Published on

April 17, 2026

FinTech M&A deals are complex, and compliance challenges can make or break them. From regulatory scrutiny to data privacy laws, navigating these hurdles is critical for ensuring a smooth transaction. Here are the top compliance challenges you need to know:

Key takeaway: Compliance issues aren't just a pre-closing concern - they can lead to long-term penalties, reputational damage, and lost partnerships if not addressed. Early due diligence and robust compliance frameworks are essential for success in FinTech M&A.

Top 5 Compliance Challenges in FinTech M&A Transactions

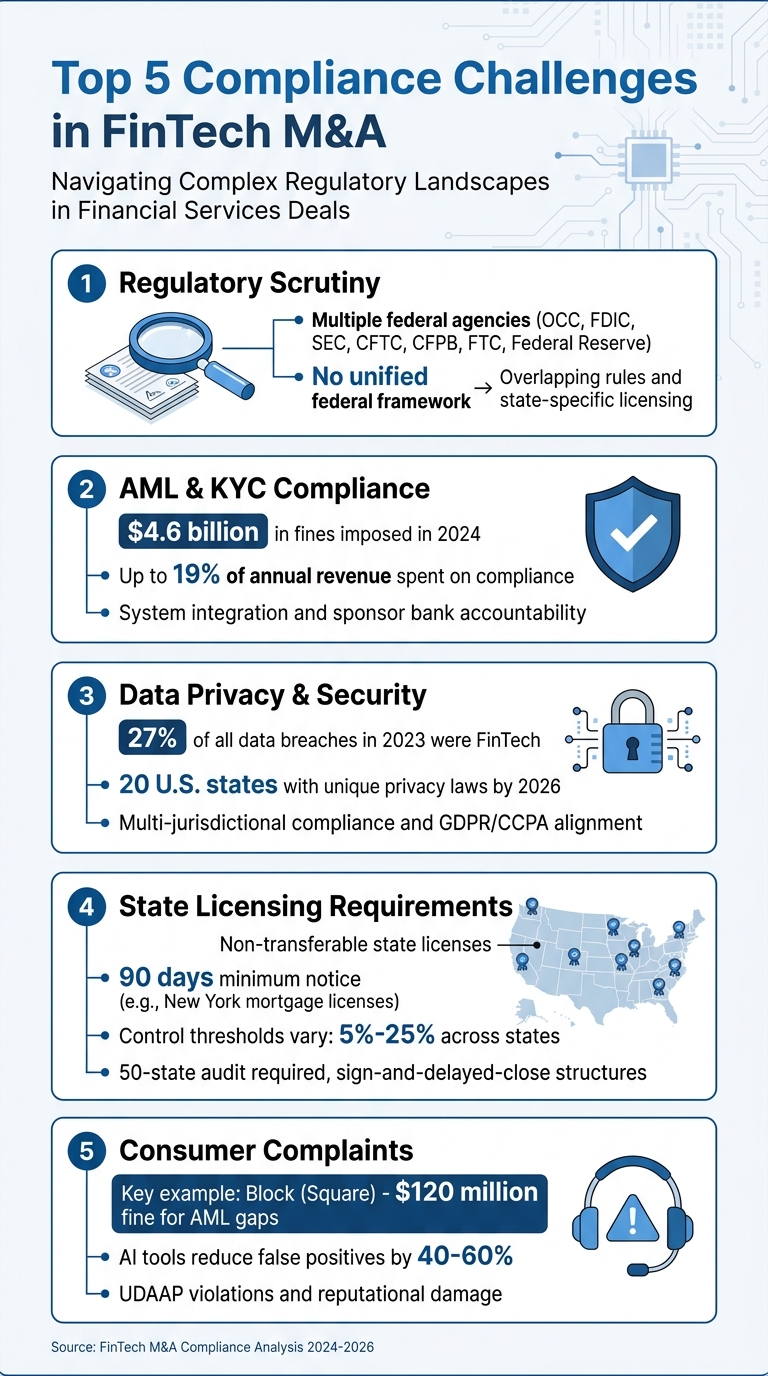

FinTech mergers and acquisitions (M&A) come under the watchful eye of a mix of federal and state regulators, creating a complicated landscape for companies involved. Federal agencies like the OCC, FDIC, SEC, CFTC, CFPB, FTC, and the Federal Reserve all play a role in the approval process, each with its own timelines and standards [3]. This fragmented approach means FinTech companies often face overlapping and sometimes conflicting regulatory demands.

