Published on

January 9, 2026

Section 382 is a tax rule that limits how much a company can use past net operating losses (NOLs) and other tax benefits after a major ownership change. This happens when 5-percent shareholders collectively increase their ownership by over 50 percentage points within three years. The annual limit on NOL usage is calculated by multiplying the company’s fair market value at the time of the change by the federal long-term tax-exempt rate.

Key points:

Failing to comply can lead to significant tax challenges. Companies should maintain detailed records, conduct regular testing, and seek expert advice to manage Section 382 impacts effectively.

An ownership change happens when one or more 5-percent shareholders collectively increase their ownership by over 50 percentage points from their lowest level during a rolling three-year testing period. This is a cumulative increase, not a 50% shift in the overall shareholder base [8][9].

The focus here is strictly on increases. For instance, if Shareholder A's ownership rises by 30 percentage points and Shareholder B's by 25 percentage points, the combined 55-point increase crosses the Section 382 threshold. Importantly, reductions in ownership by other shareholders don’t cancel out these increases.

Each time there’s an owner shift or an equity structure shift, the corporation must determine whether the 50-percentage-point threshold has been breached. If it has, the testing period resets the following day, starting a new three-year cycle.

A 5-percent shareholder refers to any individual or entity owning 5% or more of the corporation’s stock during the testing period [4]. Shareholders with less than 5% ownership are grouped together and treated as a single 5-percent shareholder, often called a "public group."

For example, in a public offering, even if no single investor buys 5% of the stock, the entire group of new investors is considered one 5-percent shareholder whose ownership increases from 0% to their combined post-offering percentage. In specific cases, like mergers, segregation rules might require tracking different public groups separately [4].

Ownership changes are typically triggered by two types of events: owner shifts and equity structure shifts.

Owner shifts include actions such as:

Equity structure shifts often result from tax-free reorganizations under Section 368, such as mergers or consolidations.

| Transaction Type | How It Triggers Section 382 |

|---|---|

| Stock Issuance | New shares dilute existing ownership, increasing stakes of new investors. |

| Stock Redemption | Repurchased shares raise the ownership percentage of remaining shareholders. |

| Merger/Reorganization | Tax-free mergers can immediately shift ownership if target shareholders hold less than 50% of the combined entity. |

| Public Offering | New public investors are treated as a single 5-percent shareholder, even if no individual owns 5%. |

Another scenario involves a shareholder owning 50% or more of the corporation who declares their stock worthless. In such cases, the IRS considers them to have reacquired the stock on the first day of the following tax year, potentially triggering an ownership change [4].

Next, we’ll break down how to calculate the annual limit imposed by Section 382.

