Published on

April 2, 2026

When companies merge or are acquired, customer relationships often represent 40-60% of the intangible value. These relationships are a key driver of revenue, retention, and long-term success, yet valuing them requires careful analysis.

Here’s a breakdown of the main methods used to value customer relationships in M&A:

Each method has unique strengths depending on the nature of the business, customer base, and deal structure. For example, MPEEM works well for subscription-based companies, while the Distributor Method fits businesses where brands or technology drive demand.

Key Takeaways:

Customer relationships are often the largest intangible asset in M&A, shaping deal outcomes, tax strategies, and financial reporting. Understanding their value ensures buyers and sellers make informed decisions.

The Multi-Period Excess Earnings Method (MPEEM) is a widely used income-based approach for valuing customer relationships as the primary intangible asset in acquisitions [5]. This method isolates cash flows tied to the existing customer base and subtracts fair market returns on contributory assets like working capital, fixed assets, workforce, technology, and brand [2]. What’s left are the "excess earnings" directly linked to customer relationships.

Here’s how it works: sales to existing customers are forecasted, annual attrition rates are applied, earnings are projected, taxes are subtracted, Contributory Asset Charges (CACs) are deducted, and the remaining excess earnings are discounted to present value. Finally, the Tax Amortization Benefit is added [2]. The attrition rate plays a crucial role in this process. As Tony Hillier, Advisor at Opagio, notes:

"The attrition rate is the single most impactful input in a customer relationship valuation."

While MPEEM provides detailed insights, it requires extensive data. Key inputs include revenue forecasts for the current customer base, historical attrition data by cohort, profit margins, and asset-specific discount rates, which are usually higher than the company’s weighted average cost of capital [2]. The method’s accuracy heavily depends on these assumptions. For example, setting CACs too low inflates the customer relationship value, while overly high CACs suppress it [2].

This method is especially effective for B2B service contracts and enterprise SaaS companies, where customer relationships often account for 45–60% of the total intangible value. Useful lives in these cases typically range from 10 to 15 years, with annual attrition rates between 5% and 10% [2]. However, MPEEM has a notable limitation: it generally focuses on a single primary intangible asset. If other assets, like a brand or technology, are the main drivers of demand, the Distributor Method may be a better fit to avoid overvaluing customer relationships [5].

For the best results, use cohort analysis to track specific customer groups over time and exclude expansion revenue, as MPEEM focuses solely on existing relationships at the valuation date [2]. It’s also critical to cross-check the total identified asset values against the purchase price to ensure the implied goodwill is reasonable and aligns with the overall deal structure [2].

Up next, we’ll explore the Distributor Method, which is often used when customer relationships support other demand-driving assets.

The Distributor Method takes a different approach from MPEEM by focusing on valuing customer relationships based on product demand rather than the relationship itself. Instead of relying on the company's actual profit margins, it uses market-based distributor margins to pinpoint the true value of the customer relationship [4][5]. When demand is driven by a strong brand or proprietary technology, the company essentially operates like a third-party distributor [4][6]. This method works best when customer relationships play a secondary role compared to broader demand factors.

For example, in a 2026 case, retailers stocked products primarily due to brand-driven consumer demand. This allowed Valuation Research Corp. to separate the value of customer relationships from brand value by applying distributor-level inputs. In this scenario, the brand value accounted for most of the deal's economic profit [4].

"The distributor's operating margin is reflective of the relative importance of the IP vs. the customer relationship" - Edward Hamilton, Managing Director at Valuation Research Corp. [4]

The calculation process is similar to MPEEM but incorporates market distributor margins. Here's how it works: forecast sales to existing customers, apply market distributor margins (which can range from 5% in food and beverage to 20% for branded manufacturers), subtract Contributory Asset Charges (CACs) for distributor-like assets such as working capital and sales teams, and then discount to present value [5][7].

"Today I use it as an analytical tool literally on every purchase price allocation that we do" - PJ Patel, Co-CEO of Valuation Research Corp. [7]

One of the main benefits of this method is its reduced subjectivity. Market databases make it easier to find observable distributor margins compared to identifying comparable royalty rates, which makes this approach less subjective than the Relief from Royalty method [4]. However, its accuracy depends on selecting the right market proxy and ensuring that CACs align with a distributor's profile rather than the manufacturer's R&D or proprietary equipment [4][5].

