Published on

February 14, 2026

Selling a business often triggers a significant tax bill, but a Deferred Sales Trust (DST) can help you defer these taxes while reinvesting the proceeds. Here's the gist:

While DSTs offer tax deferral and investment options, they come with risks like trustee selection, compliance challenges, and higher costs. Proper planning and expert guidance are essential to ensure success.

How Deferred Sales Trusts Work: 3-Party Transaction Process

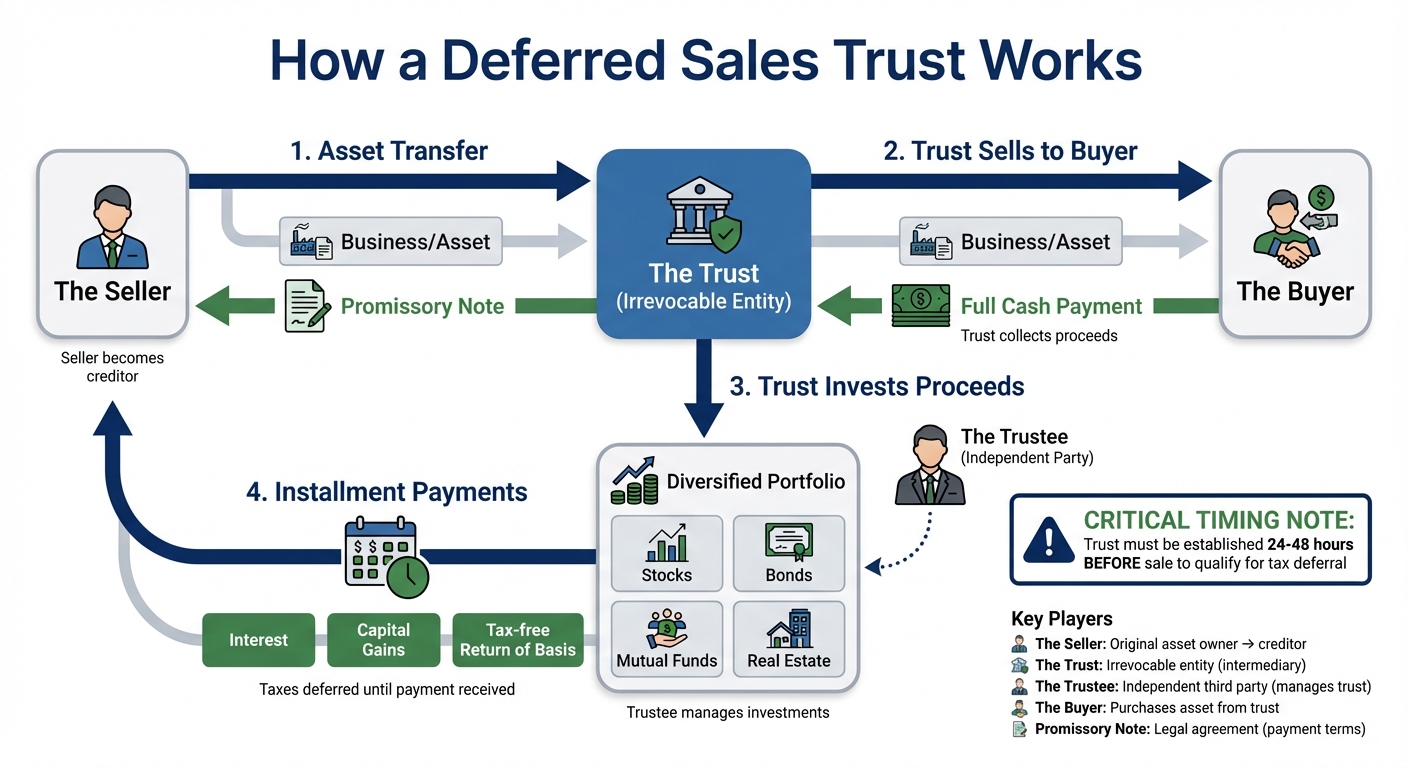

A Deferred Sales Trust (DST) involves a three-party transaction designed to separate you from the proceeds of a sale. Here's how it works: you transfer your business or asset to an independent trust in exchange for a promissory note. The trust then sells the asset to the final buyer and collects the full cash payment [1][4]. This setup is essential because the trust serves as the intermediary. The promissory note outlines your payment terms, locking in the trust's role in the process.

