Published on

July 5, 2026

If I had to boil this down to one line: core pays you sooner, opportunistic may pay you more later. The tradeoff is simple: as you move from core to core-plus, value-add, and opportunistic, cash flow gets less steady, leverage often climbs, and the deal needs more work to go right.

If I’m looking at CRE, I’d sort the four types like this:

For a growth-stage company, this is not just a property choice. It affects:

The main idea: if your business needs steady liquidity, core or core-plus will usually fit better. If you can handle cash flow dips, lease-up risk, renovation risk, or even no early income, value-add or opportunistic may offer more upside.

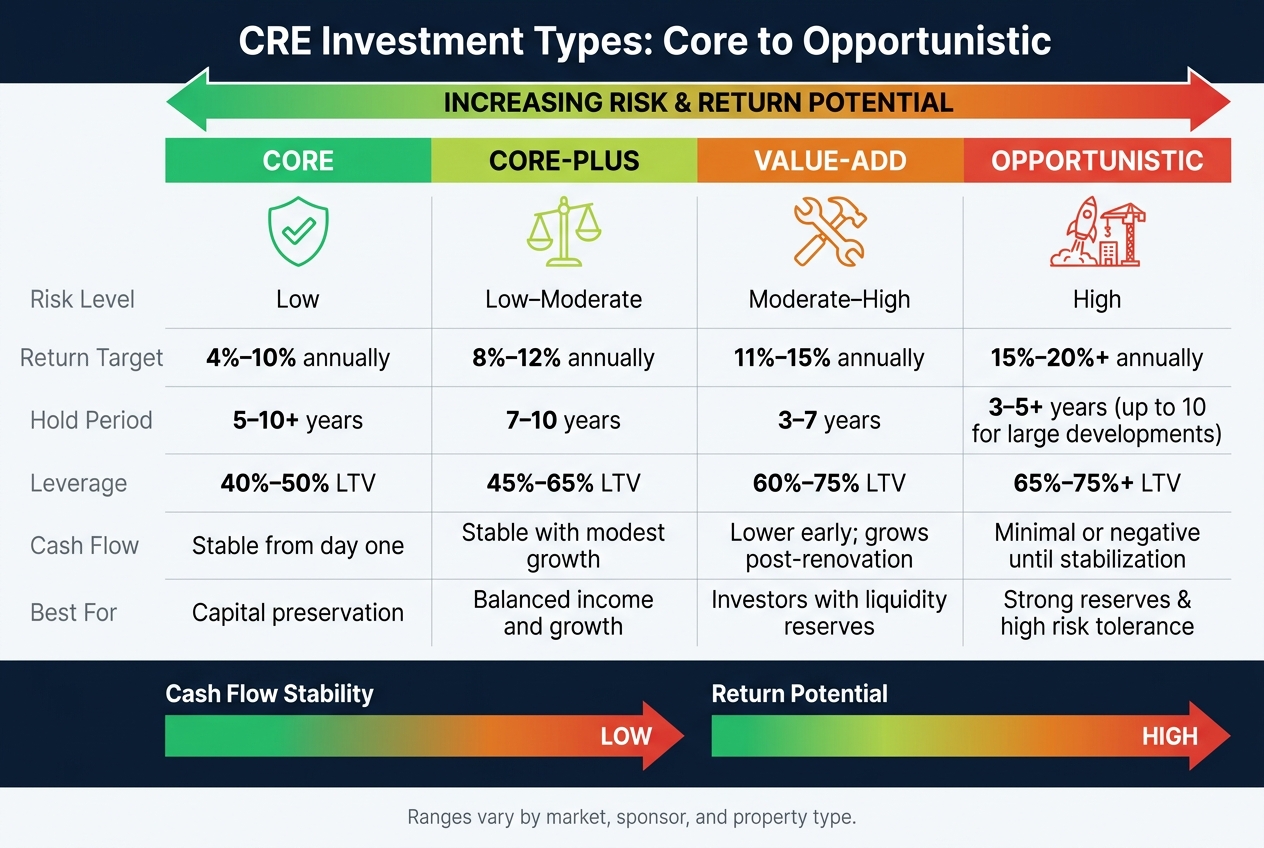

CRE Investment Types: Core to Opportunistic Risk-Return Spectrum

| Type | Risk | Return Target | Cash Flow | Leverage | Best Fit |

|---|---|---|---|---|---|

| Core | Low | 4%–10% | Stable from day one | Lower | Income and capital preservation |

| Core-Plus | Low to medium | 8%–12% | Mostly stable | Medium | Income with some growth |

| Value-Add | Medium to high | 11%–15% | Often weaker early | Higher | Buyers with reserves and time |

| Opportunistic | High | 15%–20%+ | Often thin or negative early | Highest | Buyers with strong reserves and high risk tolerance |

My quick read: the best choice is the one your balance sheet can carry without putting stress on payroll, growth spend, or debt service.

