Published on

June 2, 2026

Non-dilutive funding allows SaaS companies to raise capital without giving up equity. This is ideal for businesses looking to maintain ownership while scaling. Key options include:

Each funding type serves different needs, from scaling operations to funding R&D. The right choice depends on your business stage, cash flow requirements, and growth strategy. For example, RBF is ideal for predictable investments like marketing or hiring, while grants and tax credits suit R&D-heavy projects.

Quick Comparison:

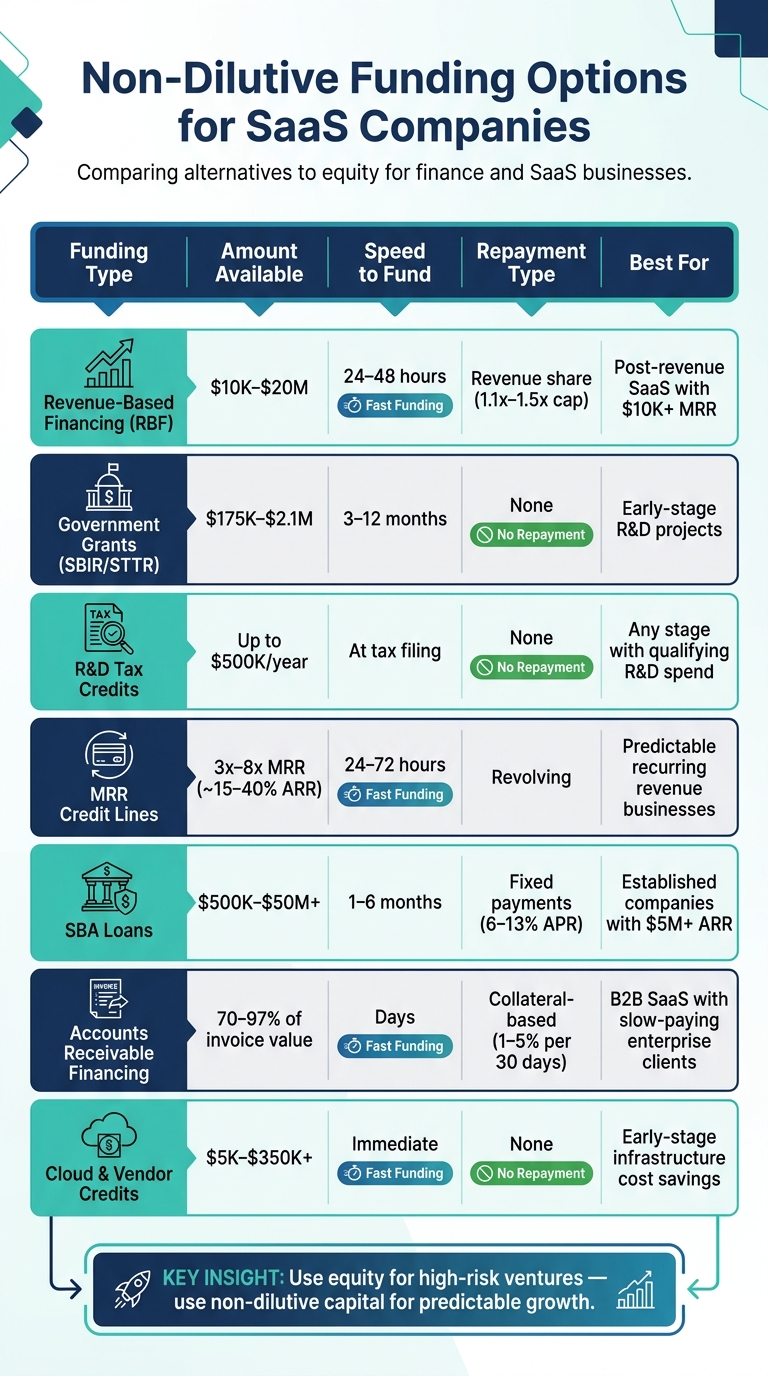

| Funding Type | Amount | Speed | Repayment | Best For |

|---|---|---|---|---|

| Revenue-Based Financing | $10K–$20M | 24–48 hours | Revenue share | Post-revenue ($10K+ MRR) |

| Government Grants | $175K–$2.1M | 3–12 months | None | R&D, early-stage |

| R&D Tax Credits | Up to $500K/yr | At tax filing | None | Companies with R&D expenses |

| MRR Credit Lines | 3x–8x MRR | 24–72 hours | Revolving | Predictable recurring revenue |

| SBA Loans | $500K–$50M+ | 1–6 months | Fixed payments | Established companies ($5M+ ARR) |

| Accounts Receivable Financing | 70–97% of invoice value | Days | Collateral-based | B2B SaaS with slow-paying clients |

| Cloud & Vendor Credits | $5K–$350K+ | Immediate | None | Early-stage infrastructure savings |

