Published on

December 27, 2025

Understanding how equity compensation is taxed across borders is critical for employees and companies alike. Different countries have varying rules for stock options, RSUs, and restricted stock, creating complexities, especially for employees who work in multiple jurisdictions during the vesting period. Here's a quick breakdown:

For employees, tracking workdays and meeting deadlines (e.g., filing a Section 83(b) election within 30 days) is essential. For companies, aligning equity plans with international tax rules ensures compliance and avoids unexpected costs.

In the U.S., the timing of taxation for equity compensation depends on the type of equity instrument. For restricted stock, taxes are triggered in the first year it becomes transferable or is no longer subject to risk. RSUs (restricted stock units) are taxed at settlement, while non-qualified stock options are taxed at the time of exercise.

If you file a Section 83(b) election within 30 days of receiving restricted stock, you can shift the tax event to the grant date. Mary Van Leuven, Director at KPMG LLP, explains:

A Sec. 83(b) election may be made to shift the U.S. federal income tax point from vesting to transfer so that appreciation in value following the initial transfer is capital gain [3].

This election only applies to restricted stock - not RSUs - and can allow you to treat future growth as capital gains rather than ordinary income. These rules set the stage for how equity compensation is taxed, as further clarified in the sections on income characterization and sourcing rules.

When equity vests or stock options are exercised, the IRS treats the value at that moment as ordinary income. The taxable amount equals the fair market value of the stock at the time, minus any amount you paid for it. Any increase in value after this point is treated as a capital gain when you sell the shares. For 2023, ordinary income was subject to Social Security tax up to a wage base of $160,200 [2].

How equity compensation is taxed depends on your residency status. U.S. citizens and green card holders are taxed on their worldwide income, meaning all equity income is subject to U.S. taxes, no matter where the work occurred. Non-residents, however, are taxed only on the U.S.-source portion of their income. Galia Antebi and Nina Krauthamer from Ruchelman PLLC elaborate:

Typically, the source of multiyear compensation is apportioned between the U.S. and a foreign country based on the relative days worked in each place [1].

This means dividing your U.S. workdays by the total workdays during the vesting period to determine what portion of your income is taxable in the U.S.

For U.S. taxpayers working abroad, Foreign Tax Credits can help offset U.S. taxes on income earned in other countries. However, mismatches in tax timing - like when one country taxes equity at grant while the U.S. taxes it at vesting - can complicate these calculations. If you’ve worked in multiple countries, keeping detailed records of your workdays is crucial for accurately calculating the U.S.-source portion of your income.

Canada handles equity taxation differently, with distinct timing rules depending on the type of equity compensation. Stock options are taxed at the time of exercise. The taxable benefit is calculated as the difference between the stock's fair market value and the exercise price [7][10].

For RSUs, taxation kicks in upon vesting and share delivery [10]. However, Canada's Salary Deferral Arrangement (SDA) rules can trigger taxation earlier. To avoid being taxed at the time of grant, RSUs must be settled by December 31 of the third year following the service year. This timing rule is often referred to as the "Three Year Bonus Exception", a term coined by Pamela L. Cross, Partner at BLG [7].

Restricted stock faces the toughest tax treatment in Canada. It is taxed immediately upon issuance, regardless of whether you might forfeit the shares later. If you do lose the shares, you typically cannot claim a deduction for the taxes already paid. Because of this, restricted stock is rarely offered to Canadian employees [7].

In Canada, all forms of equity compensation are treated as employment income (ordinary income) [7][10]. However, stock options get some preferential treatment. If the exercise price is at least equal to the fair market value at the time of grant and the shares meet "prescribed share" conditions, you can claim a 50% deduction on the taxable benefit [7][10].

Starting July 1, 2021, this deduction is capped at $200,000 annually, based on the fair market value of the shares at the time of grant. Exceptions apply to certain startups and Canadian-controlled private corporations [7]. When shares acquired through equity plans are eventually sold, any profit is classified as a capital gain, and only 50% of the gain is taxable [10].

Canada also uses a unique approach to allocate income across borders for employees who work in multiple jurisdictions. For RSUs, Canada applies a Hybrid Methodology to determine how income is sourced [8][9]. The value at grant (the "in-the-money" portion) is allocated to the jurisdiction where you worked during the grant year. Any increase in value from grant to vesting is sourced based on the number of workdays in each country during the vesting period. The ITM portion at the time of grant reflects past services and is attributed to the jurisdiction where employment services were performed in the grant year [8].

