Published on

June 5, 2026

Launching an e-commerce startup requires smart funding choices to tackle cash flow gaps, inventory costs, and growth investments. Here's a quick breakdown of the best funding strategies:

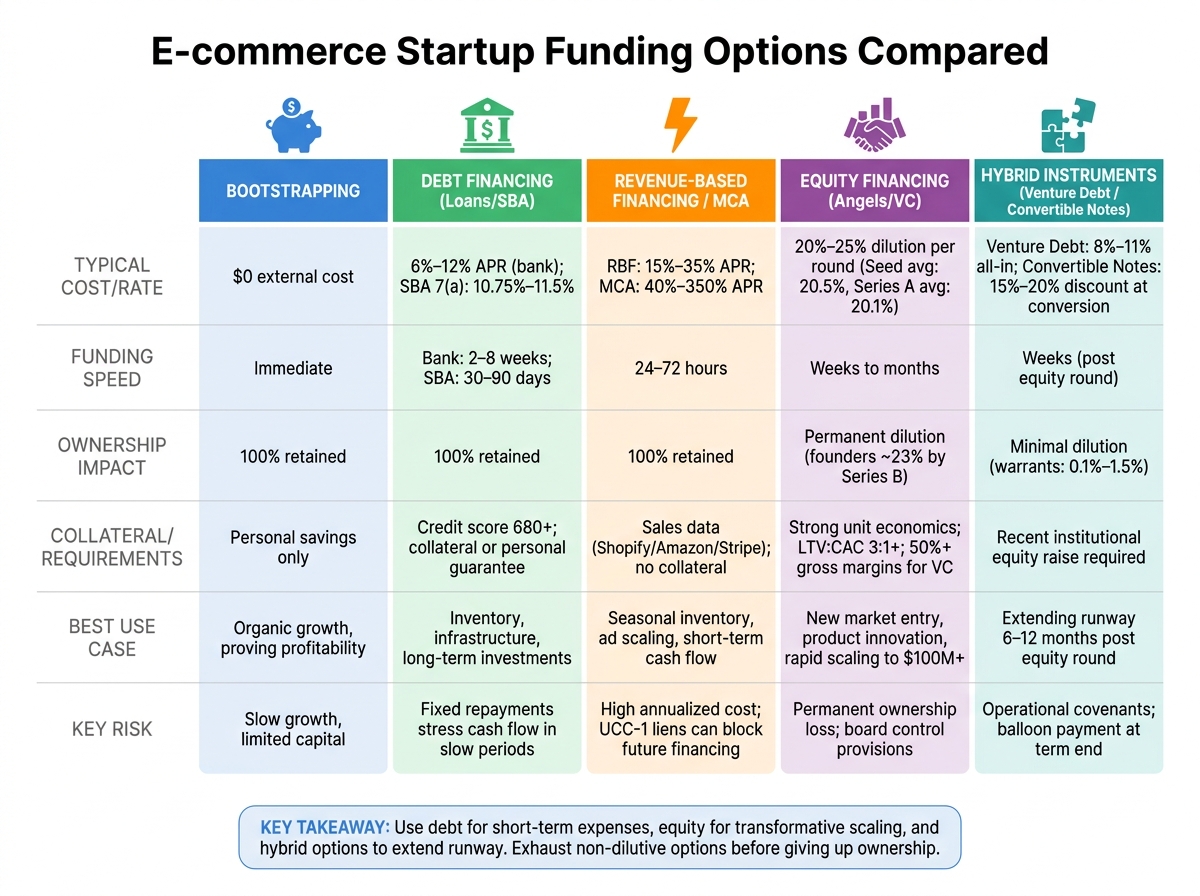

Key takeaway: Match your funding method to your business needs - debt for short-term expenses, equity for scaling, and hybrid options for flexibility. Avoid diluting ownership unless the potential return justifies it.

