Published on

December 12, 2025

When you exercise incentive stock options (ISOs), you may face the Alternative Minimum Tax (AMT) - a parallel tax system that can result in a higher tax bill. This happens because the "bargain element" (the difference between the stock’s fair market value and your exercise price) is treated as income for AMT purposes, even if you haven’t sold the shares. For example, exercising 10,000 ISOs at a $1 strike price with a $50 fair market value creates $490,000 in AMT income, potentially leading to a substantial tax liability without receiving any cash.

To reduce AMT, here are actionable strategies you can use:

Planning ahead - especially before major events like IPOs or acquisitions - can help you minimize AMT, manage cash flow, and maximize long-term gains. Start by reviewing your stock option details, income projections, and potential AMT triggers. Consulting a tax advisor can provide tailored guidance for your situation.

How AMT Works with ISO Stock Options: Calculation Process and Tax Impact

Let’s dive deeper into how Incentive Stock Options (ISOs) interact with the Alternative Minimum Tax (AMT) and what that means for your tax situation.

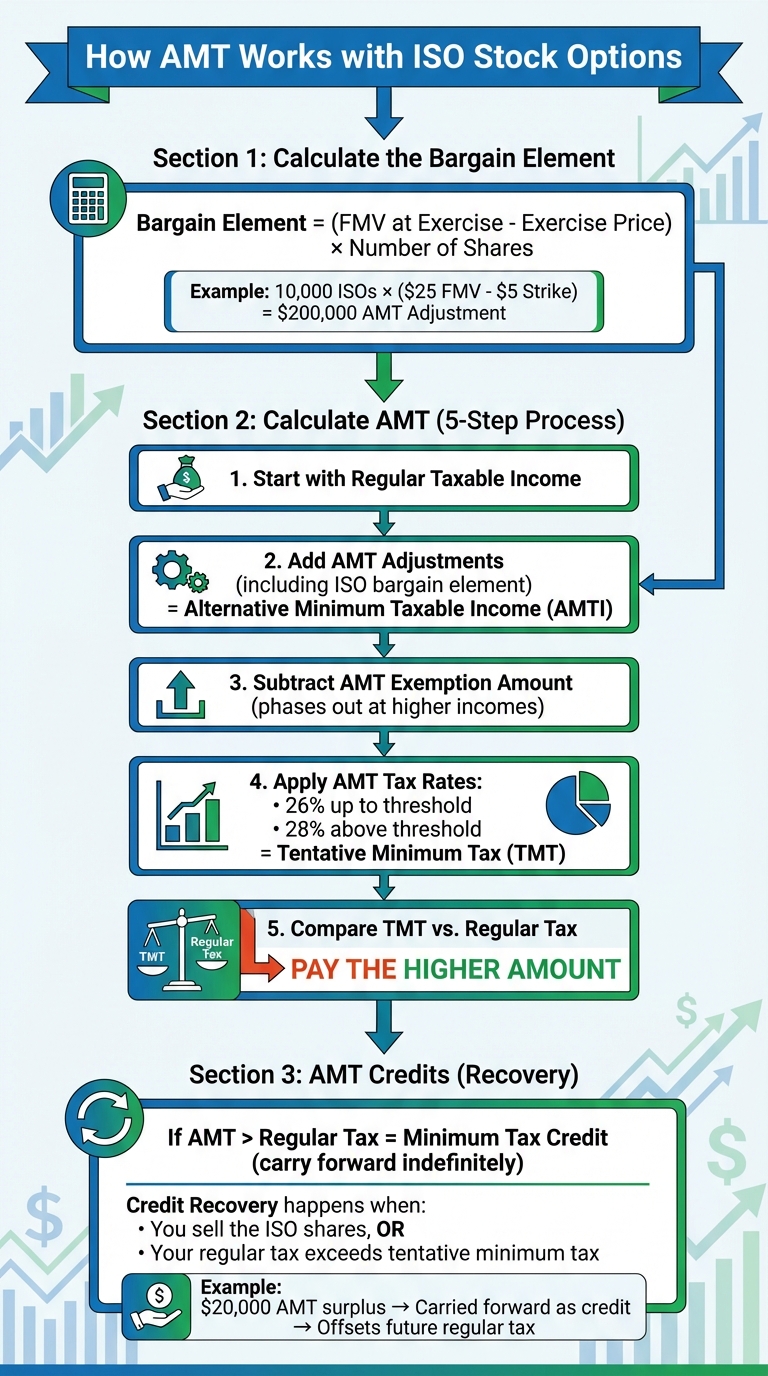

When you exercise ISOs, the bargain element - the difference between the strike price and the fair market value (FMV) at the time of exercise - creates an AMT adjustment. Here’s the formula for calculating the bargain element:

Bargain element = (FMV at exercise − exercise price) × number of shares

For example, if you exercise 10,000 ISOs with a $5 strike price when the FMV is $25, you generate a $200,000 AMT adjustment. While this amount isn’t taxable under the regular tax system at the time of exercise, it is added to your Alternative Minimum Taxable Income (AMTI). [2][4][7]

The AMT is essentially a parallel tax system designed to ensure that individuals with certain tax benefits or adjustments still pay a minimum level of tax. Here’s a simplified breakdown of how it works:

Finally, you compare your tentative minimum tax (TMT) to your regular tax. You’ll pay whichever amount is higher. [2][7]

Once you’ve calculated your tentative tax, the next step is understanding how AMT credits can help reduce your tax burden in future years.

If your AMT liability exceeds your regular tax due to ISO exercises, the excess becomes a minimum tax credit, often referred to as an AMT credit. This credit can be carried forward indefinitely and applied to reduce your regular tax in years when you’re no longer subject to AMT. However, it’s important to note that the credit cannot lower your tax below the AMT that would otherwise apply.

Recovery of the AMT credit typically happens in two scenarios:

For instance, if you have a $20,000 AMT surplus one year, this amount could be carried forward as a credit. In a future year, when your regular tax liability surpasses your tentative minimum tax, the credit would then offset part or all of the difference. [2][5]

Understanding these mechanisms is key to managing the tax implications of ISOs and planning for future tax years effectively.

To keep your Alternative Minimum Tax (AMT) in check, it's crucial to manage the bargain element that gets added to your Alternative Minimum Taxable Income (AMTI). By carefully planning the timing and size of your Incentive Stock Option (ISO) exercises, you can avoid crossing AMT thresholds while still benefiting from the potential gains of your stock options.

One effective way to manage your AMTI is to spread your ISO exercises over several years. This approach helps keep your annual AMTI at manageable levels. Many tax advisors recommend calculating your AMT crossover point each year - this is the maximum bargain element you can recognize before your tentative minimum tax surpasses your regular tax. Think of it as an annual "AMT budget" for your ISO exercises [3].

For instance, if you have 50,000 ISOs with a $10 spread per share, exercising all of them at once would create a $500,000 bargain element, likely triggering a hefty AMT liability. Instead, exercising 10,000 shares annually over five years would add just $100,000 of bargain element each year, potentially keeping you under the AMT threshold. Consult with a tax advisor, such as Phoenix Strategy Group, to calculate your annual AMT budget. This strategy also works well with other methods, like exercising during periods of low spread.

Another way to reduce AMT is to time your exercises for periods when the spread between your strike price and the fair market value is low. A smaller spread means less additional AMTI from your ISO exercise. For example, exercising 10,000 options with a $1 spread adds just $10,000 to your AMTI, compared to $150,000 if you wait until the spread widens to $15 [5]. This tactic is especially effective when your company’s 409A valuation is close to your grant price or during temporary drops in valuation. Keeping an eye on your company’s 409A valuations can help you identify these low-spread opportunities.

Exercising early in the year provides flexibility to adjust based on how your income and stock performance evolve. If the stock price drops or your AMT liability becomes higher than expected, you can opt for a disqualifying disposition - selling the shares before the year ends - to eliminate the AMT adjustment for that year. However, this means the spread will be taxed as ordinary income [2].

Here’s an example: Suppose you exercise 8,000 ISOs in January when the fair market value is $20, and your strike price is $5. This creates a $120,000 bargain element. By October or November, as your bonus and other income become clearer, you can decide whether to hold the shares for long-term capital gains treatment or sell part of your position to better manage your AMT exposure and portfolio risk. Some advisors even recommend splitting exercises between December and January to spread the AMT impact across two tax years while capitalizing on a single market view.

Carefully aligning your ISO exercises with your overall income picture can help you reduce AMT exposure while maintaining flexibility for liquidity and portfolio management. AMT is highly influenced by both your total income and the ISO bargain element in a given calendar year[3][8].

When it comes to timing ISO exercises, syncing them with periods of lower income can make a big difference in managing your AMT situation. Exercising more ISOs during years when your income is lower allows you to maximize your AMT buffer. Think about times when you might be between jobs, taking a sabbatical, working at an early-stage startup with lower cash compensation, or when your bonuses and RSU income are reduced[3][8][6]. In these scenarios, your regular tax liability tends to be lower, giving you more "room" under the AMT threshold.