Originally used in the consumer packaged goods (CPG) sector, the Distributor Method has become a widely adopted tool across industries like technology, healthcare, and government contracting [7]. It serves as a useful baseline for isolating the value of supporting customer assets, allowing MPEEM to focus on core intangibles such as brand or technology. By clearly separating these elements, the Distributor Method offers a complementary perspective in M&A valuation analyses.

The With and Without Method takes a different angle compared to the Distributor Method, focusing on the added value of an established customer base. This approach evaluates customer relationships by comparing the total value of a business with its current customer base to what it would be worth without those relationships [1]. Essentially, it estimates the extra value brought by existing customers by imagining what it would take to rebuild those connections from scratch.

Here’s how it works: two separate discounted cash flow projections are created. The "With" scenario assumes the business operates as usual, leveraging its current customer relationships, while using standard revenue and expense projections. The "Without" scenario, on the other hand, accounts for the costs, delays, and risks involved in rebuilding the customer base. The difference between the present values of these two scenarios represents the value of the customer relationships.

This method requires a lot of data and involves subjective assumptions. For example, you need to estimate how long it would take to rebuild the customer base, calculate additional marketing and sales costs, and apply a higher discount rate to reflect the risks during the rebuilding period. These factors make the process complex and emphasize the need for accurate and reliable data, similar to the challenges found in MPEEM analysis.

The With and Without Method is especially helpful when valuing non-contractual relationships, such as distributor networks, where the key advantage lies in the time saved by having an established customer base. It’s often used for secondary assets rather than core intangibles, and its effectiveness depends heavily on the accuracy of the assumptions made.

To ensure the results are reasonable, it’s important to cross-check the valuation against the overall purchase price, confirming a logical allocation of implied goodwill. Up next, we’ll look at how market-based approaches offer another way to assess customer relationship value.

The Market Approach values customer relationships by using transaction benchmarks from recent deals. Instead of predicting future cash flows or estimating replacement costs, it focuses on real-world data from comparable transactions[1][9].

This method often relies on per-user or per-customer metrics from notable acquisitions. For example, Facebook's 2012 purchase of Instagram for $1 billion, with its 30 million active users, works out to about $33.33 per user. Similarly, Facebook's 2014 acquisition of WhatsApp for $19 billion and 450 million users translates to approximately $42 per user[8]. These figures provide a reference point for assessing similar customer bases in the tech industry.

But this approach isn’t without its challenges. As Tony Hillier, Advisor at Opagio, explains:

"Customer relationships... are not registered, not standardised, and not traded in observable markets"[2]

Unlike assets such as patents or real estate, customer relationships lack clear definitions and standardized boundaries. This makes it tough to find genuinely comparable transactions. Plus, the motivations behind each deal - like entering new markets, defending market share, or enabling cross-selling - can heavily influence the price paid, making direct comparisons tricky.

Because of these limitations, the Market Approach is rarely the primary method for valuing customer relationships in mergers and acquisitions (M&A). Instead, it’s more commonly used as a secondary benchmark. It helps validate the results of income-based methods, such as the Multi-Period Excess Earnings Method (MPEEM). While its lack of standardized data and difficulty in adjusting for transaction differences can affect its precision, it’s still a helpful tool for verifying whether other valuation methods are on the right track. This supporting role complements income-based approaches like MPEEM, setting the stage for a deeper analysis in the following section.