How to Calculate Section 382 Annual Limitation: Step-by-Step Guide

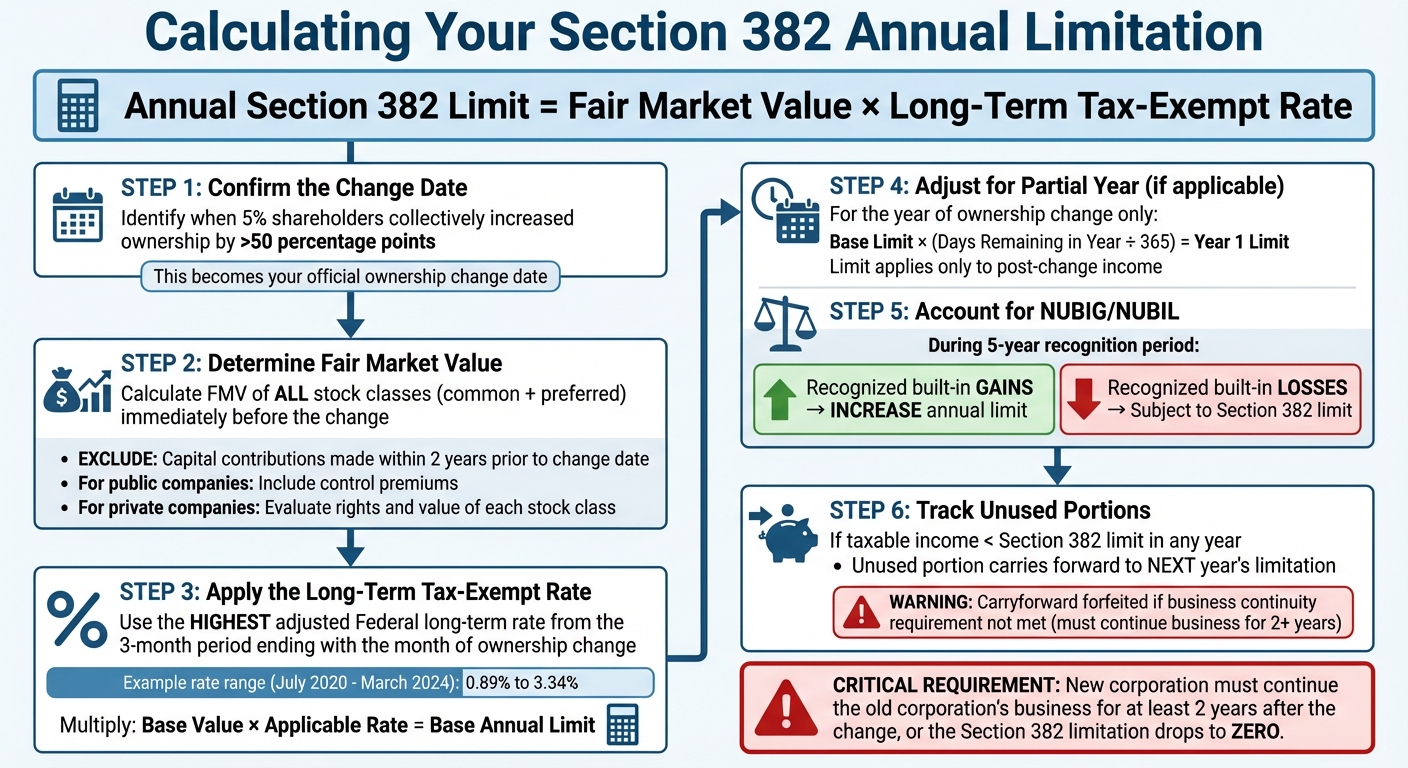

To calculate the annual Section 382 limitation, multiply the loss corporation's fair market value by the long-term tax-exempt rate [2][4][10]. This formula determines the maximum amount of pre-change losses the corporation can apply each year following an ownership change.

The value of the loss corporation includes all classes of stock - both common and preferred - measured immediately before the ownership change [2][4]. For private companies, you'll need to evaluate the rights and value of each stock class, while public companies should also consider potential control premiums [13].

The long-term tax-exempt rate is the highest of the adjusted Federal long-term rates in effect during the three-month period ending with the month when the ownership change occurs [2][3][4].

Start by confirming the change date when the 50-percentage-point ownership threshold is crossed. Then, determine the fair market value of all stock classes as of that date. Keep in mind that capital contributions made within two years prior to the change date are excluded from this valuation [2][4].

Next, multiply the base value by the applicable three-month long-term tax-exempt rate. For the year of the ownership change, the limit applies only to post-change income. To adjust for this, multiply the base limit by the ratio of the days remaining in the year to 365 [2][3].

If the corporation’s taxable income in any post-change year is less than the Section 382 limit, the unused portion carries forward to increase the limitation for the next year [2][4]. However, this carryforward is forfeited if the corporation fails to meet the continuity of business enterprise requirement. This rule requires the new corporation to continue the old corporation’s business for at least two years after the change [2][3].

Once the base calculation is complete, adjust it to account for any net unrealized built-in gains or losses.

Net unrealized built-in gains (NUBIG) and net unrealized built-in losses (NUBIL) can further modify the annual calculation. These represent the difference between the fair market value of the corporation’s assets and their aggregate adjusted basis before the ownership change [2][3]. Adjustments are only triggered if they exceed the smaller of 15% of the fair market value of the assets or $10,000,000 [2][12].

During the five-year recognition period starting on the change date, any recognized built-in gains increase the annual Section 382 limit [2][11]. For instance, if a corporation has a $120 million NUBIG tied to hypothetical goodwill, it could see an $8 million annual increase in its Section 382 limit during the recognition period [11]. On the other hand, recognized built-in losses are treated as pre-change losses and remain subject to the Section 382 limit [2][3].

When determining the threshold, exclude cash, cash items, and certain marketable securities where the value closely matches their basis [3][12]. Additionally, monitor asset sales or income items during the recognition period that qualify as recognized built-in gains, as these directly expand the ability to utilize pre-change losses.

Your cap table needs to do more than just list shareholders - it should also identify ultimate indirect owners hidden within investment vehicles and partnerships. Many growth-stage companies rely on records that only show direct shareholders, which can lead to blind spots when calculating the 5-percent shareholder thresholds. To avoid this, trace multi-tiered ownership structures to pinpoint ultimate controllers, such as private equity groups, partnerships, or holding companies.

