Published on

March 17, 2026

The green construction sector is booming with mergers and acquisitions (M&A), but regulatory risks are reshaping how deals are structured. Buyers face challenges like retroactive liabilities, compliance hurdles, and valuation declines due to missed deadlines or evolving policies. Key takeaways:

Navigating these risks requires early compliance audits, structured deal terms, and expert guidance to protect valuations and ensure regulatory alignment.

City-by-City Green Building Compliance Requirements and Penalties

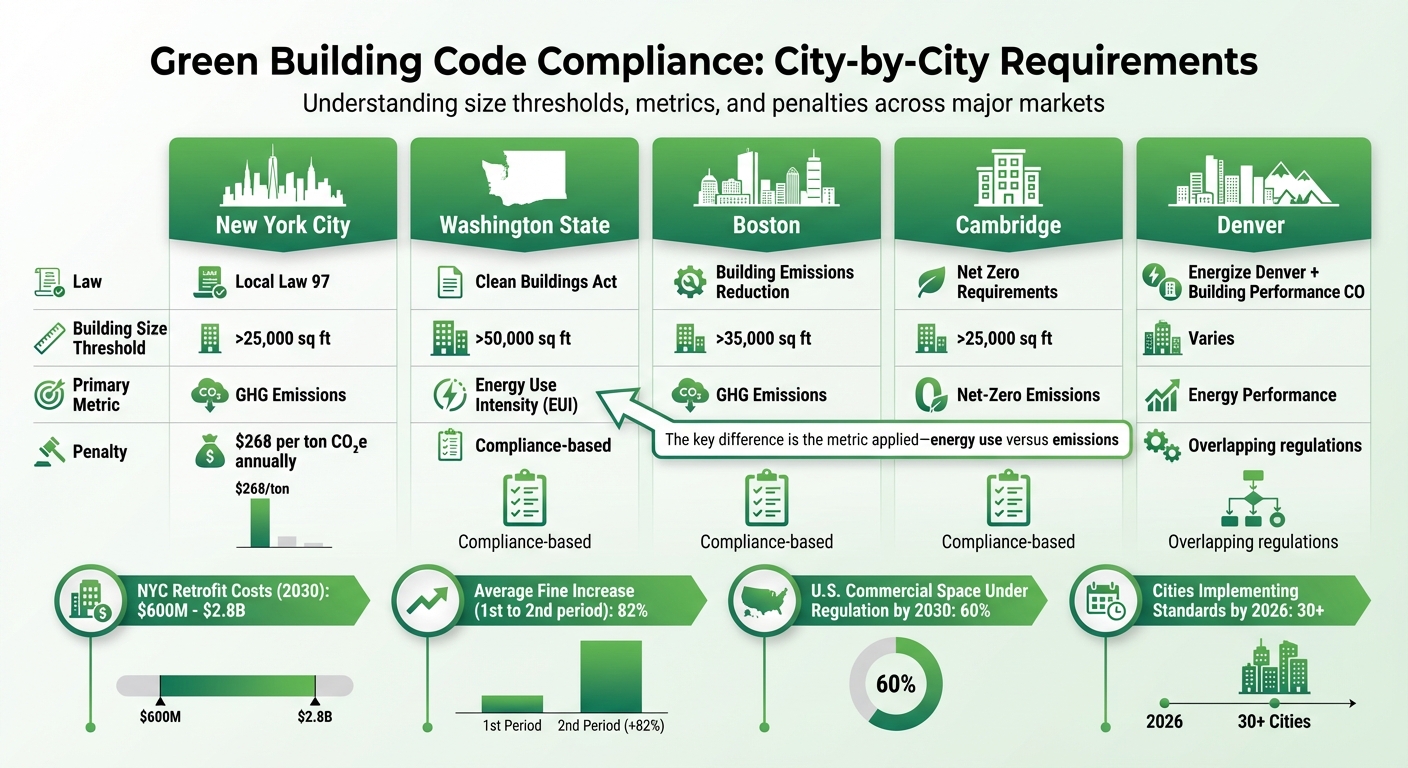

Green construction rules are anything but uniform, with federal, state, and local regulations often pulling in different directions. This patchwork of standards can make mergers and acquisitions (M&A) tricky, especially when a target company's compliance varies depending on the location of its assets. While federal incentives for energy reduction have been scaled back, state and local regulations have ramped up, creating a more complex environment for navigating building codes [6].