Choose non-dilutive funding for predictable, low-risk investments and equity for high-risk ventures. This approach ensures you grow efficiently while keeping ownership intact.

Non-Dilutive Funding Options for SaaS Companies: Quick Comparison Guide

Revenue-based financing (RBF) offers upfront capital in exchange for a fixed percentage of your monthly gross revenue until you repay a predetermined cap. Payments adjust based on your revenue - rising during periods of growth and easing during slower months. Typically, repayment caps range between 1.1x and 1.5x the borrowed amount. For instance, if you receive a $200,000 advance with a 1.25x cap, you would repay $250,000 in total, with the timeline depending on your revenue. The monthly revenue share usually falls between 2% and 10% of gross revenue [6][10].

Unlike traditional lending, RBF focuses on metrics like monthly recurring revenue (MRR), retention rates, and gross margins rather than physical assets or personal credit scores [11][12].

"Revenue-based financing is designed to move at the speed of your business. It provides the growth capital you need while offering a buffer that can protect your liquidity during slower periods." - Ryan Rosett, Founder, Credibly [8]

Funds can often be disbursed in just 24 to 48 hours, as many RBF providers integrate directly with billing platforms like Stripe or Chargebee to verify revenue. This speed and flexibility make RBF particularly effective for SaaS businesses with reliable, recurring revenue streams.

RBF is especially well-suited for SaaS companies with steady MRR. To qualify, providers generally require $10,000 to $50,000 in MRR and at least 12 months of revenue history [11][12]. Advances typically range from 2x to 6x your monthly MRR [6][10].

The ideal scenario for RBF is when you have a clear plan to invest the capital into areas with a proven return on investment. Examples include scaling paid acquisition efforts with a predictable customer acquisition cost (CAC) payback period or hiring sales reps to expand a successful sales model. Thanks to SaaS gross margins often falling between 60% and 80%, the revenue-sharing structure is manageable without placing undue strain on operations [7][9].

A common misunderstanding is equating the repayment cap with an interest rate - it’s not the same.

"The repayment cap is not your cost of capital. The effective APR on RBF depends on how fast you repay, which depends on how fast your revenue grows." - Aleksandar Stojanovic, CEO & Founder, Fiscallion [6]

For example, with a 1.25x cap and a 12-month repayment period, your effective annual percentage rate (APR) could exceed 40%. While faster growth accelerates repayment, it also increases cash outflows during high-revenue months - a dynamic often referred to as the "success tax."

To prepare, model various revenue scenarios, including minimal growth (around 1% MRR), potential declines (15–20%), and your base case [6]. Watch out for "floor" clauses, which set minimum monthly payments and can limit RBF’s flexibility. Additionally, if the term sheet includes warrants, it’s likely a hybrid product, not pure RBF [6].

Government grants and tax credits can be excellent tools to fund growth without giving up equity, complementing revenue-based financing and other non-dilutive funding strategies.

Federal grants provide non-repayable funding, especially for high-risk R&D projects. Two key programs for SaaS companies are the Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs. Together, these initiatives distribute about $4 billion annually across 11 federal agencies [14]. For SaaS founders, the National Science Foundation (NSF) - branded as "America's Seed Fund" - is particularly supportive of projects related to software, AI, and blockchain [13][17].

Here’s how NSF funding works:

A major difference between SBIR and STTR lies in their collaboration requirements. STTR mandates a formal partnership with a research institution (like a university, which must handle at least 30% of the work), while SBIR allows small businesses to execute projects independently.

