Published on

July 2, 2026

If you want to use Reg CF, you need Form C done before your campaign starts. In plain terms, that means filing the SEC disclosure first, making sure your numbers and terms match everywhere, and keeping up with update filings after the offering begins.

Here’s the short version:

What matters most is simple: consistency. If your Form C, campaign page, subscription agreement, cap table, and financials do not match, you can create filing problems fast.

I’d treat this article as a plain-English checklist for the full process - from issuer details to EDGAR filing - so you can spot gaps before they turn into amendments, delays, or investor confusion.

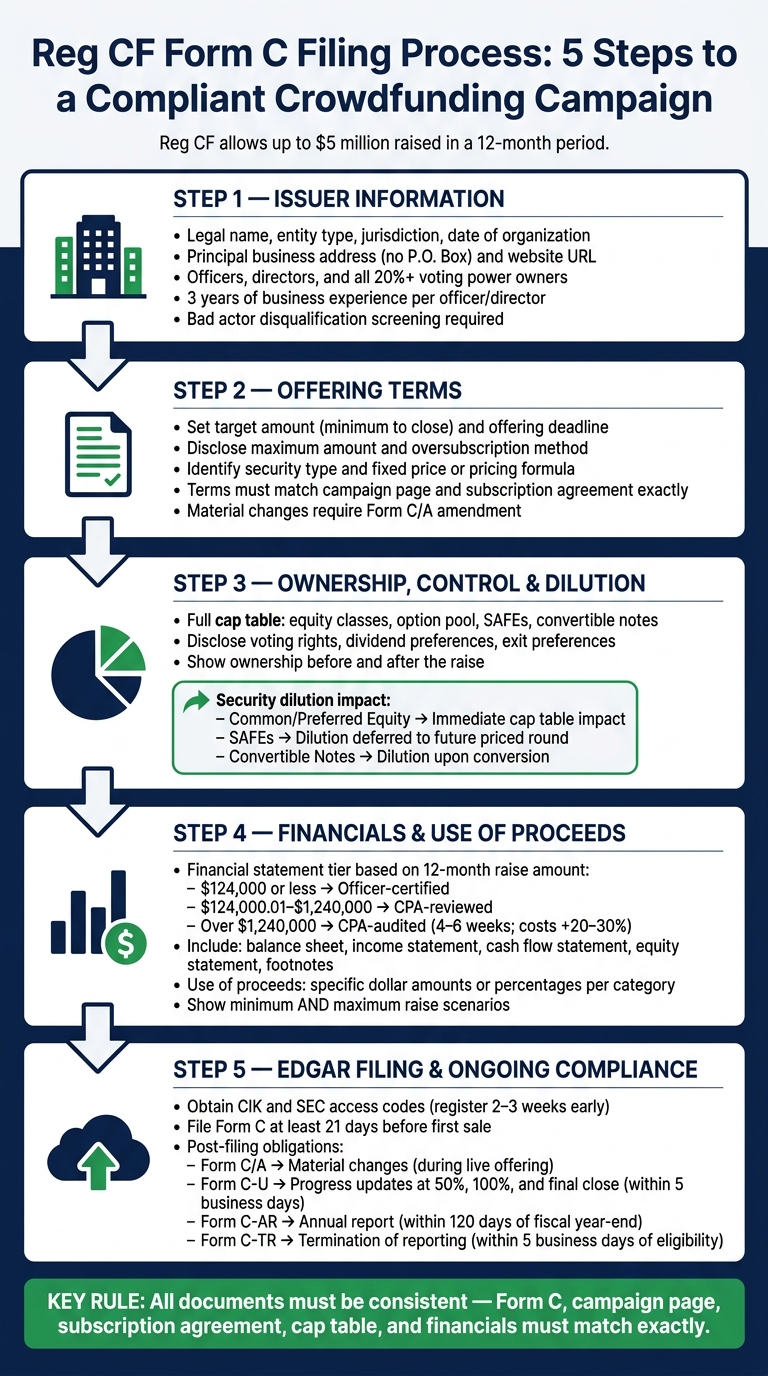

Reg CF Form C Filing Process: 5 Steps to a Compliant Crowdfunding Campaign

Start with the issuer details investors see first. Your issuer information should line up across your formation documents, website, deck, and exhibits.

Enter the main company details first: your company's legal name, entity type, jurisdiction of organization, date of organization, principal business address, and website URL. These fields need to match the legal entity that is actually making the offering.

If your team works remotely, use your company's physical principal place of business in the United States. A P.O. Box won't work. Include the URL where investors can access the annual report.[7][1][5]

After the legal details line up, describe the business in one sentence. Say what the company does today in plain English, and keep it consistent with the campaign page and deck. Skip salesy wording that sounds more promotional than descriptive.[3][6]

Under Rule 201(b) and 201(c), you must disclose the names and titles of all executive officers and directors, plus anyone who owns 20% or more of the voting power.[7] That threshold is based on voting power, not equity percentage.

