Published on

February 14, 2026

The price of carbon credits heavily depends on the risks tied to the projects they originate from. These risks - like permanence, additionality, and delivery - impact the confidence that a credit truly offsets one metric ton of CO₂e. Here's a quick breakdown of the key takeaways:

To stabilize pricing, stakeholders must focus on due diligence, better monitoring (e.g., satellite data), diversified portfolios, and buffer pools. These strategies ensure reliable credits and help prevent greenwashing claims.

Carbon Credit Risk Categories and Their Pricing Impact

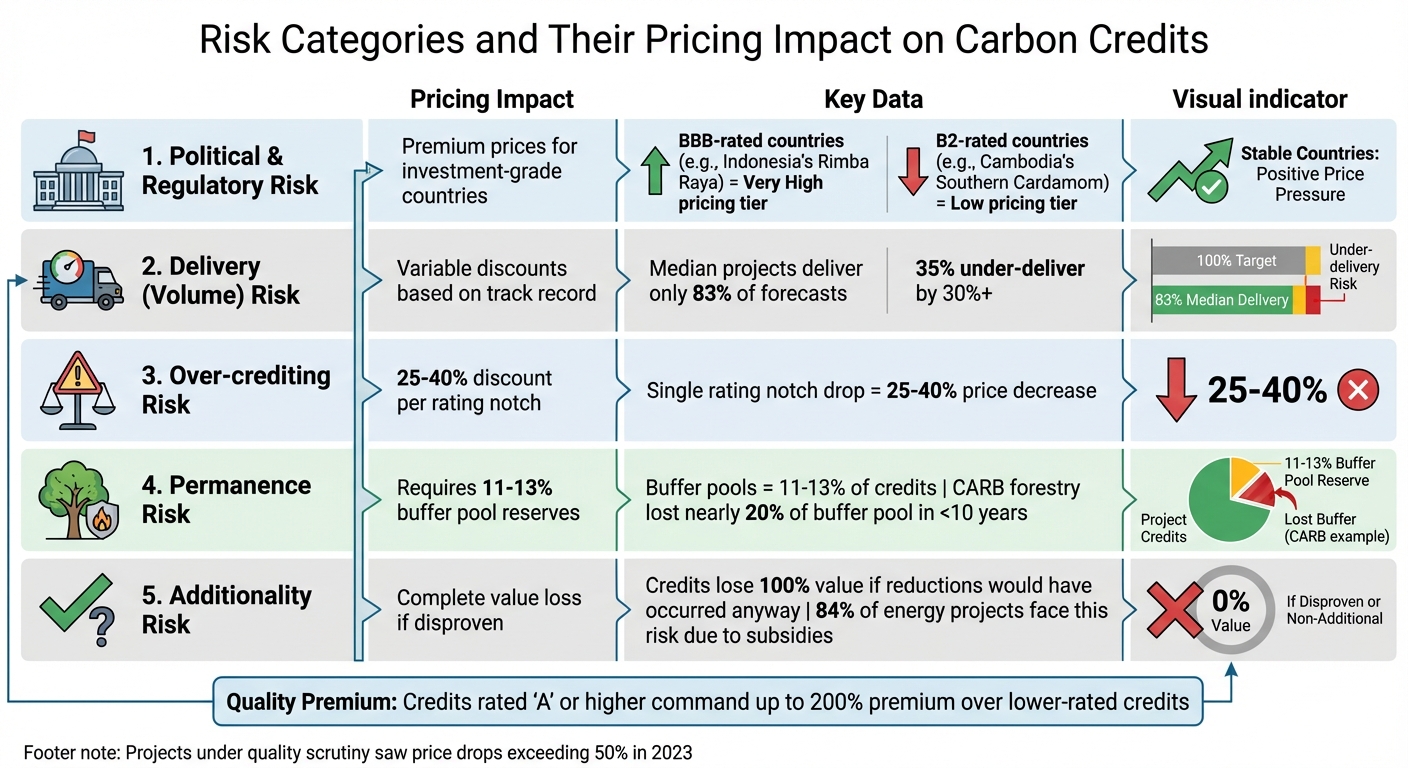

Carbon credit prices shift significantly depending on risk categories. A single rating notch can now lead to a 25–40% price gap, compared to 20% in earlier periods [2]. Grasping these risk categories is crucial to understanding why projects that appear similar might trade at vastly different price points.