Instead of waiting for a transaction or tax filing deadline, conduct regular Section 382 testing. Ownership changes can creep in through successive funding rounds or secondary market transfers, often going unnoticed until an IRS audit or buyer due diligence flags them. Testing quarterly or after each equity event can help you identify incremental shifts before they exceed the 50-percentage-point threshold.

Keep detailed records of every ownership change, noting the specific date and percentage shift. This includes stock issuances, redemptions, transfers, and option exercises. Your monitoring system should alert you when cumulative changes over the rolling three-year testing period approach the threshold. This gives you time to adjust deal structures or apply exceptions, such as the small issuance exception, which covers issuances totaling no more than 10% of the corporation's value at the start of the year.

By staying on top of these shifts, you’ll be better prepared for pre-transaction planning.

Before finalizing any deal, it’s important to model ownership changes under different investment scenarios. As GHJ Transaction Advisory Services advises, "a technical tax expert... can assist in modeling out the company's current owner shift and what it looks like in various investment scenarios" [6]. This analysis helps determine whether a transaction will trigger an ownership change and calculates the resulting annual limitation based on your company’s fair market value and the applicable long-term tax-exempt rate.

Evaluate the value of your pre-change NOLs (net operating losses) and how they align with the projected Section 382 limitation. Pre-2018 NOLs can offset 100% of taxable income but expire after 20 years, while post-2017 NOLs don’t expire but are capped at 80% of taxable income. If your company has substantial NOLs and the transaction will trigger Section 382, consider whether timing the deal during higher interest rate periods could secure a better annual limitation. For instance, between July 2020 and March 2024, the long-term tax-exempt rate rose from 0.89% to 3.34%, significantly affecting NOL utilization capacity [6].

Additionally, the new loss corporation must continue your business operations for at least two years following the ownership change date. Otherwise, the Section 382 limitation drops to zero. Buyers should include Section 382 analysis in their due diligence to uncover any previously triggered limitations that might reduce the value of your tax attributes.

After planning for ownership changes, staying vigilant post-transaction is equally important.

Maintaining compliance with Section 382 rules is essential to protect your tax strategy and maximize the value of pre-change losses.

Track your Section 382 limit usage every year and carry forward any unused portions to the next year’s limitation. For the year of the ownership change, consider making a closing-of-the-books election. This approach allocates pre- and post-change income and losses separately, allowing you to maximize the use of pre-change losses against pre-change income, rather than relying on the default method of proportional allocation based on days.

Keep an eye on asset dispositions for five years after the change date. Recognizing pre-change built-in gains during this period increases your Section 382 limitation for that tax year, while realizing built-in losses reduces it. To calculate these adjustments accurately, maintain detailed records of assets held at the change date, including their fair market values and adjusted tax bases.

If you’ve acquired another corporation through a Section 381(a) transaction, ensure separate accounting for the acquired company’s pre-change losses. This tracking continues until either the distributor/transferor corporation undergoes an ownership change or five consecutive years pass without such a change - a "fold-in event" [1][5]. Also, if you’re managing both Section 382 and Section 163(j) disallowed business interest carryforwards, remember that ordering rules typically require using interest carryforwards before NOLs, which can impact your annual Section 382 limit.

One of the biggest missteps companies make is failing to recognize when they qualify as a loss corporation. Since the introduction of the Tax Cuts and Jobs Act, disallowed business interest expense carryforwards under Section 163(j) now classify a company as a loss corporation, which brings it under Section 382 limitations [2][13]. Unfortunately, many finance teams still operate under the outdated belief that only net operating losses (NOLs) trigger these rules.

Another common mistake is overlooking multiple ownership changes. When a company goes through several financing rounds, each one can trigger a new Section 382 limitation. While companies may track the initial ownership change, they often miss subsequent ones, which can lead to compounded restrictions [13].

Valuation missteps also pose significant challenges. Companies sometimes undervalue a loss corporation by ignoring certain classes of stock or control premiums [13]. Additionally, they may fail to account for net unrealized built-in losses (NUBIL), which means that depreciation or amortization deductions tied to assets with pre-change built-in losses during the five-year recognition period fall under the Section 382 limitation [13]. Another frequent oversight is neglecting to treat warrants, options, or convertible debt as stock, potentially missing a trigger date [2][1]. These errors not only skew tax strategies but also create a domino effect of inaccuracies when managing ownership changes.

To mitigate these risks, it’s crucial to establish a testing date immediately after every equity event - whether it involves an ownership shift, issuance, or transfer of an option. This helps determine if an ownership change has occurred and avoids discovering limitations too late, such as during an IRS audit or buyer due diligence [1][5].

