Published on

February 26, 2026

Selling your business can lead to a tax bill that significantly reduces your proceeds. Without proper planning, taxes can cut your earnings by nearly half. Here's what you need to know:

Acting early and structuring your deal thoughtfully can help you retain more of your earnings and protect your financial legacy.

Selling your business can lead to a hefty tax bill. Between state and federal taxes, nearly half of your proceeds could be gone if you're not careful [4]. Understanding these tax liabilities is crucial if you want to keep more of what you've earned and plan effective tax-reduction strategies.

The structure of your sale plays a huge role in how much you'll owe. For instance, if you've owned your business for less than a year, you'll face short-term capital gains taxes, which are taxed at the same rates as ordinary income - anywhere from 10% to 37% [5]. Hold it for over a year, and you could qualify for long-term capital gains rates of 0%, 15%, or 20% [5]. But here's the catch: the IRS doesn’t see your business as one single asset. In an asset sale, things like inventory and accounts receivable are taxed as ordinary income, no matter how long you've owned them [4][6]. On the other hand, goodwill and equipment may qualify for lower long-term rates if you've held them for over a year.

How the deal is structured ultimately determines whether your gains are taxed as ordinary income or capital gains.

Your holding period directly affects how much tax you'll pay. If you've held an asset for 12 months or less, you'll pay short-term capital gains taxes at ordinary income rates, which can go as high as 37% federally [4][5]. Hold it for over a year, and you'll qualify for long-term capital gains rates, which cap at 20% [5]. On top of that, there's the 3.8% Net Investment Income Tax (NIIT), also known as the Medicare surtax [5].

Stock sales are often more tax-efficient for sellers because the entire transaction is treated as a single capital gain event [4][6]. In contrast, asset sales require both you and the buyer to allocate the purchase price across seven IRS asset categories using Form 8594 [4][5]. Sellers usually prefer allocating more to Class VII assets, like goodwill, since these qualify for long-term capital gains treatment [4][5]. As Gio Bartolotta, Partner at GoJo Accountants, points out:

Section 1202 QSBS income exclusion is a fantastic long term tax goal to have for founders of start up companies [4].

Not all payments tied to your sale qualify for capital gains treatment. Earnouts and consulting agreements, for example, are taxed as ordinary income. This means they’re taxed at your marginal rate, which could push you into a higher tax bracket [2]. Richard Brothers Financial Advisors explains:

Components of the sale, such as consulting agreements or payments for services, are taxed as ordinary income. This could push you into a higher tax bracket [2].

To manage this, you could structure payments as installment sales or use a Charitable Remainder Trust. These approaches can spread out your tax liability and potentially lower your overall rate while aligning with broader financial strategies [2].

But federal taxes aren’t the only thing to worry about - state and local taxes can add another layer of complexity.

Federal taxes are just the beginning. Many states tax capital gains as ordinary income, and the rates vary widely depending on where you live. Luckily, eight states - Wyoming, Nevada, Alaska, Texas, South Dakota, Florida, New Hampshire, and Tennessee - don’t tax capital gains at all [5]. But if you’re in a high-tax state, your combined federal and state tax burden could approach 50% [4].

Bradford Hall and Helen Wu from MGO CPA LLP caution:

effective tax rates that leave less than half of earnings in your control once you layer in state taxes [1].

Asset sales might also trigger additional state taxes, such as sales, use, real estate transfer, or franchise taxes [7]. Before finalizing the sale, it’s wise to obtain tax clearance certificates to ensure all state and local obligations are settled. Chris Vignone, Managing Director of Indirect Tax at Source Advisors, highlights:

Nexus and apportionment rules... might affect where and how much income is taxed, so it's important to understand them when formulating your exit strategy [7].

Navigating these tax challenges underscores the importance of structuring your deal thoughtfully to minimize your overall tax burden.

