Published on

February 28, 2026

Growth-stage companies often face cash flow challenges due to rapid expansion and inventory demands. Inventory financing provides a way to access funds tied up in inventory or purchase orders, helping businesses maintain operations and meet growth targets. Here’s a quick breakdown of five key financing options:

Each option suits different needs, from managing seasonal demand to fulfilling large orders. Choosing the right solution depends on your business model, growth stage, and cash flow requirements.

Inventory Financing Options Comparison: Costs, Advance Rates, and Best Use Cases

For growth-stage companies navigating tight cash flows, a line of credit (LOC) can provide much-needed financial flexibility. Unlike traditional loans that deliver a lump sum upfront, an LOC is a revolving account that allows you to borrow as needed, up to a set limit. What's more, you only pay interest on the amount you actually draw [1][6]. This makes it a practical option for businesses dealing with unpredictable inventory restocking or seasonal demand spikes.

These credit lines are typically secured by inventory, with lenders keeping a close eye on stock levels through regular appraisals to ensure the borrowing base remains sufficient [1][3]. Depending on the type of inventory, lenders usually advance between 50% and 80% of its appraised value - higher for wholesale goods (60–80%) and lower for perishable items (40–50%) [3][6].

The cost of inventory lines of credit varies. Annual percentage rates (APRs) usually fall between 6% and 20%, though alternative lenders may charge over 30% for borrowers considered higher risk [3]. Many LOCs are tied to the prime rate, with 2025 rates typically ranging from 7% to 18% [6]. Beyond interest, borrowers should anticipate additional fees, including:

Some lenders may also charge unused line fees ranging from 0.25% to 0.5% annually if a minimum usage threshold isn't met [6]. Fiona Lee, Former Content Lead at Ramp, highlights the benefits:

"Inventory financing lets you borrow money using your inventory as collateral, freeing up cash flow without selling equity or draining operating cash" [3].

This cost structure works well for businesses that value flexible repayment options.

Most inventory LOCs offer a draw period of 12 to 24 months, during which borrowers make interest-only payments. Afterward, a repayment period of 6 to 24 months begins to cover the principal [7]. Some businesses prefer a bullet repayment structure, where they make a single lump-sum payment after completing a seasonal inventory cycle [5]. As you repay the borrowed amount, the credit becomes available again, which is particularly helpful for businesses with fast-moving inventory [8].

Take the example of Inc Tablet, an e-commerce phone retailer. In June 2025, the company used a revolving credit facility from Lenkie to scale its inventory. Founder Adam Hamdoud leveraged the credit line "on loop", doubling sales from $400,000–$800,000 to a projected $2.4 million by circulating stock multiple times before full repayment [8].

As your business scales, lenders often increase your credit limit to match your growing inventory needs [8]. Online and alternative lenders can approve and fund LOCs within 24 to 72 hours, much faster than the 2 to 4 weeks typically required by traditional banks [3][6]. Non-bank lenders usually require annual revenues between $50,000 and $100,000 and at least 6 to 12 months of operating history [3][6].

Additionally, this financing option allows businesses to negotiate early-pay discounts with suppliers. For instance, a 2% discount for paying within 10 days can often offset the cost of borrowing from the LOC [6]. Expert advisors, such as those at Phoenix Strategy Group, can help customize these financing solutions to fit your company's specific cash flow and growth goals.

This combination of flexibility and scalability makes lines of credit a compelling choice for businesses exploring inventory financing options.

Trade credit is a practical way to finance inventory, giving businesses the flexibility to receive goods upfront and pay for them later - usually within 30, 60, or 90 days. Think of it as a short-term, interest-free loan built into your supplier relationships [9][10]. Unlike traditional loans, trade credit doesn’t require a formal application or collateral beyond the goods themselves [9].

This method is widely used - an estimated 80% to 90% of global trade involves some form of trade credit. For small businesses, it’s the third most commonly used financing tool [10]. What makes it stand out is its ability to cover 100% of the purchase price, far exceeding the 50% to 80% advance rates typical of inventory-backed loans [3].

If you stick to the agreed payment terms, trade credit typically comes with a 0% interest rate [10]. However, many suppliers sweeten the deal with early payment discounts. For instance, a "2/10 net 30" term means you can get a 2% discount by paying within 10 days instead of 30. But missing the deadline can be costly - expect steep penalties, high interest rates, or flat fees, which can also damage your credit profile [9][10].