Adding to the complexity, there's no unified federal framework for these transactions. For example, the uncertainty about whether digital assets are classified as securities or commodities can lead to valuation disagreements during negotiations. To address these gaps, dealmakers often use strategies like earn-out provisions or deferred payments tied to regulatory milestones, such as securing an SEC no-action letter [1][2].

And just when you think federal oversight is challenging enough, state-level regulations pile on even more hurdles.

State regulations introduce another layer of difficulty. By 2026, 20 U.S. states are expected to have comprehensive consumer data privacy laws, each with its own nuances. This lack of standardization forces acquirers to conduct thorough due diligence to ensure compliance across multiple jurisdictions [1].

To simplify things, some FinTech companies seek national bank charters through the OCC. A notable example is Varo Money, which, in July 2017, became the first mobile-only FinTech to apply for a full national bank charter with both the OCC and FDIC. This move not only streamlined its regulatory obligations but also provided FDIC insurance [3]. Keith Noreika, Acting Comptroller of the Currency at the time, highlighted the importance of such initiatives:

"The proposal to grant special purpose national bank charters to fintech companies is a good idea that deserves the thorough analysis and the careful consideration [OCC is] giving it" [3].

These varying federal and state requirements underscore the importance of having strong contractual frameworks to manage risks effectively.

In Banking-as-a-Service (BaaS) arrangements, sponsor banks are held accountable for the actions of their FinTech partners [1]. This added scrutiny means acquirers must carefully review contracts to ensure clear guidelines for areas like customer identity verification, transaction monitoring, and regulatory reporting. Without these accountability structures in place, both the acquiring company and its banking partners could face enforcement actions that might jeopardize the merger’s strategic goals.

Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance is one of the costliest and most closely watched aspects of FinTech mergers and acquisitions (M&A). In 2024, regulators imposed fines totaling over $4.6 billion on financial institutions, with compliance expenses consuming up to 19% of annual revenue for some companies [6]. This is particularly critical in Banking-as-a-Service (BaaS) setups, where sponsor banks bear direct responsibility for the compliance lapses of their FinTech partners. Any failure in areas like identity verification or transaction monitoring can lead to enforcement actions [1]. These regulatory pressures make system integration a significant operational hurdle.

M&A success hinges on the smooth integration of AML and KYC systems. Mohit Kansal, VP of Product Management at Flywire, emphasizes:

"Fintechs will not be successful if they don't pay attention to regulation and figure out how to make regulation work in their favor" [4].

This means compliance must be embedded into the core technology stack. Automated transaction monitoring systems, which flag suspicious patterns like unusual transaction volumes or rapid fund transfers, are essential. AI-driven tools have proven their value, detecting two to four times more suspicious activities compared to manual methods, while cutting false positives by 40% to 60% [4]. To overcome these challenges, acquirers must establish clear frameworks for accountability.

Clear accountability between acquirers and banking partners is crucial during consolidation. This requires detailed agreements that specify responsibilities for identity verification, transaction monitoring, and regulatory reporting. Regular compliance reviews - conducted monthly with banking partners - help identify and mitigate emerging risks before they escalate into regulatory issues [1]. Keeping detailed audit logs of every transaction and customer interaction is equally important. These records demonstrate exactly who accessed data and what actions were taken, which is invaluable during regulatory audits [1].

