Published on

March 18, 2026

Exiting a business is complex, and regulatory compliance is a critical part of the process. Without proper compliance, your deal could face delays, reduced valuation, or collapse entirely. Here's what you need to know:

Key steps include:

Proper preparation minimizes risks, simplifies the sale process, and maximizes your business's value. Begin early, conduct thorough audits, and work with legal and financial experts to ensure a smooth exit.

Business Exit Compliance: Key Statistics and Timeline for Preparation

Before selling your business, you need to ensure everything is legally sound. Potential buyers will carefully examine your corporate records during due diligence, and any gaps could slow the process or hurt your valuation. The goal here is straightforward: show that your business is properly registered, compliant, and in good standing in every jurisdiction where you operate. This preparation makes due diligence much smoother.

Start by confirming that all state filings are current. Most states require businesses to submit annual or periodic reports - sometimes called "statements of information" - to keep their public records accurate. These reports aren’t financial documents but rather administrative filings that include your business address, registered agent, and officer details [4].

Missing even one filing could lead to your business being labeled "Not in Good Standing" or "Inactive." This could not only affect your ability to enforce contracts but also result in late fees or, in extreme cases, administrative dissolution.

"The annual report is one of the most overlooked parts of ongoing compliance, and yet it's what keeps your business officially recognized, active, and in good standing" [4].

Filing deadlines vary by state, so check your local requirements. If needed, obtain Certificates of Good Standing, which typically cost between $20 and $50 each [9].

Make sure all your governing documents are accurate and complete. Buyers will review these to confirm your company's governance history and ownership structure, and any inconsistencies could raise concerns.

It’s a good idea to conduct a legal audit with your attorney at least five to seven years before you plan to sell [3][6][7]. This gives you enough time to resolve any issues that might otherwise derail the deal.

"Have your attorney perform a legal audit of your company to identify any concerns or discrepancies that need to be addressed" [6].

Pay special attention to buy-sell agreements and any clauses about ownership transfers. If you're selling to a related party, the sale must happen at fair market value - otherwise, the IRS might treat the discount as a taxable gift [7]. Also, double-check that officer and director information in your state filings matches your internal records to avoid any state inquiries [4].

Once your governing documents are in order, review your compliance in all jurisdictions where your business operates.

If your business operates in multiple states, you must be registered - or "foreign qualified" - in each one. Without proper registration, you could lose the ability to enforce contracts or file lawsuits in those states [8][9]. Buyers will look to confirm that you're registered wherever you have a nexus, which could be triggered by physical presence (like employees, inventory, or offices) or economic activity, such as $100,000 in sales or 200 transactions [9].

Make sure your registered agent information is up to date in every state where you operate. A registered agent is required to have a physical address and is responsible for receiving legal notices and service of process on your behalf [8][10].

Use state Secretary of State databases to confirm your business status is marked as "Active" or "In Good Standing" after every filing [4]. If you stop operating in a state, don’t forget to formally withdraw your foreign qualification. Otherwise, you’ll continue to accrue fees, taxes, and penalties unnecessarily.

"Until it formally withdraws, a corporation or LLC remains subject to the foreign state's annual report, franchise tax, and other compliance obligations" [10].

| State | Economic Nexus Threshold | One-Time Filing Fee |

|---|---|---|

| California | $500,000 | $100+ |

| Texas | $500,000 | $750 |

| New York | $500,000 + 100 transactions | $200+ |

| Florida | $100,000 | $70+ |

| Colorado | Varies | $70 |

Tax compliance is a critical step when preparing for a business exit. Buyers will closely examine your tax history, and any unresolved liabilities or unfiled returns can jeopardize the deal or even leave you exposed to personal liability. Your goal should be to meet all federal, state, and local tax obligations before finalizing the closure.

For the closing year, you’ll need to file a final income tax return. The specific form depends on your business structure:

Make sure to check the "final return" box on the respective form.

