Published on

June 30, 2026

A 1031 exchange can keep a large tax bill out of your sale today, but it can also lower future depreciation and tighten after-tax cash flow.

If I strip this down to the part that matters most, here’s the answer: a 1031 exchange works best when the extra reinvested equity beats the cost of lower basis, lower depreciation, fees, debt terms, and strict IRS deadlines. On a $3,000,000 sale with a projected tax hit of about $762,000, deferral can leave much more money in the next deal. But that tax is only delayed, not gone.

Before I move ahead with any exchange, I’d focus on these points:

A simple way to look at it: if the next property still works after I factor in tax drag, debt service, lower depreciation, and closing costs, the exchange may be worth it. If not, paying some tax now may leave me with better options.

A 1031 exchange comes down to four key terms.

Realized gain is your total profit on the sale: the net sale price minus your adjusted tax basis. Recognized gain is the part you actually pay tax on in the year of the exchange. If you receive no boot, recognized gain is zero, and the full realized gain is deferred. Deferred gain is the remaining piece - the amount pushed into the replacement property.

Boot is where taxes show up. It can be cash you keep out of the exchange or debt relief that is not matched by new debt [3][5]. In either case, boot creates recognized gain, up to the full amount of the boot received.

There’s one rule here that trips people up: you can offset mortgage boot by putting more cash into the deal, but you cannot offset cash boot by taking on more debt [3]. That matters because any recognized gain cuts into the money you have left to reinvest. And the deferred gain doesn’t just sit in the background. It changes the replacement property’s basis and affects future depreciation.

After gain is split into realized, recognized, and deferred, basis becomes the next big issue. This is where many investors get caught off guard. The replacement property’s basis equals the purchase price minus deferred gain, so depreciation is lower than it would be in a taxable purchase [3].

The depreciable basis is split into two parts:

That split usually means lower annual depreciation. Lower depreciation can mean more taxable income and more tax drag over time. Put simply, after-tax cash flow can get squeezed.

The deferred gain also does not vanish. It stays with the property as embedded tax liability. It should be treated as a real future bill, not brushed aside. Those basis shifts shape both annual cash flow and how much equity you can roll into the next deal.

When deferred tax stays in the deal, more of your sale proceeds can move into the next property. That means a 1031 exchange can leave a large share of equity available for reinvestment instead of sending it out the door in taxes.

In plain English: more cash can stay in play for the next acquisition, reserves, or a down payment. That can make the replacement purchase stronger without adding more leverage. The tradeoff is pretty direct, though. You may have more equity now, but less depreciation later.

More equity helps, but it’s not the whole story. To get full deferral, you generally need to replace the debt from the relinquished property with equal or greater debt, or add enough cash to make up the gap. In a high-rate market, that can push borrowing costs up and cut cash-on-cash returns [3][8].

There is another path. An investor can avoid unreplaced debt by putting in outside cash instead of taking on new financing at a higher rate [5]. That can help monthly cash flow because leverage stays lower. The catch is simple: you need more cash up front [5].

A 1031 exchange isn’t just a tax move. It’s a capital allocation choice. It keeps equity in motion, but it also changes basis and usually reduces depreciation deductions because the replacement property carries over the deferred gain [3][4].

That matters for underwriting. If depreciation drops, after-tax cash flow can look different than the sale proceeds alone might suggest. So the smart move is to model after-tax cash flow, not just the amount you can roll into the next deal.

Those gains only hold if the exchange also meets the timing and identification rules.

1031 Exchange vs. Taxable Sale: Key Differences at a Glance

That reinvestment benefit only works if the exchange is timed the right way, documented the right way, and modeled with all the costs in the deal.

The IRS sets two deadlines, and both start the moment the relinquished property closes. You have 45 calendar days to identify replacement properties in writing to your Qualified Intermediary (QI), and the exchange must be completed within 180 calendar days of the initial sale, or your tax return due date with extensions, whichever comes first [1][10][7]. Those two clocks run at the same time. So once the 45-day window ends, you have about 135 days left to close [1][10].

Miss either deadline, or break the QI rules, and the IRS treats the deal as a failed exchange. When that happens, the deferral is gone, and the whole reinvestment case falls apart.