A modular compliance framework is often the key to successful integration. By connecting KYC, transaction monitoring, and reporting systems, firms can quickly adapt to new regulations or expand into new markets without overhauling their entire compliance infrastructure [4][6]. Early investments in RegTech platforms also streamline operations by automating repetitive tasks like transaction screening and risk scoring, freeing up teams to focus on higher-level strategies [1].

Data privacy and security have become a top concern in FinTech mergers and acquisitions (M&A). In 2023, the FinTech sector was responsible for 27% of all reported data breaches, outpacing even the healthcare industry [5]. This alarming trend has led regulators to tighten their grip. Laws like the Gramm-Leach-Bliley Act (GLBA) and various state-level privacy regulations now require FinTech companies to disclose how they share data and to protect sensitive information, such as Social Security numbers and banking details [5][7]. With states introducing stricter consumer privacy standards, companies involved in mergers must navigate a maze of regulations early in the process [1].

Additionally, the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) enforce UDAAP (Unfair, Deceptive, or Abusive Acts or Practices) standards to ensure consumer trust isn’t exploited during acquisitions [5]. Sponsor banks are also held accountable for their FinTech partners’ actions. This approach helps safeguard the financial system from potential risks tied to poor data practices or liabilities [1][3][7].

The fallout from data breaches can be both financially and reputationally devastating. A stark example occurred in 2021 when hackers exploited Revolut's systems, resulting in losses exceeding $20 million [5]. To avoid such outcomes, acquirers must prioritize detailed data due diligence. This involves examining the target company's compliance history, data usage policies, and relationships with third-party vendors to identify any hidden vulnerabilities [1].

Securing specialized insurance coverage has become a common practice to manage risks. Policies such as Cyber Liability, Directors & Officers (D&O), and Errors & Omissions (E&O) can help offset the financial burden of post-acquisition breaches or lawsuits [5]. Beyond insurance, companies are encouraged to adopt modular infrastructure systems. These allow for privacy features to be adjusted based on varying state regulations. Automated tools for consent management can also simplify tracking user preferences and processing data access requests, creating clear audit trails for regulatory scrutiny [1].

Effective integration of data privacy systems across merged entities is critical to maintaining security and compliance. Many companies now use modular compliance frameworks to streamline processes like data reporting, access controls, and encryption across different jurisdictions [6]. As Built In aptly puts it:

"Treating [compliance] as something to bolt on later is like trying to build the foundation of a house after you've already moved in." [6]

For international mergers, the challenges grow even more complex. Companies must reconcile conflicting regulations, such as the EU's GDPR and U.S. federal and state laws [7]. This foundational work is especially crucial for firms adapting to global standards like GDPR. FinTech companies handling digital assets face additional scrutiny under FATF guidelines, which require transparency around transaction originators and beneficiaries [7].

To ensure a smooth integration, clear data governance policies should be established. These policies should define who can access specific information, set data retention timelines, and outline security protocols. Such measures are essential for aligning privacy practices across the entire organization during and after the merger.

State licensing adds a layer of complexity to the already challenging regulatory landscape in FinTech mergers and acquisitions. One of the biggest hurdles? State licenses are non-transferable. This means deals often rely on securities or interest acquisitions to maintain these licenses [8]. As a result, acquirers must navigate a maze of state-specific regulations.

Here's where it gets tricky: states have varying definitions of what constitutes a "change of control." While most states set the threshold at 10%, others go as low as 5%, and some allow up to 25% [8]. Mike Whalen, a Partner at Goodwin, highlights the impact of this variation:

"The one that's the long pole to closing and can cause delays: license change of control approvals by state regulators" [8].

States typically follow one of five approaches for regulatory oversight: requiring prior approval before closing, advance notice only, advance notice with discretionary approval, post-closing notice, or post-closing notice with discretionary approval [8]. These differences can lead to significant delays, making proactive planning essential.