| Risk Category | Pricing Impact | Market Evidence |

|---|---|---|

| Political & Regulatory | Higher valuations for investment-grade countries | Projects in BBB-rated countries fetch premium prices over those in lower-rated ones [5] |

| Delivery (Volume) | Variable discounts based on track record | Median projects deliver only 83% of forecast issuance, with 35% under-delivering by 30% or more [8] |

| Over-crediting | 25–40% discount per rating notch | Prices drop sharply when baseline assumptions prove unrealistic [2][7] |

| Permanence | Requires 11–13% buffer pool reserves | Wildfires depleted nearly 20% of the CARB forestry program buffer pool in under a decade [1] |

| Additionality | Complete value loss if disproven | Credits lose all value if reductions would have occurred without the project [1] |

These categories highlight the specific factors influencing pricing, which are explored further below.

Government policies and political environments create substantial uncertainty in carbon markets. Political risks often stem from actions like revoking land concessions or altering carbon rights regulations [9]. Projects in investment-grade countries consistently achieve higher valuations. For instance, the Rimba Raya REDD+ project in Indonesia (S&P rated BBB) maintained a "Very High" price category in early 2024, supported by stable policies and a low 25% credit surplus [5]. In contrast, the Southern Cardamom project in Cambodia (S&P rated B2) fell into a "Low" pricing tier due to a 77% credit surplus and governance issues reflected in a BeZero rating of "C" [5].

Policy risks also impact additionality. For example, an India Solar PV project launched in March 2018 faces scrutiny because government subsidies covered up to 30% of its costs, suggesting the project might have been viable without carbon credit revenue [10]. This kind of policy risk affects about 84% of energy projects, which often rely on existing renewable energy subsidies [10].

Delivery risk, or volume risk, challenges a project's ability to meet its forecasted credit issuance [8]. Data reveals that median projects deliver only 83% of their forecasts, and 35% under-deliver by 30% or more [8]. This inconsistency erodes buyer trust, a key factor in determining market pricing. Buyers frequently discount credits from projects with questionable delivery records.

Price volatility adds to the uncertainty. In 2023, projects under quality scrutiny saw price drops exceeding 50% [4]. Factors like market liquidity issues, currency fluctuations, and delays in credit issuance further undermine buyer confidence. As a result, credits with ratings of "A" or higher now command a 200% premium over lower-rated credits, reflecting the market's preference for reliability [2].

Permanence risks loom large for nature-based projects. Stored carbon is vulnerable to release through wildfires, illegal logging, or natural disasters. To mitigate this, buffer pools - typically set at 11–13% - are required, increasing costs and reducing credit value [7].

Over-crediting is another critical risk. This occurs when projects issue more credits than the actual tons of CO₂e reduced, often due to unrealistic baseline assumptions. BeZero Carbon defines over-crediting as the issuance of credits exceeding actual CO₂e reductions, often caused by uncertain data or flawed assumptions [7]. Nature-based solutions face higher over-crediting risks compared to technology-based projects because of the challenges in setting accurate baselines and estimating carbon stocks.

If additionality claims are disproven - meaning the emissions reductions would have occurred without the project - the credits lose all value. Understanding these risks is essential for developing effective risk management strategies. For projects requiring complex financial oversight, a fractional CFO can provide the necessary expertise to navigate these market volatilities.

Risk doesn’t just tweak the value of individual carbon projects - it fundamentally shifts how the entire carbon credit market functions. Now, credits are priced based on how likely they are to deliver the promised reductions [11]. This creates a clear divide: high-risk projects face steep discounts, while low-risk credits command premium prices.