E-commerce Startup Funding Options Compared: Costs, Speed & Best Use Cases

For most e-commerce founders, the funding journey often begins close to home. In fact, over 75% of successful e-commerce businesses rely on a mix of personal savings, reinvested profits, and strategic debt rather than outside equity [3]. This early approach not only builds a solid financial base but also prepares the business for more structured funding opportunities later on. Let’s explore how personal savings and reinvested profits serve as the backbone of early-stage funding.

Using personal funds allows founders to maintain full ownership and control, creating a direct connection between financial decisions and business performance. This level of accountability encourages careful management of resources, focusing on unit economics, contribution margins, and profitability instead of just chasing growth. Businesses that are profitable and efficient with their capital often attract acquirers because they’ve proven their ability to thrive without constant external funding [4].

Before seeking outside capital, it’s critical to hit specific internal benchmarks. For example, aim for at least a 20% net margin and an LTV:CAC ratio of 3:1 or better [3][2]. These metrics demonstrate a healthy, scalable business model.

"Every dollar of capital needs a credible path to return. If you can't trace the dollar to the outcome, you're not ready to raise." - Eightx [2]

When personal savings fall short and institutional funding isn’t yet an option, many founders turn to their personal networks for support. This approach works best when the terms are clearly defined from the outset - whether structured as a loan or equity. If equity is involved, consider using non-voting shares or crowd SAFEs to retain control over decision-making [5].

A clear, specific pitch can make all the difference. For instance, saying, "We need $150,000 for a 5,000-unit production run to reduce cost of goods by 18%", is far more compelling than a vague request for growth capital [3]. If you choose to structure the funding as a loan, ensure your business has enough cash flow to comfortably cover repayments, even during slower periods [5].

Equity should always be seen as the most expensive form of funding. For needs under $500,000, non-dilutive options like personal loans, inventory financing, or extended supplier terms are typically more cost-effective than giving up ownership in your company [2][3]. Rachel Torres, an Entrepreneurship Writer at WePitched, puts it perfectly:

"If you are using equity to pay for Facebook ads, you are effectively selling your house to pay for gas. Use debt or revenue-based financing for customer acquisition." - Rachel Torres, WePitched [3]

Once you've tapped into personal funds and your network, debt financing becomes a practical way to fuel your business while holding onto ownership. Unlike equity, debt allows you to address operational needs - think inventory, advertising, or shipping - without giving up a piece of your company. Plus, interest payments are tax-deductible. For example, with a 21% corporate tax rate, an 8% loan effectively costs about 6.3% after taxes [1]. Below, we dive into how loans, SBA programs, lines of credit, and business credit cards can fit into your financial strategy.

"The government is effectively subsidizing part of your borrowing cost every time you service a business loan, a benefit that disappears entirely when you fund growth through equity instead." - Credilinq [1]

Traditional bank loans are a solid option for founders with strong credit (750+) and established banking relationships. Rates typically fall between 6% and 12% APR [8]. The challenge? Banks often require hard collateral like real estate or equipment, which many e-commerce businesses lack.

Here’s where SBA 7(a) loans step in. As of May 2026, these loans offer variable rates ranging from 10.75% to 11.5% (Prime + 2.25–3.0%) [11]. While the rates are higher, SBA loans come with features that are hard to beat: repayment terms of up to 10 years, a modest 10% down payment, and no prepayment penalties for loans under 15 years [9][11]. In fiscal year 2024, over $27.5 billion in SBA 7(a) loans were approved, supporting more than 57,000 small businesses [15].

The downside? SBA loans aren't quick. They can take 30 to 90 days to process, making them unsuitable for urgent needs like restocking inventory [7]. Instead, use them for planned, long-term investments such as acquiring a brand, developing proprietary technology, or building infrastructure. Keep in mind, owners with 20% or more equity must sign a personal guarantee, so consider the risks before applying [11][14].