If your business is a corporation, you’re also required to file Form 966 (Corporate Dissolution or Liquidation) within 30 days of adopting a dissolution plan. For businesses selling assets, use Form 4797 to report gains or losses from items like equipment or vehicles. If the entire business is sold, both the buyer and seller typically file Form 8594 to document how the purchase price is allocated across assets.

Employment tax filings are another essential step. Submit your final quarterly (Form 941) or annual (Form 944) federal tax returns, issue final W-2s to employees (along with Form W-3 to the Social Security Administration), and file Form 1099-NEC for independent contractors paid $600 or more during the final year.

"Failure to withhold or deposit employee income, Social Security, and Medicare taxes can result in full personal liability for what's known as the Trust Fund Recovery Penalty." – Smith Patrick CPAs

At the state level, file Articles of Dissolution with your Secretary of State and cancel all state tax accounts, including those for sales tax, franchise tax, and withholding. Missing these steps can result in penalties that exceed $250 per month [5]. After completing all filings, send a formal letter to the IRS with your business name, EIN, address, and the reason for closure to officially close your account.

| Entity Type | Primary Final Federal Form | Key Additional Requirements |

|---|---|---|

| Sole Proprietorship | Form 1040 (Schedule C) | Schedule SE if earnings >$400 |

| Partnership | Form 1065 | Final Schedule K-1 for each partner |

| C-Corporation | Form 1120 | Form 966 (within 30 days of dissolution) |

| S-Corporation | Form 1120-S | Final Schedule K-1 for each shareholder |

| All with Employees | Forms 941/944 & 940 | Final W-2s and W-3 transmittal |

Once all returns are submitted, the next step is to secure a tax clearance certificate. This official document, issued by your state’s Department of Revenue, confirms that all tax obligations are satisfied as of a specific date. These certificates are critical because many states have successor liability laws, which could hold buyers accountable for unpaid taxes if the seller doesn’t obtain one.

Some states require a tax clearance certificate before you can legally dissolve or withdraw your business. Buyers and lenders often request these certificates to ensure there are no hidden liabilities. Since processing times vary by state, apply early to avoid delays.

Make sure an authorized officer, such as the CEO or CFO, signs the application, or provide a valid Power of Attorney. Most states won’t issue a certificate if you have outstanding returns, unpaid balances, or if you’re on a payment plan rather than fully paid. In certain states, employment taxes may require separate requests through the Department of Labor, while general taxes are handled by the Department of Revenue. Keep in mind that these certificates are usually valid for a limited period - often 90 days - so plan your application accordingly.

After completing all filings and securing clearance certificates, take a close look at the tax implications of your exit. Proper planning here can help you save money. For instance, when selling business assets, depreciation recapture is treated as ordinary income, while capital gains or losses are reported on Schedule D. Additionally, if you have suspended passive activity losses, your exit allows you to fully deduct these losses against other income. Net Operating Losses (NOLs) can also offset your tax liability.

If any business debt is forgiven during the exit, the canceled amount is generally taxable income unless it qualifies for specific IRS exclusions. Typically, the IRS has three years to assess additional taxes, but this can extend to six years if there’s a substantial understatement of income (25% or more).

For those owing less than $25,000 on their final balance, the IRS offers installment agreements. These plans cost $22 for automatic withdrawals or $69 for other payment methods [11]. Always settle all outstanding business debts and taxes before distributing remaining assets to owners to avoid personal liability.

"The IRS cannot close your business account until all necessary returns have been filed and all taxes owed are paid." – Internal Revenue Service

Lastly, retain tax and payroll records for at least seven years. Employment tax records should be kept for a minimum of four years. This thorough review ensures you’re fully prepared for a smooth and compliant business exit.