"SBIR and STTR are still powerful non-dilutive funding tools, but the winning playbook now depends more on topic discipline, security readiness, and transition credibility than on submitting broadly." - Ridgeway Financial Services [17]

NSF-funded SaaS projects often tackle genuine technical challenges. Examples include an AI-driven financial coaching platform using advanced machine learning and blockchain-enabled clinical registries designed to address data integrity issues. These projects focus on solving technical uncertainties rather than incremental product updates.

If grants aren’t a fit for your business, R&D tax credits can be another way to reduce costs.

The federal R&D tax credit offers a dollar-for-dollar reduction in tax liability, covering up to 13% of qualified research expenses (QREs) [22]. Eligible costs include U.S.-based engineering wages, cloud computing expenses, and contract development fees [5][24].

To qualify, your R&D activities must meet a four-part test:

"It applies to businesses of all sizes, and you don't have to be profitable to take advantage of the credit." - Ben Murray, SaaS CFO [19]

For early-stage or pre-revenue SaaS companies, the payroll tax offset can be a game-changer. If your company has less than $5 million in gross receipts and fewer than five years of revenue history, you can apply up to $500,000 annually to offset employer Social Security taxes - even if you’re not yet profitable [5][20]. However, this election must be made on your original tax return, not an amended one.

Starting in 2025, the "One Big Beautiful Bill Act" (OBBBA) introduces a significant change: domestic R&D expenses incurred after December 31, 2024, can be fully deducted immediately, while foreign R&D expenses will still need to be amortized over 15 years [21][23].

Both SBIR/STTR grants and R&D tax credits require meeting specific criteria and navigating detailed application processes. For SBIR/STTR, your project must demonstrate technical uncertainty. Projects involving new algorithms, innovative AI/ML models, or novel approaches to data integrity are strong candidates. Routine software updates, UI improvements, or dashboard tweaks generally don’t qualify [16][17].

To get started:

Beyond grants and tax credits, SaaS companies have access to debt-based funding options tailored to their recurring revenue models. These funding methods allow businesses to secure capital without giving up equity, making them an appealing choice for many SaaS founders.

An MRR (Monthly Recurring Revenue) credit facility is a revolving line of credit where borrowing limits are tied to your MRR rather than physical assets like property or equipment. Typically, lenders offer credit lines sized at 3x–8x MRR, which translates to about 15%–40% of your Annual Recurring Revenue (ARR) [25][28].

This structure is particularly advantageous for SaaS companies. It works much like a business credit card but is scaled to your subscription revenue. You can draw funds when needed, repay, and borrow again, with interest charged only on the amount you use. This can save up to 24% compared to traditional term loans [27]. Specialty lenders in the SaaS space often charge 10%–14% APR, and many can approve and fund these credit lines within 24–48 hours [26][28].

To qualify, lenders typically look for:

As your MRR grows, the borrowing limit increases, aligning the credit facility with your company’s growth trajectory.

"The thing that kills companies isn't the coupon - it's the covenants." - SaaSCEO [28]

However, these facilities come with strict covenants tied to metrics like retention and burn rate. Failing to meet these requirements could lead to breaches, so maintaining strong retention figures is critical [27][28].

Term loans provide a lump sum that is repaid over a set period, typically 36–48 months. These loans are ideal for one-time investments, such as launching a major product feature or acquiring another company.

SBA 7(a) loans, backed by the U.S. government, offer some of the lowest interest rates in the market - ranging from 6% to 13% APR. However, the approval process can take 30 to 90 days and requires extensive documentation [25].

One key consideration with term loans is the amortization cliff. Many term loans start with an interest-only period before transitioning to full principal-and-interest payments. For instance, on a $2 million loan at 13% interest, monthly payments could jump from around $21,667 during the interest-only phase to approximately $95,200 once full amortization begins [28]. It’s crucial to model this transition over the loan term and account for potential slowdowns, such as a 20% dip in new bookings.

"Used correctly, venture debt is a timing tool for a business with already-proven unit economics and a repeatable sales motion. It accelerates a working machine. It cannot fix a broken one." - SaaSCEO [28]

Understanding these repayment structures is essential to aligning your funding strategy with your cash flow needs.

