Published on

March 25, 2026

Tax residency rules are crucial for founders moving abroad because they determine where your income is taxed. Mistakes can lead to hefty bills, especially during business exits. Here's what you need to know:

Planning ahead - ideally 18-24 months before relocating - can help founders restructure assets, avoid double taxation, and minimize risks. For example, moving to a no-income-tax state like Texas before going abroad can simplify matters. Proper documentation, expert guidance, such as fractional CFO services, and understanding local tax incentives (e.g., Singapore's lack of capital gains tax) are essential for a smooth transition.

For many countries, tax residency starts with the 183-day rule. If you spend more than half the year - 183 days or more - within a country's borders, you're generally considered a tax resident and required to pay taxes on your worldwide income. But this isn't a one-size-fits-all approach, and some countries have different thresholds.

For example, Switzerland uses a 90-day benchmark, while the UK’s threshold can drop to just 16 days if you have strong ties there. The United States takes a slightly different approach with a three-year weighted formula: 31 days in the current year, combined with portions of the prior two years, must total 183 days. This formula often averages to about 122 days annually.

Here's another detail to keep in mind: most countries treat any part of a day as a full day. Even if you arrive just before midnight, that day counts. To avoid disputes, it's crucial to maintain accurate travel records - use GPS apps, flight itineraries, and credit card statements to back up your claims. In Italy, for instance, the 183-day rule is absolute. If you're physically present for that amount of time, you're a tax resident, regardless of where your family or business is based.

While physical presence is a key factor, it's not the only one. Tax residency also depends on personal and economic connections, as explained below.

Physical presence is just part of the story. Tax authorities also look at where your center of vital interests lies - essentially, your personal, social, and financial connections. For entrepreneurs and business owners, this can get particularly tricky since professional ties often weigh heavily. Managing these complexities often requires the oversight of a fractional CFO to ensure financial and tax alignment across borders.

Authorities examine various factors, such as where your spouse and children reside, where you own property, where your primary bank accounts are located, and where you conduct business. For instance, if you hold board meetings in Barcelona but claim tax residency in Dubai, tax authorities might argue that Spain is your center of economic activity. In countries like Germany or France, you could be considered a resident even without spending a single day there, as long as you maintain a home (like a rented apartment) or if the country is deemed your economic hub.

"A company without personal residency alignment is a red flag factory." - JLW Business Advisors [4]

To successfully shift your tax residency, you’ll need to sever ties with your previous country. This often involves steps like selling or leasing out your home, relocating your family, closing local bank accounts, stepping down from local boards, and canceling memberships. Document these changes thoroughly with lease agreements, school enrollment records, and utility bills to prove that your center of vital interests has moved.

Sometimes, you may find yourself a tax resident in two countries at the same time. This can lead to double taxation, especially during transitional periods when you meet residency requirements in both your old and new locations.

Fortunately, Double Taxation Agreements (DTAs) help resolve these conflicts. These agreements often include "tie-breaker rules" based on the OECD Model Tax Convention. The rules follow a hierarchy: first, where you have a permanent home; second, your center of vital interests; third, your habitual residence; and finally, your nationality. If none of these factors settle the issue, the tax authorities of the two countries may negotiate directly.

One critical document to establish your new residency is a Tax Residency Certificate (TRC) from your new country. This certificate is essential if your former country challenges your claim of non-residency. For instance, over 860,000 UK taxpayers reported foreign income in 2025, and tax authorities in high-tax regions like New York - which collected over $1 billion from residency audits between 2013 and 2017 - are becoming increasingly aggressive in scrutinizing residency changes [1][6].

Understanding how dual residency is resolved is a key step in managing the tax implications of international moves. These rules and treaties form the foundation for navigating the complexities of tax residency during relocations.

If you're a founder planning to move abroad, understanding how residency changes impact capital gains is crucial. Countries like the United States, Canada, Australia, Germany, and the Netherlands impose exit taxes. These taxes treat your assets as if they were sold at fair market value the day before you leave, meaning you'll owe taxes on unrealized gains - even if no actual sale occurs [5][1].

For U.S. citizens and green card holders, the situation gets even trickier. The U.S. taxes worldwide capital gains regardless of where you live. Moving abroad won't free you from these obligations unless you formally renounce your citizenship or green card [7][1].