Trade credit usually operates on "open account" terms. This means the supplier ships your order along with an invoice that specifies the due date - commonly Net 30, Net 60, or Net 90 [12][13]. At the end of the term, the full invoice amount is due in a lump-sum payment [12][13]. This structure aligns with your inventory turnover, giving you time to sell the goods and generate revenue before payment is due [10]. For businesses with seasonal sales or fast-moving inventory, this timing can free up cash for other essentials like payroll or marketing [9].

For rapidly scaling companies, trade credit is a valuable tool for maintaining cash flow. Much like a line of credit, it grows with your business. As your order volumes increase, suppliers often extend higher credit limits without requiring additional applications [9]. Establishing a solid payment history with smaller suppliers early on can lead to better terms as your business grows [9].

To make the most of trade credit, always document the terms in writing, use tracking systems to monitor accounts payable, and negotiate longer payment windows as your purchasing power increases [9]. This approach helps preserve equity while funding operations, making trade credit an excellent choice for companies focused on cash flow efficiency during periods of rapid expansion [11][13].

Purchase order (PO) financing is a funding solution designed to cover the upfront costs of materials or production needed to fulfill a confirmed order. Unlike inventory financing, which helps businesses prepare for future sales, PO financing is specifically aimed at enabling companies to handle large orders without straining their working capital. In this setup, the financing provider pays your supplier directly, ensuring the order is fulfilled without delay [15][21][22].

This type of financing is particularly helpful for growth-stage companies, as it leverages the creditworthiness of your customers and the reliability of your suppliers rather than depending on your own credit history. With traditional banks approving only about 13.5% of small business loan applications, PO financing offers a quicker alternative - often within just a week - if your customer has strong credit [5][15].

PO financing generally comes with higher costs than traditional loans. Monthly fees range from 1.8% to 6%, and providers typically charge transaction fees of 2%–8% of the order value. Additionally, due diligence fees of $500–$1,000 per transaction are common. Because of these costs, PO financing works best for high-margin orders. Most lenders require a gross profit margin of at least 15% to 25% to ensure you can cover the financing expenses and still turn a profit [16][19][23].

Advance rates for PO financing usually fall between 80% and 100% of your supplier's costs. The exact percentage depends on factors like your customer's creditworthiness and your supplier's reliability. Suppliers who accept direct payments via wire transfer or Letter of Credit are more likely to secure 100% funding. In some cases, specialized providers may offer lower advance rates, starting at 40% of the total purchase order value [16][17][18][20]. These advance rates are designed to work in tandem with the financing costs mentioned earlier.

Repayment for PO financing is straightforward. Once your customer receives the goods, they pay the financing provider directly. The provider then deducts their agreed-upon fees and transfers the remaining balance to you. Repayment terms are short, typically ranging from 30 to 120 days, with an average of around 45 days [17][18][19].

PO financing is an excellent option for businesses looking to grow without giving up equity or taking on traditional debt. It allows rapidly scaling companies to handle large orders from major buyers, such as retail chains, while preserving their working capital. Considering that nearly 29% of startups fail due to a lack of funds, having access to transaction-specific financing tied to your sales volume can make a huge difference [22][23].

To maximize the benefits of PO financing, it’s essential to work with reliable manufacturers and ensure your profit margins can comfortably absorb the financing fees. This approach helps maintain liquidity while supporting your expansion efforts.

For companies navigating complex financing options, consulting with experienced advisors can provide clarity. At Phoenix Strategy Group, experts specialize in crafting tailored solutions like PO financing to align with your business’s growth goals.

A merchant cash advance (MCA) isn't exactly a loan. Instead, it's a way to get upfront cash by selling a portion of your future sales at a discount. Here's how it works: the financing provider gives you a lump sum, and in return, they take a fixed percentage (usually 10% to 20%) of your daily credit or debit card sales until the advance is repaid [24][25].

MCAs are among the most expensive financing options out there. Instead of charging interest, providers use a factor rate, typically between 1.1 and 1.5. For instance, if you receive a $10,000 advance with a 1.3 factor rate, you'll end up repaying $13,000 [24][25]. This can translate to an effective APR ranging from 50% to over 200% [25]. On top of that, origination fees generally fall between 1% and 5% of the advance amount, with additional fees sometimes tacked on [24]. It's critical to calculate the implied APR before committing to an MCA so you can compare it to other financing options.