Here’s a quick breakdown of the key differences between MRR credit facilities, term loans, and SBA 7(a) loans:

| Feature | MRR Line of Credit | Term Loan | SBA 7(a) Loan |

|---|---|---|---|

| Repayment | Revolving; interest on drawn funds only | Fixed monthly payments on a lump sum | Fixed monthly payments (up to 25-year terms) |

| Collateral | Recurring revenue (MRR/ARR) | Often requires personal guarantees or assets | Government-backed; personal assets often required |

| Approval Speed | 24–72 hours | 1–2 weeks | 30–90 days |

| Best Use Case | Working capital, cash flow smoothing | One-time investments (e.g., acquisitions) | Long-term, low-cost debt for established firms |

| Typical Cost | 10–14% APR | 11–17% APR | 6–13% APR |

| Warrant Coverage | 0% | 0.5%–2.0% | None |

MRR credit facilities are particularly effective for funding customer acquisition when your unit economics, such as Lifetime Value (LTV) to Customer Acquisition Cost (CAC), are solid. On the other hand, if you’re tackling a high-cost, one-time project with clear timelines and returns, a term loan might be the better option.

Enterprise SaaS clients often operate on Net 30–90 day payment terms, which can delay cash flow even after services have been delivered. Accounts receivable (AR) financing offers a solution by converting unpaid invoices into immediate cash, giving businesses the liquidity they need.

There are two primary ways to approach this. With an AR loan, your unpaid invoices act as collateral, allowing you to keep them as assets. On the other hand, invoice factoring involves selling the invoice to a third party (a factor), who then collects payment directly from your customer. Typically, lenders will advance 70% to 90% of the invoice’s value. For invoices with excellent creditworthiness, advance rates can climb as high as 97% [31].

"The factor underwrites the credit risk of your customers, not your business, which is why factoring is sometimes available to companies that wouldn't qualify for a bank line of credit." - David Luther, Corpay [30]

Factoring fees generally range from 1%–5% per 30 days, translating to an annualized APR of 15%–60% [30]. For SaaS businesses, monthly rates often fall between 1.5% and 3.5%, depending on factors like churn and Net Revenue Retention (NRR) [29]. To secure the most favorable advance rates, prioritize annual or multi-year contracts over month-to-month subscriptions. These longer-term agreements often qualify for advance rates that are 0.5x to 1.0x higher [29]. Additionally, maintaining an NRR above 110% is a strong indicator of qualifying for the upper tier of advance rates [29].

This financing method pairs well with other non-dilutive funding options. It provides immediate working capital, which can be reinvested into cost-saving strategies, like securing cloud credits.

While AR financing focuses on boosting cash flow, cloud credits help SaaS companies cut down on infrastructure costs. Major cloud providers offer generous credit programs to support early-stage businesses, and the opportunities available in 2026 are impressive.

| Program | Max Credit Value | Primary Eligibility | Duration |

|---|---|---|---|

| Google Cloud Scale AI | $350,000 | AI-first, equity-funded | 2 years |

| Cloudflare High Growth | $250,000 | High-growth startups | 1 year |

| Microsoft Founders Hub | $150,000 | Investor-backed (Premium) | 1 year |

| AWS Activate Portfolio | $100,000 | VC/accelerator-backed | 1–2 years |

| DigitalOcean Hatch | $100,000 | Accelerator-affiliated | 12 months |

To maximize these credits, here are a few tips: use a corporate email domain when applying (avoid Gmail, as it often leads to rejection), and only activate the credits once your infrastructure is set up, as the expiration period begins immediately upon activation [32]. Joining aggregator platforms like NVIDIA Inception or Stripe Atlas can also help, as membership often unlocks higher credit tiers automatically [32].

AR financing and cloud credits are most effective when used as part of a broader non-dilutive funding strategy. While tools like MRR credit facilities or term loans provide growth capital, AR financing ensures cash flow isn’t bogged down by slow-paying invoices. Simultaneously, cloud credits help lower infrastructure costs, reducing monthly burn rates.

"Working capital discipline is one of the cheapest forms of growth funding available to a subscription business." - Ayush Agarwal, Co-founder & CPTO, Dodo Payments [33]

For a SaaS company with $10M in ARR, every 10 days of Days Sales Outstanding (DSO) ties up about $275,000 in working capital [34]. By combining AR financing with cloud credits, businesses can unlock this trapped cash and reinvest it into growth - without giving up equity. This approach not only shortens DSO but also trims infrastructure expenses, making it a smart way to manage cash flow while scaling.