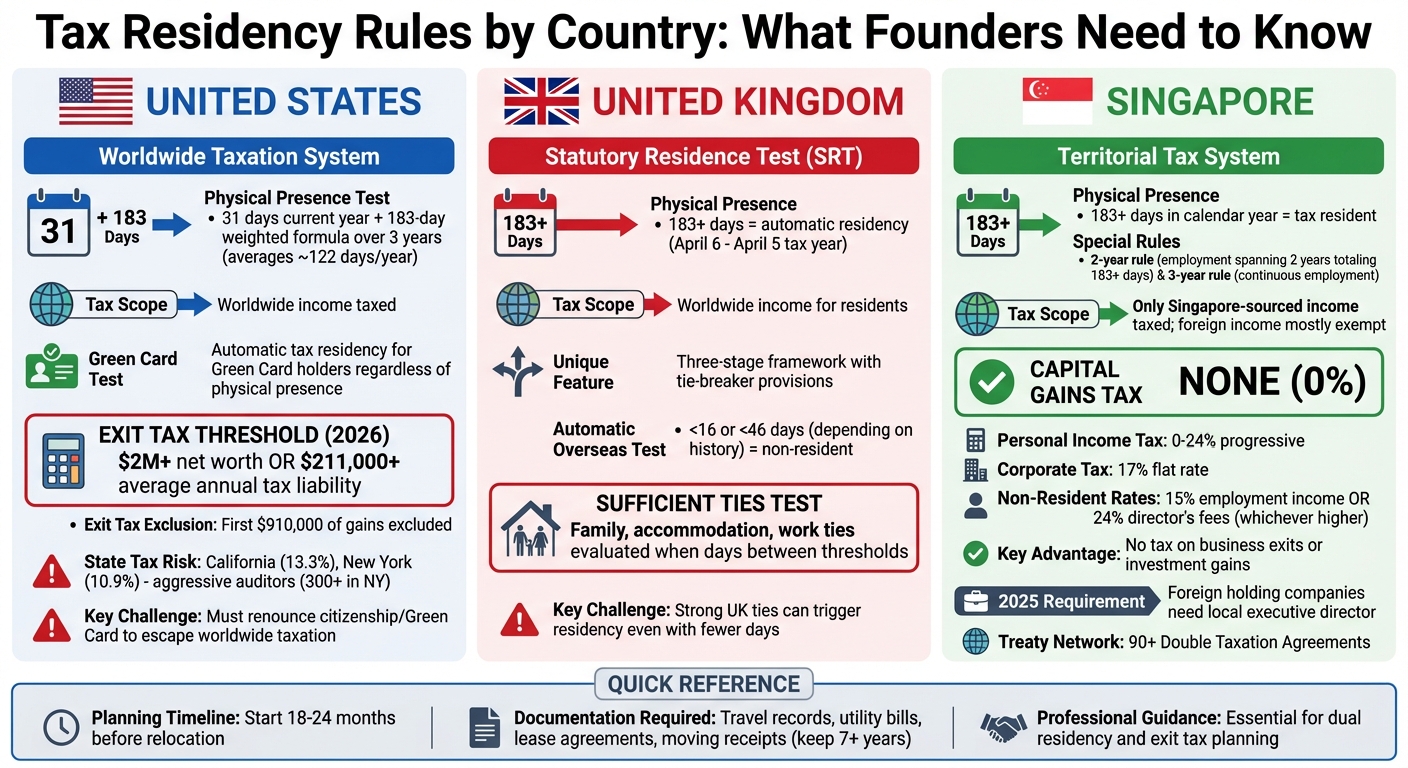

Starting in 2026, the exit tax applies to "covered expatriates." These are individuals with a net worth of $2 million or more or an average annual tax liability exceeding $211,000 over the past five years. While the first $910,000 of gains is excluded, anything above that is taxed as capital gains [2].

State-level taxes can complicate things further. States like California and New York are notorious for asserting tax rights on business exits, even after you've moved abroad. California, with its top marginal rate of 13.3%, does not recognize the federal Foreign Earned Income Exclusion (FEIE) or allow foreign tax credits, which can lead to double taxation [2].

Consider this example: In 2025/2026, a Silicon Valley tech founder with $15 million in unrealized gains planned to relocate to Singapore. By restructuring equity from common to preferred shares 18 months prior - leveraging a valuation discount and timing the move during a valuation dip - they reduced a potential $5 million tax bill to $1.5 million, cutting their tax liability by 70% [5].

"Exit tax isn't a penalty for leaving - it's a trap for the unprepared. The difference between losing millions and paying nothing often comes down to strategy, structure, and execution." - Project Black Ledger [5]

These examples highlight the importance of careful planning and compliance, which we'll explore further in the next section.