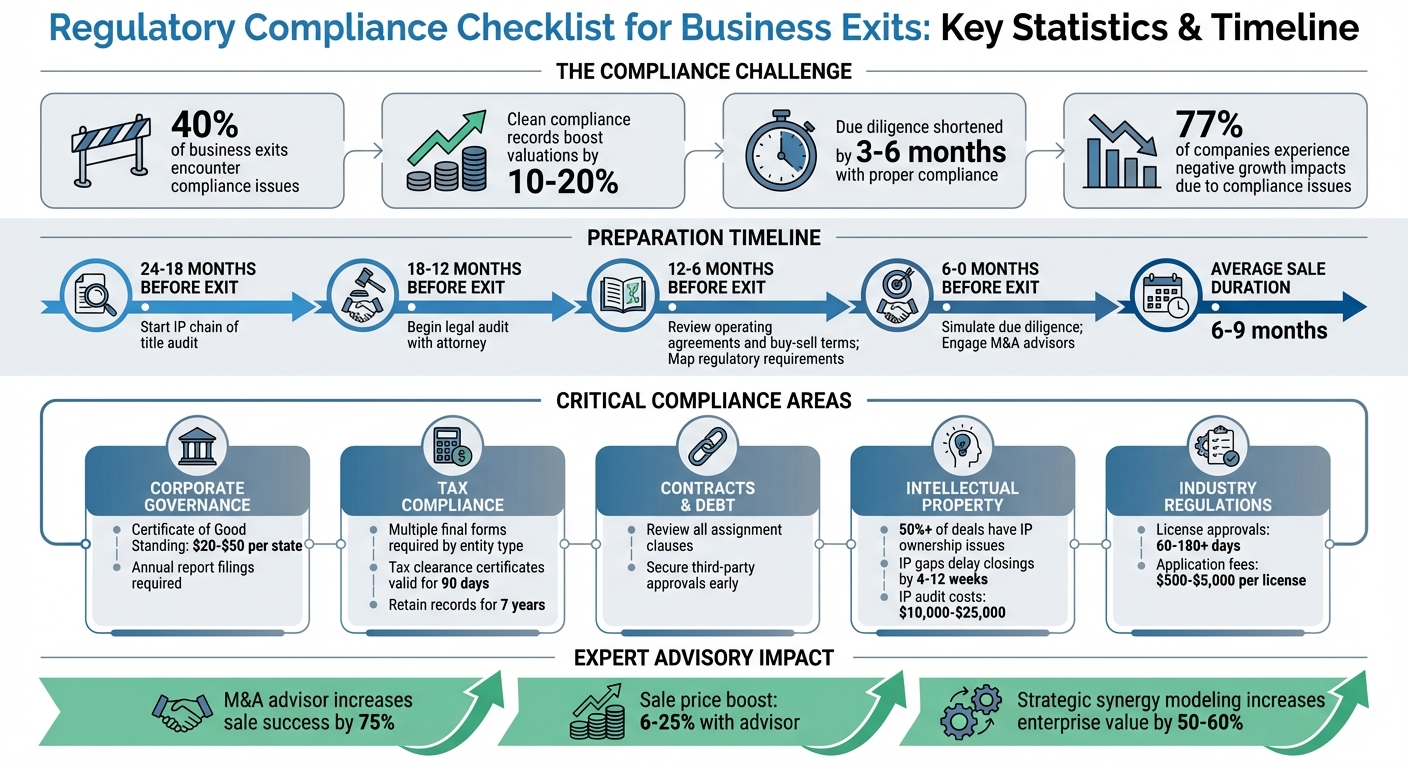

Before you finalize your business exit, it's critical to address all your contractual and debt-related obligations. These steps ensure your legal and financial records are in order, making your business more appealing to buyers. Potential buyers will examine every agreement tied to your business, and unresolved issues can jeopardize the deal or lower your sale price. On average, selling a business takes 6 to 9 months [12], which aligns with the 12–24 month preparation timeline often recommended for a smooth exit.

