Published on

February 17, 2026

Balancing cash flow across multiple business units is critical for maintaining liquidity, especially when dealing with varied revenue cycles, expenses, and capital needs. Even profitable businesses can face cash shortages without proper oversight. Here's how to manage it effectively:

Key Takeaway: Managing cash flow across units requires centralized forecasting, standardized processes, strategic resource allocation, and efficient operations. Regular monitoring and real-time insights are essential to avoid liquidity issues and support growth.

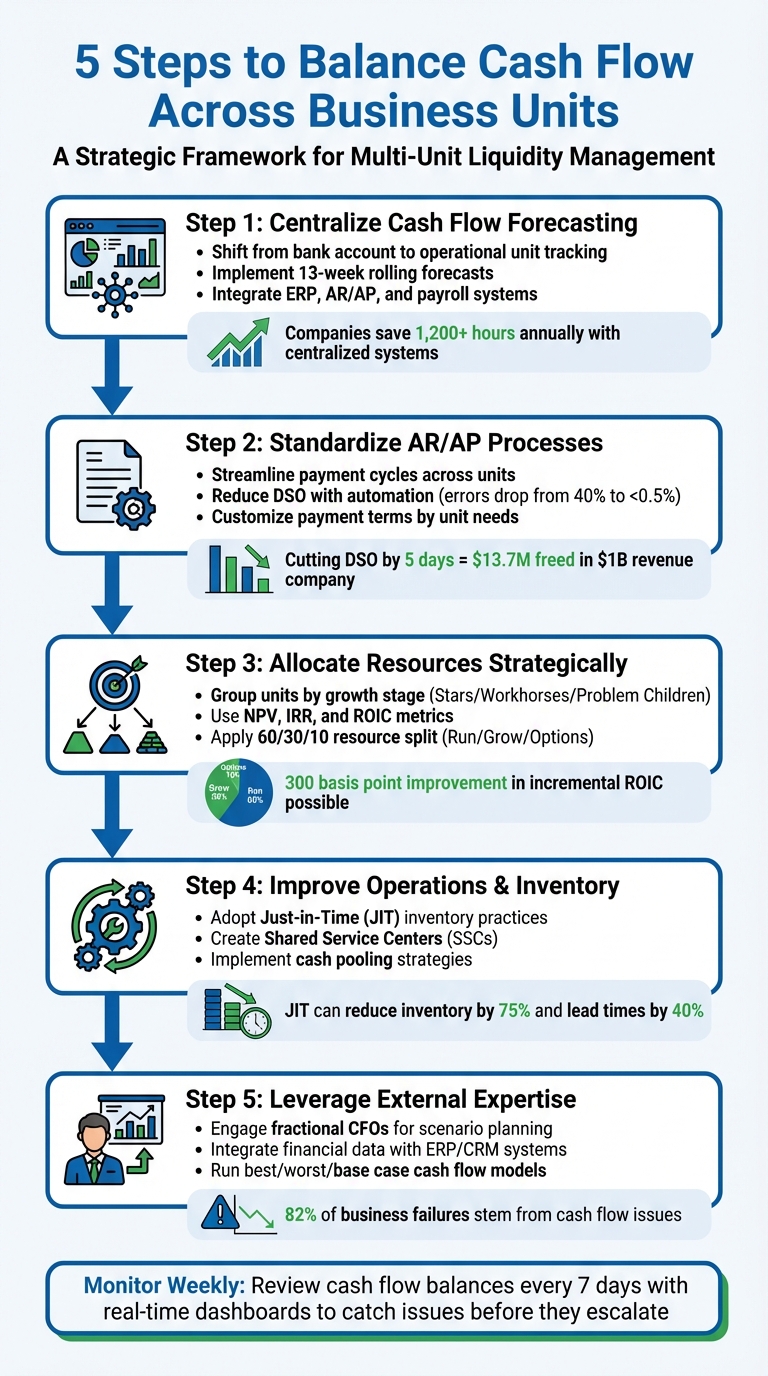

5-Step Framework for Balancing Cash Flow Across Business Units

One of the most common mistakes multi-unit businesses make is tracking cash flow by bank account instead of by operational unit. When you focus your forecasting on divisions, product lines, or regions, you can clearly see which areas are generating cash and which are draining it. This shift from a banking-focused view to an operational perspective helps identify problems early, before they turn into bigger financial challenges [3].

