Published on

May 2, 2026

Cross-border valuation is a complex process that requires balancing U.S. valuation standards with local economic, regulatory, and political factors. Missteps can lead to overpaying, tax penalties, or distorted outcomes. Key challenges include currency risks, regulatory differences, and local market conditions. For example, using incorrect exchange rates or mismatching discount rates with cash flows can skew results.

The article explores case studies like the Yell Group's LBO, highlighting how tailored methods, such as the Capital Cash Flow approach, address unique transaction complexities. It also examines intra-regional M&A synergies, which often outperform inter-regional deals due to easier integration and shared market frameworks.

Key takeaways:

Understanding these nuances can help businesses navigate cross-border deals effectively and avoid costly errors.

In September 2003, private equity firms Apax Partners and Hicks Muse explored the leveraged buyout of the Yell Group, a division of British Telecom (BT). Investors Paolo Notarnicola and Mark Veblen led the deal, which presented a unique challenge: valuing a business operating in two distinct markets. The UK’s BT Yellow Pages was a stable, mature asset, while Yellow Book USA was experiencing growth in the U.S. directory market. The bid range fell between £1.85 billion and £2.3 billion, with the base acquisition price set at £2.09 billion (including a 5% transaction fee).

For BT, this sale was part of a broader effort to reduce its significant debt burden. On the other hand, for the private equity sponsors, this was a high-stakes opportunity to establish their reputation. However, the deal wasn’t without its complications. The UK business faced regulatory constraints, including a price cap requiring rates to remain 6% below inflation. Meanwhile, the U.S. market offered significant growth potential, with independent directories expected to grow their market share from 11% to 30% between 2000 and 2005 [4]. These contrasting environments made valuation particularly complex, requiring adjustments to traditional methods.

The Yell Group team chose the Capital Cash Flow (CCF) approach over the more commonly used Free Cash Flow (FCF) method with Weighted Average Cost of Capital (WACC). Why? In leveraged buyouts, rapid debt repayment often makes the constant-structure WACC method less effective. The CCF approach simplifies the process by factoring in interest tax shields directly into cash flow, which is then discounted at the unlevered cost of equity. This method was especially suitable for Yell Group, as the debt repayment plan was clearly defined.

Given the cross-border nature of the transaction, U.S. cash flows had to be converted to pounds at the prevailing exchange rate, with adjustments for local risk-free rates and market betas. The valuation was particularly sensitive to regulatory assumptions. For instance, if the UK price cap had been set at 5% below inflation instead of 6%, the acquisition price would have jumped to £2.30 billion [4]. These nuances in valuation methods significantly influenced how the deal was structured.

To align the goals of private equity investors with those of Yell Group’s management team, carried interest mechanisms were built into the deal. This was critical given the dual nature of the business: steady cash flow from the UK operations and the growth potential in the U.S. market. The financing structure was designed to support aggressive returns while balancing both short-term and long-term objectives.

The UK corporate tax rate of 30% played a key role in shaping the deal. It affected the valuation of tax shields and ultimately influenced the equity holders’ net returns. The incentive structure had to ensure that immediate cash flow generation from the UK side didn’t overshadow the growth opportunities offered by the U.S. operations [4]. Balancing these priorities was central to the deal’s success.

Acquisitions within the same geographic region often hit what Boston Consulting Group calls the "sweet spot" of M&A. These deals balance the growth opportunities of international expansion with simpler integration compared to global transactions [5].

The numbers back this up: intra-regional deals deliver an average two-year relative total shareholder return of 1.2%, which is double the 0.6% return seen in inter-regional deals. On the other hand, domestic deals tend to lag behind, with an average two-year return of -0.9% [5].

"Intra-regional deals have consistently emerged as the optimal 'sweet spot,' providing companies with meaningful international growth opportunities combined with manageable integration complexities"

– Jens Kengelbach, Daniel Friedman, Anant Shivraj, Tobias Söllner, and Dominik Degen [5]

So, why do regional deals perform better? Factors like cultural familiarity, aligned regulations, and regional trade agreements make integration smoother. Take the example of a German company acquiring a French competitor - both operate within a similar regulatory framework and share comparable consumer profiles. Existing distribution networks across neighboring markets further simplify integration and support market expansion [5].

The industry also plays a role in determining success. Energy and industrial sectors often benefit more from regional consolidation, while financial services and consumer-focused companies tend to see greater returns from inter-regional expansion [5]. A notable example is Meredith Corp.'s acquisition of Time Inc. in November 2017. The combined entity, with sales of approximately $4.6 billion, aimed to achieve $200 million to $250 million in pretax cost synergies within two years by cutting overlapping corporate and sales expenses [7].

However, even with these advantages, integration challenges can complicate the process and require careful planning.

While intra-regional deals offer clear benefits, they still come with their own set of integration hurdles. On average, realizing synergies takes about 2.8 years, with integration costs often equaling a full year’s operating expenses [7].

Local labor laws and regulatory requirements can extend timelines, making early cultural due diligence critical. Decisions like where to locate a new headquarters or rebranding efforts can also delay synergy realization [7].

