Companies with a strong second-tier management team that can operate independently of the founder tend to reduce buyer risk and achieve higher valuations [1]. On the other hand, founder-dependent businesses may see their multiples reduced by 1x to 2x [1]. Additionally, formalizing month-to-month storage agreements into multi-year contracts can lower perceived churn risks and improve debt underwriting [14].

For businesses looking to prepare for valuation, Phoenix Strategy Group offers fractional CFO services and M&A support tailored to logistics companies in the growth stage. Learn more at Phoenix Strategy Group.

When preparing a 3PL company for sale, it’s essential to identify the key factors that drive value and address potential risks. The difference between a 3.5x EBITDA multiple and a 6x multiple often hinges on how well you manage risks and establish competitive strengths. Buyers tend to focus on areas like customer relationships, revenue stability, management depth, and operational efficiency. Let’s break down how elements like revenue mix, customer base, and management structure can impact valuation.

A strong understanding of your revenue quality and customer mix is critical to maximizing your EBITDA multiple. One of the biggest red flags for buyers is customer concentration. If a single customer accounts for more than 20–25% of your revenue, it significantly increases acquisition risk [1]. And if your top three customers generate over 50% of your revenue, you’re likely to face challenges with predictability that can lower your valuation [17]. In fact, many institutional buyers and SBA lenders won’t even consider deals where customer concentration exceeds 30% [1].

The type of revenue you generate is just as important as how it’s distributed. Contracted or managed freight revenue is far more attractive to buyers than revenue from volatile spot market transactions. This is because contracted revenue is seen as recurring and dependable [1][16]. For instance, a 3PL that earns 90% or more of its revenue from contracted programs with multi-year agreements is positioned for premium valuations. On the other hand, companies reliant on 50% or more spot freight often face intense scrutiny during due diligence [16][1]. Businesses with 90%+ customer retention rates and consistent EBITDA margins of 15–20% over three or more years typically achieve multiples in the 5.5x–6x range [1].

"Predictability drives value. Concentration challenges predictability." - Nuvera Partners Inc. [17]

To mitigate risks tied to customer concentration, consider diversifying your client base. Target adjacent markets and offer additional services to existing customers [17][18]. Convert month-to-month agreements into multi-year contracts with renewal and transferability clauses [17][1]. Use profits from large accounts to fund marketing and lead generation efforts, which can help you attract a broader range of clients [19]. These steps not only lower concentration risk but also make your business more appealing to SBA lenders [1][16].

Here’s how key factors influence valuation multiples:

| Value Driver | Low Multiple (3.5x–4.0x) | Premium Multiple (5.5x–6.0x) |

|---|---|---|

| Customer Concentration | >30% with one client | <20% per client; diversified base |

| Revenue Type | High spot freight dependency | 90%+ contracted/managed revenue |

| Management | Founder-dependent | Independent second-tier management |

| Technology | Manual/Spreadsheet-based | Cloud TMS with EDI/API integrations |

| Specialization | General commodity brokerage | Niche (Cold chain, Hazmat, P2C) |

| Margins | Variable/Low | Consistent 15–20% EBITDA margins |

Beyond customer distribution and revenue stability, expanding service offerings and building a strong management team can further increase business value.

Specialized services and independent management are essential for achieving higher valuations. Niche expertise adds a layer of defensibility that can justify premium multiples. For example, 3PLs with a focus on high-barrier verticals like cold chain logistics, hazmat transportation, oversized freight, or final-mile e-commerce fulfillment often command 5.5x–6x EBITDA multiples [1]. These services require significant investment, regulatory compliance, and operational expertise, making them hard for competitors to replicate. Expanding into a full-service model - offering forwarding, warehousing, customs documentation, and last-mile delivery - can also improve customer retention and revenue predictability [20].

Equally important is the independence of your management team. Businesses overly reliant on the founder often see their valuation reduced by 1x–2x [1]. The concern is clear: if customers leave after the founder exits, the buyer’s investment is at risk. To avoid this, transition key customer relationships to a professional management team at least 12–24 months before selling [1][16]. Create detailed organizational charts, define roles clearly, and ensure your team has the experience and tenure to operate effectively without the founder.