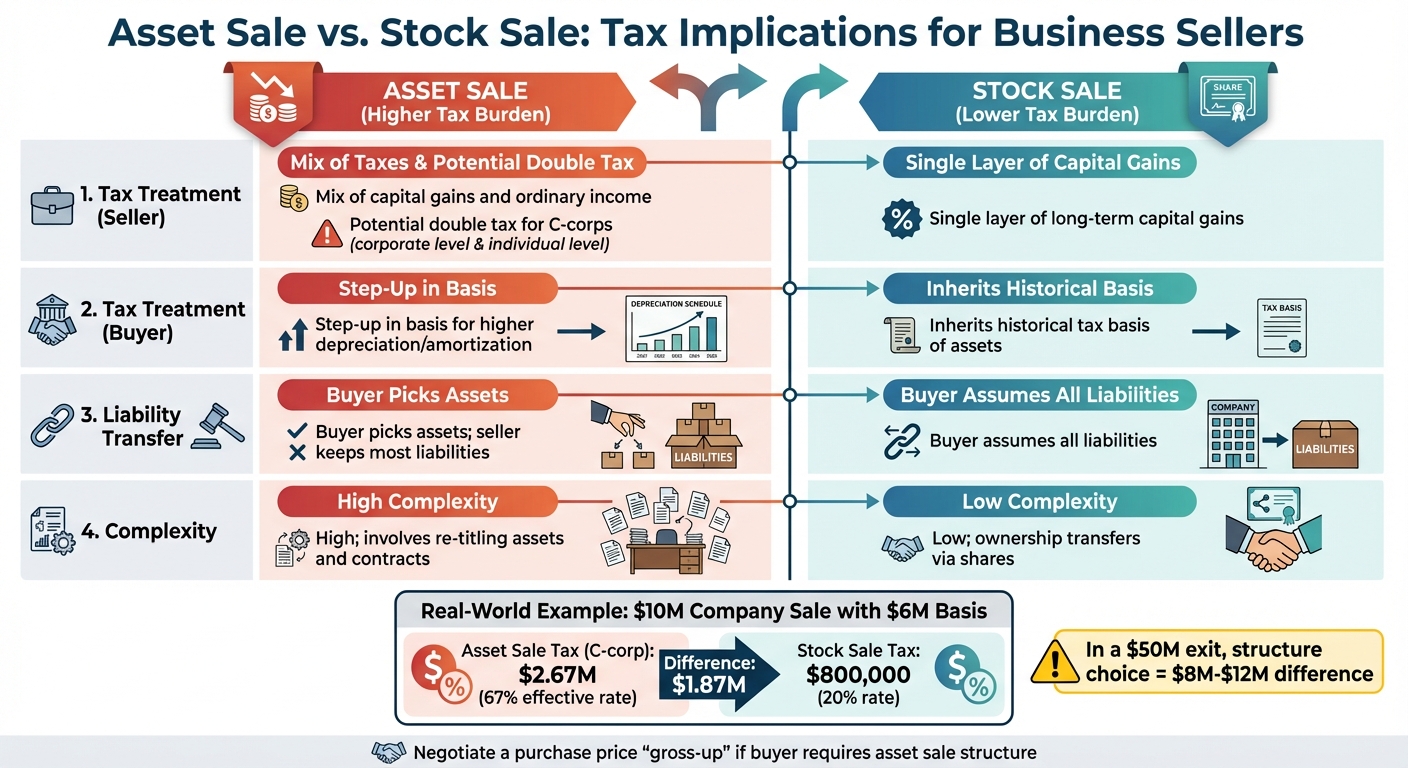

Asset Sale vs Stock Sale Tax Comparison for Business Exits

The way you set up your business sale can have a huge impact on how much you actually take home after taxes. For instance, in a $50 million exit, choosing between an asset sale and a stock sale could mean a difference of $8 million to $12 million in your pocket [8]. As Dan O'Connor from Excendio Advisors explains:

Structure is now a defining factor in shareholder value creation... The 'asset vs. stock' decision is about who captures value, who bears risk, and whether the exit delivers on shareholder expectations [8].

Making tax-efficient decisions during negotiations is key. Once the deal is finalized, your options shrink considerably. By understanding the tax mechanics of different sale structures, you can position yourself to retain more of your hard-earned money.

In a stock sale, the buyer purchases your entire legal entity, including shares, assets, and liabilities. This typically results in long-term capital gains for you, taxed at favorable rates of 0%, 15%, or 20%. For example, selling a $10 million company with a $6 million basis at the 20% rate would leave you with a $800,000 federal tax bill [9].

