Published on

June 24, 2026

Most bad investment timing comes from one mistake: spending like it’s still a boom when your numbers already say it’s not.

I’d sum the playbook up like this: match hiring, capex, software spend, and market entry to the cycle phase you’re in. Expansions usually last much longer than downturns - post-WWII U.S. expansions averaged 64.2 months, while contractions averaged 10.3 months - but that doesn’t mean I should ignore slowdown signals. It means I should watch for them early and change spending before cash gets tight.

Here’s the short version:

I’d make the phase call with a mix of macro signals and company data, such as:

A simple budget rule also stands out: aim for 18–24 months of runway. If I drop below 12 months, I’d treat that as a warning sign. From there, I’d fund work in this order: protect core revenue, preserve cash, improve efficiency, then make selective growth bets.

If I had to reduce the whole article to one line, it would be this: don’t spend based on hope; spend based on signals.

Investment Strategy by Economic Cycle Phase: Hiring, Capex & Market Entry

Use your own operating data to figure out where the business sits in the cycle before you change spending. Macro data gives you the backdrop. Your operating data tells you when those conditions are hitting your business.

Track PMI and CFNAI to understand the macro picture, but use internal signals to confirm what’s happening on the ground. The ISM PMI reads above 50 during expansion and below 50 during contraction [8][6]. The CFNAI pulls from 85 monthly indicators: above +0.5 points to strong growth, 0 to -0.7 points to slowing, and below -0.7 points to recession conditions [8].

Your internal signals are usually faster and more specific. These are the ones to watch:

Don’t hang everything on one number. Look for a pattern. If close rates are falling, sales cycles are getting longer, and customers are stretching payment terms, that’s hard to brush off.

Use this monthly or quarterly. The table below helps turn raw signals into a phase call.

| Signal | Expansion | Peak/Slowdown | Recession | Recovery |

|---|---|---|---|---|

| ISM PMI | Above 50, rising | Above 50, flattening | Below 50 | Crossing back above 50 |

| CFNAI | Above 0, rising | 0 to -0.7 | Below -0.7 | Rising from below -0.7 |

| Yield curve | Steepening (positive) | Flattening | Inverted | Normalizing |

| Pipeline conversion | High and improving | Declining | Low and falling | Stabilizing |

| Sales cycle length | Shortening | Lengthening | Extended | Beginning to shorten |

| Churn rate | Low or falling | Ticking up | Elevated | Stabilizing |

| Customer payables | On terms (30 days) | Stretching (45–60 days) | Extended (60–90+ days) | Returning to terms |

| Talent availability | Scarce, expensive | Loosening slightly | Readily available | Competitive again |

If most of your signals fall into the same column, you’ve got a usable phase call. If the picture is mixed - say, a strong pipeline but rising churn - you’re probably in a transition period. That usually calls for caution, not a push on spending.

The goal isn’t to label the phase with perfect precision. It’s to classify it well enough to make the next spending decision. Then use that phase call to time hiring, capex, software, and market entry.

Your phase call should shape where each dollar goes: people first, then capacity, then software, then market entry. In plain English, set headcount before you add fixed costs, and deal with fixed costs before you make growth bets.