The promissory note is a critical document - it specifies the payment schedule, interest rate, and total amount owed to you. This arrangement changes your position from asset owner to creditor. Meanwhile, the trust invests the proceeds to ensure it can meet the payment obligations outlined in the note [1][5][3][4].

Here’s a breakdown of the main players and their roles in a DST:

| Component | Role in the DST Structure |

|---|---|

| The Seller | Transfers the asset to the trust and becomes a creditor, receiving payments over time. |

| The Trust | An irrevocable entity that buys the asset from the seller and resells it to the buyer. |

| The Trustee | An independent third party who manages the trust and oversees investments. |

| The Buyer | Purchases the asset from the trust. |

| Promissory Note | A legal agreement detailing payout terms, interest rates, and the deferral period. |

The trustee plays a vital role and must be an independent third party, often a tax attorney or professional trustee. For complex exits, many owners also consult a fractional CFO to model the long-term impact of these deferred payments on their overall wealth strategy. Neither you, your spouse, nor close relatives can serve as the trustee [5][3]. If the IRS finds that you have control over the trust's assets, they might classify the arrangement as a "sham", which would disqualify the tax deferral.

"To receive installment sale benefits the seller may not directly or indirectly have control over the proceeds or possess the economic benefit therefrom." - Wrenn v. Commissioner, Tax Court Ruling [4]

The buyer interacts solely with the trust and pays the full purchase price directly to it [3][4]. After the sale, the trust reinvests the proceeds based on the trustee's direction. To safeguard your interests as a creditor, it’s wise to secure the promissory note with a Security Agreement and a UCC-1 Financing Statement, giving you first claim to the collateral if the trust defaults [4].

The real advantage of a DST lies in its ability to defer taxes.

This tax deferral is possible thanks to IRC Section 453, which uses installment sale rules. These rules allow sellers to recognize capital gains gradually, as payments are received, instead of all at once in the year of the sale [6][3]. Since you receive a promissory note instead of immediate cash, the proceeds are not officially "realized" until payments are made. Taxes are only triggered when principal payments are distributed to you over time.

Each payment you receive includes three components:

For example, spreading a $750,000 gain over 10 years instead of taking it as a lump sum could significantly lower your federal tax burden. Instead of paying approximately $119,865 in taxes upfront, you might reduce your liability to around $5,318 per year by staying in a lower tax bracket and avoiding the 3.8% Net Investment Income Tax [3].

Timing matters. To qualify for these benefits, the trust must be set up, and the asset transferred before entering into a binding agreement with the buyer [6][5]. If you sign the purchase agreement first, the IRS may view the sale as direct, triggering immediate tax liability.

A Deferred Sales Trust (DST) offers a way to postpone immediate taxes, allowing the entire sale proceeds to grow without the initial tax bite. This means you can reinvest with money that hasn’t yet been taxed, potentially increasing your long-term wealth. By deferring taxes, you’re essentially giving your investments more room to grow, creating a larger financial base for future returns and income - money that might have otherwise gone straight to the IRS [1].

Another key advantage is the flexibility it provides for reinvestment. With a DST, the trustee can allocate the proceeds across a variety of investments, including stocks, bonds, mutual funds, or other ventures [1]. While the trustee must follow IRS rules, you typically have a say in how the assets are allocated and in shaping the overall investment strategy [1][3].