An asset sale, on the other hand, lets the buyer pick specific assets such as inventory, equipment, and goodwill. This allows them to "step up" the tax basis of those assets, increasing future depreciation deductions. However, for you, it means a mix of capital gains and ordinary income taxes, depending on how the price is allocated. If you're a C-corporation, this could mean double taxation - once at the corporate level and again at the shareholder level. For instance, a $4 million gain in an asset sale could result in a combined tax burden of $2.67 million, or an effective rate of 67%, compared to $800,000 in a stock sale [9].

| Factor | Asset Sale | Stock Sale |

|---|---|---|

| Tax Treatment (Seller) | Mix of capital gains and ordinary income; potential double tax for C-corps | Single layer of long-term capital gains |

| Tax Treatment (Buyer) | Step-up in basis for higher depreciation/amortization | Inherits historical tax basis of assets |

| Liability Transfer | Buyer picks assets; seller keeps most liabilities | Buyer assumes all liabilities |

| Complexity | High; involves re-titling assets and contracts | Low; ownership transfers via shares |

Buyers often prefer asset sales for the tax benefits, especially in tight credit markets. If they push for this structure, negotiate a purchase price "gross-up" to offset your additional tax costs. For example, in October 2025, Excendio Advisors handled the sale of a $50 million IT services company structured as a C-corp. Initially, the seller faced net proceeds of $30–$32 million due to double taxation and contract reassignment. After negotiations, the buyer agreed to a hybrid structure, grossing up the purchase price by $8 million to bring net proceeds to $40–$42 million [8]. Eric Welchko, President of Harney Capital, points out:

The choice [of deal structure] can generate or cost millions... it affects tax treatment, transfer of liabilities, and post-closing flexibility, and ultimately, how much value you take home [9].

An installment sale allows you to spread your tax liability across multiple years rather than paying it all at once. With this approach, you receive at least one payment after the tax year of the sale and only pay taxes on the portion of the gain received each year [10][11]. This strategy can keep you in lower tax brackets while giving you more time to invest the deferred tax capital.

To calculate, determine the gross profit percentage [(Selling Price – Adjusted Basis) / Selling Price] and apply it to each payment. For example, if your gross profit percentage is 60% and you receive a $1 million payment, $600,000 would be taxable gain for that year. While the interest portion of payments is always taxed as ordinary income, the principal portion qualifies for capital gains treatment.

Arron Bennett from Strategic CFO highlights the advantage:

The real cost of paying capital gains tax immediately isn't just the tax itself. It's the opportunity loss of permanently giving up investable capital [10].

However, there are some caveats. Depreciation recapture must be reported in the year of the sale, regardless of when payments are received, and interest is taxed as ordinary income [10][11]. If selling to a related party, ensure they don't resell the asset within two years, or the IRS could trigger immediate recognition of the deferred gain [10][11]. Additionally, if your total outstanding installment notes exceed $5 million, the IRS may impose an interest charge on your deferred tax liability under IRC Section 453A [10][11][12].

To implement this strategy, set up a formal installment note, create a clear payment schedule, and file IRS Form 6252 annually. Ensure the interest rate complies with the Applicable Federal Rate (AFR) to avoid imputed interest issues [10][11].

If your business is structured as a C-corporation, Section 1202 of the Internal Revenue Code offers a powerful tax break: up to $10 million - or $15 million under new rules - in capital gains can be excluded from federal taxes. This is a full exemption for eligible gains, making it one of the most attractive tax benefits available for founders.

To qualify, your company must meet these criteria:

You must also hold the stock for five years to claim the full exclusion. The One Big Beautiful Bill Act (OBBBA), passed in July 2025, introduced partial exclusions: 50% after three years and 75% after four years [13][16].

The OBBBA also raised the exclusion cap from $10 million to $15 million for shares issued after July 2025 and increased the asset threshold to $75 million [13][17]. This change makes the C-corp structure particularly appealing for high-growth startups compared to LLCs.

Abbie M.B. Everist, Principal at BDO's National Tax Office, explains:

The most effective QSBS outcomes tend to be a result of discipline rather than last-minute structuring [13].

If you're currently an LLC, consider converting to a C-corp early to start the QSBS holding period clock - though only value created after the conversion qualifies [16][17]. You can also "stack" exclusions by gifting QSBS to family members or multiple non-grantor trusts before a binding sale agreement is in place [15][17]. If you need to sell before the five-year period, you can defer gains by reinvesting proceeds into new QSBS within 60 days under Section 1045 [13][14].

Finally, remember that not all states follow federal QSBS rules. For instance, California, Pennsylvania, Alabama, and Mississippi don't recognize the exclusion, meaning you may still owe state capital gains taxes [13][16].

Once you've minimized exit taxes, the next step is designing a portfolio that maximizes after-tax returns. By addressing ongoing tax challenges, you can reduce tax drag and preserve wealth over the long term. A study by Vanguard highlights the impact of a tax-aware approach, showing a projected median after-tax return of 5.5%, compared to 5.0% for portfolios that overlook tax considerations [20]. Over time, that seemingly small difference can grow into hundreds of thousands of dollars.