Take the example of Hennecke Group, a $180 million manufacturing company that struggled with manual cash flow consolidation. Their team of four employees spent an entire day every week gathering cash flow data from five sites and multiple ERP systems. In 2025, their CFO, Yves Souguenet, introduced a centralized forecasting system that moved cash updates from weekly to daily. This change reduced their manual workload from 32 hours a week to just 2 hours, saving over 1,200 hours annually while providing real-time visibility into liquidity [4].

"We've saved over 1,200 hours annually, minimized errors, and have real-time information at our fingertips - enabling us to focus on strategic decisions, not spreadsheet maintenance."

- Yves Souguenet, Group CFO, Hennecke Group [4]

This example highlights the importance of structuring cash forecasts around operational units. Many mid-market companies still struggle with unreliable forecasting - about 43% rely on forecasts that cost them an average of $465,000 annually due to unexpected cash deficits exceeding $50,000 every 20 days [4]. Centralizing your forecasting brings all your data into one place, integrating inputs from ERPs, accounting tools, and banking platforms. This creates a clearer picture of your finances and enables more proactive management.

A 13-week rolling forecast is widely recognized as a reliable approach for balancing short-term liquidity needs with medium-term planning [4]. This timeframe gives you enough visibility to spot potential working capital issues while staying closely aligned with actual cash transactions. Unlike long-term budgets that often rely on estimates, a 13-week rolling forecast tracks actual cash movements, including supplier invoices, customer payments, and debt schedules [4][5].

For daily liquidity control (3–15 days), use data from bank accounts, accounts payable, accounts receivable, and payroll. For the 4–13-week period, pull details from your ERP system, invoices, DSO metrics, and purchase orders to monitor working capital and manage risks [4].

Daily reconciliation is critical. By matching expected cash movements with actual bank activity at both the entity and group levels, you can keep your forecast accurate and dynamic. For instance, if one retail division shows high inventory turnover but a B2B unit struggles with extended DSO, you'll catch the problem quickly [3].

Consistency is also key. Establish a standardized chart of cash inflow and outflow categories - such as payroll, taxes, debt service, and customer collections - so that data from all units can be consolidated easily and compared accurately [4]. This consistency lays the groundwork for automation and advanced forecasting tools.

Manual data entry is prone to errors, with rates as high as 20%, and studies show that 94% of spreadsheets contain mistakes [6]. Modern FP&A systems eliminate these issues by automating data consolidation and reducing fragmentation. Start by linking your primary data sources - bank balances, ERP accounts, and payroll calendars - to create a reliable foundation [7].

Many FP&A systems now use AI to process data, categorize cash flows, and predict payment timelines based on historical trends. This automation frees up your team to focus on strategy instead of spreadsheet maintenance. Companies with accurate cash forecasting are 76% more likely to avoid cash shortages and 64% better at identifying investment opportunities [6].

If a full ERP suite isn't in your budget, platforms like Power BI, Tableau, or Azure SQL can bridge the gap between manual spreadsheets and fully automated systems. However, it's important to establish what Deloitte calls "foundational governance" to prevent forecasting from becoming overly time-consuming or unsustainable [7]. By integrating payroll systems, CRM data, and AR/AP aging reports, you can ensure your forecast reflects upcoming financial obligations.

Real-time bank feeds are another essential tool for daily cash management. They allow you to reconcile expected versus actual cash movements quickly and adapt to region-specific challenges, such as regulatory changes in Europe or extended payment terms in Asia [7]. This level of detail is particularly important for companies in growth phases, where understanding which divisions can support debt payments or new investments is critical [3].

