Published on

June 30, 2026

Clean energy companies don’t usually stall because the tech fails. They stall because the business is not ready for bankable scale.

If I had to sum up the article in plain English, it’s this: growth-stage VC fills the gap between a working pilot and a financeable commercial business. That gap is large - about $100 billion to $200 billion - and it exists because scaling energy companies takes more time, more money, and more deal work than many VC-backed businesses.

Here’s what matters most:

What changes at this stage is simple: the question is no longer “Does it work?” It becomes “Can this company turn a working product into financeable projects and repeat sales?”

If you’re reading this as a founder, the short checklist is clear:

That’s the core of the article: growth-stage VC is less about invention and more about getting a clean energy business ready for scale capital.

Once a company gets past pilot validation, the funding conversation changes. It’s no longer just about getting capital in the door. Now the focus is on round size, the mix of investors, and how the capital stack comes together.

Growth-stage rounds often range from $2 million to $100 million [1]. In many cases, those rounds close in tranches tied to milestones like deployment, permitting, or revenue. That’s common in clean energy, where money tends to follow execution instead of arriving all at once.

At this stage, companies usually put capital toward manufacturing readiness, deployment, working capital, engineering, procurement, and construction (EPC) partners, and regulatory execution [6][7]. A simple way to think about the capital stack is this: use debt for hard assets like equipment, inventory, and infrastructure, and keep equity for moves that shape the business, such as entering a new market or building out the team [3].

That setup has a direct effect on who can lead the round.

A few different investor groups show up in growth-stage clean energy rounds, and each one is pricing a different kind of risk.

Lead investors are usually growth equity or late-stage VC funds. They want to see commercial traction, often $10 million to $20 million in revenue, a diversified customer base, and 20%+ annualized growth. They also bring infrastructure-style diligence into venture deals, looking closely at unit economics, offtake agreements, and EPC partners [2].

Specialist climate VC funds tend to focus on TRL 5–7 companies that are still trying to cross the valley of death. They look for a technical edge and a clear place in the broader energy system. Strategic corporate investors can add market signal and access to deep balance sheets. In many cases, they invest to secure future offtake or manufacturing partnerships. Existing insiders often join as follow-on investors, but they can run into check size limits. So even when insiders stay involved, a larger growth round usually still needs a new lead investor [2].

The strongest rounds often combine these groups well:

For founders with $500,000 to $10 million in annual revenue, the bar is usually higher before they go after larger checks. Investors will want to see a path to bankability, signed offtake agreements or letters of intent with creditworthy counterparties, and audited financials [1][2].

Those are the pieces investors use to judge revenue proof and project risk.

Growth-stage investors aren’t betting on promise anymore. They’re looking for repeatable revenue and a company that looks ready for larger pools of capital. In practice, they’re checking three things: whether revenue is real, whether the project can be financed, and whether reporting is clean.

A paid pilot is a good start. But for most investors, that alone isn’t enough. They want to see contracted revenue that can repeat, along with margins that are moving in the right direction.

Contract quality matters more than raw volume. 83% of investors are willing to consider fully contracted projects, compared to only 25% for partially contracted ones [10]. That gap says a lot. A fully contracted project with a creditworthy counterparty is one of the clearest signals that a project can hold up under lender and investor review.

Modular design helps here too. If pilot data from one module can be carried into a multi-unit commercial facility, the leap from pilot to scale is much easier to defend during diligence [8]. It gives investors a cleaner story: the company isn’t starting from scratch each time it grows.

Still, revenue proof doesn’t erase execution risk. It just gives investors one less reason to hesitate.

At this stage, investors are pricing five buckets of risk:

The pattern is simple: each risk that comes off the table moves the company closer to project debt or larger growth equity.

Construction risk is often handled through fixed-price, full-wrap EPC contracts [9]. Technology risk is reduced through manufacturer warranties and independent engineer reports. Offtaker risk falls when long-term agreements are signed with creditworthy counterparties. Regulatory risk drops as permits are secured and interconnection agreements are executed.