The QI is not optional. All sale proceeds must stay in a segregated account controlled by the QI. If you receive the money or have control over it, the exchange fails [1][9]. Your attorney, CPA, or broker also cannot act as the QI if that person served as your agent during the last two years [7][9].

Fourth-quarter sales can create an extra problem. Your tax return due date may arrive before the 180-day period ends. Filing a tax return extension with Form 4868 or 7004 preserves the full 180 days [7][2]. Skip that step, and the exchange window gets cut short.

Costs matter because they shrink the cash you can carry into the next deal.

Standard QI fees, legal and advisory fees, broker commissions, and title and escrow charges all come out of the proceeds before anything is left for reinvestment. Some exchange costs count as qualified expenses. Others reduce net proceeds but do not reduce boot [3][7]. That distinction matters more than people think. Get it wrong, and you can either pay too much tax or overstate how much equity is available for the replacement property.

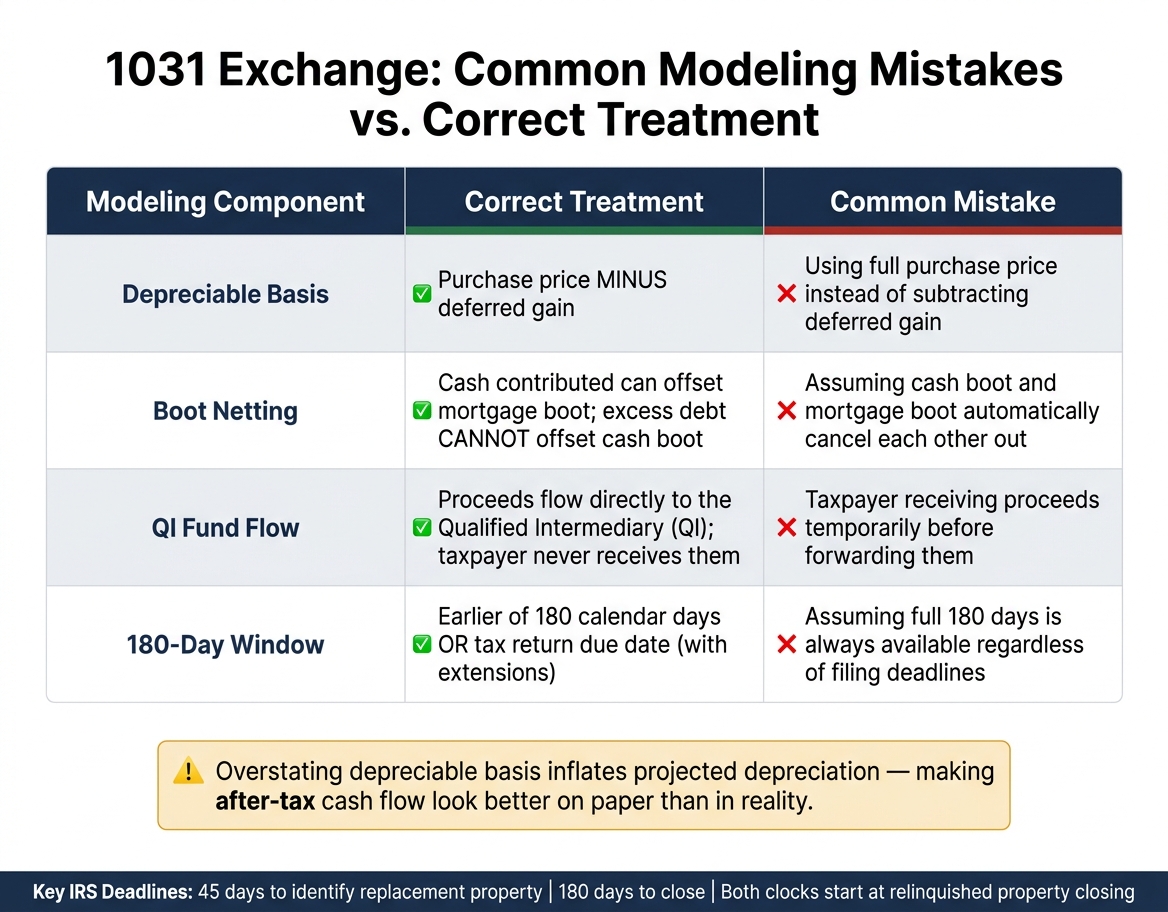

The biggest mistakes usually are not about tax law. They show up in the model.