Approval timelines are a major deal risk. Standard change of control approvals usually take 30–60 days, but some licenses - like those for mortgage lenders - can take even longer [8]. For example, New York mandates a minimum of 90 days' prior notice for changes to mortgage banker licenses [8]. Since many states don't allow deals to close while waiting for prior approvals, transactions often need to be structured as "sign and delayed close" agreements, with regulatory approval as a condition for closing [8].

To address these delays, acquirers should perform a 50-state audit during due diligence. This involves creating a detailed chart that evaluates how new ownership will affect each state license [8]. Additionally, savvy negotiators include a "critical mass" clause in purchase agreements. This clause allows the deal to close once approvals are secured from states that account for a significant portion of the company's revenue, minimizing the impact of delays from smaller jurisdictions [8].

The filing process for state licensing is exhaustive. States often require full license applications, updated NMLS forms, organizational charts, and personal disclosures, including fingerprints and financial histories for all new directors and individual owners [8]. To stay on track, it's crucial to maintain weekly updates on filing statuses, communications with regulators, and projected approval timelines [8].

In distressed M&A scenarios, the process becomes even more complicated. Regulators tend to take longer to approve changes and scrutinize the target company's ability to meet net worth and surety bond requirements more rigorously [8]. If a particular state's approval is significantly delayed, parties may opt to surrender that license rather than hold up the entire transaction [8].

Unresolved consumer complaints can be a red flag for potential UDAAP (Unfair, Deceptive, or Abusive Acts or Practices) violations, drawing the attention of regulators like the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC). These agencies, established in the wake of the 2008 financial crisis, work to ensure institutions uphold consumer trust [5]. A high volume of complaints often signals compliance issues that could derail an M&A deal before it even closes.

Recent enforcement actions highlight the financial and operational risks of compliance failures. For example, Block (formerly Square) faced a $120 million fine and was required to overhaul its anti-money laundering (AML) procedures after compliance gaps emerged during its rapid growth [4]. Such cases show how liability can shift to the acquiring company, making UDAAP due diligence a critical step in the M&A process.

Given the regulatory scrutiny, managing consumer complaints proactively is crucial. Like other compliance hurdles in FinTech M&A, consumer complaint risks demand meticulous due diligence and ongoing oversight. Failures in consumer protection can harm the target company's reputation and disrupt key Banking-as-a-Service (BaaS) partnerships. Sponsor banks are increasingly held accountable for the actions of their FinTech partners, adding another layer of risk [1]. Systemic issues, such as frequent technical outages or software bugs that block customer access to funds, often lead to litigation and regulatory penalties that ultimately impact the acquirer [5].

To mitigate these risks, acquirers should carefully examine the target company's complaint history and regulatory track record during due diligence. Leveraging RegTech platforms to automate complaint tracking and resolution can help maintain regulatory compliance and improve the company’s appeal to potential buyers [4].

The integration phase often reveals weaknesses in how consumer complaints are handled, especially if systems are fragmented. A unified approach that ties complaint management to Know Your Customer (KYC) and transaction monitoring systems is essential. This ensures that the company can handle increased transaction volumes without attracting regulatory scrutiny [6].

AI-powered monitoring tools can play a significant role in improving the consumer experience during M&A transitions. For instance, these tools can reduce false positives - such as unnecessary account freezes - by 40% to 60%, addressing a common source of complaints [4]. Embedding compliance into core systems from the start not only ensures scalability but also strengthens the overall compliance framework. This is an area where expert financial advisors can provide critical guidance, helping to align complaint management with broader M&A objectives.

Financial advisors play a key role in navigating the complex regulatory landscape of FinTech mergers and acquisitions (M&A). During due diligence, they conduct in-depth compliance audits, reviewing areas like regulatory history, risk management practices, banking relationships, and tools for automated identity verification and anti-money laundering (AML) compliance [1][5].

To ensure smooth integration, advisors use enforcement data and cost benchmarks to structure contracts that clearly define compliance responsibilities. These contracts specify accountability for tasks like identity verification, transaction monitoring, and regulatory reporting. This clarity helps prevent disputes and keeps all parties aligned throughout the M&A process [1].