Local building codes are a big deal in M&A because they directly affect property valuation and potential liabilities. The standards themselves vary widely, focusing on different metrics like energy consumption or greenhouse gas (GHG) emissions, and often applying to buildings of different sizes. For example:

"The key difference is the metric applied - energy use versus emissions. This makes it rather complicated to track all of this manually." - Mike Zatz, Senior Vice President of Global Ecosystem Data and Partnerships [6]

The financial stakes are massive. In New York City alone, retrofitting buildings to meet 2030 targets could cost anywhere from $600 million to $2.8 billion, depending on the type of building [3]. Across major cities, fines are expected to jump by an average of 82% between the first and second compliance periods [6]. By 2030, around 60% of U.S. commercial square footage will be subject to energy regulations, with over 30 cities planning to implement building performance standards by 2026 [6].

Adding to the complexity are overlapping regulations. Take Denver, for instance, where state and city initiatives like "Building Performance Colorado" and "Energize Denver" create additional layers of compliance [6]. Meanwhile, states like New York and Colorado are introducing "All-Electric" mandates, phasing out gas-powered appliances in new buildings between 2026 and 2029 [4][5]. California is also stepping up, with updated energy codes requiring heat pumps and electric-ready designs by September 2024, aiming to cut 4 million metric tons of GHG emissions and save $4.8 billion in energy costs over time [5].

To navigate this maze of regulations, acquirers need to conduct thorough, multi-level compliance audits. These audits should assess local, state, and federal compliance simultaneously, as state rules often don’t override stricter local standards [6]. Structuring the deal wisely is also crucial. For instance:

Some states add extra layers of scrutiny. Connecticut's Transfer Act (CTA) and New Jersey's Industrial Site Recovery Act (ISRA) require environmental audits and filings before a deal can close, potentially delaying timelines if not addressed early [7]. In Michigan, completing a Baseline Environmental Assessment (BEA) within 45 days of acquisition offers protection against existing contamination liabilities [7].

Finally, using local penalty rates as a "shadow carbon price" can help acquirers gauge the long-term financial implications of a deal [3]. This approach ensures that potential costs tied to compliance are factored into the overall valuation, reducing surprises down the road.

Carbon reporting has become a key financial factor that directly influences enterprise value and can determine whether a deal proceeds or collapses [11]. By 2026, regulatory changes will increasingly enforce ESG reporting requirements [8].

The regulatory environment is becoming more fragmented. While federal climate regulations face ongoing legal challenges, individual states are stepping in with their own rules. For example:

"Penalties for noncompliance with this regulation can reach as high as $25,000 a day when enforced by the state government." - Green Building Law Update [12]

The consequences of non-disclosure go beyond fines. Failing to provide carbon performance data can be seen as a material breach of contract, giving buyers the right to terminate deals and potentially seek damages [12]. This is no small issue - over 50% of global dealmakers have canceled transactions after identifying ESG-related risks during due diligence [15]. On the other hand, 83% of M&A buyers are willing to pay more for businesses with strong ESG credentials, while 67% would lower their offers for companies with sustainability weaknesses [14].

Federal tax credits add another layer of complexity. The One Big Beautiful Bill Act (July 2025) introduced "Foreign Entity of Concern" (FEOC) restrictions that impact power plant owners and equipment manufacturers claiming tax credits under Sections 45Y, 48E, and 45X [10]. According to IRS Notice 2026-15, released in February 2026, power projects starting in 2026 must ensure at least 40% of equipment comes from non-prohibited foreign entities, with this requirement increasing to 60% by 2030 [10].

These shifting mandates highlight the importance of integrating carbon metrics into due diligence processes.

Traditional due diligence methods no longer suffice. Buyers must assess material ESG factors like energy use, emissions, and compliance with evolving regulations. To do this, they can use specialized frameworks such as SASB, GRI, or TCFD, while AI-driven carbon analytics help quantify climate risks and compliance costs [11]. Tools like Persefoni and Sphera allow buyers to model scenarios and evaluate the financial impact of carbon performance [11]. For FEOC compliance, taxpayers should also secure certificates from suppliers verifying they are not prohibited foreign entities [10].