Core CRE is stabilized, high-quality property built for predictable income with very little hands-on management. These are usually Class A assets in major U.S. markets like New York City, Chicago, Los Angeles, and Boston. They’re fully leased, or close to it, and meant to generate steady cash flow [1][4][7].

Core is about protecting capital and producing stable income, not chasing price growth. Annual total returns usually fall in the 4% to 10% range, with most of that return coming from rent [4][9].

Core deals are long-term holds, often 5 to 10+ years. Think of them as portfolio anchors: stable assets that don’t need much day-to-day attention [1][2][4].

Core properties are often leased to investment-grade tenants on long leases. Triple-net (NNN) leases are common, and terms can last 10, 20, or even 30 years [5][8].

For example, a Walgreens on a 30-year lease fits the core profile [3].

Leverage is usually conservative, at about 40% to 50% of property value [3][4]. Lower debt can help shield equity when markets soften and supports cash flow from day one. For growth-stage operators, core can help preserve liquidity and keep distributions stable without adding much management work [2][3].

Core-plus keeps much of this stability, but takes on some lease or property issues in exchange for more yield.

Core-plus is an income-plus-growth strategy. It carries a bit more risk than core and usually involves stable, well-occupied assets that need small fixes, lease rollovers, or sit in a less prime location. Put simply, it lands in the middle between fully stabilized core assets and more active value-add deals.

The risk profile here is low to moderate. Investors aren't buying a distressed property or taking on a major renovation. They're making focused improvements to an asset that already has a solid base.

That extra work can lead to annual returns in the 8% to 12% range [4][5].

Hold periods are usually long enough to finish light upgrades, renew leases, and sell at a better price [1][2][4].

Tenants are usually solid, but the property may have near-term lease expirations or some minor vacancy. That creates room to strengthen the tenant mix through active lease management and light cosmetic work.

Those changes can help bring in better tenants and support rent growth without the heavier execution risk that comes with a full repositioning [4][3].

Leverage is moderately higher than core, usually in the 45% to 65% LTV range [4][3]. That added debt can help pay for smaller improvements and improve returns, but it also makes the deal more sensitive to interest rate moves and refinancing conditions [5][1].

Cash flow is usually stable, with some modest variation tied to vacancies and lease renewals [8]. For operating companies, that can mean some upside without giving up baseline liquidity.

For growth-stage investors, core-plus offers current income with some upside while avoiding the heavier work that comes with value-add. Value-add starts when light improvements turn into a more active repositioning.

Where core-plus deals rely on light upgrades, value-add is a different animal. This is active repositioning.

You're buying a property that already brings in some income, but it's not doing its job well. Maybe vacancy is high. Maybe rents are below market. Maybe maintenance has been pushed off for too long. The plan is to lift NOI through focused upgrades and stronger leasing. The upside comes from execution, not from buying something already steady.

Risk sits in the moderate-to-high range because the return depends on getting the work done right. Renovation, leasing, and day-to-day operations either go well or they don't.

Target IRRs usually fall between 11% and 15% [10][4]. Those returns are generally driven by a mix of income growth and price gain at exit.

Most value-add deals last 3 to 7 years [10][11].

That time usually covers the full arc of the business plan:

Value-add properties are often Class B or C properties [12][13]. They may come with high vacancy, below-market rents, or weak operations.

The idea is simple: improve the property enough to bring in better tenants who are willing to pay higher rents. That's where the upside lives. But there's a catch. Stable distributions can take time because the property often needs work before it can perform the way the sponsor wants.

Leverage usually lands between 60% and 75% LTV [10][7]. That can push returns higher, but it also makes the deal more sensitive to interest rates.