For stock options, Canada adheres to OECD principles. The benefit is apportioned based on where you worked during the vesting period, requiring careful tracking of workdays across jurisdictions. This differs from the U.S. approach and can make cross-border taxation more complex [8].

Canadian residents can offset taxes paid to other countries by claiming foreign tax credits under subsection 126 of the Income Tax Act [8][9]. Canada’s bilateral tax treaties, such as the Canada-U.S. Convention, provide additional relief by assigning primary taxing rights based on specific criteria, including the 183-day rule [8][11].

However, the portion of your equity benefit sourced to Canada using the Hybrid Methodology may not always align with what is taxable in Canada under the Income Tax Act. This can impact your foreign tax credit calculations [8]. Tax treaties play a crucial role in determining which jurisdiction holds the primary taxing authority, based on your work location during both the grant and vesting periods.

European countries approach equity taxation in ways that differ from North America, often involving multiple stages: grant, vesting, exercise, and sale [14]. Generally, stock options are taxed at the time of exercise, while RSUs are taxed at vesting when the shares are delivered. The grant itself usually doesn’t trigger taxation unless the option has immediate value [14].

One key concept here is accrual. Income is considered earned over the time between the grant date and the vesting date [4]. This accrual period plays a crucial role in determining tax obligations, especially for employees who move between countries during this time. For instance, if you receive an equity grant while working in Germany but relocate to France before vesting, both countries may claim a portion of the tax based on your work history during the accrual period. This framework directly impacts how income is classified, as explained below.

In most European countries, stock options and restricted shares are taxed as employment income at the time of exercise or vesting [4]. This means they are subject to progressive income tax rates, which in France can go as high as 45%. After vesting, dividends are taxed separately as investment income, often with different withholding rates [15].

France also offers an incentive program called BSPCE (Bons de souscription de parts de créateur d'entreprise) for eligible equity plans [14]. If your plan meets specific conditions under the French Commercial Code - such as minimum vesting and holding periods - you could qualify for more favorable tax treatment compared to standard plans, which are taxed like regular salary.

When employees work across multiple European countries during the vesting period, tax obligations are divided proportionally based on workdays spent in each jurisdiction. For example:

"The stock option benefit is sourced based on workdays between grant and vesting." - PwC Germany [16]

If you worked 500 days in Germany and 300 days in the UK during the grant-to-vest period, Germany would claim 62.5% of the taxable benefit, while the UK would claim 37.5%. Accurate tracking of workdays is essential for compliance.

Germany, for instance, exempts portions of stock option income that weren’t earned while working there. If you weren’t employed in Germany during part of the grant-to-vest period, that portion of the income may be fully exempt from German taxes. Typically, the "source country" (where the work was performed) withholds taxes first, while the "residence country" (where you live) taxes worldwide income [14]. These rules are designed to help manage double taxation, as discussed below.

To avoid taxing the same equity income twice, European countries rely on bilateral double tax treaties (DTTs), often based on OECD models [12][14]. Relief mechanisms include either a tax credit in your residence country for taxes paid abroad or an exemption for foreign-sourced income.

"The residence country takes into account the taxes paid in other countries to avoid double taxation. The division of taxing rights is often agreed upon in bilateral agreements between countries, so-called double tax treaties." - Elo Madiste, Global Tax Expert, Salto X [14]

To take advantage of reduced withholding tax rates under these treaties, you’ll need a certificate of residency from your home country’s tax authorities, which must be submitted to the source country [15]. For example, the Germany-UK tax treaty lowers Germany’s standard dividend withholding rate from 26.375% to 15% for UK residents [15]. However, the process for reclaiming withheld taxes can be challenging - statistics show that over 83% of investors fail to successfully reclaim taxes withheld in another EU Member State, often resulting in effective double taxation [13].

India's approach to taxing equity compensation aligns with global practices, emphasizing both the timing of taxable events and the employee's work location. RSUs are taxed at the time of vesting, while ESOPs and ESPPs are taxed when exercised [17][18][20]. The fair market value (FMV) at vesting or exercise, minus any employee contribution, is treated as salary income (classified as a perquisite). When the shares are sold, any increase in value from the vesting or exercise date is taxed as capital gains. Dividends from these shares are categorized as income from other sources and taxed based on the employee's applicable income tax slab rate [17][18].