Even within a region, cultural differences can pose challenges. For instance, varying decision-making styles - ranging from consensus-driven approaches to strict hierarchies - and differing communication norms can disrupt integration if not addressed proactively. Thorough cultural due diligence is key to mitigating these risks [5].

One U.S.-based manufacturer tackled these challenges using a "W" approach to integration. By embedding synergy targets into regular business reviews and balancing top-down goals with bottom-up input, they turned a theoretical $4 billion cost reduction target into a workable plan [6]. Another example is a merger between two U.S. retailers, which initially aimed for $300–$500 million in cost savings but ultimately achieved $740 million in synergies through detailed pre-close planning [6].

Valuation Methods Comparison for Cross-Border M&A Transactions

A frequent misstep in cross-border valuations is relying on a U.S.-centric approach that overlooks critical factors like local inflation, political risks, and industry-specific details. Another common error is using spot exchange rates for future cash flows, which fails to account for expected currency fluctuations. This can be avoided by applying a forward exchange curve instead. Similarly, mismatching the discount rate with the currency of cash flow projections - such as using a local WACC for USD-based forecasts - can skew results. In countries with hyperinflation, neglecting to adjust the local risk-free rate for potential government default risk often leads to an overestimation of value.

Another issue is relying solely on one valuation method. Experts strongly recommend using at least two approaches - typically the income and market methods - to provide a more defensible valuation.

"The valuation of a non-U.S. company can sometimes be problematic if the analysis is conducted with a U.S.-centric mindset."

– Ankura Consulting Group [1]

These challenges underscore the importance of tailoring valuation approaches to the specific jurisdiction.

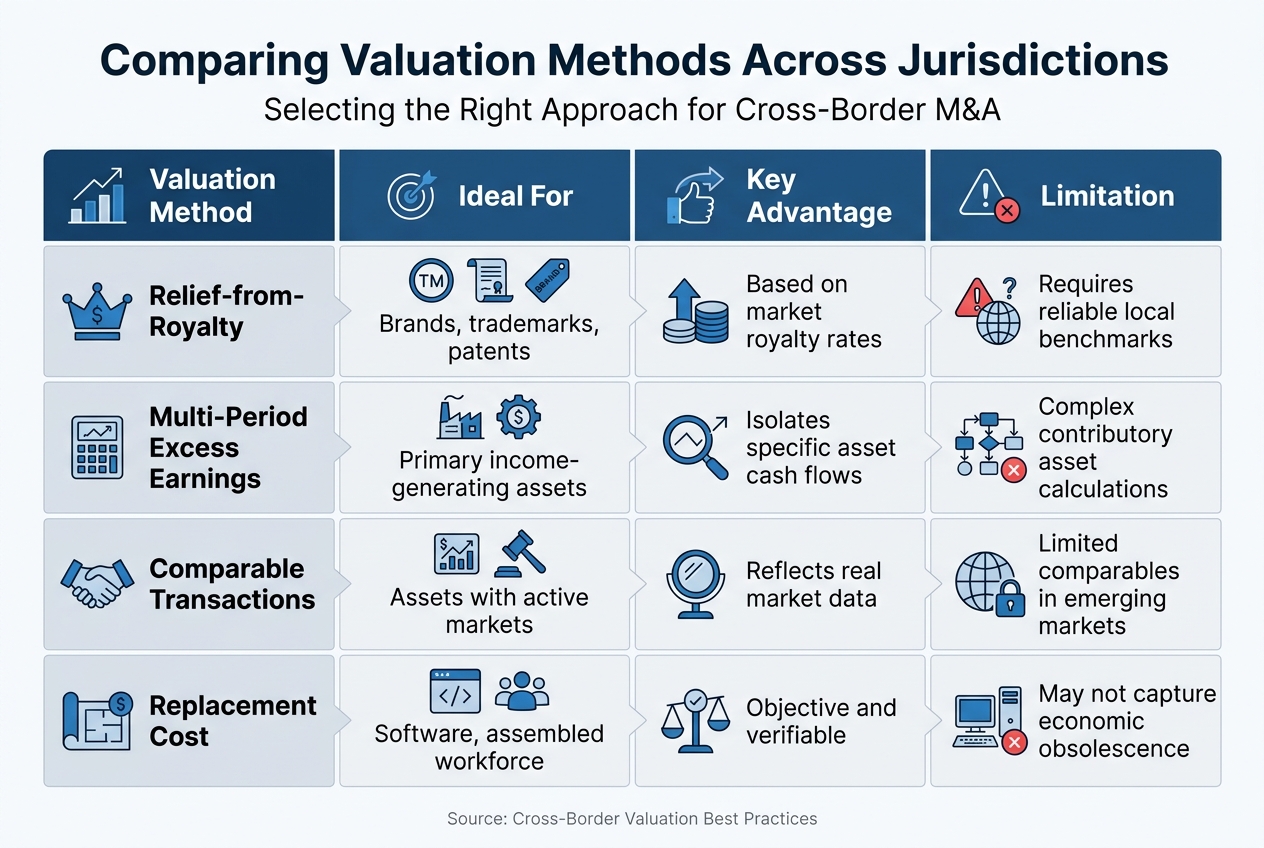

Understanding how valuation methods vary across markets is crucial for addressing common errors. The income approach, using techniques like Relief-from-Royalty or Multi-Period Excess Earnings, is particularly useful for valuing intangible assets such as brands and patents [2]. The market approach relies on active market data from comparable transactions, while the cost approach is best suited for assets like software or assembled workforces, where replacement or reproduction costs are key [2].