An added challenge arises when new owners are required to report greenhouse gas emissions for the year prior to their ownership. This means sellers must transfer historical emissions data during the M&A process [12]. Aligning carbon accounting systems between organizations is critical, often requiring a 100-day post-merger integration plan to standardize reporting frameworks [11].

In the construction industry, the use of green materials presents unique challenges. Products like low-carbon concrete often lack historical performance data, which complicates project insurability. To address this, contractors increasingly involve insurers during the design phase to ensure coverage [9].

"Although green materials can reduce the carbon footprint of projects, they may increase material risk for the insurance market. Builders, operators, manufacturers, and suppliers should aim to provide sufficient historical data, testing, and performance guarantees on these products to facilitate their insurability in the markets." - Vincent Banton, Head of Construction & Infrastructure, Asia, Aon [9]

Carbon metrics are also being incorporated into deal terms through sustainability-linked earn-outs, where part of the purchase price is tied to achieving emissions reduction targets [11]. This approach keeps carbon performance front and center after the acquisition.

Meeting carbon reporting demands not only ensures compliance but also protects deal valuations, emphasizing the growing role of ESG in mergers and acquisitions.

The integration of carbon metrics into due diligence has made ESG procurement criteria a critical factor in shaping deal valuations within the sustainable construction M&A landscape.

Federal agencies are now required to prioritize sustainable products and services under FAR Subpart 23.1 and FAR 52.223-23, a mandate effective starting May 2024 [16]. This reflects the federal government’s growing emphasis on sustainability, with over $630 billion in annual spending. Notably, the General Services Administration (GSA) aims for 95% of new contracts to include green product requirements [16].

For construction companies, meeting these procurement standards is essential. Requirements include compliance with EPA-designated recovered materials, ENERGY STAR certification, and USDA BioPreferred products [16]. Buyers assessing acquisition targets must evaluate whether these companies can maintain access to the expansive federal market. Tools like the GSA’s Green Procurement Compilation (GPC) serve as benchmarks, and manufacturers failing to meet these criteria risk losing out on valuable government contracts [16].

This dynamic is especially challenging for small business contractors. Starting January 16, 2025, under Small Business Administration (SBA) rules, if a small business is acquired by a larger firm and cannot recertify as "small" within 30 days, it will lose eligibility for set-aside orders under Multiple Award Contracts (MACs) and Federal Supply Schedules [17]. This immediate loss of eligibility can severely impact a company’s valuation by cutting off access to critical revenue streams.

These procurement mandates don’t just secure government contracts - they also significantly shape acquisition valuations.

A strong ESG profile can directly influence acquisition outcomes. According to recent data, 83% of M&A buyers are willing to pay a premium for companies with solid ESG credentials, while 67% would seek a price reduction for companies that fall short on sustainability [1]. Companies with robust ESG practices often see 10–20% higher growth and valuations, along with operational cost reductions of 5–10% [16].

"Sustainability has grown from optional to essential for business success." – GOV.deal [16]

Sustainability is no longer a side consideration. A growing majority - 62% of businesses - now prioritize sustainability as much as, or more than, financial performance. Additionally, 37% of companies focused on sustainability report improved access to capital [16]. For acquirers, ensuring strong ESG compliance is critical to securing future revenue streams and staying competitive in a market that is increasingly shaped by regulatory demands.

Investors in sustainable construction M&A can gain an edge by leveraging specialized advisory services. Firms like Phoenix Strategy Group (https://phoenixstrategy.group) help stakeholders navigate evolving ESG standards and integrate them into acquisition strategies. Beyond driving valuation premiums, robust ESG practices also help mitigate regulatory risks, making them indispensable in green construction M&A.

Strong ESG practices at a target company don’t automatically protect acquirers from the risks tied to third-party suppliers. In green construction M&A, supply chain transparency has become a legal necessity. Acquirers can now face legal and financial consequences for ESG failures that occur deep within their supply chains. This growing emphasis on supply chain oversight aligns with earlier discussions on regulatory and carbon reporting, highlighting the importance of thorough due diligence.