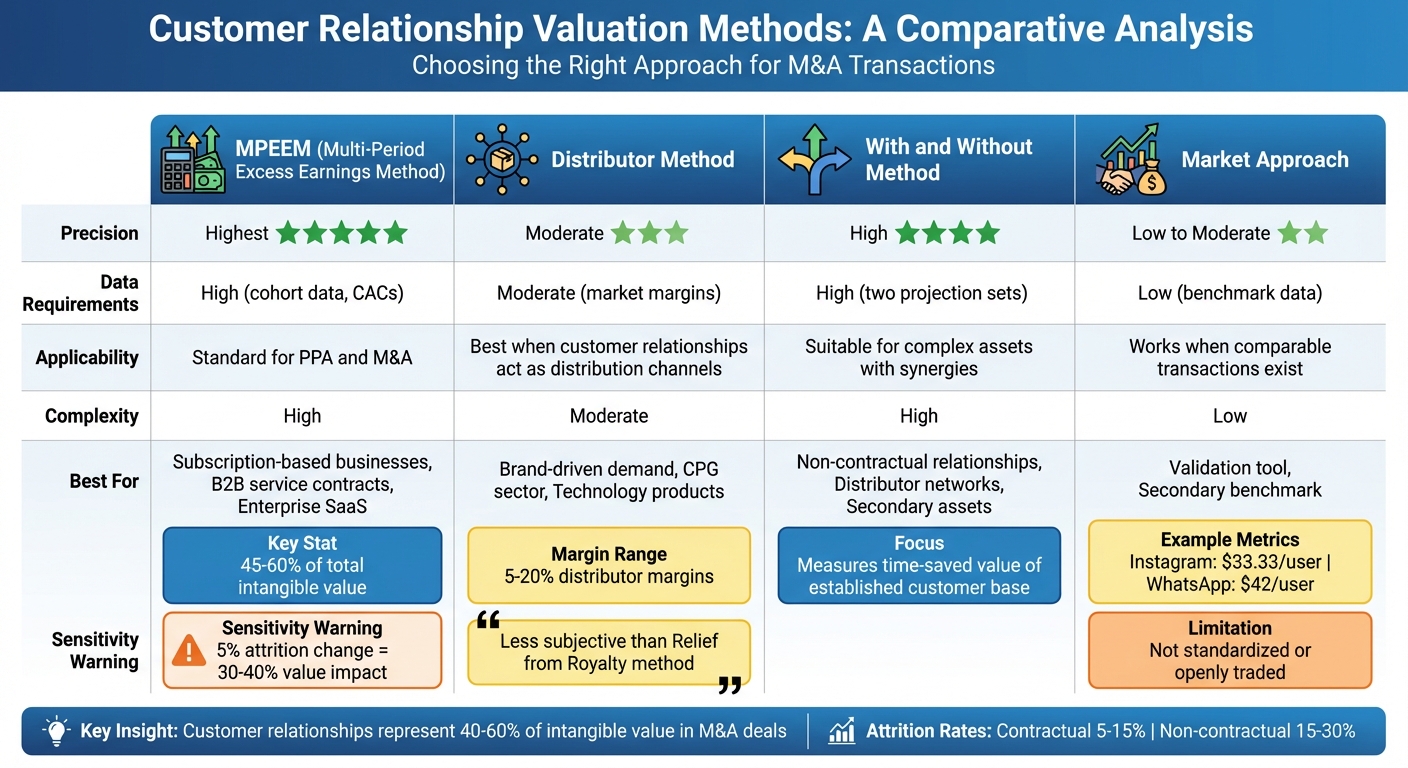

Comparison of 4 Customer Relationship Valuation Methods in M&A

Each valuation method comes with its own strengths and limitations. The Multi-Period Excess Earnings Method (MPEEM) stands out for its ability to closely pinpoint customer-specific cash flows. However, it demands a wealth of historical data - such as cohort analysis, profit margins, and detailed contributory asset charges - and its accuracy is highly dependent on input sensitivity. For instance, even a 5% change in attrition rates can cause a 40–50% swing in value, underscoring how critical precise inputs are for MPEEM [2].

The Distributor Method simplifies the process by using market-based distributor margins, making it a good fit when customer relationships function more like distribution channels rather than core assets. On the other hand, the With and Without Method provides a broader perspective by comparing a business's performance with and without the asset in question. However, this method requires building two complete sets of financial projections, which adds complexity. Lastly, the Market Approach bases its valuation on actual transaction data. While this method offers a practical, real-world perspective, it often struggles with comparability because customer relationships lack standardization and are not openly traded.

These differences highlight how each method impacts deal structuring and valuation outcomes.

| Method | Precision | Data Requirements | Applicability | Complexity |

|---|---|---|---|---|

| MPEEM | Highest | High (cohort data, CACs) | Standard for PPA and M&A | High |

| Distributor Method | Moderate | Moderate (market margins) | Best when customer relationships act as distribution channels | Moderate |

| With and Without | High | High (two projection sets) | Suitable for complex assets with synergies | High |

| Market Approach | Low to Moderate | Low (benchmark data) | Works when comparable transactions exist | Low |

In a Schneider Downs valuation conducted in July 2022, a dual-method approach was employed to meet ASC 805 standards [5]. These trade-offs not only shape the precision of valuations but also play a critical role in influencing M&A deal outcomes.