Start by reviewing every agreement - whether it’s with customers, vendors, or landlords - for assignment clauses or change of control provisions. These clauses often require third-party approval before you can transfer agreements to a buyer [13][14]. For instance, a landlord may need to approve the new tenant, or a vendor might demand renegotiation of pricing terms. Identify all third parties, such as landlords or suppliers, who need to provide written consent, and secure these approvals early to avoid last-minute complications [12][13]. If you operate a franchise, carefully review the franchise agreement for specific requirements like mandatory notifications, franchisor approvals, or "right of first refusal" clauses [12].

To streamline due diligence, organize all agreements into a consolidated folder well in advance. If you have any informal arrangements with suppliers or customers, formalize these into signed contracts [14]. Buyers are unlikely to accept verbal or informal agreements.

"Due diligence is the buyer reducing uncertainty. The more you reduce uncertainty early, the smoother the process tends to be." – Voyant Legal [14]

Additionally, check for any UCC filings or liens on assets, as these must be cleared before transferring ownership [14].

| Document Type | Review Focus for Exit | Transferability Consideration |

|---|---|---|

| Operating Agreement | Buy-sell terms, voting thresholds | Does it require unanimous consent for a sale? |

| Lease Agreements | Assignment clauses, remaining term | Will the landlord allow the buyer to take over? |

| Vendor Contracts | Exclusivity, termination rights | Can the buyer maintain the same pricing/terms? |

| Customer Contracts | Change of control, term length | Does the customer have the right to cancel? |

| Loan Agreements | Covenants, prepayment penalties | Does the sale trigger immediate repayment? |

Once contracts are reviewed, turn your attention to any loan agreements or credit lines. Go through each loan document to identify covenants that could impact your exit. Some lenders require full repayment if ownership changes, while others may impose prepayment penalties. If your loan includes consent clauses or a "right of first refusal", begin discussions with your lender as early as possible to avoid delays [12]. Also, ensure any pending litigation or unresolved tax issues are resolved before listing your business [12].

At least 6 to 12 months before your planned exit, review your Operating Agreement or Shareholder Agreement [14]. These documents outline who has the authority to sell, what happens if a partner wants to exit, and whether co-owners can block the transaction. Missing or outdated provisions are a common cause of delays or disputes during the sale process [14].

"Even a simple review of governing documents and buy-sell terms can prevent last minute disputes about price, authority, or who has the right to approve the sale." – Voyant Legal [14]

Make sure all buy-sell terms are clear and up to date. Resolve any discrepancies in unsigned agreements or outdated records that no longer reflect your business’s current operations [14]. It’s also wise to consult with both an M&A attorney and a CPA before signing a Letter of Intent (LOI). The LOI often determines the deal structure - whether it’s an asset or stock sale - which directly impacts how contracts are transferred [13][14].

"The biggest mistake is waiting until the LOI is signed to talk through tax impact. By then, you may be negotiating from a smaller set of options." – Voyant Legal [14]

When it comes to selling your business, intellectual property (IP) and other assets often play a huge role in determining its value. Buyers dig deep to verify that you own what you’re selling and that these assets can be transferred without restrictions. This process ensures your asset records are airtight, meeting the high standards of due diligence during an exit. Properly presenting your intellectual property can significantly boost your company’s valuation - potentially moving from a 4x revenue multiple to 7x or higher [15]. However, IP ownership issues arise in over half of lower middle market deals, often delaying closings by 4 to 12 weeks [18].

Start by creating a detailed inventory of your intellectual property. This includes patents, trademarks, software, proprietary algorithms, databases, branding materials, and digital assets [17]. If any digital assets are still registered to founders, make sure they’re officially transferred to the company [16][17].