For each officer and director, list the past three years of business experience, including prior employers and their businesses.[7][1] Make sure the titles match the company's bylaws or operating agreement. Don't leave out this work history.

| Required Issuer Field | Source for Verification |

|---|---|

| Legal Name | Certificate of Incorporation / Formation |

| Entity Type | Articles of Organization / Bylaws |

| Jurisdiction | State Filing Records (e.g., Secretary of State) |

| Physical Address | Lease Agreement / Utility Bills |

| Officers & Directors | Board Meeting Minutes / Employment Agreements |

| 20% Beneficial Owners | Cap Table / Stock Ledger |

| Business Description | Offering Page / Investor Deck |

Also, screen all officers, directors, and 20% owners for bad actor disqualification before filing.[1]

With the issuer data done, move to the offering terms.

Next, lay out the terms of your offering. This is one of those places where small mismatches can turn into disclosure mistakes fast. Your terms need to match your campaign page and subscription agreement exactly.[2]

Your target offering amount is the minimum amount you need to close the raise. If investor commitments don't hit that target by the deadline, no securities are sold, commitments are canceled, and investor funds are returned.[7]

Set your offering deadline as a specific date. That date matters because investors can cancel their commitment until 48 hours before the deadline. In plain English, the date you list starts a hard countdown for the campaign.[7]

If you want to take investments above the minimum target, disclose a maximum offering amount and explain how you'll handle oversubscriptions.[7] Be specific. Say whether you'll allocate on a pro-rata basis, first-come, first-served, or another defined method.[7]

If you reach the target early, you can close the offering before the original deadline. But there's a catch: you must give at least five business days' notice of the new deadline.[7]

After the economics, define the security itself.

Identify the security you're offering, and disclose either a fixed price or the method used to set that price.[2][1] If you're using a pricing formula, spell it out clearly. The goal is simple: keep the terms aligned across the Form C narrative, the EDGAR data fields, the campaign page, and the subscription agreement.[2][3]

Before you file, cross-check every field in this section against your campaign page and subscription agreement.[2] If you make a material change, you'll need a Form C/A amendment, and investors may need to reconfirm their commitment within five business days.[8]

Next, describe ownership, control, and dilution.

After you set the offering terms, the next job is simple: show people how this raise changes ownership and control.

Form C requires a full cap table summary, not just a list of names. You need to describe each equity class, the option pool, any SAFE, and any convertible note, along with the rights tied to each class, the securities you're offering, and any exempt securities offerings completed during the prior three years.[5]

That means spelling out things like voting rights, dividend preferences, information rights, and exit preferences so investors can see where each class sits in the company's control structure.[2] Put plainly, they should be able to tell who controls the company today and how that may shift after the raise.

This part shouldn't feel like legal fog. If one share class gets more votes, say that. If one group gets paid first in an exit, say that too. If SAFEs or notes may turn into equity later, make that easy to follow.

Before you file, make sure the cap table matches across all documents.

Dilution is straightforward: when new shares are issued, each existing holder usually owns a smaller percentage of the company. That can happen in a later financing round, when stock options are exercised, or when SAFEs and convertible notes convert into equity.[2][9]

| Security Type | Impact on Dilution and Control |

|---|---|

| Common/Preferred Equity | Immediate impact on the cap table and voting power |

| SAFEs | Defers valuation and dilution until a future priced round |

| Convertible Notes | Debt that converts to equity later; dilution occurs upon conversion |

Tie this section directly to the securities you're actually offering. Don't hide behind generic legal copy. If you're selling equity, explain the immediate effect on ownership and voting. If you're using SAFEs or notes, explain that the ownership hit may come later, often in the next priced round.

Later rounds can reduce your ownership percentage even if the company's value rises.[2]

That's the kind of plain, direct wording investors can use.

After you show how the raise affects ownership, the next step is to show whether the business can actually support the amount of money you're asking for. This is the point where investors compare the raise to the company's financial situation.