Technology infrastructure also plays a critical role in valuation. Buyers look for scalable, cloud-based Transportation Management Systems (TMS) with EDI integrations and real-time tracking [1][16]. These systems demonstrate operational maturity and enhance customer retention. For instance, in January 2024, Bulu Group replaced its manual Excel-based system with Extensiv 3PL Warehouse Manager, SmartScan, and Small Parcel Suite. The result? A 25% increase in labor efficiency, a 50% reduction in billing time, and 100% order accuracy. These upgrades allowed the company to guarantee same-day shipping and implement a 4PL network strategy [21].

For 3PLs planning an exit, Phoenix Strategy Group provides M&A advisory and fractional CFO services tailored to logistics businesses. Their expertise in financial modeling, due diligence preparation, and valuation strategies helps companies maximize their sale price. Learn more at Phoenix Strategy Group.

When it comes to valuing a 3PL business, the approach depends heavily on the size and characteristics of the company. For smaller, owner-operated firms with less than $5 million in revenue, Seller's Discretionary Earnings (SDE) is often the best metric, as it reflects the total economic benefit to the owner [1][2]. On the other hand, larger 3PLs generating $300,000 or more in normalized EBITDA are better suited for valuation using EBITDA multiples, which take into account the cost of replacing the owner with a market-rate manager [1][2]. For early-stage or high-growth businesses, revenue multiples or Discounted Cash Flow (DCF) analysis may be more appropriate to capture future earnings potential [2][22].

Choosing the wrong metric can lead to valuation discrepancies of 50% or more, a major factor in why only 20% to 30% of businesses listed for sale actually close [2]. Critical elements such as customer concentration, the balance between contracted and spot freight, and the ability of the business to operate without its founder can significantly influence whether a business commands a 3.5x EBITDA multiple or a 6x multiple [1]. Even small errors, like missing a single dollar in add-backs, can cost $4 in valuation on a 4x multiple [2].

"The act of valuing your business honestly forces you to confront the operational realities a buyer would price in, and that exercise alone usually surfaces the two or three highest-ROI changes you can make." - Lorenzo Nourafchan, Fractional CFO, Northstar Financial Advisory [2]

To maximize value and reduce risks, it's crucial to start financial preparations 12–24 months before an exit. Ensure your financials are accrual-based, thoroughly document all add-backs, and work to reduce customer concentration to less than 20% per client [1][2]. These steps not only enhance buyer trust during due diligence but also strengthen your operational foundation.

For 3PL owners looking to sell, secure funding, or plan for long-term growth, Phoenix Strategy Group offers tailored M&A advisory services, fractional CFO support, and financial modeling expertise specifically for logistics businesses. Their services, including normalization, Quality of Earnings reports, and exit planning, help businesses maximize sale prices and navigate complex transactions. Learn more at Phoenix Strategy Group.

Choosing between Seller's Discretionary Earnings (SDE) and EBITDA comes down to your 3PL's size and how it's structured. SDE works best for smaller, owner-operated businesses since it includes the owner's compensation and discretionary expenses. On the other hand, EBITDA is typically used by larger, more structured companies because it excludes owner-specific costs, offering a more standardized view of profitability for potential investors. When deciding, think about your company's scale and the type of buyer you're targeting.

Buyers typically account for financial adjustments known as add-backs when evaluating a 3PL business. These include owner-specific expenses, non-recurring costs, and discretionary expenses that aren't essential to the business's regular operations. These adjustments are crucial because they help present a clearer picture of the company's actual earnings and normalize its cash flow for valuation purposes.

To boost your valuation multiple before selling your 3PL business, focus on a few critical areas. Build strong, long-term customer relationships to showcase stability and reliability. Improve operational efficiency by streamlining processes and reducing waste, and invest in modern technology to stay competitive and scalable.

If your business has issues like heavy reliance on a few customers or outdated systems, address them proactively. Shifting to contracted revenue streams can also make your business more appealing to buyers by providing predictable income.

Another strategy is to specialize in high-demand niches, such as cold chain logistics. Buyers often prioritize businesses with profitability, diversified revenue sources, and operational resilience, all of which can drive higher valuation multiples.