"SBA loans offer terms that no conventional bank or CMBS can match for small business and owner-operator real estate - 90% LTV on SBA 504... and working-capital-included structures (7(a)) that bundle everything into one loan." - Ed Freeman, Capital Advisor, PeerSense [11]

For recurring short-term expenses like supplier deposits, advertising campaigns, or seasonal inventory, a revolving line of credit is a flexible option. Since you only pay interest on the amount you draw, it’s a cost-effective solution for fluctuating capital needs [1].

Business credit cards can be even more advantageous. Cards like AMEX offer up to 51 days of interest-free financing if you pay off the balance in full each cycle [12].

The trick is pairing the right tool with the right need. Lines of credit are ideal for ongoing, repeatable expenses, while term loans work better for one-time investments with a clear repayment timeline.

Integrating debt into your capital structure requires careful planning. Debt introduces fixed repayment obligations, which are manageable when revenue is steady but can become stressful during slower periods. A good rule of thumb? Make sure your monthly cash flow from the last six months comfortably covers your repayment amounts [1].

The real issue isn’t taking on debt - it’s choosing the wrong type of debt.

"The mistake is not using debt. The mistake is using the wrong debt without understanding how it actually behaves." - Drew Fallon, Co-Founder & CEO, Iris Finance [13]

When comparing offers, always calculate the effective annual rate (APR) so you can see the true cost. Flat fees and factor rates might seem simple, but they can translate into much higher annualized costs than they initially appear [12]. Here’s a quick comparison of popular debt options to help you decide:

| Feature | Traditional Bank Loan | SBA 7(a) Loan | SBA Microloan |

|---|---|---|---|

| Max Amount | Varies (up to $5M+) | $5 million [10] | $50,000 [10] |

| Typical Term | 1–5 years | 10 years (working capital) [9] | Up to 6 years [10] |

| Funding Speed | 2–8 weeks [10] | 30–90 days [7] | 2–4 weeks [10] |

| Min. Credit Score | 680–720+ | 680+ [7] | 620+ [10] |

| Down Payment | 20–30% | 10% (or less) [9] | Rarely required [10] |

| Best For | Established brands with assets | Long-term growth investments | Early-stage, small capital needs |

When traditional loans feel too slow or restrictive, many e-commerce founders explore funding models that better align with the way online businesses generate revenue. Instead of relying on collateral or credit scores, these models use real-time sales data from platforms like Shopify, Amazon, or Stripe to determine eligibility. This makes them accessible to businesses that may not meet the criteria for conventional loans.

Revenue-Based Financing (RBF) offers a more adaptable approach to funding by tying repayments to your actual sales performance. Here’s how it works: a provider advances you capital upfront, and in return, you agree to pay back a fixed percentage of your daily or weekly revenue - typically between 5% and 15% - until the agreed total is repaid. This total usually ranges from 1.2x to 1.5x the original amount borrowed. What makes RBF appealing is its flexibility; payments decrease during slower sales periods.

For example, in late 2025, a Shopify-based direct-to-consumer (DTC) brand generating $80,000 per month secured a $150,000 RBF advance with a 1.2x repayment factor. This meant they owed $180,000 in total. The funding allowed them to stock up on inventory for Q4, which tripled their monthly revenue. Impressively, they repaid the advance in just 150 days [17].

"RBF is the only capital that bends to your sales curve. Not the lender's amortization schedule." - Nautix Capital [17]

The RBF market is expected to grow significantly, from $6.4 billion in 2023 to $178.3 billion by 2033. Funding is often delivered within 24 to 72 hours, and because no equity is involved, founders retain full ownership of their businesses.

Merchant Cash Advances (MCAs) work differently. Legally, an MCA is not classified as a loan but as the purchase of your future receivables. This distinction places it outside many traditional lending regulations. With an MCA, you receive a lump sum upfront and repay it either through fixed daily ACH debits or as a percentage of your card sales.

Costs are expressed using a factor rate. For instance, a $100,000 advance with a 1.2x factor rate requires a total repayment of $120,000. Platforms like Shopify and Amazon have streamlined this process by offering pre-approved MCAs directly through seller dashboards, using internal sales data to make the funding process nearly seamless.