The key threshold to watch for is the AMT crossover point, where your ISO bargain element causes your AMT to equal your regular tax. By exercising only up to this point each year, you can effectively avoid or minimize AMT altogether[3][6]. A tax advisor can calculate this annual AMT threshold for you, helping to create an "AMT budget" that guides how many ISOs you can safely exercise. This strategy not only reduces AMT risk but also preserves cash for future liquidity needs.

When you exercise ISOs and hold the shares, you might still owe AMT on the bargain element - even if you haven’t sold any stock[1][2]. If you don’t have enough cash to cover the AMT bill, a "sell-to-cover" approach can help. This involves selling just enough shares to pay the taxes and exercise costs while holding onto the rest for potential future gains[2][3].

Another option is an intentional disqualifying disposition in the same year as the exercise. Doing so avoids AMT completely because the ISO is treated as an NSO, and the bargain element is taxed as ordinary income rather than as an AMT preference item[1][3]. If you exercise ISOs early in the year and later find that the stock price has dropped or your projected AMT bill feels overwhelming, you can sell the shares before December 31 to reduce or eliminate AMT and convert your position back into cash[1][3]. This approach also helps manage single-stock risk, which is particularly important if your job and net worth are heavily tied to the same company[4][3].

If you end up paying AMT due to ISOs, you may qualify for a minimum tax credit (AMT credit) that can offset your regular tax in future years, provided your regular tax exceeds the tentative minimum tax in those years[1][2].

To recover AMT credits efficiently, consider selling shares with the largest original spread (the difference between the fair market value at exercise and the strike price) first. These lots likely generated the most AMT in previous years, so selling them can speed up your credit recovery[1]. Keep detailed records of each ISO exercise, including dates, share counts, strike prices, and fair market values, to ensure you can match sales to prior AMT payments effectively[1][2][3]. These strategies not only help you recover AMT credits but also set you up for smoother exit planning down the road.

When you're gearing up for an IPO, acquisition, or other liquidity events, your risk of triggering the Alternative Minimum Tax (AMT) can skyrocket [3]. If the fair market value (FMV) of your incentive stock options (ISOs) rises significantly above your strike price, the resulting "bargain element" becomes subject to AMT. Without proper preparation, you could face massive tax bills and cash flow issues. To avoid this, start planning 12–24 months before a potential exit. This gives you the runway to explore strategies like early exercise, 83(b) elections, and ISO exercise management to help keep your AMT exposure in check.

Some companies - especially startups - offer the option to exercise unvested ISOs early. This can be a smart move when the 409A valuation is still low, and the FMV is close to your strike price. By filing an 83(b) election within 30 days of exercising, you can lock in a minimal taxable spread, reducing your ordinary income and AMT liability. For example, if you exercise 10,000 ISOs at a $0.10 strike price when the FMV is $0.12, the taxable spread is just $200. Filing an 83(b) election ensures this small amount is taxed immediately, shifting future growth into the long-term capital gains category.

Timing is everything here. This strategy works best before major events like funding rounds or an S-1 filing, which can drive valuations higher. However, it comes with a downside: you might end up paying tax on a value that later declines.

Even with careful planning, balancing AMT reduction with your overall financial health is essential. One key consideration is avoiding over-concentration in your employer’s stock. Financial advisors often recommend keeping employer stock to no more than 20–30% of your total net worth. Gradually selling shares in stages can help reduce this risk.

If you need liquidity to cover AMT bills, a strategy to consider is an intentional disqualifying disposition - selling ISO shares before meeting the one-year and two-year holding periods. While this triggers ordinary income tax instead of the more favorable long-term capital gains rate, it provides the cash flow needed to manage your tax obligations.

Putting these strategies into action requires meticulous planning. Modeling different exit scenarios - such as IPO prices, exercise timing, and sales patterns - demands integrated cash-flow and tax projections. These projections should factor in grant details, vesting schedules, AMT calculations, and state tax implications. Specialized advisors can help pinpoint your AMT crossover point each year, guiding you on how many ISOs to exercise without incurring excessive AMT. In some cases, they may even recommend controlled AMT triggering to maximize future AMT credits.

For founders, aligning personal equity decisions with company-level financial strategies is crucial. Firms like Phoenix Strategy Group offer services that combine personal tax planning with company forecasting and M&A support. Their fractional CFO and FP&A services can help you time your option exercises, 83(b) elections, and secondary sales to match funding rounds or exit events, ensuring you preserve cash flow and maximize net proceeds.