For growing businesses looking to scale or secure funding, working with experienced financial advisors - like those at Phoenix Strategy Group - can help you implement advanced FP&A systems tailored to your needs. This ensures your cash flow forecasting is both efficient and responsive to your company's growth trajectory.

When accounts receivable (AR) and accounts payable (AP) processes vary across business units, it creates data silos and mismatched payment cycles. These inefficiencies can obscure your overall liquidity picture and make it hard to pinpoint which units are causing cash flow delays. By standardizing AR and AP processes, you eliminate these silos and establish a unified view of cash flows across the organization [8].

The main advantage of standardization is that it addresses inefficiencies in your cash-conversion cycle, freeing up "trapped" cash. Instead of relying on periodic cost-cutting, you can optimize the timing between supplier payments and customer receipts. This approach tackles cash flow issues at their source [9]. Automation is a key piece of the puzzle. Integrating your ERP, treasury systems, and bank accounts through APIs reduces manual errors and minimizes the need for spreadsheet-heavy workflows. In fact, 65% of treasury leaders are expanding these integrations to gain better real-time visibility [8].

Standardized AR and AP processes also make it easier to calculate key metrics like Days Sales Outstanding (DSO) and Days Payable Outstanding (DPO) consistently across all units. When everyone uses the same definitions and data standards, you can compare performance across units and identify where improvements are needed [9]. This unified approach not only releases trapped cash but also creates a foundation for improving DSO and customizing payment terms.

Quicker payment collection means more cash on hand to reinvest or meet obligations in other areas. Even small reductions in DSO can have a big impact. For example, cutting DSO by just five days in a company with $1 billion in revenue could free up around $13.7 million in cash [9].

Automation plays a huge role in reducing DSO. Automated invoicing, for instance, significantly reduces errors - dropping them from nearly 40% to below 0.5% - by using OCR (optical character recognition) and built-in validations [11]. Automated audits ensure invoices are accurate before they're sent, checking for correct purchase order numbers, tax codes, and customer details. This "invoice-right-first-time" approach minimizes rejections and keeps cash flowing smoothly [9].

Another effective strategy is implementing a fixed dunning cadence. This could include a courtesy alert three days before the due date, issuing the invoice on Day 0, an automated reminder on Day 7, and a follow-up phone call on Day 15 [9]. For high-value or high-risk accounts, reserving senior collectors for escalations while using automation for routine reminders can be highly effective.

Self-service portals and one-click payment links also help speed up collections. When customers can easily view and pay invoices online via card or ACH, they're more likely to settle quickly [9]. Take Veeva Systems as an example - they achieved a 75% reduction in bad debt write-offs and cut the number of 90-day aged accounts in half by automating their AR processes. Their team also slashed the time spent on low-priority accounts from 25% of their week to under two hours [12].

While reducing DSO improves cash collection, tailoring payment terms to each unit's specific needs ensures liquidity remains steady.

Customizing payment terms for each business unit's cash flow cycle can help balance liquidity needs without disrupting operations. For instance, units with high inventory turnover may require shorter payment windows, while those with longer sales cycles might need extended terms [9][10].

To enforce consistency, embed default payment terms directly into your ERP system's vendor and customer setup forms. This step prevents procurement teams from entering non-standard terms - like net 30 instead of net 60 - without approval from the CFO [9]. These controls ensure that new relationships align with your standardized framework, reducing the risk of unexpected cash flow issues.

For customers, payment terms can be adjusted based on their risk profiles and payment histories. Strategic customers with strong records might qualify for net 45 terms, while newer or riskier accounts could start with net 30 or even prepayment requirements [9][10]. Including payment term discussions in the onboarding and sales processes sets clear expectations upfront, helping to avoid disputes later [10]. For units handling long-term projects, milestone-based billing can provide steady cash inflows instead of waiting until project completion [10].