Cash flow is usually there at acquisition, but it can drop during renovations [1][8]. As the property stabilizes, cash flow may improve. That gap matters. Operators in this stage need enough reserves to carry the property through the dip.

Opportunistic strategies take this one step further, with even more uncertainty and a larger possible upside.

Opportunistic takes the value-add playbook and pushes it much further. This is where you see ground-up development, major redevelopments, and distressed turnarounds. And unlike value-add, the property usually needs a major overhaul before it can produce much income.

This is the highest-risk part of the spectrum. A deal can hinge on entitlements, construction, financing, and plain old market timing. If one piece slips, the whole plan can get thrown off.

Target annual returns usually land in the 15% to 20%+ range [3][6][4]. In this bucket, returns depend less on lease-up alone and more on getting approvals, finishing construction, and hitting the market at the right time.

Most opportunistic deals last 3 to 5 years. Large development projects can stretch to 7 to 10+ years [3][14].

That’s why many opportunistic assets begin as vacant buildings, underused properties, or raw land [2][7]. The plan is to turn them into stable, income-producing assets and bring in strong tenants once the business plan is in place.

Leverage often falls around 65% to 75%+ LTV [3][7]. That debt is often short-term bridge financing instead of long-term stabilized loans.

Early cash flow is often thin or even negative. So these deals tend to fit investors or operators with a long time horizon and the ability to carry out a complicated plan.

As you move from Core to Opportunistic, current income tends to drop, leverage goes up, and execution risk gets heavier. Put simply: the more upside you chase, the more moving parts you have to manage. The table below shows how risk, return, hold time, and cash flow shift across the spectrum. Ranges vary by market, sponsor, and property type.

| Strategy | Risk Level | Target Return Range (Annual %) | Typical Hold Period (Years) | Tenant Profile | Leverage Range | Cash Flow Pattern | Fit for Growth-Stage Investors |

|---|---|---|---|---|---|---|---|

| Core | Low | 4%–10% | 5–10+ | Credit tenants, long-term leases | 40%–50% | Stable from day one | Best for capital preservation |

| Core-Plus | Low–Moderate | 8%–12% | 7–10 | High-quality assets with some near-term renewals | 45%–65% | Stable with modest growth | Best for balanced income and growth |

| Value-Add | Moderate–High | 11%–15% | 3–7 | Transitional; higher vacancy or below-market rents | 60%–75% | Lower early; grows post-renovation | Requires liquidity reserves |

| Opportunistic | High | 15%–20%+ | 3–5+ | Vacant, distressed, or pre-development | 65%–75%+ | Minimal or negative until stabilization | Only for strong reserves and high risk tolerance |

For growth-stage firms, the main question is simple: can the business handle delayed cash flow?

The move from Core-Plus to Value-Add is not just a bump in return. It changes the day-to-day demands of the deal. Floating-rate or short-term bridge debt becomes more common, which means interest rate swings can hit much harder [1][7]. Reserves also need to do more work. They have to cover normal operating costs, renovation overruns, longer vacancy, and possible lease-up delays [1][6].

Opportunistic deals add even more uncertainty. Underwriting has to price in variables that do not yet exist, like future rent premiums, exit cap rates years down the road, and construction timelines that almost never go exactly to plan. These deals also use heavier leverage, so delays, rate moves, and pricing misses can eat into returns fast. One example is the April 2026 Natiivo Fort Lauderdale project, where investors reportedly lost about $22 million in raised capital before construction began [1].

For growth-stage companies looking at value-add or opportunistic deals, tighter modeling, KPI tracking, and cash-flow forecasting become much more important; Phoenix Strategy Group can support that work.

Every CRE strategy gives you a different trade-off between steady performance and upside. Core sits on the safe end. Core-Plus adds some growth. Value-Add can produce stronger gains, but only if the plan works. Opportunistic aims for the biggest payoff and brings the biggest risk.

For growth-stage buyers, the big question is simple: How much cash flow volatility can the business handle?

It also helps to avoid a common mistake. Risk is not set by asset type alone. The business plan plays a huge role. In Value-Add and Opportunistic deals, results often come down to how well the operator executes.