Corporate buyers are increasingly favoring quality over quantity, a trend often referred to as the "flight to quality" [6]. This shift is largely driven by information asymmetry - where project developers know far more about their projects than buyers do [4]. To protect their reputations and ensure their investments lead to real climate impact, buyers are leaning heavily on third-party ratings to guide their decisions.

High-quality credits now come with hefty price tags. A single-notch improvement in a project’s rating can lead to a price increase of around 40% [2]. On the flip side, projects under intense scrutiny for quality concerns can see their prices plummet by more than 50% as demand dries up [4].

"The attempted commodification of this market has left carbon projects open to criticisms, because it is incredibly hard in practice to prove that each credit represents exactly one tonne of avoided or removed carbon dioxide equivalent." – Ted Christie-Miller, Director of Carbon Removal, BeZero Carbon [11]

Geography also plays a major role in pricing. Projects located in politically stable, investment-grade countries consistently fetch higher prices compared to those in riskier regions. For example, Indonesia’s Rimba Raya REDD+ project (rated BBB) maintained "Very High" pricing in early 2024, while Cambodia’s Southern Cardamom project (rated B2) fell into the "Low" tier, despite having a similar structure [5]. Buyers clearly prefer jurisdictions with stable governance, predictable regulatory frameworks, and secure carbon rights.

While the focus on quality is growing, the uncertainties surrounding project delivery continue to drive significant price swings.

The market’s demand for high-quality credits exists alongside significant price volatility, largely fueled by uncertainty. When media reports or academic studies cast doubt on project quality, prices can drop sharply [11]. Research suggests that 51% of evaluated carbon credits have a low or very low chance of achieving their full climate impact [11]. To hedge against this uncertainty, buyers may retire as much as 123% more credits than their actual emissions [11].

Risk grading operates on a spectrum. Proposed risk discount rates range from 5% for "AAA"-rated credits to a staggering 99% for "D"-rated ones [11]. This pricing system is similar to how bonds are valued, with a project’s perceived creditworthiness directly affecting its market price. In this environment, high-risk projects not only sell at significant discounts but often struggle to find buyers at all. This highlights the critical need for strong risk management strategies to stabilize credit prices and maintain market confidence.

Dramatic price fluctuations in the carbon market make solid financial risk management essential. With the median carbon project delivering only 83% of its forecasted credits and about 35% of projects under-delivering by 30% or more [3][8], the need for proactive strategies becomes clear. Below are practical approaches to help mitigate risks and stabilize pricing.

Understanding risks is key - buyers must differentiate between volume risk (actual credit issuance vs. forecasts) and value risk (credit quality per tonne of CO₂e) [8]. Start by analyzing the Project Design Document (PDD) and comparing its assumptions with realistic benchmarks. Ensure the buffer pool is appropriately sized for the project's risk profile, as historical data shows these reserves can deplete significantly [1].

Contracts should hold sellers accountable for losses stemming from issues like leakage, permanence failures, or weak additionality [1]. Independent third-party ratings from organizations like BeZero or Sylvera can also provide reliable quality assessments. Notably, credits rated "A" or higher typically command a 200% price premium [4]. Technology can further refine this evaluation process, offering deeper insights into project quality.

Modern tools like remote sensing and geospatial analytics are transforming risk monitoring. For instance, Sentinel-2 satellite data can track vegetation health using NDVI, while Sentinel-3 monitors land surface temperature to identify wildfire risks early [1]. For renewable energy projects, incorporating dynamic emission factors that adjust with annual grid changes prevents over-crediting, unlike static baselines set at project inception [7].

Digital measurement, reporting, and verification (dMRV) systems are replacing outdated PDF reports with machine-readable data formats. The Carbon Crediting Data Framework (CCDF) streamlines project information sharing, cutting due diligence time and slashing transaction costs that often exceed $100,000 per project [13]. Additionally, BeZero's Carbon Plots Database, which aggregates data from over 200,000 sites worldwide, helps create more accurate carbon yield projections [8]. Pairing such advanced monitoring tools with a diversified investment strategy can help mitigate localized risks.