However, MCAs come with potential drawbacks. While marketed as flexible, many contracts require fixed daily payments, even during slower sales periods. Some providers address this with reconciliation processes, where they review bank statements and issue credits if overpayments occur during low-revenue periods.

These funding options are particularly useful for addressing the cash flow challenges of e-commerce businesses, complementing the debt strategies discussed earlier.

Both RBF and MCA bring speed and simplicity to the table. Funding is often available within 24 to 72 hours, without the need for collateral, and founders retain 100% ownership of their businesses. However, their cost structures can be more complicated than they initially seem.

"The flat fee is marketing. The effective APR is reality. The faster your ecommerce business grows, the more you actually pay in annualized terms for the same RBF advance." - Luca AI Intelligence Report [16]

RBF typically carries effective APRs between 15% and 35% annually, while MCA rates can range from 40% to a staggering 350%, depending on how quickly the advance is repaid. Additionally, many providers file UCC-1 blanket liens on business assets, which can limit access to traditional bank or SBA financing until the debt is cleared. Stacking multiple advances can also lead to daily payments consuming over 25% of revenue, creating severe cash flow challenges.

| Feature | Revenue-Based Financing (RBF) | Merchant Cash Advance (MCA) |

|---|---|---|

| Legal Structure | Loan or revenue-share agreement | Purchase of future receivables |

| Repayment Trigger | Percentage of daily/weekly revenue | Fixed daily debit or card sales % |

| Cost Expression | Flat fee (e.g., 6–12%) | Factor rate (e.g., 1.2x–1.5x) |

| Flexibility | High; adjusts with sales | Moderate; may include payment floors |

| Regulatory Status | Subject to lending regulations | Often unregulated |

| Effective APR Range | 15%–35% annually | 40%–350% |

When used wisely for short-term opportunities - like scaling a successful ad campaign or purchasing inventory ahead of peak seasons - these options can provide a meaningful boost. However, they can become risky when used to cover ongoing losses or when multiple advances are stacked without careful financial planning. Engaging fractional CFO services can help founders navigate these complex capital structures while maintaining long-term profitability.

Revenue-based financing and merchant cash advances are great for tackling short-term cash flow needs, but equity financing is a whole different ballgame. It’s designed for long-term goals - like launching a groundbreaking product, entering a new market, or bringing in top-tier leadership - where the timeline for returns is unclear, but the potential rewards could be massive. Unlike short-term funding solutions, equity financing focuses on fueling strategic growth that pays off over time.

The trade-off? Equity financing means giving up a piece of your company. This isn’t a temporary loan; it’s a permanent stake in your future profits and any eventual sale of the business.

"Debt is temporary; equity is forever." - Rachel Torres, Entrepreneurship Writer, WePitched [3]

Once you’ve decided equity financing is the right path, you’ll need to weigh your early-stage options. Angel investors are one route. These are usually high-net-worth individuals - often former entrepreneurs - who invest their own money in startups. Their investments typically range from $25,000 to $500,000 [6]. Angels tend to offer more flexible terms, act quickly, and are willing to take on more risk compared to institutional investors [18].

But angels bring more than just money. Many founders now look for "smart money" - angels who can provide industry connections, like introductions to distributors, manufacturers, or buyers, along with their financial backing [3]. If you’re choosing between two angels offering the same deal, go with the one who can open doors in your industry.

Equity crowdfunding platforms are another option, offering a dual benefit: raising funds while testing market interest. A successful campaign can prove demand for your product, making it easier to attract larger investors down the line [20]. Take Bushbalm, for example. This skincare brand started with just $900 and used crowdfunding as part of its early growth strategy, eventually scaling into an eight-figure business [19].

Venture capital (VC) is a different beast. These are institutional investors managing large pools of money, writing checks from $500,000 to $10M+ [6]. VCs look for startups with the potential to hit a $100M+ valuation and operate on strict 7–10 year timelines, which creates significant pressure for founders to deliver strong exits [3].