New laws are pushing companies to monitor their supply chains at all levels. Regulations like the German Supply Chain Due Diligence Act (LkSG) and the EU Corporate Sustainability Due Diligence Directive (CSDDD) require businesses to identify, address, and resolve ESG risks across their entire supply chain - even for indirect suppliers they’ve never directly worked with [18][19]. Auditing just Tier 1 contractors is no longer enough.

"The age of plausible deniability is over. Companies are now expected to know, prevent, and mitigate such risks proactively." – smartKYC [19]

To meet these demands, many companies are moving away from manual compliance processes and adopting automated platforms. These systems use real-time data and OSINT (open-source intelligence) to flag supplier practices, such as forced labor or environmental violations [19]. They can map suppliers across multiple tiers, categorize them by risk, and monitor news in various languages for potential issues. Under German law, violations can result in fines of up to 2% of a company’s global revenue [19]. These automated tools are becoming essential for reducing risks after acquisitions.

Managing supplier liabilities doesn’t stop at the deal’s closing - it’s critical for protecting the value of the acquisition. Non-compliant suppliers can lead to massive financial fallout. For example, in 2023, DuPont, Chemours, and Corteva created a $1.185 billion settlement fund to address PFAS-related claims [1]. Cases like these show how environmental issues tied to suppliers can directly affect acquirers, especially under U.S. laws like CERCLA, which enforces strict liability for hazardous substances.

"When environmental liabilities surface after a deal closes, the consequences can be severe: plummeting valuations, securities litigation, and breach of fiduciary duty suits against directors and officers." – Woodruff Sawyer [1]

To avoid such risks, investors should involve ESG and environmental experts early in the deal process, rather than treating due diligence as a last-minute task [1]. Phase I Environmental Site Assessments now need to follow ASTM E1527-21 standards, which include PFAS pathways [13][1]. Warning signs include missing historical data, weak internal processes for identifying ESG violations, and the absence of PFAS screening at industrial sites [13][18]. Increasingly, acquirers are opting for asset purchases instead of stock deals to limit exposure to legacy liabilities and selectively accept specific obligations [13][1].

Setting up grievance mechanisms and whistleblowing channels can also help address issues tied to subcontractors before they escalate into costly legal battles [19]. Post-acquisition, maintaining "Bona Fide Prospective Purchaser" status under CERCLA requires careful adherence to land-use restrictions and cooperation with regulatory actions [13]. In cases where uncertainty lingers, pollution legal liability insurance can provide protection against unknown pre-existing claims and reassure lenders [13].

For companies navigating these intricate supply chain and compliance challenges in green construction M&A, working with specialized advisors - like those at Phoenix Strategy Group (https://phoenixstrategy.group) - can be a crucial step in structuring deals and managing risks effectively.

Green financing has become a key focus in sustainable construction M&A, especially as regulatory changes in 2025 reshaped the investment landscape. These shifts have amplified both risks and opportunities for stakeholders.

The transition from the Inflation Reduction Act (IRA) to the One Big Beautiful Bill Act (OBBBA) in July 2025 brought stricter eligibility rules and accelerated timelines by 6–8 years [20][22]. To qualify for the Investment Tax Credit (ITC) under Section 48E or the Production Tax Credit (PTC) under Section 45Y, projects must begin by July 4, 2026, or be operational by December 31, 2027 [22][23].

The 5% safe harbor rule, once a common path to eligibility, has been largely replaced by a physical work test. This means projects must show tangible progress, such as excavation, foundation work, or significant off-site manufacturing, to qualify for credits [20][22]. These changes have had a tangible impact: wind and solar investments fell by 18% to around $35 billion in the first half of 2025, and over $20 billion in clean energy investments were canceled due to the tighter OBBBA timelines [20].