"You control the payout structure. And the trust can invest the proceeds in a diversified portfolio during that time, creating income and appreciation inside the trust." - Arron Bennett, Strategic CFO, Bennett Financials [1]

One of the standout features of a DST is its ability to invest in multiple asset classes, offering diversification. Unlike a 1031 exchange, which forces you to reinvest in a replacement property within 180 days, a DST gives you breathing room. The trustee can create a balanced portfolio aimed at meeting the trust’s payout obligations while still growing the remaining capital [1].

Another significant benefit is the shift in credit risk. In a traditional installment sale, you depend on the buyer to make payments over time. With a DST, the trust receives the full cash payment upfront, transferring the risk from the buyer’s financial success to the trust’s investment performance. Essentially, you become a creditor of the trust, secured by its assets, rather than relying on the buyer’s ability to pay [3]. This makes the DST a smart tool for tax deferral and financial security, especially when planning a business exit.

Beyond investment flexibility, a DST can turn a lump sum into a structured, steady income stream tailored to your retirement needs. You control the payout schedule - whether it’s monthly, quarterly, or annually - helping to manage your taxable income and potentially keeping it within lower tax brackets [1]. Each payment you receive includes a mix of interest, deferred gains, and tax-free returns [3].

The ability to manage your tax bracket is a game-changer. In one 2024 scenario modeled by Kitces.com, a business owner named Tina sold her company for $1 million (with a $250,000 basis). By choosing a 10-year installment sale with 5% interest instead of a lump sum, she saved $114,547 in federal taxes. Structured payments kept her within the 0% capital gains bracket and below the threshold for the Net Investment Income Tax [3].

For high-income earners, spreading payments can also help avoid the 3.8% Net Investment Income Tax. For instance, in May 2025, Bennett Financials shared a case where a client sold a business for $3.8 million. By using a DST, the client deferred $700,000 in first-year tax exposure and structured a 15-year income stream while reinvesting the bulk of the proceeds into a diversified, asset-backed portfolio [1].

Deferred Sales Trusts (DSTs) can offer appealing benefits, but they come with certain risks that require careful consideration. One significant concern is that you must relinquish all legal control over the proceeds from your sale. To qualify for tax deferral, you cannot act as the owner, trustee, or beneficiary of the trust. Instead, you take on the role of a creditor. This means that if the trust is mismanaged, your ability to recover funds is limited.

"If the DST trustee mismanaged the sales proceeds and caused them to default on the installment loan, the seller would have no recourse to recover those funds." - Ben Henry-Moreland, Senior Financial Planning Nerd, Kitces.com [3]

Another key issue is the lack of clear guidance from the IRS. DSTs are not officially recognized or endorsed by the IRS, and there is no safe harbor guidance. Many DST providers treat this as a proprietary offering, often requiring advisors to sign non-disclosure agreements before sharing full details. This makes independent verification challenging. In one instance, the Washington State Department of Financial Institutions filed charges in 2020 against a DST trustee and associated professionals for securities violations and fraud. Additionally, the trademark for "Deferred Sales Trust" has been listed as abandoned by the U.S. Patent and Trademark Office since 2021 [3]. These concerns highlight the importance of careful trustee selection and due diligence.

Selecting the right trustee is critical for both compliance and the success of your DST. To meet IRS requirements, the trustee must be entirely independent, with no personal or business ties to you [8]. If the IRS determines that you have any influence over the trustee, the trust could be deemed a sham, which would lead to immediate capital gains taxes, along with interest and penalties [10].

"If an owner can control or influence the trustee of the DST, the IRS may view the trust as a sham trust created to avoid taxation and may impose full capital gains tax liability, interest, and penalties on assets sold by the DST." - Andre Pennington, Tax Lawyer and Estate Planning Attorney, 453 Trust [10]

Timing is another critical factor. The trustee must assume legal ownership of your asset 24–48 hours before the sale to avoid "constructive receipt" of the funds [8]. Any misstep in this process or a misunderstanding of complex rules - such as those governing which business assets qualify for installment treatment - could result in unexpected tax liabilities. Since any remaining funds after the installment note is paid often go to the trustee, it's essential to thoroughly vet their track record and fiduciary history [3].