Brad Koval, Director of Financial Solutions at Fidelity Investments, sums it up well:

You can't control market returns, and you can't control tax law, but you can control how you use accounts that offer tax advantages - and good decisions about their use can add significantly to your bottom line. [18]

The key is aligning investment income types with the right account types to minimize tax exposure.

Different investments come with varying tax implications, so choosing the right vehicles can significantly cut annual costs. For instance:

Beyond selecting tax-efficient investments, where you hold them matters just as much.

Asset location involves placing specific investments in taxable, tax-deferred, or tax-exempt accounts to maximize their tax treatment benefits [21][24]. This strategy can add an estimated 0.05% to 0.30% to annual portfolio returns, with some analyses suggesting gains as high as 0.75% per year [25][26]. Over 30 years, this could mean saving $74,000 in taxes on a $1 million portfolio [26].

The basic principle is to align the tax characteristics of investments with the tax treatment of accounts:

Matt Bullard, Regional Vice President at Fidelity Investments, offers a helpful analogy:

I like to compare asset location to using building blocks to build a tower. If the same set of blocks is arranged in a more efficient way, you can often build the tower higher. [21]

There are exceptions to these guidelines. For example, international stock funds should be held in taxable accounts to claim foreign tax credits for taxes paid to other governments - a benefit lost if held in an IRA [19][25]. Similarly, placing municipal bonds in tax-advantaged accounts wastes their inherent tax-exempt status [22][25].

Proper asset location lays the foundation for further tax optimization through active management.

To complement asset selection and placement, adopt strategies like tax-loss harvesting and disciplined rebalancing.

Tax-loss harvesting involves selling investments at a loss to offset capital gains or up to $3,000 of ordinary income annually. Excess losses can be carried forward indefinitely [29][30][33]. For high-income investors facing a top federal rate of 23.8% on long-term capital gains, this approach can boost annual returns by 0.78% to 1.38%, depending on their tax burden [29].

To avoid the "wash sale" rule, which disallows tax deductions if you repurchase the same or similar security within 30 days, consider replacing a sold ETF with one that tracks a different index [29][30]. Automated tax-loss harvesting services can be especially effective, with a median tax benefit-to-fee ratio of 5.5x, and more than 95% of clients receiving more in tax benefits than they pay in fees [29].

Portfolio rebalancing ensures your asset allocation stays on track while managing tax exposure. Instead of rebalancing on a fixed schedule, use "rebalancing bands" to trigger trades when allocations deviate by an absolute 5% for major asset classes or ±25% for sub-asset classes [31]. Before selling appreciated assets to rebalance, try using new cash inflows, dividends, or even gifting appreciated shares to charity [31].

Justin Reed, Partner and Chief Investment Officer at Brown Brothers Harriman, explains:

We think about rebalancing as primarily an exercise in risk control – that is, one that keeps a portfolio's characteristics in line with a carefully developed target asset allocation. [31]

To maintain the benefits of tax-loss harvesting as your portfolio grows, consider contributing 10% to 15% of your account's value in cash annually. This creates new tax lots with a higher basis [32]. Reinvesting the immediate tax savings from harvesting back into your portfolio can further amplify the advantages over time [29].

Planning for wealth transfer is a critical step in ensuring your legacy remains intact after your financial exit. Once you’ve optimized your portfolio for tax efficiency, the next task is to minimize the taxes that can chip away at your wealth during transfers. Starting in 2026, the federal lifetime estate and gift tax exemption will be $15 million per individual - or $30 million for married couples. Any amount exceeding these thresholds may be subject to a hefty 40% federal estate tax rate [38].

Selecting the right trust depends on your goals, timeline, and liquidity needs.

When appreciated securities are donated to a CRT, they can be sold and reinvested into a more efficient diversified investment portfolio... undiminished by any income taxes. [34]

These trust options can be paired with gifting and charitable strategies to further reduce your taxable estate.

The 2026 exemption increase allows for an additional $1,010,000 in gifting capacity per individual compared to 2025 [38]. If you’ve already maximized your exemption, this is an opportunity to transfer more appreciated assets out of your estate. Additionally, the annual gift tax exclusion - $19,000 per recipient ($38,000 for married couples) - offers a way to gradually reduce your taxable estate without using any of your lifetime exemption [38].