| Valuation Method | Ideal For | Key Advantage | Limitation |

|---|---|---|---|

| Relief-from-Royalty | Brands, trademarks, patents | Based on market royalty rates | Requires reliable local benchmarks |

| Multi-Period Excess Earnings | Primary income-generating assets | Isolates specific asset cash flows | Complex contributory asset calculations |

| Comparable Transactions | Assets with active markets | Reflects real market data | Limited comparables in emerging markets |

| Replacement Cost | Software, assembled workforce | Objective and verifiable | May not capture economic obsolescence |

This comparison highlights the importance of selecting the right method to address valuation challenges. Additionally, it's essential to consider varying accounting standards. For example, while IFRS 3 and ASC 805 prohibit goodwill amortization, some local GAAPs in Japan and parts of the EU still require it. This can significantly impact how cross-border deals are structured and reported [1].

To improve valuation accuracy, it’s critical to apply lessons from past mistakes and leverage method comparisons effectively. Start by engaging local expertise early. Involving local valuation specialists and legal teams during due diligence ensures enforceability of intellectual property rights and access to reliable market benchmarks [1]. This is especially important given that intangible assets now account for approximately 90% of the S&P 500's market value, a sharp increase from just 17% in 1975 [2].

Thorough documentation is another key factor. Under OECD Hard-to-Value Intangibles rules, tax authorities may challenge your projections if actual outcomes differ significantly from initial assumptions [3]. Modeling tax implications before finalizing deals can also help avoid unexpected liabilities later on [2]. Additionally, understanding local tax laws around the deductibility of intangible asset amortization - often referred to as the Tax Amortization Benefit (TAB) - can have a significant impact on net present value [1].

Finally, corroborating your primary valuation method with a secondary one can enhance credibility, particularly in situations where data is limited [1].

"Intangible asset valuation in cross-border M&A is a balancing act between local market realities, global compliance, and strategic deal objectives."

– CA Prateek Mittal, Registered Valuer [2]

Cross-border valuations are complex and demand a coordinated approach that blends expertise in local tax laws, currency considerations, and regulatory nuances. As Shakespeare James and PJ Patel from Valuation Research Corp. emphasize:

"Finding the right valuation experts and giving them a seat at the table early on can reduce headaches and, more importantly, help head off and defend problems and challenges from tax authorities down the road" [8].

Keeping thorough documentation of valuation assumptions is crucial. Tax authorities are increasingly applying "hindsight" rules under the OECD's Hard-to-Value Intangibles framework. If actual outcomes deviate significantly from initial projections, detailed records can help justify your original assumptions.

Another critical point is aligning cash flow projections with the appropriate discount rate. Mixing currencies and discount rates leads to flawed results. Tony Hillier from Opagio explains:

"using a GBP discount rate with BRL cash flows would produce a meaningless result" [3].

To ensure accuracy and defensibility, rely on at least two valuation methods - most commonly the income and market approaches - and make sure cash flow projections match their respective discount rates.

To put these lessons into action, consider the following steps:

For businesses managing intricate cross-border transactions, Phoenix Strategy Group (https://phoenixstrategy.group) offers tailored financial and strategic advisory services. Their expertise in FP&A, M&A support, and fractional CFO services can help you navigate these challenges effectively. Cross-border valuations leave little room for error, but with careful planning and the right team, you can turn these complexities into opportunities for strategic growth.

When choosing exchange rates for future foreign cash flows, you have a couple of options. One approach is to use forward exchange rates, which represent the market's expectations for currency values on specific future dates. Alternatively, you can rely on estimated future spot rates, often derived from models like uncovered interest parity. Whichever method you choose, make sure the rates you use are consistent with your valuation approach to ensure precision and dependability.

Capital Cash Flow (CCF) is particularly useful in cross-border transactions, especially when evaluating the total cash flow available to all capital providers. This approach shines in scenarios where the capital structure is either complex or subject to change. Additionally, CCF is a better choice than Free Cash Flow (FCF) with Weighted Average Cost of Capital (WACC) when the tax benefits of debt are uncertain or vary between countries. It effectively addresses these inconsistencies, providing a more accurate assessment in such situations.

When assessing asset values in emerging markets, it's crucial to factor in risks such as political instability, economic unpredictability, currency swings, and a lack of financial transparency. These elements are usually addressed by adding a country risk premium (CRP). This adjustment helps create a more precise discount rate, accounting for the distinct challenges tied to operating in these regions.