Beyond compliance and control risks, DSTs come with notable costs. Setting up a DST involves significant legal fees, typically around 1.5% of the first $1,000,000 of the sales price and 1.25% for amounts exceeding that [11]. On top of that, there are ongoing fees - approximately 0.5% annually for the independent trustee and another 0.5% to 1.0% for an investment advisor managing the trust’s assets. For a $1,000,000 sale, you can expect to pay $15,000–$25,000 upfront and $10,000–$15,000 in annual fees.

The financial benefits of a DST generally outweigh the costs within 12–24 months, provided the investment income meets expectations [11]. However, high fees or underperformance could erode those benefits. It’s crucial to consult with an independent accountant or tax attorney to ensure compliance with your state’s laws, as not all states align with IRC § 453 in the same way [8].

If you’re considering a DST as part of your exit strategy, working with experienced professionals is essential. For personalized guidance, you can reach out to Phoenix Strategy Group (https://phoenixstrategy.group).

To make the most of a Deferred Sales Trust (DST), timing is everything. You need to establish the trust before your asset sale is finalized - any delay could mean losing out on the tax deferral benefits [12].

"A DST must be fully established before the sale closes. This means you should finalize the trust documents and installment agreement in advance." - Pennington Law, PLLC [12]

Start the process during negotiations to give yourself enough time to assemble a solid estate planning team. This typically includes a tax attorney, an Independent Certified DST Trustee, and a Registered Investment Advisor (RIA) [13]. The DST process itself involves two key steps: first, selling your asset to the DST in exchange for an installment note; and second, the DST selling the asset to the ultimate buyer for a lump sum [3]. Before diving in, though, you’ll need to confirm whether your asset qualifies.

Not all assets can be used in a DST. Qualifying assets include privately held businesses, real estate, artwork, and other capital assets held for over a year [3]. However, publicly traded stocks and bonds are excluded from the IRC §453 installment treatment that DSTs rely on [3].

DSTs tend to be most effective when capital gains exceed $500,000, as these gains often push sellers into higher tax brackets [3]. To determine your asset's value, you’ll use the agreed-upon sales price between you and the buyer. For tax purposes, this value is assessed using the "Gross Profit Percentage", which is calculated as:

(Total Sales Price - Adjusted Basis - Selling Expenses - Recaptured Depreciation) ÷ Total Sales Price [3].

Getting this valuation right is critical - it affects installment payments and tax obligations. Also, ensure the transfer to the trust is documented as a "bona fide sale" to meet IRS scrutiny [7]. Once eligibility and valuation are squared away, you’re ready to transfer the asset into the trust.

After confirming eligibility, the next step is transferring all rights to the asset into the trust before the final sale. This step is crucial to avoid "constructive receipt" of the proceeds [13]. In return, the trust issues you a secured installment note, which outlines the payment terms, interest, and duration [12][13].

"The key to this setup working from a tax perspective is that the seller never actually takes possession of the sales proceeds until they receive installment payments from the trust." - Ben Henry-Moreland, Senior Financial Planning Nerd, Kitces.com [3]

Once the sale is completed, the proceeds are deposited into a controlled bank account. For added security, any investments made from this account require signatures from you, the trustee, and a bank officer [13]. To protect your position as a creditor, establish a Security Agreement and file a UCC-1 Financing Statement, ensuring you remain the first-place creditor in case of default [4]. It’s important to remember that IRS regulations require you to act solely as a creditor, not as the owner of the trust [3].

For tailored support throughout the DST setup and your business exit strategy, you can reach out to the professionals at Phoenix Strategy Group (https://phoenixstrategy.group).

When planning a business exit, knowing how Deferred Sales Trusts (DSTs) stack up against 1031 exchanges can make a big difference. Both methods allow you to defer capital gains taxes, but they function under different IRS rules and cater to different needs.