Only about 0.05% of startups ever secure venture capital [3], so it’s not the right fit for most businesses. VC funding makes sense if your brand has a defensible market position, excellent unit economics (think LTV:CAC ratios of 3:1 or better [19][6]), and the ability to scale quickly without costs rising proportionally. High-performing brands aiming for VC funding often target gross margins of 50% or more [6].

The VC landscape has shifted in recent years. The days of "growth at all costs" are over. Today’s investors prioritize sustainable growth and solid EBITDA margins over simply chasing revenue [6].

Every equity round you raise changes your company’s ownership structure, and these changes add up over time. As of 2024, the median dilution for Seed rounds was 20.5%, while Series A rounds averaged 20.1% [1]. By the time a company reaches Series B, founders typically own only 23% of the business collectively [1]. On top of dilution, VC funding often comes with strings attached, like board seats, protective provisions, and decision-making controls that require investor approval [18]. These conditions may not be deal-breakers, but they will influence how you operate your business.

Equity financing also impacts your ability to raise debt in the future. A clean and well-structured cap table makes it easier to secure loans or additional funding. On the flip side, messy cap tables - think informal equity promises or unresolved intellectual property issues - can raise red flags during due diligence and complicate future rounds [21]. For founders navigating these complexities, working with a fractional CFO or financial advisor, such as Phoenix Strategy Group, can help ensure your capital structure supports your goals instead of creating hurdles.

| Feature | Angel Investors | Venture Capital |

|---|---|---|

| Investment Size | $25,000–$500,000 [6] | $500,000–$10M+ [6] |

| Flexibility | High; flexible on terms and risk [18] | Low; rigid criteria, strict timelines [3] |

| Governance | Minimal; usually information rights [18] | High; board seats and protective provisions [18] |

| Exit Pressure | Low [3] | High; 7–10 year fund lifecycle [3] |

| Best For | Early-stage validation, brand building [3] | Rapid scaling to $100M+ valuation [3] |

Hybrid instruments like venture debt and convertible notes provide startups with funding options that avoid the immediate need for a full equity round. Here's how they work and when they make sense.

Venture debt is essentially a term loan that startups repay with interest over a set period. It's often available to companies that have recently raised institutional equity and need additional runway without diluting ownership further. Typically, lenders size these loans at 20%–35% of your latest equity raise [13]. For instance, if you just closed a $5M Series A, you might qualify for about $1M–$1.75M in venture debt.

The cost? By 2026, the annual all-in cost for venture debt is expected to be around 8%–11%, often structured as SOFR (Secured Overnight Financing Rate) plus 3%–5%, along with a one-time facility fee of 0.5%–2.0% of the committed capital [25][22]. Additionally, many deals include warrants - small equity options representing 0.1%–1.5% of your fully diluted shares [25]. This results in significantly less dilution compared to a full equity round.

"Adding six to twelve months of runway might cost you just 2–4% of your company instead of 15–25%." - Ascent CFO Solutions [23]

However, venture debt usually comes with operational covenants. These might require maintaining a minimum cash balance or hitting specific revenue targets. It's crucial to model how these covenants will hold up during slower periods and to plan for the balloon payment at the end of the term [26]. Despite these structured terms, venture debt offers a compelling way to extend runway without heavy equity dilution.

Convertible notes are another hybrid option, functioning as debt that converts into equity during a future priced round rather than being repaid in cash. This makes them particularly popular at the Seed stage, where agreeing on a valuation can be tricky. Conversion typically happens at a discount (often 15%–20%) or under a valuation cap that protects investors.

SAFEs (Simple Agreements for Future Equity) are similar but are not technically debt. Instead, they provide a contractual right to future equity without accruing interest.

One thing to watch out for: multiple convertible notes can stack up and compound dilution. Founders should carefully track outstanding convertible instruments to avoid making Series A negotiations unnecessarily complicated. Understanding these nuances allows founders to choose the right tool for their funding strategy.