Form C requires a written narrative about your liquidity, capital resources, past operating results, and any material changes in results of operations.[4][1] In plain English, you need to explain cash on hand, runway, access to capital, and any major shifts in performance so investors can read the numbers with the right context.[1]

Issuers also need to include historical financial statements prepared under U.S. GAAP. If the company has existed for less than two years, the statements must cover the period since inception. The full package includes:

The level of financial statement assurance depends on how much you plan to raise over a 12-month period.[10] The SEC splits the rules into tiers:

| Offering Amount (12-Month Period) | Financial Statement Requirement | Level of Assurance |

|---|---|---|

| $124,000 or less | Certified by the principal executive officer | Issuer certification |

| $124,000.01 – $1,240,000 | Reviewed by an independent CPA | CPA review (AICPA standards) |

| More than $1,240,000 | Audited by an independent CPA | CPA audit (AICPA standards) |

Note: First-time Reg CF issuers targeting more than $1,240,000 may, in limited cases, substitute a reviewed statement if audited financials aren't yet available.[1]

That last tier can slow things down. Audited statements can add 4–6 weeks to your timeline and increase preparation costs by 20%–30%, so it's smart to bring in your accountant early.[2]

Once your financials are done, line them up with the filing. The numbers in the statements and the spending plan should tell the same story.

The use-of-proceeds section needs to be specific. Break out each major use of proceeds with dollar amounts or percentages.[1][4] Broad labels like "growth" or "operating expenses" without any detail won't cut it.[6]

You also need to show two cases: what happens if you only reach the minimum target, and what changes if you raise the full maximum amount.[3] This keeps the plan grounded in actual cash needs instead of turning into a wish list.

Here’s the split between what Form C requires and what founders should prepare behind the scenes:

| Required Form C Disclosure | Useful Founder-Prepared Supporting Detail |

|---|---|

| Specific dollar amounts for major categories (e.g., hiring, R&D) | Detailed hiring roadmap with specific roles and timing |

| Percentage of proceeds allocated to each category | Marketing spend breakdown by channel, including CAC/LTV projections |

| Use of funds if only the minimum target is raised | Milestone-based triggers for secondary spending |

| Use of funds if the maximum amount is raised | Cash flow forecasts showing runway extension per dollar raised |

| Disclosure of intermediary fees and commissions | Vendor quotes or equipment price lists for capital expenditures |

A simple example helps. If the minimum target only gives you enough cash to hire one engineer and cover six months of payroll, say that. If the full amount lets you add paid acquisition, equipment, or extra hires, spell that out too. Investors want to see where the money goes and what each level of funding changes.

After the numbers and use of proceeds are locked in, move to the EDGAR filing and final error checks.

Once your terms, ownership, and financials are set, it's time to file Form C in EDGAR and get ready for follow-up filings.

Before you file, your company needs a Central Index Key (CIK) and SEC access codes through EDGAR. If you've never filed with the SEC before, register early - ideally 2 to 3 weeks before your planned launch date - so a technical snag doesn't throw off your timeline.[2]

After you get access, log into the EDGAR online filing portal, choose "Form C" from the Regulation Crowdfunding templates, enter the required financial data directly into EDGAR, and upload PDFs for financial statements and exhibits in SEC format. The full Form C has to be filed at least 21 days before the first sale.[2]

After the offering goes live, you'll need to stay on top of these filings:

| Filing Type | Purpose | Deadline |

|---|---|---|

| Form C/A | Amendment for material changes | During the live offering |

| Form C-U | Progress update at 50%, 100%, and final close | Within five business days of each milestone |

| Form C-AR | Annual report after the offering | Within 120 days of fiscal year-end |

| Form C-TR | Termination of reporting obligations | Within five business days of eligibility |

Use Form C/A when there's a material change, like a new officer, a revised use of proceeds, or an updated risk factor. If the change calls for reconfirmation, check the reconfirmation box and give investors five business days to reconfirm their investment.[2][8]

The errors that cause the most trouble usually come down to one thing: mismatch. If the terms in your subscription agreement don't line up with the EDGAR narrative, or your portal pitch deck describes a different security type than the one in the filing, investors may get mixed signals and the SEC may comment.[2]

A few other trouble spots show up all the time:

Before you submit, compare every document side by side. Make sure the offering terms match everywhere, confirm that your financial statement tier fits your raise amount, and run EDGAR's real-time validation tool to catch missing fields or formatting issues before they turn into SEC comments.[2]

A material change to Form C is any major update to the original filing. That can include changes to the target offering amount, the campaign deadline, or the offering terms.

If that happens before the campaign closes, the issuer must file an amendment. Current disclosures matter because investors rely on them when making decisions, and issuers need to stay compliant.

Investors must reconfirm their commitment within five business days if the issuer makes a material change to the offering statement.

That rule helps make sure investors have the latest facts before moving ahead, especially when major updates come up, like shifts in business conditions or changes to the offering terms.

Plan on 6 to 8 weeks to get a complete Form C ready. In most cases, the financial work takes the most time, so it’s smart to start that part months before your planned launch.

If you need audited financial statements, add another 4 to 6 weeks to your timeline. It also helps to pre-register your Central Index Key and EDGAR access codes early so you don’t get held up later.