It's also a good idea to conduct an annual audit of payment terms. Compare actual delivery cycles with invoice triggers and adjust templates as needed [9][10]. Rising DSO, frequent late payments, or customers pushing for extended terms are all signs that your payment structure might need tweaking [10]. Regularly reviewing these metrics and making adjustments ensures your cash flow stays aligned with the operational realities of each unit.

After standardizing your cash flow processes, the next step is to allocate resources where they deliver the most value. Focus on investing in units that maximize returns. To do this, evaluate each unit's revenue model, capital requirements, and cost structure to make informed capital allocation decisions [14][15].

Start by dividing your organization into Strategic Business Units (SBUs). Each SBU should have a clear economic logic: who it serves, what it offers, and how it generates revenue [14]. For each SBU, create a concise, one-page summary that outlines its revenue model, working capital needs, and key cost drivers. This approach allows for standardized comparisons across units using metrics like Net Present Value (NPV), Internal Rate of Return (IRR), and Return on Invested Capital (ROIC) [15].

For example, a global equipment manufacturer shifted $180 million from low-IRR Industrial Systems rebuilds to CleanTech component lines delivering 17–20% IRR. Over 18 months, CleanTech's share of capital expenditures grew from 28% to 48%, Services' recurring revenue increased by 22%, and the company's overall incremental ROIC improved by roughly 300 basis points [15].

"Corporate strategy becomes practical when you can describe the portfolio as it is, not as you wish it were." - Umbrex Corporate Strategy Playbook [14]

Once you've defined your SBUs, group them by growth stage to fine-tune resource allocation.

Segmenting units based on their growth stage ensures resources are allocated according to each unit's maturity and cash flow characteristics. Here's how to approach it:

Many companies adopt a Run/Grow/Options strategy, starting with a 60/30/10 or 70/20/10 resource split and adjusting as growth units prove their potential [15].

It's also crucial to consider each unit's burn rate and the lag between cash outflows (like hiring or inventory) and cash inflows (like sales). Early-stage units often have higher burn rates and longer delays, requiring additional capital to extend their runway [17][18]. Similarly, units in seasonal industries, such as travel or agriculture, need tailored cash reserve strategies compared to those in more stable sectors [19].

"When you understand your cash flow position, you can make much better decisions. Right now, given the shortage of IPO exits and the macroeconomic headwinds, you need that more than ever." - Oliver Grummitt, Managing Director of Global Treasury & Payments at SVB [17]

Once units are grouped, establish KPIs to ensure resource allocations align with your strategic goals. These KPIs help track whether each group is meeting its financial and operational targets.

NPV should be your primary decision-making metric [15]. Use differentiated hurdle rates that reflect each unit's risk and maturity - early-stage units can have lower initial thresholds but must meet stricter benchmarks as they grow [15]. Introduce "kill rules" with predefined milestones; if a unit fails to meet these, stop or pivot the investment and redirect resources to higher-performing units [15].

Monitor unit-specific metrics like cash conversion cycles, working capital fluctuations, and incremental ROIC. Identifying key drivers - such as pricing, utilization rates, or customer churn - can help fine-tune performance [14]. Real-time dashboards that integrate data from ERP and CRM systems allow you to track all units simultaneously, enabling quicker month-end closes and more agile adjustments [17]. This level of visibility ensures resources are allocated based on current performance and future potential, not just past results.

Streamlining operations and inventory management across your business can unlock significant cash flow. Inefficiencies like idle inventory and redundant processes drain resources. The solution? Shift from fragmented, unit-specific operations to centralized, demand-driven systems. This approach reduces waste and improves liquidity [20][21].

Traditional "push" systems often lead to overproduction and excess stock. Adopting a just-in-time (JIT) approach ensures goods are produced or ordered only when there's confirmed demand, freeing up capital. For example, Nike reduced lead times by 40% and improved productivity by 20% using JIT practices [21]. Harley-Davidson achieved even more dramatic results, cutting total inventory by 75% and significantly reducing warehousing costs [21].