Customer relationship valuations play a critical role in determining purchase price allocation, reported earnings, tax strategies, and potential impairment risks under ASC 805 and IFRS 3. In many mergers and acquisitions (M&A), customer relationships often represent the largest identifiable intangible asset separate from goodwill [3]. This makes them a cornerstone for analyzing customer metrics and assessing market risks.

"In most acquisitions, buyers believe they are paying for technology, EBITDA, or revenue. In reality, they are predominantly paying for the value of the customer." – Lebanon Hub [3]

Metrics like Customer Lifetime Value (CLV) and Customer Acquisition Cost (CAC) are essential for projecting cash flows, which are used to estimate revenue synergies and cost savings. Strategic buyers use these projections to evaluate opportunities like cross-selling, boosting pricing power, and reducing acquisition costs by leveraging existing customer relationships [3]. However, failing to account for uncertainties through probability-weighted scenario modeling can lead to overestimated synergies and diminished deal value.

Overreliance on a small number of clients, high churn rates, or external risks like technological changes can significantly impact valuation. Since customer relationship assets are amortized over their useful lives, any overvaluation can negatively affect post-acquisition earnings [1][3].

For growth-stage companies preparing for exits or fundraising, accurate segmentation of customer profitability and identification of incremental value can provide a strategic advantage. Advisory services, such as those offered by Phoenix Strategy Group, help ensure precise valuations that stand up to audit scrutiny and align with long-term deal strategies.

Ultimately, the success of an acquisition often hinges on how well customer relationships are understood, modeled, and priced. Buyers who use advanced analytics, like Monte Carlo simulations to account for uncertainty in synergies, gain a clearer understanding of the true value they are acquiring [3].

When valuing customer relationships in M&A, the choice of methodology depends heavily on the specifics of the deal and the nature of the target company. The Multi-Period Excess Earnings Method (MPEEM) is often the go-to for subscription-based businesses with steady, predictable cash flows. On the other hand, companies with distributor networks, one-off sales models, or stable customer bases might find methods like the Distributor Method or the With-and-Without Method more suitable.

Several factors play a critical role in this decision, particularly whether the customer relationships are contractual or non-contractual. Contractual relationships typically see annual attrition rates of 5–15%, while non-contractual ones experience higher rates, around 15–30%[2]. Even small changes in these assumptions can have a big impact - a 5% shift in attrition rates can alter the calculated asset value by 30–40%[2]. This highlights the importance of reliable data and careful selection of valuation methods.

Customer relationships often represent the most valuable identifiable intangible asset in acquisitions, yet they don’t always receive the same level of scrutiny as technology or brand assets. For growth-stage companies planning an exit, understanding these valuation complexities is essential. In service-sector deals, customer relationships can account for 40–60% of the total identified intangible value[2], making them a key driver of deal success. To maximize valuation and reduce post-acquisition risks, businesses should prioritize diversifying their customer base, tracking retention metrics, and clearly distinguishing between different types of customer relationships.

Phoenix Strategy Group applies advanced analytics and deep industry knowledge to help growth-stage companies achieve optimal valuation outcomes and successful exits.

Choosing among MPEEM, the Distributor Method, and With-and-Without hinges on the specific valuation scenario and the characteristics of customer relationships.

The right method depends on factors like the industry you're analyzing, the type and quality of available data, and the specific objectives of the valuation.

Accurately assessing the value of customer relationships hinges on gathering data such as retention rates, spending growth, switching costs, and historical customer behavior. It’s also crucial to evaluate behavioral patterns, which can be modeled and projected to forecast future trends with greater accuracy.

The importance of customer relationships extends beyond business operations - it plays a key role in taxes and post-deal financial performance. These relationships directly affect purchase price allocation and goodwill calculation, both of which influence taxable income and financial reporting outcomes. By valuing customer relationships accurately, businesses can ensure the correct tax treatment and potentially adjust how post-deal earnings are reported.