Further complicating matters, foreign sourcing restrictions disqualify projects involving material support from Prohibited Foreign Entities (PFE) or Foreign Entities of Concern (FEOC), including those based in China or Russia [21][22]. Violations can significantly raise costs; for instance, battery projects that lose the 30% ITC due to FEOC sourcing violations could face a 42.9% hike in capital expenses [20]. Starting in 2026, projects must meet a 40% non-PFE content requirement, increasing to 60% by 2030 [22][24]. This puts about 83% of the 219 GW planned grid storage pipeline at risk of losing tax credits [20].

Projects that qualify for bonus credits - such as those located in Energy Communities or using domestic materials - can see tax incentives rise by 10 percentage points. This boost can reduce a project’s payback period from 7–8 years to 6–7 years [20]. However, policy uncertainty has led to higher discount rates and reduced EBITDA multiples across the sector.

"These headwinds... are leading to a rise in the cost of capital to all stakeholders in renewable energy projects as compared to just a few years ago" [20].

These stricter conditions are pushing acquirers to rethink their strategies.

In response to these challenges, acquirers are shifting their focus toward mature, credit-qualified assets [20]. Pre-notice-to-proceed (pre-NTP) funding for equipment and construction surged to over $7 billion in the first half of 2025 as developers rushed to meet the new deadlines [23].

To navigate these changes effectively, prioritize projects that have already passed the physical work test, such as those with completed excavation, foundation work, or racking installation, rather than those relying solely on financial safe harbors [22]. Rigorous due diligence is essential to ensure compliance with FEOC restrictions for every component and vendor [20]. Keep in mind that IP licensing agreements with specified foreign entities signed after July 4, 2025, can disqualify projects from earning clean energy credits [21].

In a high-interest-rate environment, the ITC may be more advantageous than the 10-year PTC because it offers a quicker five-year capital return, reducing sensitivity to discount rate fluctuations [20]. Performing sensitivity analyses across various policy scenarios - such as credit phaseouts or changes in energy pricing - can help identify key factors influencing profitability [20]. Additionally, cost segregation studies conducted by certified professionals can ensure accurate depreciation and ITC classifications, preventing overestimation of project value [20].

For tailored strategies to address these financing challenges, specialized advisory services - like those provided by Phoenix Strategy Group - can help structure transactions to maximize incentives while minimizing regulatory risks.

Waste management policies are shaping the way construction M&A valuations are approached. Federal mandates now require diverting at least 50% of construction and demolition (C&D) materials from landfills. This has led to a growing demand for products made with recycled content, creating both compliance hurdles and opportunities that influence deal valuations [25][27].

The Resource Conservation and Recovery Act (RCRA) obligates federal agencies to prioritize products with the highest recovered material content. This includes 61 designated products across eight categories, such as construction materials [26]. Additionally, Executive Order 14057 and the Infrastructure Investment and Jobs Act require the EPA to regularly update these standards, raising compliance demands for manufacturers [26][27].

The Federal Buy Clean Initiative emphasizes sourcing American-made, low-carbon materials like steel, concrete, asphalt, and glass that incorporate recycled components [25]. With agencies responsible for 90% of federally-financed construction materials participating in the Buy Clean Task Force, suppliers lacking Environmental Product Declarations (EPDs) risk being excluded from federal contracts [25]. Furthermore, thirteen states, including California, New York, and Washington, have aligned their procurement rules with federal guidelines through the Federal-State Buy Clean Partnership, intensifying market pressures [25].

During due diligence, it’s essential to check if target companies have Construction Waste Management Plans, designated C&D Waste Data Coordinators, and systems for tracking materials. These measures help ensure compliance and protect valuations [27]. Evaluating the recoverable value of salvaged materials, such as historic architectural elements or HVAC systems, can also help offset acquisition costs [27]. Additionally, demolition firms face stringent hazardous waste regulations under the RCRA and the Toxic Substances Control Act, covering materials like asbestos, lead-based paint, and PCB-containing components. Non-compliance can lead to substantial post-acquisition liabilities.

Beyond meeting these compliance standards, companies are now expected to adopt circular economy practices to enhance sustainability and maximize value.