For shares of foreign companies not listed on Indian exchanges, a valuation must be obtained from a SEBI-registered Category 1 merchant banker. This valuation must be performed either on the vesting date or within 180 days before that date [17][19]. The tax treatment for capital gains depends on how long the shares are held. Shares held for over 24 months are considered long-term and taxed at a flat 20% rate with indexation benefits. Shares held for 24 months or less are taxed at the individual's applicable slab rates. Employers are responsible for tax withholding (TDS) at the time of vesting or exercise, but employees must independently pay advance tax on dividends and capital gains [17][18].

This system highlights the importance of accurately allocating service periods for cross-border equity benefits.

Taxation in India is heavily influenced by an individual's residency status. Residents are taxed on their worldwide income, meaning foreign-earned equity is taxable even if the services were performed outside India [17]. Non-residents and those with Resident but Not Ordinarily Resident (RNOR) status are taxed only on the portion of income tied to services rendered in India. For instance, if an employee worked in India for 200 days out of a total 500-day grant-to-vest period, approximately 40% of the vesting benefit would be taxable in India. However, for non-residents, proceeds from selling foreign shares are not taxable unless the funds are deposited directly into an Indian bank account [17].

India has measures in place to address double taxation. The Foreign Tax Credit (FTC), as outlined in Section 90 of the Income Tax Act and relevant Double Taxation Avoidance Agreements (DTAA), allows taxpayers to claim relief. The credit is limited to the lower of the tax payable in India or the actual tax paid abroad. To claim this credit, Form 67 must be filed before the tax return deadline. For example, under the India-U.S. DTAA, dividends from U.S. corporations may be subject to a 25% federal tax in the United States, which can then be credited against Indian tax liabilities. Indian residents are also required to disclose all foreign assets, such as vested RSUs and foreign brokerage accounts, in Schedule FA of their tax return. Notably, this disclosure follows the calendar year (January to December), differing from India’s financial year [17][18][21].