Russell P. Love of Nelson Mullins points out:

For many clients, federal estate tax is no longer the primary concern regarding planning. Rather, we are observing increased focus on control, asset protection, liquidity, and family governance. [38]

Keep in mind that portability of the estate tax exemption isn’t automatic. Executors must file a federal estate tax return and elect portability [37].

You can also make unlimited tax-free gifts for educational or medical expenses by paying providers directly - these payments won’t count against your annual or lifetime limits [39]. For 529 plans, the "super-funding" rule allows contributions of up to $95,000 (five years’ worth of annual gifts) at once, accelerating the reduction of your taxable estate [40].

Charitable giving complements trust and gifting strategies by offering additional tax benefits. Donating appreciated assets to charity helps you avoid capital gains taxes while providing an income tax deduction [41][34].

The One Big Beautiful Bill Act introduced a new above-the-line charitable deduction - $1,000 for single filers and $2,000 for married couples who take the standard deduction [41]. For those over 70½, Qualified Charitable Distributions (QCDs) from IRAs (up to $108,000 for 2025) can satisfy required minimum distributions while keeping those amounts out of taxable income [34].

Some high-net-worth individuals are also “bunching” their charitable contributions into a single year to surpass the standard deduction threshold, maximizing their itemized deductions [41]. This approach can reduce both income and estate taxes while supporting causes you care about.

For tailored advice on incorporating these strategies into your overall financial plan, consult the experts at Phoenix Strategy Group (https://phoenixstrategy.group).

Navigating post-exit taxes requires careful, layered planning well before signing any sale agreements. As Bradford Hall and Helen Wu point out:

Taxes have become more than just a line item in your budget - they're a force that can quietly erode your returns, complicate your business exit, and reshape your legacy [1].

A thoughtfully structured exit can minimize your tax liabilities, ensuring you retain a larger portion of your sale proceeds.

Strategies like optimizing the sale structure, utilizing Section 1202 exclusions, and employing tax-efficient investments and trusts work together to protect your wealth during multiple tax events. As RSM Global emphasizes:

implementing an exit plan well in advance of a transaction leads to much better outcomes than attempting to undertake concurrent with a sale [3].

Starting your planning 18–24 months ahead of a potential exit offers the time and flexibility needed to refine your entity structure and achieve the most favorable after-tax results [1].

After the exit, managing diverse income streams - such as capital gains, earnout payments, investment returns, and trust distributions - requires a coordinated approach. Each of these streams comes with distinct tax implications, and mismanagement can lead to higher tax brackets, trigger the 3.8% Net Investment Income Tax, or result in missed exclusions and deferrals. Proactive planning ensures you can preserve wealth while maintaining financial flexibility.

Expert guidance is crucial when tackling these challenges. The financial professionals at Phoenix Strategy Group specialize in helping business owners navigate exits and handle the intricate tax and financial planning that follows. Their comprehensive approach combines M&A advisory, financial planning, and strategic decision-making to structure your post-exit portfolio in a way that protects your wealth, sustains income, and supports both future endeavors and family priorities. This unified strategy simplifies the process and strengthens your financial legacy for the long term.

If you own stock in a U.S. C corporation, you might meet the criteria for QSBS (Qualified Small Business Stock) under certain conditions. These include holding the stock for at least five years, ensuring the company's gross assets were below $50 million when the stock was issued, and acquiring the stock through eligible methods, such as a purchase or in exchange for services. It's always a good idea to consult a tax professional to confirm how these rules apply to your unique circumstances.

When it comes to reducing taxes in an asset sale, a few strategies can make a big difference. For instance, structuring the deal to take advantage of lower long-term capital gains tax rates can lead to significant savings. Another option is using installment sales to spread the tax liability over several years, making the payments more manageable. If the assets qualify as Qualified Small Business Stock (QSBS), you might even benefit from certain exclusions.

The key to optimizing your tax outcome is careful planning. It's always a good idea to consult with a financial advisor or tax professional to ensure you're making the most of these opportunities while staying compliant with tax laws.

To make your post-exit portfolio more tax-efficient, focus on three key areas: asset types, entity structures, and timing of sales. Consider strategies such as using tax-advantaged accounts, taking advantage of Qualified Small Business Stock (QSBS) benefits, and structuring installment sales. Ideally, start planning 18–24 months before your exit. This gives you time to restructure assets and set up strategies that maximize tax benefits. A carefully planned portfolio weaves together timing, smart entity choices, and tax-efficient investments to help protect your wealth from excessive tax burdens.