Finding the right funding option for your SaaS company depends on where you are in your growth journey and how much capital you need.

Start by considering the cost of capital. This includes origination fees, prepayment penalties, and warrants. For example, revenue-based financing (RBF) typically carries an APR equivalent of 12–30%, while SaaS-focused bank loans are closer to 6–12% APR [4]. That difference can add up significantly over time.

Timing is another critical factor. If you need capital quickly to take advantage of a proven growth opportunity, traditional bank loans, which can take 2–6 months to process, may not be practical. In contrast, RBF can provide funding within 24–48 hours, while grants might take anywhere from 3–12 months [4][1]. Match the funding timeline to the urgency of your business needs.

Also, think about your debt service capacity. A good rule of thumb is to keep your total debt payments below 20–25% of your monthly revenue. Exceeding this limit can turn growth-focused capital into a cash flow burden [4]. To be safe, stress-test your projections by assuming a 10% interest rate to ensure you can cover payments, even during slower months.

"Capital is a tool, not a trophy. Stop measuring your success by the size of the round you announced on LinkedIn and start measuring it by the percentage of the company you still own." - Rachel Torres, Entrepreneurship Writer, WePitched [3]

These considerations will help you compare funding options effectively, as shown in the table below.

| Financing Type | Amount | Speed | Dilution | Best For |

|---|---|---|---|---|

| Revenue-Based Financing | 1–4x MRR | 24–48 hours | None | Bootstrapped SaaS, $10K+ MRR |

| Venture Debt | 20–35% of last round | 4–8 weeks | 0.5–2% (warrants) | VC-backed companies |

| Bank / SBA Loans | $500K–$50M+ | 1–6 months | None | $5M+ ARR, established companies |

| SBIR/STTR Grants | $175K–$2.1M | 3–12 months | None | Early-stage R&D, Pre-seed to Seed |

| R&D Tax Credits | Up to $500K/yr | At tax filing | None | Any stage with qualifying R&D spend |

| AR Financing | 70–97% of invoice value | Days | None | Companies with slow-paying enterprise clients |

Once you've narrowed down the options, focus on aligning the funding type with your specific business goals. Non-dilutive debt is ideal for predictable outcomes, such as scaling a marketing channel with proven returns, hiring SDRs for repeatable sales processes, or covering infrastructure expenses. On the other hand, equity funding is better suited for high-risk, high-reward investments.

If you're planning for an exit or a future equity round, your funding decisions now will shape your leverage later. Companies that scale efficiently using non-dilutive capital - while maintaining strong metrics like high NRR, clean financials, and low churn - are more attractive to lenders and acquirers. These businesses demonstrate financial discipline, not just growth for growth's sake. The best time to secure a credit facility or RBF line is when you have at least 12 months of runway and don't urgently need the funds; this is when you'll secure the most favorable terms [3].

Securing non-dilutive capital takes more than just ambition - it demands meticulous preparation. Lenders and grant reviewers expect clean financial records, clear metrics, and a strong growth narrative. Phoenix Strategy Group (PSG) sets up what they call financial mission control by integrating models, dashboards, and audit-ready data. This ensures a clear financial picture that’s ready to present at a moment’s notice. They overhaul charts of accounts, correct past data issues, and implement GAAP-compliant accrual accounting. So, when lenders request a year’s worth of financials, PSG’s clients can deliver within hours. Every step of this process ties directly to the funding strategies mentioned earlier.

"Startup financial models are the mission control of your startup." - Phoenix Strategy Group [35]

When it comes to non-dilutive funding, strong financial metrics are non-negotiable. PSG steps in to ensure SaaS companies meet these critical benchmarks. Their FP&A systems track vital metrics like MRR, churn, LTV:CAC, and burn rate in real time. Meanwhile, finance automation slashes manual bookkeeping time by 80%, delivering audit-ready results [36]. Their fractional CFOs go a step further, using 13-week cash flow forecasts to stress-test repayment capacity, ensuring companies are prepared for the scrutiny of lenders. This rigorous approach gives SaaS companies a clear advantage in securing funding.