The amount you can borrow depends on your monthly credit card sales. Most MCA providers require a minimum of $5,000 to $10,000 in monthly credit card transactions and at least 6 to 12 months of operational history [24][25]. The global MCA market hit $17.9 billion in 2023 and is expected to grow to $32.7 billion by 2032, showing increasing demand for this financing option [25]. Approval rates for MCAs are also high - around 84%, much higher than the approval rates for traditional bank loans [25].

Repayment is simple but frequent. A fixed percentage of your daily or weekly sales is automatically deducted. This setup adjusts with your revenue, so on slower days, the repayment amount is smaller. While this flexibility can ease cash flow pressures in the short term, frequent deductions may strain businesses with tight profit margins [25][26]. It's worth noting that the repayment period is generally short, and because the total repayment amount is fixed by the factor rate, paying off the advance early won’t save you money [25][26].

"MCAs can seem attractive because repayment flexes with your business's cash flow, adjusting automatically to your revenue levels. For example, when sales dip, repayment amounts scale down to match."

– Tucker McKay, Mercury [24]

Next, we’ll compare how accounts receivable factoring stacks up in terms of cost and repayment flexibility.

MCAs are ideal for businesses that need cash fast - sometimes within 24 to 48 hours - to jump on opportunities like stocking up on inventory ahead of a busy season [24][26]. This speed and accessibility make them appealing when traditional financing options take too long. However, their steep costs mean they should only be used if your gross margins can comfortably handle the fees. For most businesses, experts suggest exploring lower-cost alternatives like SBA loans or business lines of credit first [25].

It’s also a good idea to avoid using MCAs for long-term needs or stacking multiple advances, as this can lead to a cycle of escalating debt [24]. Growth-stage companies that can absorb the high fees may benefit from an MCA, but careful planning is essential. Services like those offered by Phoenix Strategy Group can provide the financial expertise needed to evaluate whether an MCA aligns with your company’s long-term goals.

Accounts receivable factoring allows businesses to sell unpaid invoices to a third-party factor in exchange for immediate cash. Instead of waiting the typical 30–90 days for customers to pay, you can receive 70%–90% of the invoice value upfront. Once your customer pays the factor directly, the remaining balance is released to you, minus the factoring fee [28].

Factoring fees typically fall between 1% and 5% of the invoice value per month [27]. This translates to monthly rates of around 1.15% to 4.5%, depending on factors like your industry, transaction volume, and the creditworthiness of your customers. While these fees are higher than traditional bank interest rates, the approval process focuses on your customers' credit rather than your own [27]. Additionally, factoring setup costs are minimal, especially when compared to inventory financing, which can incur due diligence expenses ranging from $10,000 to $20,000 [28].

"Invoice factoring is more flexible and cost-effective. In most cases, it should be deployed first. Inventory financing is more complex and expensive."

– Marco Terry, Managing Director, Commercial Capital LLC [28]

The advance rate determines how much of the invoice value you receive upfront. Typically, this ranges from 70% to 95%, depending on your customers' payment history and your industry [28]. For example, low-risk industries like transportation or staffing often qualify for rates as high as 95%, while higher-risk sectors like construction may see lower rates between 60% and 80% [29]. Once your customer pays the invoice, the reserve (the remaining balance) is released to you, minus the factoring fee [29]. This flexible funding approach stands apart from the fixed repayment schedules found in other financing options.

With factoring, there are no monthly installments. Instead, the transaction is settled when your customer pays the invoice [27]. At that point, you receive the reserve amount, reduced by the agreed-upon fee. Since the repayment structure depends on your customers' payment cycles rather than fixed deadlines, it offers flexibility. However, because factors often handle collections directly, it's crucial to choose a provider with a strong reputation [30].

Factoring is particularly advantageous for growth-stage businesses because it scales in tandem with your sales. The more invoices you generate, the more funding you can access [27]. This makes it an excellent option for companies growing too quickly for traditional bank lines or those labeled "unbankable" due to limited credit history. With funding often available within 24 to 36 hours of submitting an invoice, factoring provides liquidity far faster than inventory financing or bank loans [30].

Another perk? Factoring turns receivables - an existing asset - into cash without adding debt to your balance sheet, keeping your financials clean. However, businesses with thin profit margins should weigh the costs carefully, as the fees could outweigh the benefits. Factoring can also complement other financing methods by converting receivables into immediate cash, helping support cash flow during critical growth phases.