Fervo Energy's Cape Station financing is a good example of how this tends to unfold: operating data, strategic capital, permits, grid access, and independent validation all came before non-recourse debt [4].

That sequence matters. Investors want to know the company can move from a good technical case to something the market can actually finance.

Once contracts look solid and the risk picture is more controlled, attention shifts to reporting discipline. Investors want a business that is easy to diligence, not one that creates extra work.

They’re usually looking for a short set of numbers and materials:

This is the stuff that signals a company is transaction-ready, not scrambling at the last minute. Clean reporting doesn’t just make the business look organized. It helps investors move with more speed and less friction.

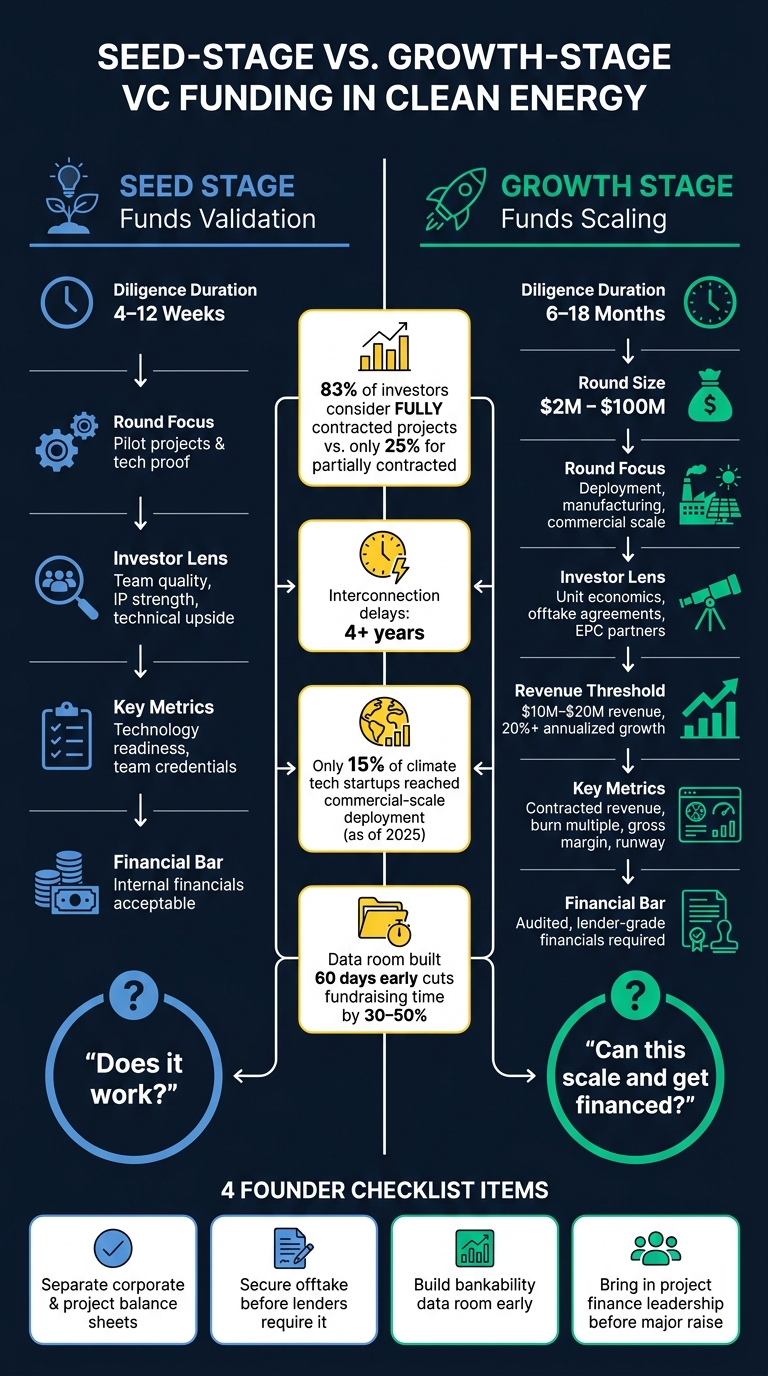

Seed-Stage vs. Growth-Stage VC Funding in Clean Energy

The biggest change in clean energy funding isn’t just a bigger check. It’s a shift in purpose.