Venture debt works best right after a successful equity round. With recent investor backing and a solid cash position, lenders are more likely to offer favorable terms [24]. Using venture debt at this stage can extend your runway by 6–12 months, giving your company time to grow its valuation before the next funding round. This approach supports the broader goal of maintaining cap table integrity while optimizing your financial strategy.

"The longer you push off a round - it's linear, right? If you're doing your job, the company's becoming more and more valuable every day. So you want to push off that next round as far as you can." - David Johnson, Co-founder & CEO, Rooled [24]

For startups in industries like e-commerce, venture debt is especially useful for predictable, revenue-driven needs, such as seasonal inventory builds or scaling proven marketing channels [25]. On the other hand, convertible notes are better suited for the Seed stage, where speed is critical, and lengthy valuation negotiations can be avoided. These instruments should be used to hit key milestones, not just to cover burn rates.

Need help navigating these options? A fractional CFO from Phoenix Strategy Group can model dilution scenarios and evaluate covenant impacts before you commit.

After reviewing different debt, equity, and hybrid funding options, it's clear that the ideal mix depends on your business's growth stage and strategic goals. For e-commerce startups, aligning funding strategies with specific needs - like capital requirements and ownership preferences - is critical.

Every dollar raised should directly contribute to growth. As noted earlier, it’s wise to exhaust non-dilutive funding options - such as SBA loans, revenue-based financing, or inventory lines - when seeking amounts under $500,000. Reserve equity funding for transformative opportunities, like entering new retail markets or building proprietary technology, where the potential return justifies dilution.

Here’s a quick breakdown of how different funding types align with specific needs:

| Funding Type | Best Use Case | Key Consideration |

|---|---|---|

| Equity | Strategic growth, retail expansion, technology | Permanent dilution with a higher long-term cost |

| Debt | Inventory, seasonal demands, working capital | Requires steady cash flow; preserves ownership |

| Bootstrapping | Organic, sustainable growth | Founder control and long-term value maximized |

A well-thought-out funding mix is essential for sustainable growth. Approaching capital raises with strong cash flow visibility - ideally 13–26 weeks ahead - positions you to secure better terms and choose the right funding tools. Services like Phoenix Strategy Group help e-commerce founders refine their financial strategies by analyzing unit economics, exploring dilution scenarios, and uncovering recoverable profit (often between $500,000 and $2M for mid-sized brands). This preparation ensures founders can raise capital with clarity and confidence.

"If you don't have a specific capital need tied to a specific return, preserving ownership often compounds better than accelerating with dilution." - Eightx [2]

Ultimately, the focus isn’t on raising the maximum capital possible. It’s about securing the right amount, at the right time, with the right structure to support your business's long-term success.

If your startup has a steady cash flow and can manage fixed payments, debt financing might be the way to go. It allows you to keep full ownership of your business, and the interest payments are often tax-deductible. On the other hand, if your revenue is unpredictable or your company is growing quickly, equity financing could be a better fit. While it doesn’t require repayment, it does mean giving up a portion of ownership, which could also impact your level of control. Many startups choose to combine both approaches to strike a balance between securing funds and minimizing ownership dilution.

The effective APR for revenue-based financing (RBF) and merchant cash advances (MCA) often ends up being much higher than the advertised flat fees or factor rates suggest. In many cases, it can range anywhere from 20% to 56% or more.

This happens because these financing models rely on flat fees rather than compounding interest. The catch? If your business experiences rapid revenue growth and repays the loan faster, the annualized APR increases significantly. This can lead to unexpected costs that might catch businesses off guard.

Venture debt and convertible notes are great options if you're looking to limit equity dilution, retain control, or hit key valuation milestones. Venture debt works best if your business has steady revenue and you need extra runway after raising equity. On the other hand, convertible notes are a solid choice during the seed stage when you need quick funding but want to postpone valuation negotiations. While both options help you avoid immediate dilution, they come with repayment responsibilities, so it's crucial to evaluate your cash flow and potential risks thoroughly.