Relocating abroad adds layers of complexity to your tax obligations. U.S. citizens and green card holders must report all global income - including wages, investment returns, and business income - even while living overseas [9]. If your foreign financial accounts exceed $10,000 at any point in the year, you'll need to file a Foreign Bank Account Report (FBAR). Penalties for willful non-compliance can be steep, reaching the greater of $100,000 or 50% of the account balance per violation [1][9].

Under FATCA (Form 8938), you must report specified foreign financial assets if their value exceeds certain thresholds - usually $200,000 at year-end or $300,000 at any point during the year for those living abroad [1][8]. Founders with stakes in foreign entities may also need to file additional forms, such as 5471 (foreign corporations), 8865 (partnerships), or 8858 (disregarded entities). Failing to file these forms typically results in penalties of $10,000 per missed filing [8].

Even after moving abroad, state taxes can follow you. States like California and New York are particularly aggressive, often continuing to assert tax rights unless you’ve thoroughly documented your residency change. These states employ hundreds of auditors specifically to monitor high-income taxpayers [2].

"The burden of proving domicile change under state tax residency rules lies entirely with the taxpayer." - George Dimov, President & Managing Owner of Dimov Tax [2]

To protect yourself, maintain detailed records for at least seven years. Keep documents such as foreign leases, utility bills, flight itineraries, and moving receipts in a "compliance folder" to defend against residency audits. Also, note that while the Foreign Earned Income Exclusion allows qualifying individuals to exclude up to $132,900 of foreign earnings from U.S. tax in 2026, this does not extend to capital gains from a business exit [9].

Given these challenges, effective planning is essential to minimize tax exposure. Ideally, you should begin planning 18–24 months before your move to allow time for strategic asset restructuring and to document your intentions [5]. For example, exchanging common shares for preferred stock can create valuation discounts, reducing the taxable base for exit taxes [5].

For U.S. founders, relocating to a no-income-tax state like Florida, Texas, or Nevada before moving abroad can simplify the process and help avoid entanglements with high-tax states like California or New York [2][10]. Some countries also offer appealing tax incentives for new residents. Spain’s Beckham Law, for instance, provides a 24% flat tax on Spanish-sourced income up to €600,000 for six years. Similarly, Italy offers a flat tax of €100,000 per year on all foreign-sourced income for up to 15 years [1].

Poor planning can be costly. Take the case of a Dutch manufacturing business owner with a €12 million enterprise. By implementing a multi-phase strategy 18 months before moving to Portugal - such as separating operational and holding companies and using a Dutch cooperative structure - they reduced their effective exit tax rate from 26.9% to 12.4%, saving over €1.7 million [5].

Phoenix Strategy Group specializes in helping growth-stage companies prepare for exits. Their fractional CFO and M&A advisory services can guide founders through the complexities of tax residency planning, ensuring compliance while minimizing tax burdens across jurisdictions.

Tax Residency Rules Comparison: US, UK, and Singapore for Founders

In the U.S., residents are taxed on their worldwide income. You qualify as a resident if you either hold a Green Card or meet the Substantial Presence Test, which uses a weighted formula over three years to determine residency [11][13][14].

The Green Card Test applies to anyone with lawful permanent resident status (Form I-551). This status makes you a tax resident, even if you spend most of your time outside the U.S., and it remains in effect until you formally renounce it or it is administratively terminated [12][14]. The Substantial Presence Test, on the other hand, applies to non-citizens who spend at least 31 days in the U.S. during the current year and meet a 183-day threshold calculated over three years [13][14].

"Once you obtain US tax residency under the GCT [Green Card Test], you must report all your worldwide assets and pay taxes on your worldwide income for as long as you hold your green card." - Hanspeter Misteli Reyes, Associate, Greenberg Glusker [14]

Keep detailed records of your travel, as even partial days spent in the U.S. count toward the Substantial Presence Test [13]. If you’re considered a resident of both the U.S. and another country, tax treaties can help determine which country has primary taxing rights through "tie-breaker" provisions [11][14]. Additionally, long-term Green Card holders should be cautious: surrendering your status could trigger an exit tax if you meet certain income or net worth thresholds [13][14].

These rules highlight the U.S.'s approach to tax residency, which differs significantly from other countries' systems.

The UK determines tax residency using the Statutory Residence Test (SRT), a three-stage framework based on physical presence and ties to the country [15][16][17]. The first stage, the Automatic Overseas Test, classifies you as non-resident if you spend fewer than 16 or 46 days in the UK, depending on your recent residency history [15][16].

The second stage, the Automatic UK Test, establishes residency if you spend 183 days or more in the UK during the tax year (April 6 to April 5) [15][17]. If neither of these tests determines your status, the third stage - Sufficient Ties Test - comes into play. This test evaluates factors like family, accommodation, and work ties to decide residency [16][17].