The most striking difference lies in what assets qualify. A 1031 exchange is restricted to "like-kind" real estate used for business or investment purposes [14]. So, if you're selling something like a private business, artwork, or private stock, a 1031 exchange won't work. On the other hand, DSTs cover a broader range of highly appreciated assets, including private businesses, real estate, artwork, and private stock [15]. Let’s break down the key contrasts in asset eligibility, reinvestment rules, and timing requirements.

Here’s where the two approaches really diverge: 1031 exchanges require all proceeds to be reinvested into like-kind property, which limits diversification [14]. DSTs, however, allow for much more flexibility. With a DST, your proceeds can be invested in a wide array of assets - like stocks, bonds, and mutual funds - giving you more control over your financial future [7].

"A 1031 exchange is ideal for real estate investors looking to continue investing in real estate and defer taxes. A DST is suitable for those seeking diversification beyond real estate or who want to manage their tax liability over time." - Deferred.com [14]

Timing is another major difference. In a 1031 exchange, you’re under a tight deadline: you have 45 days to identify a replacement property and 180 days to close the deal. Miss these deadlines, and you lose the tax deferral [14]. DSTs, by contrast, don’t come with these rigid timelines [14].

| Feature | 1031 Exchange | Deferred Sales Trust (DST) |

|---|---|---|

| Eligible Assets | Investment/Business Real Estate only [14] | Real Estate, Businesses, Stock, Artwork [15] |

| Reinvestment Rule | Must be "like-kind" property [14] | Diversified assets (stocks, bonds, etc.) [7] |

| Timing Rules | 45 days to identify; 180 days to close [14] | No specific reinvestment window [14] |

| Tax Authority | IRC Section 1031 [14] | IRC Section 453 (Installment Sales) [7] |

| Control | Direct ownership of replacement property [14] | Seller becomes a creditor [3] |

| Setup Costs | Generally lower cost [14] | Higher costs (legal/trustee fees) [7] |

From a cost standpoint, 1031 exchanges are often simpler and less expensive - some providers even offer "No Fee" options [14]. However, DSTs involve higher setup and ongoing costs, such as legal and trustee fees [7]. That said, for anyone selling non-real estate assets or looking for broader investment options, a DST may be the only practical route for deferring taxes.

A Deferred Sales Trust (DST) provides a way to defer capital gains taxes while creating structured retirement income. By utilizing the installment sale rules under IRC Section 453, you can spread your tax payments over several years instead of facing a hefty upfront tax bill. This strategy can ease immediate tax burdens and offers the flexibility to reinvest proceeds into a broad range of assets, such as stocks, bonds, and other investments. Unlike 1031 exchanges, which are more restrictive, DSTs offer greater reinvestment options [4][3][2]. However, these advantages come with specific costs and risks.

Setting up a DST typically costs between $25,000 and $50,000, with ongoing annual fees ranging from 1% to 1.5% [2][17]. As Arron Bennett, Strategic CFO and Founder of Bennett Financials, explains:

"A DST isn't a universal fix... Used properly, the IRS has no issue with deferring gains via legitimate installment methods. Used sloppily, you're inviting an audit" [1].

Timing is critical. The trust must be established, and the asset transferred into it before the sale is finalized. Failing to meet these requirements or mishandling trustee responsibilities can lead to immediate taxation, penalties, and interest [2][9]. Additionally, because the DST strategy lacks an explicit IRS safe harbor ruling and has been flagged for potential misuse, it's crucial to have the structure reviewed by independent tax counsel [3][1]. Proper planning can help reduce these risks while maximizing the strategy's benefits.

For those considering this option, especially when dealing with business sales generating capital gains exceeding $1 million, consulting experienced tax attorneys, CPAs, and independent trustees is essential [16]. With the right professionals guiding you, a DST can help you achieve significant tax savings and preserve your wealth for the long term.