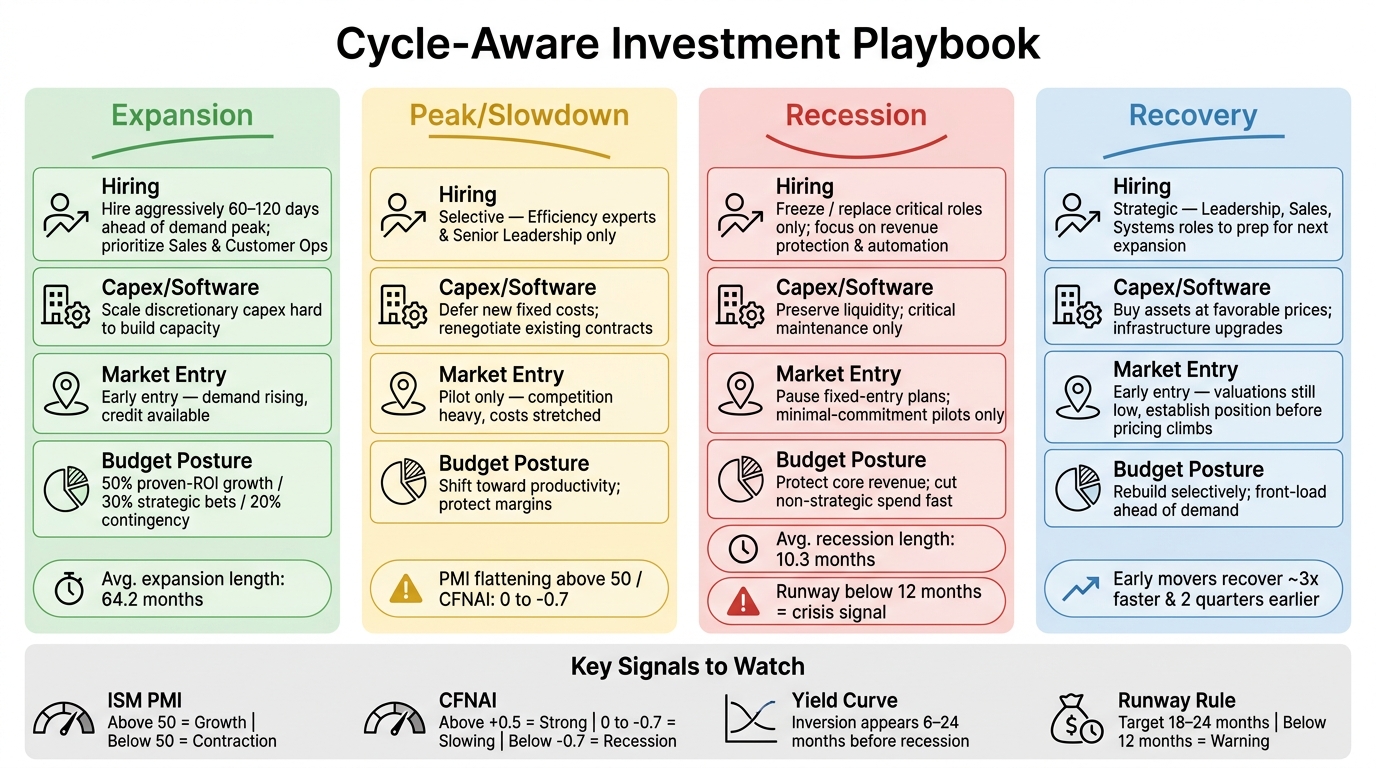

Hire before demand tops out. Bringing people in 60 to 120 days ahead of a workload peak helps keep operations steady. If you wait until demand is already spiking, bottlenecks show up fast [1][2].

Timing matters, but role type matters just as much. In expansion, put revenue-producing roles first, especially sales and customer-facing operations. At peak/slowdown, shift toward efficiency experts and senior leadership who can protect margins before conditions get tighter [2]. In a slowdown, only hire when the role cuts costs, supports automation, or covers a must-have function. In recovery, bring in fractional CFO leadership and systems roles so the business is set up for the next expansion [2].

| Cycle Phase | Hiring Intent | Highest-Priority Role Types |

|---|---|---|

| Expansion | Accelerate | Revenue-producing (Sales), Customer-facing Ops |

| Peak/Slowdown | Selective | Efficiency experts, Senior Leadership |

| Recession | Freeze / replace critical roles only | Revenue protection, cash control, automation |

| Recovery | Strategic | Leadership, Sales, Systems Professionalization |

Once staffing is locked in, use that same phase-based approach for capex and software.

Buy late-cycle, then put assets to work just before demand comes back.

Late-cycle conditions usually favor buyers. Suppliers are clearing backlogs, lead times get shorter, and pricing is more open to negotiation [3]. That makes slowdown periods a good time to buy equipment or lock in software contracts at better rates, then deploy those assets before demand returns.

In expansion, scale discretionary capex hard to build capacity [1][2]. At peak/slowdown, hold off on anything that doesn't fix an immediate bottleneck. Adding fixed costs near the top of the cycle can squeeze margins once conditions soften [2][3]. In recovery, focus on infrastructure upgrades that reduce friction and get the business ready for the next growth phase [5].

| Cycle Phase | Capex Action |

|---|---|

| Expansion | Scale aggressively to build capacity |

| Peak/Slowdown | Defer; avoid new fixed costs |

| Recession | Preserve liquidity; critical maintenance only, no new fixed costs |

| Recovery | Strategic upgrades ahead of demand; modernize to remove friction |

The same idea applies to software. In a slowdown or recession, cut low-use subscriptions and renegotiate what stays.

The same timing rule also carries over to market entry.

For expansion bets, timing can matter just as much as fit.

Expansion phases tend to favor early entry. Demand is moving up, credit is available, and getting in early gives you room to build position before competitors pile in [5][2]. Peak/slowdown periods call for restraint because competition is heavy and costs are already stretched [5]. In slowdowns and recessions, stick to minimal-commitment pilots and watch for openings where competitors are pulling back [10]. Recovery can also open a strong entry window: valuations are still relatively low, and early movers can establish position before pricing climbs [5].

| Cycle Phase | Entry Action |

|---|---|

| Expansion | Early entry |

| Peak/Slowdown | Pilot only |

| Recession | Pause fixed-entry plans; minimal-commitment pilots only |

| Recovery | Early entry |

Once you've mapped hiring, capex, and market entry by cycle phase, the next job is sequencing. When cash is tight and leadership attention is stretched, you can't fund everything at once. So what goes first?

The order is simple: protect core revenue first, preserve liquidity second, fund efficiency third, and expand selectively last. Aim for 18–24 months of runway. If you're below 12 months, treat that as a crisis signal [12].

Before approving any major efficiency or growth spend, put it through a simple filter: does it remove a current bottleneck, improve measurable productivity, and still make sense if revenue doubles? [2] If the answer is shaky, the spend probably is too.

Selective growth should come last, and it needs to earn that spot. That means there must be evidence-backed payback within 18 months and a competitive window that is starting to close [12].