Diversification remains one of the most effective ways to manage risk. Spread investments across different project types, geographies, and stages to avoid single-point failures. For example, while over 70% of rated forestry projects carry high over-crediting risks, more than 80% of waste projects are considered low risk [14]. Balancing nature-based solutions (which are cost-efficient but face permanence challenges) with technological approaches (which offer higher permanence but may struggle with scalability) can enhance resilience [6][14].

"Diversification in the carbon market can spread risk across different projects, geographies, and project types, ensuring that the overall impact is not compromised by the failure or underperformance of a single project." – CEEZER [4]

Geographic diversification is equally important. It helps shield investments from localized risks like regulatory changes, natural disasters, or economic instability in host countries. Working with multiple reputable developers adds another layer of protection, ensuring that the failure of one proponent doesn’t undermine the entire portfolio [14][4]. With every dollar traded in the secondary market generating $3 to $5 in primary market investments, forward-looking risk assessment is crucial [4].

In addition to diversification, setting aside resources for risk mitigation can cushion against market volatility. Buffer pools, typically set at 10% to 20% of total credit issuance, act as safeguards against losses from events like fires, disease, or reversals [1][7]. On average, nature-based avoidance projects contribute about 13% to these buffers, while removal projects average around 11% [7]. Emerging carbon insurance products are also becoming available to protect against project failures and market instability [4].

For early-stage or experimental carbon removal methods, it's wise to limit exposure and secure backup credits in case of underperformance [4].

Managing risks tied to specific projects plays a crucial role in stabilizing the carbon market. When stakeholders commit to thorough due diligence, use independent ratings, and diversify their portfolios, they create the groundwork for steady pricing and a dependable supply of carbon credits. Recent research highlights delivery gaps, emphasizing the pressing need for strong risk management practices [8][3].

The market is already reflecting these improvements. Carbon credits with an "A" rating or higher now fetch premiums as high as 200% compared to lower-rated credits [4][2]. This pricing transparency empowers buyers to make smarter decisions while motivating developers to uphold high standards of integrity and transparency.

"The goal of ratings data is to arm market participants with risk information, giving them a new and valuable input into price discovery and helping to make the market more efficient." – BeZero Carbon [2]

Strong risk management also enhances the appeal of projects to institutional investors and lenders. For every $1 spent on issued credits, an estimated $4 is being directed toward pre-issuance projects [12]. Tools like satellite monitoring, carbon curve analysis, buffer pools, and diversified portfolio strategies have proven effective in mitigating risks across the market. These methods underscore the importance of strategic approaches to ensure the market remains reliable and capable of supporting long-term goals.

Effectively managing project risks is essential to guarantee that each carbon credit represents one metric ton of CO₂e. Without this assurance, buyer trust diminishes, and price volatility rises. Practical strategies - such as satellite monitoring, carbon curve analysis, buffer pools, and insurance products - help mitigate risks like non-delivery, permanence issues, and quality concerns. By adopting these measures, stakeholders can foster a more stable market, attract the necessary capital for growth, and support long-term climate commitments.

For companies navigating these challenges, Phoenix Strategy Group offers advisory services to help integrate robust risk management into sustainable development strategies.

A carbon credit is only valid when it supports a project that wouldn’t have happened without the financial support from the credit itself. This means the project shouldn’t be something that would occur as part of regular operations. To determine this, assess if the project genuinely relies on the funding from the credit and whether it aligns with the principles of additionality.

Pricing delivery risk effectively means diving into the unique uncertainties of a project and its expected performance down the line. Some useful approaches include carbon curve analysis, which models emissions reductions, and tools that compare forecasted credit issuance against actual outcomes. By blending geospatial analytics, ecological modeling, and in-depth project-level evaluations, it becomes possible to address operational and implementation risks. This combination allows for more precise pricing based on how likely a project is to meet its delivery goals.

Buyers can reduce the risk of permanence issues without breaking the bank by focusing on projects with a well-defined management plan to handle potential reversals. Pay attention to key elements like physical safeguards, legal protections, and strong financial practices. Rather than depending entirely on certifications, take a closer look at the project's specific safeguards and enforcement strategies to ensure it can deliver lasting results.