Here’s a closer look at PSG’s services and how they align with funding success:

| Service | What It Delivers | Why It Matters for Funding |

|---|---|---|

| Fractional CFO | Stabilizes cash flow, advises on debt/equity mix | Strengthens lender confidence, minimizes dilution risk |

| FP&A & Modeling | Provides driver-based forecasts, tracks MRR and churn | Helps qualify for RBF and MRR credit lines |

| Bookkeeping | Automates AP/AR, ensures accrual accounting | Produces audit-ready financials |

| Data Engineering | Creates real-time CAC vs. LTV dashboards, integrates ERP systems | Enables compelling, data-backed narratives for investors |

With their comprehensive suite of services, PSG has helped clients secure over $200 million in capital in the past year alone, working with more than 240 portfolio companies [37][38]. Their impressive track record includes assisting Robin Healthcare in raising a $50 million Series B and supporting General Assembly through a $413 million acquisition [37].

"As our fractional CFO, they accomplished more in six months than our last two full-time CFOs combined." - David Darmstandler, Co-CEO, DataPath [37]

For SaaS founders navigating non-dilutive funding, having a partner like PSG to handle financial modeling, compliance, and lender preparation can significantly lighten the operational load while increasing the likelihood of funding success.

Non-dilutive funding offers several options for SaaS founders to grow without giving up equity. Revenue-based financing (RBF) is ideal when you have a proven sales strategy and need funds to scale operations. Government grants, like SBIR, are perfect for deep research and development projects, though they can take 6–18 months to secure. MRR credit lines provide flexible cash tied to recurring revenue, and cloud credits from providers like AWS can save significant infrastructure costs without requiring repayment.

The main idea? Use equity for high-risk ventures and non-dilutive capital for predictable growth. Rachel Torres from WePitched sums it up well:

"Equity is the most expensive way to pay for a marketing campaign or a new engineering hire." [3]

This approach helps founders hit critical milestones while retaining ownership. For instance, DevPulse leveraged a $400,000 RBF facility to double its ARR from $1.2M to $2.4M. [3]

By combining these strategies, SaaS founders can create businesses that are both resilient and primed for growth.

To put these strategies into action, start by evaluating your unit economics. Lenders in 2026 expect metrics like a Magic Number above 1.0, an LTV/CAC ratio over 3.0, and well-organized financial records. Sloppy or inaccurate financials can lead to immediate rejection. [3]

It’s also wise to secure a credit line or RBF facility early, ideally with at least 12 months of runway. If your financials aren’t in order, consider working with Phoenix Strategy Group. Their fractional CFO and FP&A services can ensure your books are audit-ready, so you’re prepared to act when funding opportunities arise.

"Runway is not just protection; it is strategic flexibility." - Shraddha Chouhan, CMO, Float Finance [2]

When deciding between revenue-based financing (RBF) and an MRR credit line, it all comes down to what your business needs at the moment.

With RBF, you get a lump sum upfront, which you repay as a percentage of your revenue. This option works well if you need quick, one-time funding to fuel growth. On the other hand, an MRR credit line acts as a revolving facility, giving you ongoing access to funds that adjust based on your monthly recurring revenue (MRR).

RBF is typically faster to secure, making it a go-to for immediate cash needs. Meanwhile, an MRR credit line offers more flexibility in repayment, making it a better fit for businesses seeking consistent liquidity.

For SaaS companies, qualifying work needs to pass a four-part test. First, it must serve a permitted purpose, such as improving software. Second, it should address technical uncertainty, meaning the outcome isn't immediately clear. Third, it must rely on computer science or engineering principles. Finally, it should involve experimentation, like prototyping or testing new ideas.

For SBIR/STTR programs, the focus shifts slightly. These programs require R&D efforts that align with federal missions and include a clear plan for commercialization. Activities that typically qualify might include designing systems architecture, conducting complex testing, or creating internal tools to tackle unresolved technical challenges.

To get a clear picture of your actual cost of capital for non-dilutive financing options, you need to look beyond the surface-level rates. For revenue-based financing, estimate the effective APR by forecasting monthly repayments tied to your revenue growth until you hit the repayment cap. With venture debt, don't forget to factor in the dilutive effect of warrants and additional fees. Always ask for a detailed, all-in cost estimate to fully grasp the total financial commitment you're making.