Seed capital is there to prove the tech works. Growth capital is there to help the company deploy that tech again and again at commercial scale.

In clean energy, that difference shows up fast. Seed rounds usually pay for validation work and pilot projects. Growth rounds pay for deployment and scale. At the seed stage, investors lean hard on the team and the promise of the technology. At the growth stage, they want proof the business can operate at scale, make money on each unit, produce audited financials, and stand up to lender scrutiny.

Once a company starts moving toward scale, the investor lens changes. The story is no longer mostly about technical promise. It’s about operating proof.

That’s why diligence gets much heavier at the growth stage. A seed investor may spend 4 to 12 weeks looking at the team, the product, and the core thesis. A growth-stage investor may run a process that lasts 6 to 18 months [1].

The scope changes too. Seed rounds tend to focus on team quality, IP strength, and technical upside. Growth rounds go much deeper into the nuts and bolts of the business, including unit economics, manufacturing yield rates, and whether a third-party operator could run the plant if the sponsor fails [5][12]. As Katharine Hawthorne notes, growth investors back businesses with proven recurring revenue and limited technology risk [6].

By this stage, lender-grade financials matter. Founders need to start building a bankability data room long before they’re out raising the next round. That means tracking and organizing reliability metrics, degradation curves, and performance data from Series A onward, so growth-stage and debt investors can review a long-term operating record [1][7].

The governance bar rises as well. Growth investors want to see systems that go beyond founder-led execution in every part of the company. LanzaJet, for example, used EPC partners to close the execution gap while scaling its sustainable aviation fuel refinery [8]. That kind of operational de-risking is often what separates a technically promising company from one that can attract scale capital.

The clean energy funding gap is a bankability problem, not a technology problem. Too many companies get past the pilot stage, then hit a wall when it’s time to bring in scale capital.

That’s where growth-stage VC comes in. It funds the move from proof to bankable execution - the stage where debt can start replacing expensive equity. At this point, investors aren’t just betting on the idea. They’re judging whether the company can execute at scale. They want to see contracted revenue, proven unit economics, and financial reporting that can hold up under 6- to 18-month diligence [1]. And that kind of raise can’t be treated like a fire drill. Growth-stage capital needs to be mapped out years in advance.

The companies that become financeable tend to get four things right:

Bankability is the inflection point. It’s when debt starts to open up on much cheaper terms than equity. But getting there takes more than a strong product. It takes operational discipline, solid financial infrastructure, and clear milestones that show the business is ready.

For founders, that work starts long before the next round. Phoenix Strategy Group helps growth-stage clean energy companies put the right financial infrastructure in place - fractional CFO support, FP&A, and data systems - so they’re prepared for scale capital.

A clean energy company should raise growth-stage VC once it has moved past basic tech validation and can show repeatable, scalable, and economically defensible commercial execution.

At that point, the company needs more than a working product. It should be able to point to field-proven performance, clear market demand, a standard delivery process, steady customer acquisition, signed offtake agreements, and a believable path to profitability.

A clean energy project becomes bankable when it stops looking like a bet and starts looking like infrastructure. That shift matters because investors want proof that both technical and commercial risks are under control.

What do they look for? A few things tend to matter most:

At its core, bankability is about predictability. The more a project can show steady performance and fewer surprises, the easier it is for lenders and investors to get comfortable.

Founders need to stop selling pure upside and start showing predictable execution. That means proving the business can run well, manage operations, and generate cash flow in a way investors can track.

A strong data room should include:

In clean energy, the bar is often higher. Investors want proof that the tech works reliably, not just in theory. Show standardized procedures, performance data, and verified supply chains. That kind of proof helps turn a big promise into something investors can trust.

Your story should also match the time horizon investors are thinking about. Tie the company’s direction to long-term growth and show a clear path to profitability or exit.