Taking a closer look at historical financing rounds can also uncover previously unrecognized ownership changes. Often, this kind of review reveals earlier shifts that may already be restricting your tax benefits. Additionally, when planning asset sales, consider holding onto assets with pre-change built-in losses for at least five years. This approach helps avoid subjecting those losses to the annual Section 382 cap [13].

Engaging an independent valuation firm to determine the fair market value of all stock classes just before a change date is another key step. This valuation directly impacts the annual limitation, and a well-documented process can safeguard against IRS challenges by ensuring the limitation is calculated as favorably as possible [13]. Including Section 382 covenants in shareholder agreements and equity incentive plans can also provide early warnings of transactions that might trigger limitations.

Given the complexity of Section 382 rules, working with expert advisors can make a significant difference. As Jessica L. Jeane, Director of Tax Policy at Baker Tilly, emphasizes:

"It is imperative that loss corporations have a thorough understanding of the aggregation and segregation rules under Sec. 382 to achieve the correct result in determining whether an ownership change under Sec. 382 has occurred" [14].

Navigating these rules becomes even more challenging when dealing with multi-tiered ownership structures, public groups, or exceptions. This is where experienced advisors can provide invaluable support.

For example, Phoenix Strategy Group specializes in helping growth-stage companies integrate tax limitation modeling into their financial strategies. Their fractional CFO services include tracking ownership changes across funding rounds, developing cap table systems to trace indirect owners, and conducting pre-transaction analyses to assess Section 382 impacts under different investment scenarios. By aligning tax strategies with a company’s growth plans, they help preserve the value of tax attributes while enabling necessary capital raises and strategic decisions.

Partnering with advisors who understand both the technical tax rules and the practical realities of running a business ensures compliance without sacrificing growth opportunities.

Section 382 imposes limits that can restrict the use of tax benefits like net operating losses (NOLs), disallowed interest expense carryforwards, and built-in losses. For growth-stage companies navigating multiple funding rounds, it’s critical to understand when an ownership change occurs and how to calculate the resulting limitations. This knowledge is key to preserving the value of these tax attributes.

Staying ahead of these changes requires ongoing monitoring. Ownership shifts can happen gradually, even through small transactions, making regular ownership studies a must. As Plante Moran highlights:

"Crossing these thresholds can cause significant tax challenges that executives can't address when they don't realize the limitations have been triggered" [7].

When a change is identified, quick and strategic action becomes essential. Tools like independent valuations, the small-issuance rule, and precise tracking of indirect ownership can help optimize tax outcomes during ownership transitions. Remember, the annual limitation is determined by multiplying your stock’s fair market value by the federal long-term tax-exempt rate [13][3], which caps the amount of tax attributes you can use each year.

Failing to comply with Section 382 doesn’t just mean losing tax benefits - it can lead to larger financial consequences. Regular monitoring, thoughtful transaction planning, and partnering with experienced advisors are crucial to maintaining compliance while pursuing growth. By staying proactive and seeking expert guidance, companies can safeguard their tax attributes and avoid costly missteps. For further assistance, consider working with specialists like Phoenix Strategy Group (https://phoenixstrategy.group), who help growth-stage companies navigate complex ownership and tax planning challenges.

To comply with Section 382, companies need to keep a close eye on ownership changes. The rules hinge on whether 5% shareholders increase their ownership by more than 50 percentage points during a testing period. Staying on top of this requires precise tracking of stock ownership and valuations.

Here’s how to maintain compliance:

If you’re unsure how to manage this process, Phoenix Strategy Group offers expert support. They can help set up reliable tracking systems and develop financial strategies to protect your net operating loss carryforwards.

Failing to meet the continuity of business enterprise (COBE) requirement under Section 382 can have a serious impact on a company's ability to use net operating losses (NOLs) or other tax benefits after an ownership change. If the COBE requirement isn't met, the company may lose the opportunity to offset taxable income with these attributes, which could result in higher tax bills.

To prevent this, companies need to carefully assess their operations and ensure they continue to carry out a significant portion of their historic business activities or maintain the use of a substantial amount of their historic assets. Seeking guidance from financial and strategic experts, like Phoenix Strategy Group, can provide valuable insights and help businesses handle ownership transitions with greater confidence.

Net unrealized built-in losses can lead to a corporation being labeled as a loss corporation, triggering the Section 382 limitation. This means the company can only use losses up to the annual limitation set by the rule. In contrast, net unrealized built-in gains are exempt from this restriction and don’t reduce the allowable loss amount.

Grasping this difference is essential for businesses dealing with ownership changes, as it directly affects how tax attributes like net operating losses can be used. Careful planning and strategic preparation can help minimize the challenges posed by Section 382.