Ownership documentation is equally critical. Review and confirm IP assignments from everyone who contributed - founders, employees, and contractors alike. Standard offer letters often don’t cut it; specific IP assignment clauses are necessary [15][16]. If you’re dealing with a portfolio involving just 10 contributors, fixing documentation gaps could take 16 to 24 weeks due to scheduling and negotiations [18]. To stay ahead, start an IP chain of title audit 18–24 months before your planned exit [18].

"IP is not just paperwork. It's power. And diligence is how you make sure you're actually buying it." – PatentPC [16]

Organize your due diligence materials, including patent and trademark filings, maintenance records, and open-source audits [15][16]. Review licensing agreements for clauses that might restrict transfers, like “change-of-control” terms, and ensure compliance with open-source software rules to avoid sharing proprietary code [15][16]. Protect trade secrets by marking confidential information, limiting access, and using NDAs with employees and vendors [15][16].

Ensure all business assets, licenses, and permits are correctly titled and transferable. Map out contributors and confirm that all have signed proper IP assignment documents [18][16]. Early employees and contractors often present gaps, especially if they used their own agreements without assignment clauses [18]. Founders sometimes mistakenly believe ownership transfers automatically, but formal assignment documents are required for any IP created before the company was incorporated [18][20].

Double-check the legal status of patents and trademarks with the USPTO or other registries to confirm they’re granted, pending, or properly maintained [16]. Confirm that digital assets are registered under the company’s name [16][17]. Also, review all licenses - both inbound and outbound - for restrictions that might complicate asset transfers [16][19]. Before the transaction begins, separate personal assets from company-owned ones to avoid confusion [19].

| Contributor Type | Required Documentation | Common Gaps |

|---|---|---|

| Founders | IP Assignment Agreement | Often missing; founders assume ownership transfers automatically [18]. |

| Employees | Employment Agreement with invention assignment | Early employees may lack formal agreements; technical staff may have incomplete versions [18]. |

| Contractors | Services Agreement with explicit IP assignment | Verbal agreements or contractor-provided templates without assignment language [18]. |

| Acquired Entities | Acquisition docs plus contributor agreements | Inherited gaps not resolved during prior acquisition diligence [18]. |

Once ownership is confirmed, address any issues that might prevent a smooth transfer.

Buyers will require assurances in the purchase agreement that all assets are owned “free and clear of liens or claims” [20]. Unresolved liens can lead to escrow holdbacks or even lower the valuation [18][20]. To avoid these problems, conduct an internal audit of your asset portfolio 18–24 months before your exit to identify and resolve any liens or encumbrances [18][20].

Carefully review third-party agreements for assignment restrictions or change-of-control clauses that could complicate transfers [19][20]. Ensure all employees and contractors have signed explicit assignment agreements to prevent future ownership disputes [18][20]. If you can’t resolve a lien or encumbrance before closing, consider options like representations and warranties (R&W) insurance, escrow holdbacks, or specific indemnities to address buyer concerns [18][16]. In asset sales, make sure every piece of intellectual property is explicitly listed and assigned in the purchase agreement to avoid leaving any encumbrances behind [20].

"IP chain of title is about provenance - proving that ownership rights transferred clearly at each point where intellectual property changed hands or was created. Think of it like title insurance for real estate." – ExitReadyAdvisors [18]

An IP audit and legal review can cost anywhere from $10,000 to $25,000, depending on the complexity of your company and portfolio. Resolving ownership gaps with contributors can run between $5,000 and $50,000, depending on the contributor’s leverage and the importance of the IP [18].

When preparing for a business exit, industry-specific regulations can play a critical role. Beyond meeting general legal and financial standards, your compliance with sector-specific rules will be closely examined by potential buyers. Any lapses here could delay or even derail the sale.

"Ignoring or mishandling these aspects can lead to significant legal and financial repercussions, potentially derailing the entire exit plan." – Vincent Mastrovito, Founder, Prometis Partners [21]

These specialized regulations work in tandem with broader compliance measures to ensure the process runs smoothly. Research shows that 77% of companies have experienced negative growth impacts due to compliance issues [25].