Adopting circular economy principles has become a necessity in key markets. For instance, in March 2025, New York City introduced the Clean and Circular Design & Construction Guidelines, mandating 75% diversion of C&D waste and 95% reuse or recycling of concrete and soil for city-backed projects exceeding $5 million [29]. A notable example is the SPARC Kips Bay campus pilot project, which aims to cut 26,400 tons of CO₂e using mass timber and low-carbon concrete. Winning suppliers for this project have secured multi-phase contracts extending through 2031 [29]. Companies lacking third-party-verified Type III EPDs were barred from bidding entirely.

"If your product cannot document its GWP in kg CO₂e, it simply cannot count toward the 25% [low-carbon requirement]. An EPD is the only widely accepted receipt." - Toby Urff, Product Manager, Parq [29]

In the European Union, regulations like the Construction Products Regulation and Ecodesign for Sustainable Products Regulation require Digital Product Passports (DPPs) to track environmental impacts and end-of-life potential [28][30]. With buildings contributing 35% of all waste in the EU, these transparency measures are essential for market access [28][30]. Post-acquisition, companies must implement systems to monitor material lifecycles and demonstrate compliance with recyclability and durability standards.

Buyers should carefully audit a target company’s product catalogs for EPD gaps and assess their ability to meet waste diversion goals before finalizing any deals [29]. Drafting material take-back policies that facilities can execute ensures compliance with end-of-life recycling commitments [29]. These evolving regulations around waste management and circular practices are critical factors in due diligence, helping acquirers avoid potential liabilities while optimizing deal valuations. For tailored guidance on incorporating these practices into transaction strategies, firms like Phoenix Strategy Group can provide expert support.

Navigating policy risks in green construction mergers and acquisitions (M&A) requires careful planning and early action. With carbon reporting requirements and federal environmental regulations evolving rapidly, these factors are reshaping how acquisitions are evaluated and structured [31]. The earlier discussion about the influence of strict environmental mandates on deal valuations ties directly into this need for proactive risk management.

For instance, civil fines under the Resource Conservation and Recovery Act (RCRA) can soar to $50,000 per day [31]. However, the Department of Justice (DOJ) Safe Harbor Policy offers a significant incentive for companies to self-report misconduct within six months and complete remediation within a year [31].

"Compliance must have a prominent seat at the deal table if an acquiring company wishes to effectively de-risk a transaction" [31].

To address these risks, investors are increasingly involving compliance teams early in the process. These teams assess potential liabilities under key federal laws like the Clean Air Act, Clean Water Act, and RCRA. Based on their findings, deal terms are adjusted to shield against non-compliance risks - often through mechanisms like escrows or offsets [31].

Adding to the complexity, New York’s mandatory greenhouse gas (GHG) disclosures will come into effect in 2026, and the SEC’s ongoing review of ESG Fund Names Rules [31], along with the EPA’s focus on compliance enforcement, further compress the timeline for resolving legacy issues.

Given the growing regulatory pressures, expert advice is more critical than ever. Phoenix Strategy Group offers tailored support to growth-stage companies, helping them pinpoint compliance gaps, structure deal terms to minimize regulatory exposure, and build strong post-acquisition financial systems. Their expertise in financial planning and analysis (FP&A) and data engineering transforms regulatory hurdles into opportunities for competitive growth.

Buyers can sidestep unexpected environmental risks by performing detailed environmental due diligence. This process involves assessing potential issues such as soil or water contamination and addressing any legacy pollution tied to the property. Structuring the deal carefully and clearly defining responsibilities through representations is equally important. These measures ensure that environmental risks are identified and managed both before and after the transaction.

Diligence needs to pay close attention to city-specific green building regulations. This includes adhering to requirements such as net-zero carbon goals, energy efficiency standards, fossil fuel-free heating systems, embodied carbon reductions, EV charging infrastructure, and climate adaptation measures. Additionally, it’s essential to account for local mandates involving benchmarking, energy audits, retro-commissioning, and building performance standards to stay aligned with the ever-changing landscape of sustainability rules.

To qualify for OBBBA tax credits and adhere to FEOC limits, it's crucial to steer clear of any dealings with prohibited foreign entities (PFEs) or entities of concern (FEOCs). These typically refer to organizations influenced or controlled by adversarial nations such as China, Russia, North Korea, or Iran. Additionally, make sure to meet all legislative requirements regarding timing, ownership, and control to maintain compliance.