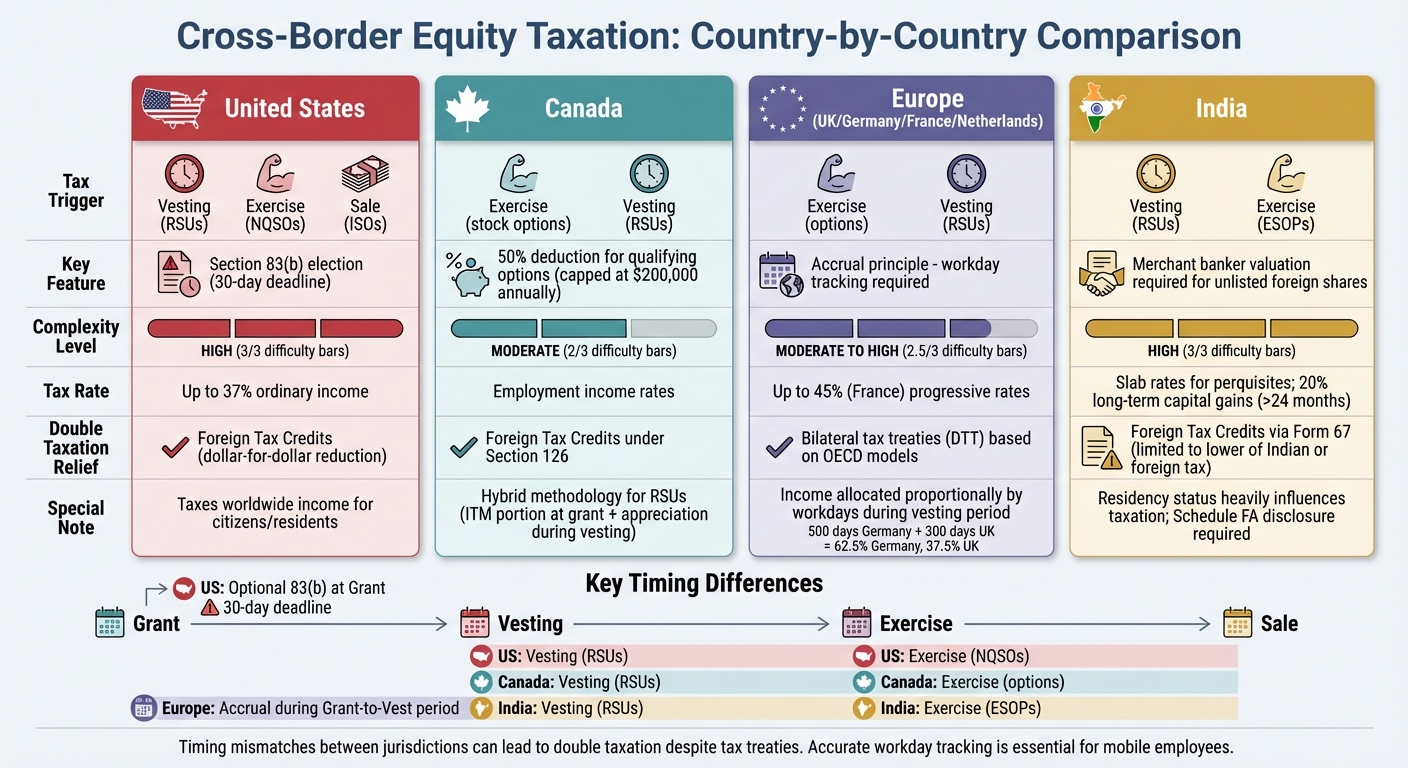

Cross-Border Equity Taxation Comparison by Country

Building on the country-specific rules outlined earlier, this section compares how different nations handle cross-border equity taxation. The timing of taxation, administrative processes, and overall complexity vary significantly from one country to another.

In the United States, a notable feature is the Section 83(b) election, which allows employees to choose taxation at the time of grant instead of vesting. This option, however, must be exercised within 30 days of the grant date. Missing this deadline means future gains are taxed at higher ordinary income rates, which can climb to 37%.

Canada simplifies things by taxing stock options at the time of exercise and treating the resulting benefit as employment income. For qualifying options, a 50% deduction is available, reducing the tax burden. On the other hand, many European countries, including the UK, Germany, France, and the Netherlands, use the accrual principle. Under this approach, taxing rights are split based on the number of workdays an employee spends in each country during the vesting period. While this ensures proportional taxation, it adds complexity for mobile workers who must carefully track their workdays across borders [4].

India takes a different approach, taxing equity awards at vesting for RSUs and at exercise for ESOPs. For unlisted foreign shares, valuations by merchant bankers are often required. Residency status also plays a significant role in how taxes are calculated. Timing mismatches between jurisdictions - where one country taxes at grant and another at exercise or sale - can lead to double taxation despite tax treaties. As Vistra notes:

The goal is to eliminate double taxation where possible - this includes the possible double taxation of stock options. [6]

Here’s a quick look at the differences across regions:

| Country/Region | Tax Trigger | Complexity | Double Taxation Relief |

|---|---|---|---|

| United States | Vesting (RSUs), Exercise (NQSOs), Sale (ISOs) | High – 83(b) elections, 409A compliance, AMT concerns | Foreign Tax Credits (dollar-for-dollar reduction) [22] |

| Canada | Exercise | Moderate – 50% deduction for qualifying options | Foreign Tax Credits and treaty provisions |

| European (UK/Germany/France/Netherlands) | Accrual during vesting | Moderate to High – workday tracking required | Treaty-based apportionment and sourcing rules [4] |

| India | Vesting (RSUs), Exercise (ESOPs) | High – merchant banker valuations, residency rules | Foreign Tax Credits via Form 67 and DTAA provisions |

The effectiveness of double taxation relief varies widely. For example, the U.S. Foreign Tax Credit directly reduces tax liability dollar-for-dollar - so a $200 credit fully offsets $200 in taxes. By contrast, a $200 deduction for someone in a 25% tax bracket only lowers the tax bill by $50 [22]. In Europe, under the accrual principle, if an employee worked in Finland for 90 days out of a 730-day vesting period, only that proportion of the equity benefit would be taxed in Finland [4]. India’s system requires filing Form 67 before the tax return deadline, and relief is limited to the lower of Indian tax or the foreign tax paid, which can leave gaps when foreign tax rates are lower.

For both employers and employees, tracking workdays, income classifications, and withholding obligations across jurisdictions is critical. Maintaining detailed records of where services are performed during each vesting period is particularly important. Missing deadlines, such as the 30-day window for filing a Section 83(b) election, can turn potential capital gains into ordinary income, with tax rates as high as 37% [3][6]. This comparison underscores the importance of meticulous record-keeping and informed planning for cross-border equity plans.

Navigating cross-border equity taxation is no small feat, especially for mobile employees and growth-stage companies. Every country has its own approach to taxing equity compensation. For instance, in the U.S., RSUs are taxed at vesting, while in Israel, share awards are taxed at the time of sale. Meanwhile, many European countries calculate income based on the number of workdays during the vesting period[6][23]. These differences can lead to timing mismatches, double taxation, and unexpected liabilities, even when tax treaties are in place. This makes careful cross-border planning an absolute must.