Every industry has its own set of compliance challenges:

If you discover gaps in compliance, create a plan to address them. This might involve updating policies, securing missing permits, or retraining your team [21].

Data privacy is another critical area during a business sale. Transferring personal data is much more complex than selling physical assets or intellectual property. Laws like the Virginia Consumer Data Protection Act (VCDPA) and the California Consumer Privacy Act (CCPA) govern how personal information can be handled during a sale [23]. If your privacy policy promises not to share data with third parties, transferring that data could lead to legal violations [23].

Sensitive data - such as health, biometric, or financial information - requires even stricter oversight. For example, under Section 363 of the U.S. Bankruptcy Code, courts may appoint a privacy ombudsman to ensure data transfers align with stated privacy policies [23].

"Privacy policies must reflect your intentions. If your privacy policy states you 'do not share data with third parties,' transferring that data in a sale may violate consumer trust - and potentially the law." – Moore Christoff & Siddiqui [23]

To prepare, conduct a privacy audit to catalog what data you collect, where it’s stored, and how it’s shared. Notify users about the sale and offer options for data deletion or opting out of transfers [23]. If data won’t be transferred, securely delete it following NIST SP 800-88 guidelines for cloud systems, local servers, and physical devices [23].

Licenses and permits can be one of the trickiest parts of a business exit. Many are not transferable and may require new applications instead of simple updates [24]. The timeline for approvals varies widely - professional licensing boards may take 60–120 days, environmental permits 90–180 days, and certain licenses (like liquor or cannabis) could take over a year [24].

For instance, healthcare businesses need to ensure compliance with HIPAA, medical waste permits, state medical and nursing board licenses, DEA registrations, and controlled substance licenses [22][24]. Financial services firms must verify Form ADV disclosures, SEC/FINRA compliance, AML policies, and state-specific licenses for money transmitters, investment advisors, and lenders [22][24][25]. Restaurants often deal with non-transferable liquor licenses, along with health department and food safety certifications [22][24].

"Compliance isn't a formality. It's deal insurance. Skip it, and you risk delays, price cuts, or failed closings." – Anthony Whitbeck, CEO and Owner, Advisor Legacy [25]

To avoid last-minute issues, start mapping out regulatory requirements 6 to 12 months before listing your business. Notify agencies and begin any necessary reapplications early [24][25]. Document every state where your business operates or holds licenses to identify overlapping requirements [24]. Check whether licenses are tied to the property or the owner, as some states require 30- to 90-day advance notice for ownership changes [24].

Finally, budget for associated costs. Application and filing fees can range from $500 to $5,000 per license, while legal counsel and compliance consultants may cost $5,000 to $50,000 and $10,000 to $100,000 respectively for complex scenarios [24].

Once you've addressed legal, tax, and asset compliance, the next step is advanced financial planning. This phase is critical for ensuring a seamless exit. Proper financial oversight helps you stay ahead of regulatory requirements, minimize risks, and maximize value. Financial experts use tools like forecasting and scenario planning to identify potential issues that could impact profitability before they arise.

A Quality of Earnings (QoE) report is a key part of pre-exit financial preparation. This report ensures that your earnings are both sustainable and backed by credible data. Financial experts also look for liabilities that could jeopardize a deal, such as unresolved legal disputes, undocumented workers, or improper tax filings. The goal is to normalize EBITDA by distinguishing recurring profits from one-time expenses and documenting acceptable add-backs.