Duplicated functions like accounts payable, payroll, or treasury operations across units inflate costs unnecessarily. Centralizing these activities through Shared Service Centers (SSCs) can streamline processes and save resources. For instance, Liberis automated its treasury functions, saving 1,600 hours annually by replacing manual workflows with a centralized platform in December 2025 [24]. Similarly, Mangopay centralized its financial operations, unlocking €20 million in idle cash and achieving a 6.1× return on investment [24].

"By freeing trapped cash on the balance sheet through working capital improvements, companies can fuel growth, pay down debt, or return capital to shareholders."

- Anthony Jackson, Principal, Deloitte Transactions and Business Analytics LLP [23]

These strategies lay the groundwork for efficient, demand-driven operations across all units.

JIT reduces waste by aligning production and ordering directly with demand. To start, establish a baseline at the SKU level by analyzing purchase orders and forecasts to identify overstock [22]. For example, a global chemicals company optimized its inventory across 130 sites, cutting excess by more than 25% in just three months [22]. Tools like Kanban signals can help trigger reorders only when stock reaches a predefined threshold, keeping inventory lean and efficient [21].

JIT also minimizes defects. Producing in small lots allows errors to be caught early, reducing scrap and rework costs. Motorola leveraged real-time inventory views to reduce its inventory needs by 20% [21]. To make this system work across multiple units, cross-train employees to handle various production tasks as demand shifts. Local sourcing can further reduce lead times and the need for large safety stocks [21].

| Feature | Traditional Inventory (Push) | Just-in-Time Inventory (Pull) |

|---|---|---|

| Inventory Levels | High (Safety stock maintained) | Minimal (Demand-driven) |

| Lot Sizes | Large | Small |

| Waste Risk | High (Obsolescence) | Low (Responsive production) |

| Cash Impact | Tied up in storage | Freed for investments |

| Supplier Role | Transactional | Collaborative |

To ensure success, centralize inventory governance. A Project Management Office (PMO) can track key metrics like ABC/XYZ classifications and safety stocks across all units [22]. Integrating JIT with centralized forecasting sharpens cash visibility and streamlines operations.

Centralizing administrative functions is another effective way to free up cash. Shared Service Centers (SSCs) consolidate tasks like accounts receivable, reconciliation, and payroll into a single structure, eliminating redundancies and improving efficiency [25]. This aligns with the unified operational approach introduced earlier.

For global operations, Regional Treasury Centers (RTCs) can manage liquidity, risks, and banking relationships on a regional level [25]. Taking it further, an In-House Bank (IHB) can act as a central entity for holding balances, enabling self-funding across locations and reducing reliance on external borrowing [25].

"What worked for a $200 million company simply isn't effective in supporting the volume and operational requirements of a $2 billion company."

- Vicky Albovias, Managing Director, Treasury Consulting, J.P. Morgan [25]

Cash pooling is another powerful tool. Physical cash pooling moves funds between units automatically, addressing deficits and eliminating idle cash. Notional pooling offsets debit balances in one unit with credit balances in another without physically transferring funds, reducing foreign exchange costs in global operations [13][24]. Modern API-driven treasury solutions can automate these processes, moving cash as soon as balances cross predefined thresholds [24].

"A pooled setup gives treasury a consolidated view of group liquidity, supporting more accurate forecasting and quicker allocation of funds to where they are needed."

When implementing shared services, take a phased approach. Full centralization requires buy-in from executives and local managers to ensure each step is executed effectively [25]. Choose SSC locations based on factors like cost, skilled labor availability, and time zones [25]. If you’re working with multiple ERP systems, cross-train staff or establish specialized subteams to handle variations [25]. Automating reconciliation with direct ERP-to-bank connectivity eliminates manual uploads and ensures every transfer is recorded instantly [24].