As Lauren Nagel, CEO of SpokenLayer, shared, "PSG and David Metzler structured an extraordinary M&A deal during a very chaotic period in our business, and I couldn't be more pleased with our partnership" [9].

Starting early - ideally 12–24 months before a liquidity event - gives you the flexibility to explore various scenarios, avoid pitfalls like high-valuation exercises late in the year, and align your equity moves with your overall portfolio and cash flow strategy.

Smart timing and careful planning can significantly reduce the Alternative Minimum Tax (AMT) burden on stock options. By exercising early in the year, such as January or February, you give yourself the flexibility to monitor your stock's performance. If needed, you can sell before year-end to manage your AMT exposure. Strategies around timing, exercise sizing, and coordination can help you stay below the AMT threshold. And remember, AMT isn’t always a permanent tax: the credits generated can often be recovered in future years when your regular tax liability surpasses AMT. Keeping detailed records - organized by lot - is crucial for your CPA to correctly apply those credits using Form 8801.

For founders, integrating AMT planning with your broader exit and liquidity strategy is essential. Major events like an IPO, acquisition, or secondary sale naturally guide these decisions. Early exercise, particularly through an 83(b) election, can lock in a minimal taxable spread when your company’s 409A valuation is low, helping shift future growth into long-term capital gains. Coordinating exercises and staged sales 12–24 months before a liquidity event can ensure you have the cash to cover AMT, reduce over-concentration in employer stock, and align your equity moves with key milestones like funding rounds.

Effective planning ties together these strategies into a cohesive approach for managing AMT liability. A comprehensive plan should include cash-flow and tax modeling that factors in grant details, vesting schedules, AMT calculations, and state tax implications. Specialized advisors can help identify your AMT crossover point and model various exit scenarios, considering factors like IPO pricing, exercise timing, and sales strategies. For instance, Phoenix Strategy Group offers support in timing option exercises, 83(b) elections, and secondary sales to preserve cash flow while maximizing net proceeds during key events like funding rounds or exits.

As Lauren Nagel, CEO of SpokenLayer, shared, "PSG and David Metzler structured an extraordinary M&A deal during a very chaotic period in our business, and I couldn't be more pleased with our partnership."

To put these strategies into practice, start your ISO and AMT review within the next 30–60 days. Gather your option details, the current 409A (or FMV) valuation, and income projections. Create a simple one-page plan that outlines target exercises, potential AMT triggers, liquidity sources, and a method for tracking AMT credits. Treat this as an ongoing process rather than a one-time task, with a year-start decision on exercises, a mid-year check-in, and a year-end review. With early action, thoughtful planning, and the right support, you can minimize AMT while building lasting wealth from your equity compensation.

When exercising incentive stock options (ISOs), you can reduce your alternative minimum tax (AMT) liability by timing your exercises early in the year and spreading them out over several years. This strategy can help you stay under AMT thresholds and avoid a hefty, one-time tax burden.

It’s also worth looking into any tax deductions or credits that might apply to your situation. Working with a qualified tax advisor can help you create a plan tailored to your financial goals. Thoughtful preparation can lower your AMT exposure while allowing you to make the most of your stock options.

Filing an 83(b) election when you exercise incentive stock options (ISOs) early can come with some appealing tax advantages. For one, it lets you treat potential gains as capital gains rather than ordinary income, which often means a lower tax rate. Plus, it kicks off the clock for long-term capital gains tax treatment earlier, which could help reduce your tax liability if the stock’s value increases over time.

That said, there are some risks to weigh. Choosing the 83(b) election means you’ll owe taxes on the stock’s value at the time of exercise - even if the stock hasn’t vested yet or its value later drops. This upfront tax payment can be a strain, particularly if the stock doesn’t perform as expected. And remember, once you file the election, it’s irrevocable. That’s why it’s crucial to carefully evaluate your situation and consult a tax advisor before making this move.

If you’ve previously paid the Alternative Minimum Tax (AMT), you might qualify to use AMT credits to offset your regular tax liability in future years. The good news? These credits don’t expire - you can carry them forward indefinitely until they’re fully utilized. This can help reduce your overall tax bill whenever your regular tax exceeds your AMT liability.

This approach can be especially useful if your income varies from year to year or if you expect higher regular tax obligations down the road. To make the most of your AMT credits, it’s a smart idea to consult a tax professional who can tailor strategies to fit your specific financial situation.