A lot of spreadsheets make the deal look better than it is by overstating usable equity, basis, or timing flexibility. Here’s where that tends to happen:

| Modeling Component | Correct Treatment | Common Mistake |

|---|---|---|

| Depreciable Basis | Purchase price minus deferred gain [3] | Using full purchase price instead of purchase price minus deferred gain |

| Boot Netting | Cash contributed can offset mortgage boot; excess debt cannot offset cash boot [3][10] | Assuming cash boot and mortgage boot automatically cancel each other out |

| QI Fund Flow | Proceeds flow directly to the QI; the taxpayer never receives them [1][9] | Taxpayer receiving proceeds "temporarily" before forwarding them |

| 180-Day Window | The earlier of 180 calendar days or the tax return due date, including extensions [7][10] | Assuming the full 180 days is always available regardless of filing deadlines |

Overstating depreciable basis makes projected depreciation deductions look higher than they will be in practice. And that can make after-tax cash flow look better on paper than it will in the actual deal. The next step is to test whether the after-tax return still holds up once timing, fees, and basis are all built into the numbers.

Once you model timing, debt, fees, and basis, the issue gets pretty simple: does the deferral improve after-tax cash flow or not? A 1031 exchange tends to make the most sense when you have a large built-in gain, a solid replacement property lined up, and a full after-tax model in front of you. In that setup, more of your equity stays in the deal instead of going out the door in taxes. But the tax bill doesn’t disappear. It’s delayed, and that deferred gain stays attached to the property as a tax liability for the next sale [3].

There’s a tradeoff, though. A lower basis usually means less depreciation. Because the deferred gain carries into the replacement property, the depreciable basis is lower. That cuts annual deductions and can put pressure on after-tax cash flow over time [3].

Debt, fees, and timing can chip away at the upside too. Higher borrowing costs matter. So do the 45-day identification window and the 180-day closing deadline, which don’t give you much room to miss a step [3]. If the only replacement option is weak or overpriced, it may make more sense to pay tax on part of the gain instead of forcing a bad deal [3].

Before moving ahead, compare a taxable sale and a 1031 exchange on an after-tax basis. Look at net proceeds, replacement debt service, carryover basis, excess basis, and exchange fees. Then pressure-test the replacement property’s cash flow using financing terms that reflect the market as it is, not as you hope it will be.

The main test is straightforward: if the replacement property still makes sense after taxes, deferral can help keep more capital working for you. If it doesn’t, taking part of the gain now may leave you with more flexibility later.

A 1031 exchange can make sense if your goal is long-term wealth building through tax deferral. The big upside is simple: more of your money stays invested, which can give you more buying power for your next property.

That said, the tax bill doesn’t disappear. It’s delayed. And that changes the math.

You also need to factor in a lower carryover basis, less depreciation going forward, exchange fees, and strict IRS timing rules. You must identify the replacement property within 45 days and close within 180 days.

In a 1031 exchange, a lower basis can trim near-term cash flow because it cuts your yearly depreciation deductions. The basis carries over from the relinquished property instead of resetting to the new purchase price, so your tax shelter is smaller.

That can mean a higher tax bill each year and less after-tax cash flow. It’s the trade-off for deferring capital gains taxes, so make sure you build those lower deductions into your investment model.

Common mistakes can blow up a 1031 exchange fast.

Miss the 45-day identification deadline or the 180-day closing deadline, and the exchange can fail. The same goes for taking constructive receipt of the sale proceeds instead of using a Qualified Intermediary. If the money touches your hands, even for a moment, that’s a problem.

Other slipups include receiving cash boot or not replacing debt. Both can trigger taxable gain, even if the rest of the exchange looks fine on paper.

Changing ownership or title too close to closing can also invalidate the exchange. This is one of those details that seems small until it isn’t.

And there’s a bigger planning issue here: a 1031 exchange defers tax, but it does not erase it. If you don’t think ahead, you can end up carrying a large embedded tax liability for years.