Once you've improved internal processes, bringing in external experts can take your cash flow management to the next level. Handling cash flow across multiple business units often requires specialized knowledge that might not exist in-house. This is where fractional CFO services come in. These professionals provide high-level financial expertise without the cost of a full-time hire. They can handle advanced forecasting, scenario modeling, and system integration, ensuring resources are allocated effectively.

External advisors also help finance teams transition from basic spreadsheets to more sophisticated financial performance platforms. This expertise is critical, especially since cash flow issues account for 82% of business failures [26]. These professionals can identify timing mismatches and adjust billing practices to keep liquidity intact [1].

External experts can refine your cash flow planning by testing multiple scenarios. This involves creating best-case, worst-case, and base-case models to see how different strategies might affect liquidity across business units [1][16]. For example, you might model the effects of extending payment terms to preserve cash or offering early payment discounts to save money. Scenario modeling also helps you evaluate risks tied to new revenue opportunities, such as launching a new product line or acquiring another business.

Take the case of a construction company in 2022. They worked with their accountant to address a three-month cash gap. By shifting from a 25% upfront/75% at completion payment model to a 30% upfront, 40% at midpoint, and 30% at completion structure, they eliminated their cash shortfall and ensured timely payments to subcontractors [1]. Firms like Phoenix Strategy Group specialize in this kind of planning, helping growth-stage companies model cash flow impacts across various units.

Scenario planning is only part of the equation - integrating your financial data with ERP and CRM systems is just as important. Consolidating data from platforms like ERP, CRM, HRIS, and accounting software gives you a real-time, unified view of cash flow across the organization. External experts can help break down data silos by implementing systems that ensure everyone is working with the same accurate information. For businesses with multiple units, this integration provides visibility into cash flow across accounts, currencies, and divisions.

For instance, in 2022, Vivino adopted Tipalti's AP automation platform to centralize operations across its subsidiaries. This system gave them weekly global cash flow insights and improved forecasting accuracy, enabling more strategic planning [2]. Advisors often recommend a phased approach: first, centralize data by linking existing systems, and then automate recurring tasks like accounts payable and receivable. Depending on the complexity of your organization, this process typically takes three to six months. The result? Fewer manual errors and more time for finance teams to focus on strategic planning instead of routine data entry.

Once systems are in place and external expertise is secured, the real work begins: continuous monitoring. Managing cash flow effectively requires regular, ongoing reviews. The difference between businesses that maintain steady liquidity and those that face sudden cash crunches often boils down to how often they assess their financial standing. Waiting for monthly financial statements isn’t enough. As Brian Keyser, Director of CFO Services at Anthem, explains:

"Monthly financial statements arrive too late. By the time you see last month's numbers, you've already made dozens of financial decisions, some good, some not so good." [27]

Weekly reviews, on the other hand, allow you to catch potential problems early. For example, if a client who usually pays within 25 days suddenly stretches payments to 40 days, it’s a red flag that needs immediate attention. Spotting this early gives you time to act before the issue grows. This proactive approach enables smarter decisions - like approving new opportunities or delaying non-essential expenses - based on your actual liquidity. Weekly evaluations, paired with real-time insights, create a system that supports quick, informed adjustments.

Real-time dashboards provide instant visibility into your cash flow across all areas of the business. Tools like Monday Morning Metrics from Phoenix Strategy Group automatically sync financial data, so you’re not relying on outdated spreadsheets. These dashboards should include key metrics like current cash position, accounts receivable aging, upcoming payables, and projected balances. The goal? Spotting problems as soon as they arise.

A well-designed dashboard can also track customer payment trends and flag unnecessary subscription expenses, such as unused SaaS tools or duplicate charges that quietly drain resources. With all this information in one place and updated in real time, finance teams can make faster, more informed decisions. Pair these dashboards with structured weekly reviews to address issues before they escalate.