The table below turns that risk-return range into a quick side-by-side view of what each strategy gives up and what it may deliver.

| Strategy | Main Pros | Main Cons | Best For | Key Watchouts |

|---|---|---|---|---|

| Core | Predictable income; lowest risk; highly passive | Low upside; sensitive to interest rate shifts | Capital preservation; conservative investors | Macroeconomic cycles; inflation eroding low yields |

| Core-Plus | Balanced income and growth; moderate risk; higher yield than Core | More active management than Core; minor maintenance needs | Investors seeking modest upside with stability | Near-term lease rollovers; secondary market volatility |

| Value-Add | Meaningful appreciation through forced NOI growth | Execution risk; early cash flow dips during renovation | Growth-oriented investors with operational expertise or a strong sponsor | Construction cost overruns; leasing velocity; sponsor experience |

| Opportunistic | Highest potential returns (20%+) [3][4] | No early cash flow; high leverage; real risk of capital loss | Aggressive investors with long time horizons and strong reserves | Market timing at exit; entitlement and zoning delays; high leverage exposure |

One point stands out here: Core is driven by income, while Opportunistic leans mostly on appreciation at exit. That difference matters a lot if the business needs cash before a sale or refinance.

That’s why liquidity planning becomes a major issue before moving into Value-Add or Opportunistic deals.

The table shows the range. Now comes the part that matters: picking the option your balance sheet can actually handle.

The right CRE strategy is the one your balance sheet can support. That means matching the deal to your liquidity, leverage tolerance, and hold period. For growth-stage companies, the goal is pretty simple: protect operating cash while still putting capital to work.

If your business relies on steady distributions to help fund growth, Core or Core-Plus is usually the more workable fit. These strategies tend to suit companies that need stable income. Value-Add makes more sense for businesses with stronger reserves and a 3–7 year horizon. Opportunistic fits only investors that can live with little or no cash flow before exit.

That’s the gut check. Can the deal sit alongside payroll, growth spending, and refinancing needs without creating strain? If not, the upside on paper may not matter much.

And when a deal needs more hands-on management, underwriting discipline starts to matter even more.

Higher-risk strategies don’t just ask for more capital. They ask for tighter planning before you commit.

Execution risk sits at the center of value-add performance, and a lot depends on the sponsor and the operating team. Before moving into a Value-Add or Opportunistic deal, stress-test the underwriting across three variables: construction costs, leasing velocity, and exit cap rates [1][6]. A miss in any one of those areas can cut into returns fast.

Growth-stage companies also need to prepare for capital calls, or extra equity requests during the project [1]. That part can sneak up on teams that are already using cash to hire, invest in sales, or extend runway.

This is where integrated financial planning helps. It gives teams a way to pressure-test tradeoffs before capital goes out the door. Companies with stronger forecasting and scenario planning are in a better spot to judge whether a deal fits day-to-day operating needs. Phoenix Strategy Group provides fractional CFO services, FP&A, cash flow forecasting, and integrated financial modeling that can help growth-stage companies evaluate whether a high-risk CRE deal fits their current operating reality.

The best CRE strategy is the one that fits your capital structure and operating capacity. Core leans toward stable income and lower execution risk. Opportunistic leans toward exit-driven upside and comes with the most risk. Value-Add and Core-Plus land somewhere in the middle.

The choice comes down to liquidity, debt capacity, operating bandwidth, and how much delay your business can absorb.

For steady, predictable cash flow, Core real estate is usually the best fit. These properties are stabilized, fully occupied, and leased to high-credit tenants under long-term agreements.

If you want a mix of income and moderate growth, Core-Plus may be a better match. Value-Add and Opportunistic strategies lean more toward long-term appreciation, so cash flow is often lower, delayed, or not there at all during the hold period.

Value-add and opportunistic deals need a lot more cash than the purchase price alone. You also have to pay for renovations, repositioning, or even ground-up construction.

That’s where things get more demanding. These deals often don’t come with steady cash flow, and opportunistic projects may bring in no income at all for months or even years.

So investors need deep liquidity to carry the project through rough patches. That includes covering delays, handling cost overruns, and getting by with little or no income until the property stabilizes and starts to gain value.

The biggest risks move away from small day-to-day gains and toward execution and repositioning risk. Value-add deals often use more leverage and need hands-on management to deal with deferred maintenance, occupancy problems, or weak prior management.

Because these assets aren’t operating at full potential, returns hinge on carrying out a clear plan to increase net operating income. If that plan comes up short, the downside is steeper because the property doesn’t have the stable income cushion that core-plus assets usually provide.