To set yourself up for success, start this process 2 to 4 years before your planned sale. During this time, focus on cleaning up financial reports and implementing necessary controls. As you approach the final 6 to 12 months, experts can simulate due diligence to anticipate buyer questions and address any weak points. This phase also involves ensuring financial statements are consistent, timely, and prepared on an accrual basis. At least three years of clean, audited records are essential, and separating personal expenses from business accounts demonstrates strong operational integrity.

| Phase | Timing Before Sale | Focus |

|---|---|---|

| Foundation | 2–4 Years | Clean financial reporting and establish robust controls |

| Optimization | 12–24 Months | Focus on EBITDA growth, KPI tracking, and operational improvements |

| Readiness | 6–12 Months | Prepare QoE reports, simulate due diligence, and engage bankers |

| Transaction | 0–6 Months | Execute and close the deal |

A fractional CFO can ensure your financials meet buyer expectations by identifying the key drivers of revenue and cash flow, such as customer acquisition cost (CAC), contribution margin, and unit economics. These are the metrics buyers rely on to assess value. Additionally, working with an M&A advisor significantly increases the likelihood of a successful sale - by up to 75% - and can boost the final sale price by 6% to 25% [26].

These experts also help reduce dependency on the founder by establishing financial systems and decision-making frameworks. This ensures your business can operate independently, making it a more attractive and transferable asset. To determine an accurate valuation, financial experts use methods like Discounted Cash Flow (DCF), Comparable Companies (Comps), and Precedent Transactions. They also employ strategic synergy modeling to identify potential revenue, cost, and operational synergies, which can increase enterprise value by 50% to 60% compared to a purely financial valuation approach [27].

For growth-stage companies, Phoenix Strategy Group offers tailored fractional CFO and M&A advisory services. Their expertise includes cash flow forecasting, compliance verification, financial modeling, and KPI development. These services are designed to help businesses navigate the complexities of regulatory compliance and maximize value during the exit process.

Strategic financial preparation not only enhances operational readiness but also ensures your business is positioned for a successful and profitable exit.

Navigating the regulatory landscape is a critical step toward a successful business exit. Any unresolved compliance issues can directly impact your company’s valuation at the time of sale. To avoid this, it’s crucial to identify and resolve any discrepancies early on by conducting thorough legal and financial audits[1].

The best exits don’t happen by chance - they follow a well-thought-out timeline. Begin preparing for compliance well ahead of your planned sale. This includes cleaning up your financial records and implementing solid internal controls. Afterward, a self-audit can help highlight high-risk areas like intellectual property, contract transferability, and tax clearance. Tackling these issues early can help you secure the highest possible value for your business.

It’s also essential to bring in the right professional advisors. CPAs, attorneys, and financial experts can help you avoid costly mistakes. Regular check-ins with your advisory team to review operating documents, tax planning, and compliance measures can save significant headaches down the road. For example, fractional CFOs are particularly effective at spotting covenant breaches or compliance gaps, potentially preventing up to 25% of deal-breaking issues[1][2].

If you’re looking for expert guidance, Phoenix Strategy Group offers specialized support for growth-stage companies. Their services include compliance verification, cash flow forecasting, financial modeling, and KPI development - tools that can help ensure your business is in top shape for a successful exit.

Don’t wait. Start assembling your advisory team and schedule a detailed compliance review. By systematically addressing each area of concern, you’ll position your business for a smooth and profitable exit.

Common roadblocks in business sales often stem from compliance issues such as incomplete or outdated legal filings, missing ownership or corporate records, and unmet industry-specific licensing or permit requirements. These problems don't just slow things down - they can lead to fines, lawsuits, or even regulatory investigations, adding layers of complexity and delay to the process.

Buyers often ask for tax clearance certificates and good standing certificates to verify that a seller is meeting their tax and legal responsibilities. These documents typically confirm that the business has up-to-date tax filings and complies with regulations, ensuring it maintains a positive standing with the appropriate authorities.

Starting an intellectual property (IP) and contract transfer audit well in advance of your planned exit is a smart move. Ideally, this process should kick off several months before the exit to allow enough time to identify and resolve any potential issues. It also helps synchronize this review with other critical preparations, such as meeting regulatory requirements, conducting financial due diligence, and ensuring legal readiness. Taking action early can make the entire transaction process much smoother.