A weekly cash flow review doesn’t have to take long - 15 minutes is often enough if you stick to a structured routine. Start by comparing your current bank balance to last week’s. Then, review accounts receivable to identify overdue invoices that need immediate follow-up - don’t wait until they’re 60 or 90 days past due. Check accounts payable and payroll to see if any optional expenses can be postponed without harming vendor relationships. Finally, calculate your projected ending balance: Current Balance + Expected Deposits - Known Expenses [27].

If this projection shows less than two weeks of operating expenses, you’ve entered what Keyser calls the "danger zone":

"If your projected balance drops below 2 weeks of operating expenses, you're entering the danger zone. Take action now, not next week." [27]

End each weekly review with a clear corrective action that can be completed within 48-72 hours. This keeps adjustments manageable and prevents small issues from snowballing. Schedule these reviews at the same time every week - Monday mornings or Friday afternoons work well - to make them a consistent habit. Coordinate with your bookkeeper or accountant to ensure all necessary data (like AR aging, bank balances, and upcoming bills) is ready in advance. This disciplined approach keeps cash flow steady and helps avoid major disruptions.

Maintaining steady cash flow across multiple business units takes consistent effort and a solid strategy to ensure liquidity. The core steps - centralized forecasting, streamlined processes, resource allocation tied to unit economics, efficient operations, and real-time monitoring - work together to create a system that supports reliable cash flow and enables quick, informed decisions.

Cash flow challenges are a leading reason many small businesses shut down each year[28]. Companies relying only on monthly financial statements often lack the timely data needed to make effective decisions. By adopting integrated platforms with automated data updates and real-time insights, businesses can catch potential issues early and address them before they escalate into serious problems.

For growth-stage businesses, managing cash flow complexity across units requires more than basic accounting practices. Experts at Phoenix Strategy Group specialize in implementing systems that provide leadership with real-time financial visibility. Their solutions, including tools like Monday Morning Metrics, help businesses automate financial data syncing, optimize liquidity, run cash flow scenarios, and make smart allocation decisions without the need for full-time financial executives.

Take a moment to evaluate your current cash flow processes. Are you reviewing financial data weekly, or waiting until month-end reports? Do you have real-time insight into committed spending across all units? Can you easily pinpoint which units are delivering the best returns on investment? If you notice gaps, consider seeking expert guidance to establish systems that ensure smooth cash flow. The right investments in these processes can extend your company's financial runway, improve decision-making, and support long-term growth.

To build a 13-week cash flow forecast for multiple units, begin by structuring it in a weekly format that spans the next 13 weeks. Collect both actual and projected cash flow data for each unit, breaking it down into estimated inflows (like sales or payments received) and outflows (such as operating expenses or vendor payments). Create a model to track these figures consistently.

Make it a habit to update and review the forecast regularly. This allows you to spot potential liquidity gaps or surpluses early, which can help with smarter resource allocation and more effective planning across your business units.

To keep cash flow under control across different business units, it's crucial to focus on specific metrics. Start with Operating Cash Flow (OCF) - this helps determine whether a unit can support itself financially. Then there's Free Cash Flow (FCF), which indicates how much cash is available for growth opportunities or paying down debt.

Additionally, keep an eye on the Operating Cash Flow Ratio, which measures liquidity, and the Cash Burn Rate, showing how quickly cash reserves are being used. Lastly, the Working Capital Ratio is essential; aim for a range between 1.2 and 2.0 to maintain a healthy balance. Consistently monitoring these numbers helps ensure financial stability and keeps the business on track for growth.

A shared services center can centralize key functions such as treasury, payments, and cash management, streamlining operations and making better use of resources. For companies, especially those with global operations, an in-house bank serves as a powerful tool to handle intercompany transactions, enhance liquidity management, and consolidate cash across different countries. Both approaches offer improved oversight, cost savings, and stronger cash flow control - choosing the right one depends on how centralized and complex your company's operations are.