Once the sequence is clear, use it to decide how much cash goes into each bucket. The split should follow risk, not department lines.

A simple starting point is 50/30/20:

Those shares shouldn't stay fixed. They move with the cycle.

After sequencing priorities, split remaining cash by risk, not by department.

| Cycle Phase | Primary Focus | Budget Posture |

|---|---|---|

| Expansion | Growth & Scale | Weighted toward proven-ROI growth; maintain Rule of 40 discipline [6][11] |

| Slowdown | Efficiency & Liquidity | Shift toward productivity; protect margins [3][4] |

| Recession | Survival & Retention | Protect core revenue; cut non-strategic spend [4][6] |

| Recovery | Careful Re-acceleration | Rebuild selectively; front-load ahead of demand [1][3] |

Use this table as a budget map, not as a way to reclassify the phase you're in. That call has already been made.

A practical way to force cleaner decisions is to sort every activity into three buckets:

That structure helps keep emotion out of the room. It also makes faster action easier when conditions change.

The payoff is hard to ignore. Companies that cut costs before revenue drops recover about 3x faster and get back to growth around two quarters earlier than companies that wait and react [12].

Once the budget mix is set, the next issue is where fractional CFO services help speed up the call.

Once spending priorities are set, the next step is deciding when to fund them. That’s where a dashboard matters. Cycle-aware planning only works if you can see ahead. Strong operators handle capital planning the same way they handle inventory planning: they forecast needs before constraints show up[1].

The core toolkit is pretty simple. You need a rolling cash flow model that shows gaps caused by delayed receivables or upfront project costs, a KPI dashboard that tracks leading indicators like demand, capacity, and constraints, and three scenario plans - best case, base case, and downside - that get updated as the cycle shifts[1][13].

For capital decisions, four finance-market indicators deserve their own view:

Each one helps signal whether it makes sense to accelerate, defer, or protect cash[13].

Use the dashboard to refresh the plan every month, or sooner if the signals move. Scenario planning helps turn cycle signals into faster decisions when conditions change. Keep a base-case plan tied to current cycle signals. Then keep a downside version that clearly separates projects that can attract outside funding from projects that need internal bridge capital[13].

There’s a point where the dashboard and forecast stop lining up with the calls you need to make. When that happens, outside finance support can fill the gap. The clearest sign is simple: your current finance systems can’t keep up with the pace or level of decision-making. More specifically, that shows up when finance reporting no longer supports hiring, capex, or funding decisions, or when an expansion decision calls for complex financial modeling[2][3].

Fractional CFO services, FP&A support, and data engineering help founders move faster on hiring freezes, capex deferrals, renegotiations, and expansion approvals. The goal is better financial visibility before revenue scales, so decisions stay proactive[2]. Phoenix Strategy Group supports that work with bookkeeping, fractional CFO, FP&A, data engineering, and M&A support for growth-stage companies that need clearer financial visibility.

Every major investment decision - hiring, capex, software, market entry - gets better when you tie it to a clear cycle phase. The playbook is simple: build capacity before demand peaks, protect cash before downturns get worse, cut low-value spend fast, and ramp back up with care during recovery. The order matters just as much as the calls themselves.

Once the phase is clear, turn it into a spending sequence: hire, invest, enter, or wait. Timing can turn an ordinary investment into an edge.

Phase - not instinct - should drive the next spend.

Use this as the monthly filter for every major spending call.

| Cycle Phase | Priority Move |

|---|---|

| Expansion | Hire aggressively; enter new markets |

| Peak/Slowdown | Shift to efficiency; prioritize productivity software and renegotiate contracts |

| Recession | Preserve cash; cut low-value spend fast |

| Recovery | Upgrade key talent; buy assets at favorable prices |

The core discipline is simple: every spending decision should link to a measurable return and a clear signal. Not a forecast. A signal. When leading indicators weaken, move from growth to cash preservation. Act before the financial results confirm what the leading indicators already showed you.

Read the signals, match the phase, then spend to fit the moment.

Reassess it on a regular basis by tracking leading indicators, which often signal shifts 6 to 12 months before they show up in broader economic data.

Instead of trying to call the exact peak or bottom, use a rolling forecast and review capital needs and market positioning 60 to 120 days ahead. Think of cycle analysis as active oversight, not a once-a-year exercise.

Prioritize internal evidence over broad economic headlines. Look at margins and the actual payback from the past 12 to 18 months, not forecasts. If revenue is stable and demand is outpacing capacity, investment may still make sense even in a sluggish macro environment.

If payback is inconsistent or you're entering untested segments, stay conservative with cash and rebalance spending. Match capital deployment to your business phase instead of reacting to macro volatility.

Start with discretionary spending that won’t hurt revenue much. That usually means things like duplicate software licenses, tools hardly anyone uses, and perks or benefits with no clear payoff.

Before you cut anything, sort each expense by two things: lead time and revenue impact. That gives you a simple way to see what can go now, what needs more planning, and what you should leave alone.

From there, trim variable costs such as:

Skip blanket cuts across every team. They may look neat on paper, but they often do more harm than good. Protect customer-facing work and the investments that help bring in revenue.