For tailored guidance, Phoenix Strategy Group can assist in determining if factoring aligns with your cash flow needs and long-term growth objectives.

Here’s a breakdown of the pros and cons for each financing option:

Lines of Credit offer low interest rates and the flexibility to borrow only what you need, paying interest solely on the amount used. They’re a great fit for businesses managing seasonal inventory or frequent restocking. However, they often require detailed financial documentation, which can be a hurdle for newer, growth-stage businesses [1][14].

Trade Credit allows you to finance inventory without interest - provided you meet the payment terms. This lets you use revenue from sales to cover inventory costs, making it a cost-effective option [2].

Purchase Order Financing provides upfront funding for large orders, which is helpful when cash flow is tight. However, it comes with higher transaction fees and depends heavily on having creditworthy customers [2][31][32].

Merchant Cash Advances are a quick way to access capital with minimal paperwork, making them ideal for urgent cash needs. The downside? They carry higher costs that can strain cash flow during slower sales periods. Bryan Gerson, co-founder of Clarify, explains:

"Merchant cash advance... payments adjust with your sales volume... making it a flexible option for businesses with fluctuating income" [4].

Accounts Receivable Factoring turns unpaid invoices into immediate cash, leveraging your customers’ creditworthiness. This is especially useful if traditional lenders aren’t an option. However, the fees - ranging from 1% to 5% monthly - can be challenging for businesses with tight profit margins. Despite the cost, this method provides liquidity that supports rapid growth [27].

The table below highlights key metrics for each financing option, helping you compare their costs, repayment structures, and ideal use cases.