For international employees, meeting deadlines is non-negotiable. Filing a Section 83(b) election, for example, must happen within 30 days of the grant date[1][3]. Similarly, failing to comply with Section 409A can result in immediate penalties. Keeping an accurate record of workdays is just as essential, especially as audits become more frequent and detailed. Companies need to integrate mobility tracking with payroll systems and maintain thorough records of where employees work during each vesting period. This not only ensures proper tax withholding but also provides a defense in case of audits.

As highlighted by GTN:

US-based equity compensation plans may not have consistent tax treatment in other countries. These differences can create risk and unforeseen tax consequences that, in extreme cases, can result in the equity income becoming a disincentive, rather than an incentive, to the employee. [23]

Given the varied tax treatments across jurisdictions, companies must take a proactive approach. Growth-stage businesses expanding internationally should carefully review their equity plans to identify potential Section 409A conflicts, address local securities laws, and decide whether a U.S. addendum or localized plan is necessary[24][5].

The complexities of equity taxation require expertise and thoughtful planning. Phoenix Strategy Group offers support tailored to growth-stage companies, providing fractional CFO services and strategic advisory solutions. Whether you're preparing for funding rounds, expanding globally, or planning an exit, working closely with tax advisors, mobility specialists, and payroll administrators can help ensure compliance and shield both the company and its employees from costly pitfalls.

To steer clear of double taxation on equity compensation in cross-border situations, employees need to tackle a few key steps. Start by figuring out where the income is sourced and understanding your tax residency in each country involved. In the U.S., income is typically taxed based on where the work is done. However, other countries might also tax the same income, which can create a double taxation issue. To address this, map out the periods you worked in each jurisdiction and check if any tax treaties apply. For example, U.S. treaties with countries like Canada or those in Europe often provide options such as foreign tax credits or exemptions to offset taxes paid overseas.

Timing plays a crucial role in managing tax exposure. Aligning the vesting, exercise, or sale of equity awards with tax-friendly periods can make a big difference. For instance, exercising stock options after a change in residency or deferring taxes by opting for stock options instead of RSUs could significantly lower your tax bill. It’s also essential to ensure proper withholdings are made in each jurisdiction and to maintain detailed records of any foreign taxes paid.

Getting advice from a cross-border tax specialist early on can make the process much smoother. Professionals, such as those at Phoenix Strategy Group, can help structure equity awards, apply treaty benefits, and ensure compliance with both U.S. and foreign tax rules, reducing the risk of double taxation.

Equity compensation in the U.S. and Canada comes with notable differences in how it's taxed, particularly in terms of timing and treatment.

In the U.S., restricted stock awards and restricted stock units (RSUs) are taxed as ordinary income when they vest, with payroll taxes also applying at that point. If the shares are later sold, any additional gains are taxed as capital gains, and a lower rate may apply if the shares are held for more than a year. For stock options, taxes are based on the difference between the exercise price and the fair market value (FMV) at the time of exercise, with further gains taxed as capital gains upon sale. The Section 83(b) election offers an option to pay income tax at the time of grant rather than at vesting, but employees must file this election within 30 days of receiving the award.

In Canada, employees must report the FMV of vested shares or the stock option spread as taxable income when the shares vest or the option is exercised. This income is taxed at the employee’s marginal federal and provincial rates, but unlike in the U.S., it isn’t subject to payroll tax withholding. Canada also does not provide an equivalent to the Section 83(b) election, meaning taxation is strictly tied to vesting or exercise.

For employees working across borders, the U.S.–Canada Income Tax Convention helps avoid double taxation by allocating taxing rights and permitting foreign tax credits. However, the rules and timing of equity compensation taxation remain distinct between the two countries, making it essential for both international employees and employers to carefully navigate these differences.

In Europe, determining taxes on equity vesting for employees working across multiple countries hinges on two key factors: tax residency and bilateral tax treaties. Generally, employees are taxed on their worldwide income in the country where they are considered tax residents. For instance, if someone is a tax resident of Germany, they must declare income from foreign employers on their tax return. However, thanks to international agreements, they may qualify for tax relief to prevent double taxation.

In practice, the country where the work is physically performed often imposes withholding taxes on the income. At the same time, the employee must report this income in their country of residence. Bilateral tax treaties play a crucial role here - they allocate taxing rights between countries, ensuring that employees aren’t taxed twice on the same income. The employee’s final tax obligation typically factors in any withholding taxes paid abroad, with adjustments or credits applied in their home country based on treaty provisions.