Another critical area of focus is data privacy and cybersecurity. With data breaches being a significant risk in the FinTech sector, advisors evaluate data usage practices and cybersecurity measures to ensure they align with global regulations such as GDPR, CCPA, and the Gramm-Leach-Bliley Act (GLBA). They also assess incident response plans and the adequacy of regular data backups to minimize vulnerabilities [5].

An example of this advisory expertise comes from Phoenix Strategy Group, which specializes in helping growth-stage FinTech companies prepare for exits. Their approach includes designing modular compliance systems that can scale across jurisdictions without requiring a complete overhaul. By embedding compliance into tech infrastructures and customer onboarding processes - rather than treating it as an afterthought - they help companies manage increasing transaction volumes while avoiding regulatory pitfalls [4][6]. This proactive strategy also lays the groundwork for automating compliance processes.

Advisors further support companies by introducing AI-driven compliance automation. These tools can significantly improve efficiency, reducing false positives in transaction monitoring by 40% to 60% [4]. By embedding automation and controls into their systems, FinTech companies can transform regulatory requirements into strategic advantages, using compliance as a lever for competitive growth.

Regulatory compliance stands as the biggest challenge in FinTech M&A heading into 2026. Overlooking requirements like the EU AI Act or AML compliance can jeopardize both deal valuation and closure. The EU AI Act, fully enforceable from August 2, 2026, carries steep penalties - up to 7% of a company’s global annual turnover [9].

Thorough compliance due diligence plays a crucial role in determining deal success. Addressing regulatory gaps early can prevent "integration shock", which happens when outdated systems fail to align with modern standards post-transaction [9]. As Plausity highlights:

"Regulatory compliance, particularly the EU AI Act and AMLA oversight, represents the most significant risk to deal closure and valuation" [9].

Adding to this, 97% of CIOs report that technology due diligence often reveals issues or opportunities that significantly influence deals [10]. Multi-jurisdictional reviews and pre-closing cost assessments help refine enterprise value and avoid unexpected hurdles.

The insights gained during due diligence also inform a focused action plan. A well-structured 100-day post-closing plan prioritizes critical risks - like GDPR compliance or AML readiness - ensuring these are tackled immediately. This proactive strategy not only accelerates synergy realization but also keeps companies aligned with regulatory standards across regions. For deal professionals, quickly acting on compliance findings can become a competitive edge [9].

Ultimately, success in FinTech M&A requires more than just financial expertise - it demands a firm grasp of the regulatory landscape. With careful preparation and expert guidance, companies can turn compliance challenges into strategic opportunities. For those seeking to navigate these complexities, Phoenix Strategy Group offers specialized advisory services to help maximize M&A success.

Compliance due diligence in a FinTech acquisition needs to tackle a range of regulatory risks. This includes ensuring compliance with laws like GDPR and DORA, meeting AML/KYC standards, and verifying licensing requirements. It’s also essential to evaluate data privacy and security measures to ensure they align with legal and operational expectations.

Another critical focus is the assessment of legacy systems and data migration processes. These areas play a significant role in ensuring a seamless integration and maintaining compliance after the acquisition is complete. Neglecting these factors can lead to operational disruptions and regulatory challenges down the line.

State licensing approvals often slow down the closing of FinTech mergers and acquisitions. This is because regulatory reviews and approvals can take time. For example, securing or transferring Money Transmitter Licenses or other state-specific permits usually demands a lot of documentation and thorough scrutiny. These steps can stretch timelines and delay the finalization of the deal.

To integrate AML/KYC and privacy controls efficiently after a deal closes, leverage automated tools and modular compliance frameworks to simplify workflows. Centralizing data management not only enhances risk analysis but also speeds up onboarding processes. Additionally, seeking expert advice helps ensure compliance with regulatory standards. Together, these approaches reduce manual effort, minimize delays, and support a seamless transition while maintaining ongoing regulatory compliance.