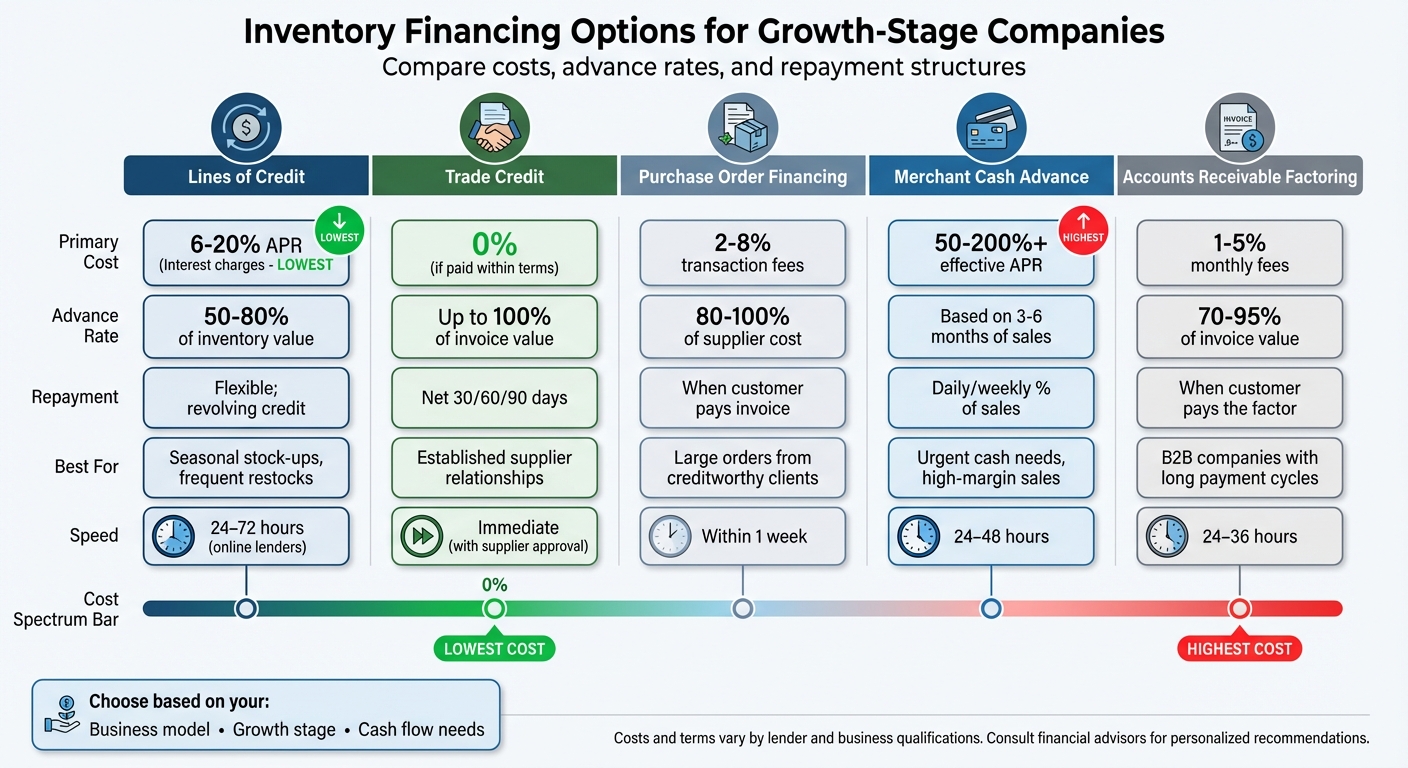

| Financing Option | Primary Cost | Advance Rate | Repayment Structure | Best Fit for Growth-Stage |

|---|---|---|---|---|

| Lines of Credit | Interest charges (lowest) [1] | 50–65% of inventory cost [1] | Flexible; revolving credit | Seasonal stock-ups, frequent restocks [1][14] |

| Trade Credit | None if paid within terms [2] | Up to 100% of invoice value [2] | Net 30/60/90 days [33] | Established supplier relationships [31] |

| Purchase Order Financing | Transaction fees [31] | Up to 100% of supplier cost [32] | When customer pays invoice [31] | Large orders from creditworthy clients [2][32] |

| Merchant Cash Advance | Percentage of sales (highest cost) [4] | Based on 3–6 months of sales [4] | Daily/weekly percentage of sales [4] | Urgent cash needs, high-margin direct sales [4] |

| Accounts Receivable Factoring | Fees between 1% and 5% per month [27] | 70–95% of invoice value [28][29] | When customer pays the factor [27] | B2B companies with long payment cycles [31][33] |

Matching the right financing option to your business needs is a key step in managing inventory effectively. Your choice should depend on factors like your business model, how quickly your inventory turns over, and the stage of growth you're in. For example, a fast-growing e-commerce company gearing up for Black Friday might need financing that supports a quick inventory buildup. On the other hand, businesses with stable cash flows might benefit from solutions like lines of credit, purchase order financing for large orders, or trade credit when there’s a strong relationship with suppliers.

Take early-stage logistics startups as an example - they’ve used revolving inventory lines to handle seasonal demand surges successfully. This approach not only improved supplier terms but also allowed for fleet expansion after repayment [34]. These cases highlight how aligning financing with your business specifics can turn inventory into a strategic advantage instead of a financial strain.

Accurate forecasting plays a crucial role here. A mismatch between financing and inventory needs can lead to stockouts or overstocking, both of which can hurt cash flow [5]. Phoenix Strategy Group’s fractional CFO services specialize in tailored cash flow forecasting, helping businesses model scenarios like how inventory turnover impacts repayment. Whether it’s using lines of credit for fast-growing e-commerce or factoring to support steady cash flows, their integrated FP&A and data engineering ensure precise liquidity planning. This alignment helps avoid unnecessary costs or equity dilution while keeping your business on track for growth.

Choosing the right financing, paired with solid planning and expert forecasting, can free up cash for other critical investments like marketing or hiring. It also gives you the flexibility to seize growth opportunities as they arise.

To find the right inventory financing option, start by understanding your business's specific needs, the type of inventory you manage, and how your cash flow operates. Options like asset-based lending or inventory lines of credit can offer flexibility, but choosing the right one requires careful consideration. Look closely at factors like repayment terms, the nature of your inventory, and how long you'll need the funding. By aligning your inventory levels with your cash flow timing, you can maintain liquidity and keep your business poised for growth. Choose a financing method that fits both your financial objectives and operational requirements.

Lenders usually expect businesses to have between 6 and 12 months of operating history and an annual revenue ranging from $50,000 to $100,000 to qualify for inventory-based financing. Additionally, they require thorough financial documentation during the application process, including income statements, balance sheets, and cash flow statements.

Yes, you can. Factoring allows you to sell unpaid invoices for immediate cash, giving your business a quick boost in cash flow without taking on additional debt. On the other hand, lines of credit and trade credit provide flexible funding options for ongoing financial needs. By combining these strategies, you can better manage liquidity during periods of growth or seasonal shifts. Factoring offers fast access to capital, while lines of credit and trade credit provide borrowing flexibility and extended payment terms.