For individuals like founders, the UK’s system can be particularly tricky. The number of ties required to trigger residency decreases as your days in the UK increase, making it easier to unintentionally become a tax resident if you maintain strong connections to the country [15][17].

Careful planning is essential to navigating these criteria and avoiding unexpected tax liabilities, including exit taxes.

Singapore operates a territorial tax system, meaning only income earned within the country is taxed. Most foreign-sourced income is exempt, making it an appealing option for founders with international business interests [19].

You qualify as a Singapore tax resident if you spend at least 183 days in the country during a calendar year [18][19]. Singapore also offers beneficial concessions. For instance, the two-year rule grants residency for both years if your employment spans two calendar years and totals at least 183 days. Similarly, the three-year rule provides residency for all three years if you maintain continuous employment, even if one of those years falls below the 183-day threshold [18][19].

Singapore’s tax framework offers several advantages. There’s no capital gains tax, so business exits and investment gains are untaxed [20]. Personal income tax rates are progressive, ranging from 0% to 24%, while corporate tax is a flat 17% [18][19][20]. However, starting in 2025, stricter rules will require foreign-owned holding companies to meet new substance requirements, including having at least one non-nominee executive director based locally or ensuring local management to qualify for a Certificate of Residence [18].

Tracking your travel days is critical, as your tax rate can change significantly based on your residency status. Non-residents face a flat 15% tax on employment income or 24% on director’s fees and consultancy income, whichever is higher [18][19]. To benefit from Singapore’s network of over 90 Double Taxation Agreements, you’ll need to ensure board meetings are physically held in the country and that strategic decisions are documented locally [18].

This system allows founders to retain more of their gains, making Singapore a strategic choice for those planning business exits.

When it comes to navigating tax residency changes, proactive planning is absolutely essential. The financial and legal complexities involved can be costly if not handled correctly.

Relocating founders often find themselves caught between overlapping tax systems, which can lead to unexpected expenses. For instance, you might end up with dual tax residency, making it crucial to understand Double Taxation Agreements and tie-breaker rules [1]. On top of that, your physical location could inadvertently shift your company’s "place of effective management", potentially subjecting your business to taxation in your new country [3].

Tax authorities are becoming increasingly sophisticated. In New York, for example, more than 300 residency auditors are tasked with investigating high-income taxpayers who claim to have moved [2]. These auditors dig deep, examining flight records, Slack messages, WhatsApp chats, and even GPS data to determine where key business decisions are being made [3]. To avoid disputes, secure written confirmation from a qualified tax advisor detailing the exact dates of your residency change [1]. This simple step can save you from costly overlaps and potential audits.

If you're a founder planning to exit your business, expert advice becomes even more critical. Firms like Phoenix Strategy Group (https://phoenixstrategy.group) specialize in financial and strategic advisory for growth-stage companies, including M&A transactions and exit preparation. Their experience can be a game-changer when coordinating cross-border tax planning with your broader exit strategy.

Start by keeping meticulous records. Maintain a "clean break" file for at least seven years, including documents like foreign utility bills, flight records, moving receipts, and proof of surrendering your old driver’s license and voter registration [2]. If you’re leaving a high-tax state such as California (13.3% top rate) or New York (10.9% top rate), consider establishing domicile in a no-income-tax state like Florida, Texas, or Nevada before moving abroad. This creates a "domestic anchor" that can simplify your tax situation [2].

Additionally, formalize your corporate governance as soon as possible. Ensure your board of directors exercises real decision-making authority in your company’s home jurisdiction. Avoid making strategic decisions informally through messaging apps while traveling [3]. Once you arrive in your new country, apply for a Certificate of Residence from the local tax authority. This document is key to claiming treaty benefits and reduced withholding rates [1].

While the rules can be intricate, a combination of careful planning and professional guidance can help you manage these challenges effectively.

Exit taxes come into play when you give up U.S. citizenship or long-term residency. These taxes are meant to account for any unrealized gains on your assets at the time of your departure. The goal is to prevent individuals with substantial assets from avoiding taxes by leaving the U.S. permanently.

To show you've officially left a high-tax state like California, it's crucial to provide solid proof of your new domicile and demonstrate that you've cut ties with California. Here's how you can do that:

Yes, it’s possible to be considered a tax resident in two countries simultaneously. This typically occurs when you meet the residency requirements of both countries independently. When this happens, you might encounter dual taxation, meaning both countries could tax the same income. However, many countries have tax treaties in place to help resolve these conflicts and provide relief, ensuring you're not taxed twice on the same earnings.